George Athanassakos of UWO makes an interesting point about the Taylor Rule:

Since the markets have spoken, what is the Fed waiting for? Why is the Fed not raising its effective interest rate yet? According to the well-known Taylor rule, which stipulates by how much nominal interest rates should change in response to a change in inflation and economic activity, the interest rate set by the Fed should have stood by now at about 2 per cent as opposed to almost zero per cent – not because of a rise in inflation but simply because of a pickup in economic activity.

Now if economic activity also results in a pickup of inflationary expectations, then an even higher normalized nominal federal-funds interest rate should be called for. This seems to have been coming into focus recently given that the iShares Long U.S Treasury Bond prices (which were up on a year-over-year basis) are now down by over 3 per cent since May, 2015, while the iShares U.S. TIPS Bond Index is down only by about 1.5 per cent over the same period.

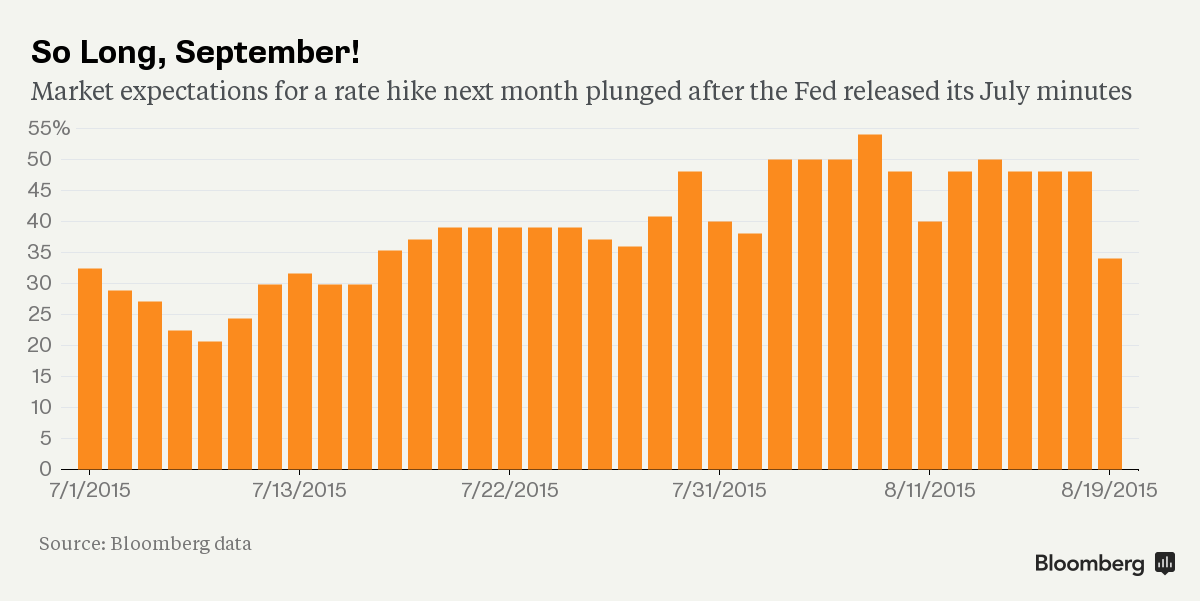

The loonie has problems. Wait a minute, you think the loonie has problems?

Kazakhstan’s tenge plunged a record 23 percent after the country relinquished control of its exchange rate, becoming the latest emerging market to abandon efforts to prop up its currency after China devalued the yuan.

The nation has switched to a free float and will pursue an inflation-targeting monetary policy, Prime Minister Karim Massimov told a government meeting in Astana. Supply and demand will determine the exchange rate, central bank Governor Kairat Kelimbetov said, adding that there will only be intervention if stability is threatened. The tenge sank to an all-time low of 257.21 per dollar in Almaty, data compiled by Bloomberg show.

…

Russia let the ruble float freely and switched to inflation targeting in November after spending about $90 billion last year from reserves trying to contain the depreciation.The ruble has lost 46 percent of its value in the past 12 months, versus a 7.6 percent weakening for the tenge before today’s switch. As a result, Kazakhstan witnessed an influx of grain, metals, construction materials, oil products and coal from its northern neighbor, according to Kazakh business association Atameken.

Bloomberg has put together a list of other currencies that looks shaky. Who wants to play dominos?

There was no respite from yesterday’s moronization in the Canadian preferred share market today, with PerpetualDiscounts down 29bp, FixedResets losing 88bp and DeemedRetractibles off 25bp. Yet another extremely lengthy Performance Highlights table is yet again dominated by losing FixedResets. Volume was average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

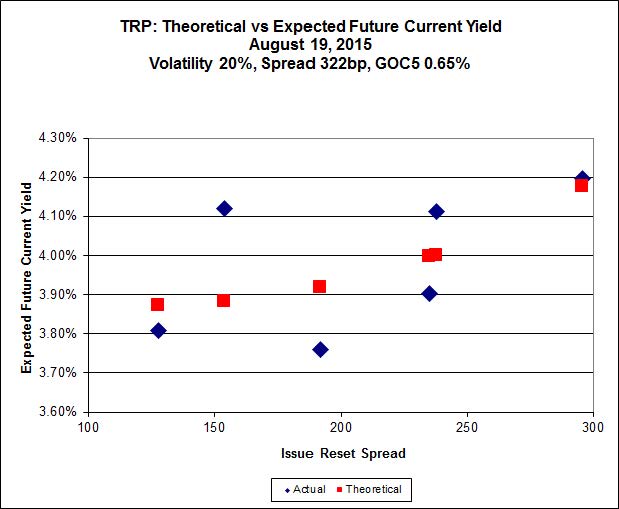

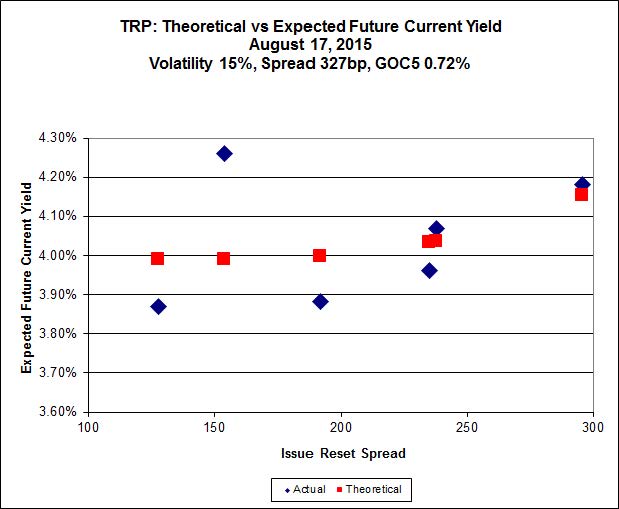

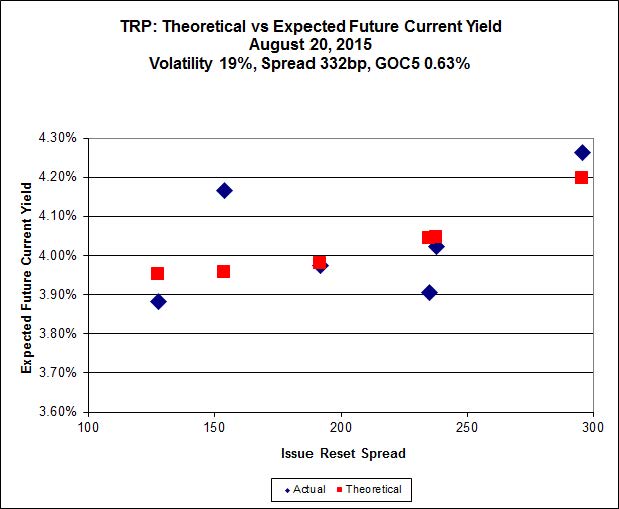

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.08 to be $0.65 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.69 cheap at its bid price of 13.02.

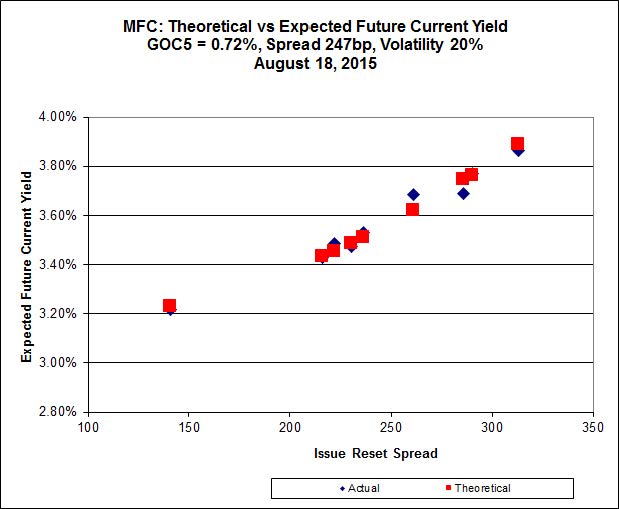

Click for Big

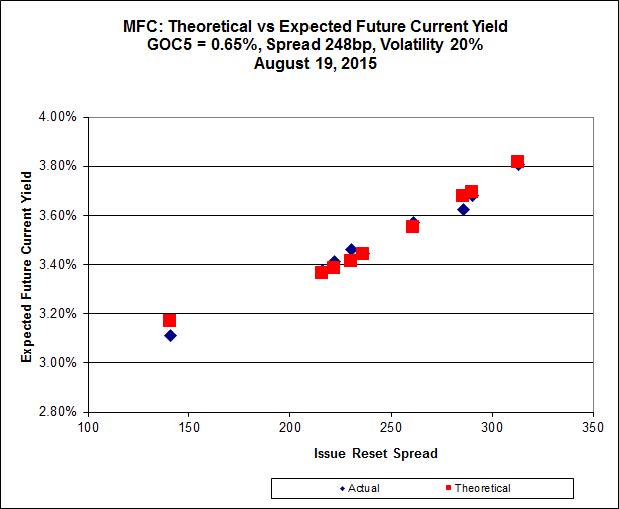

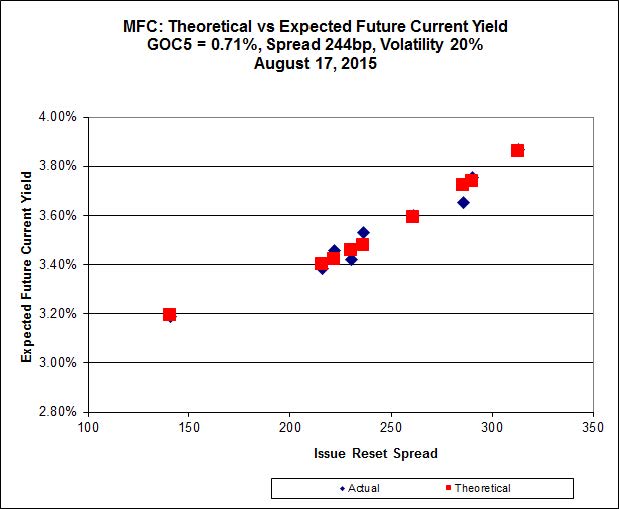

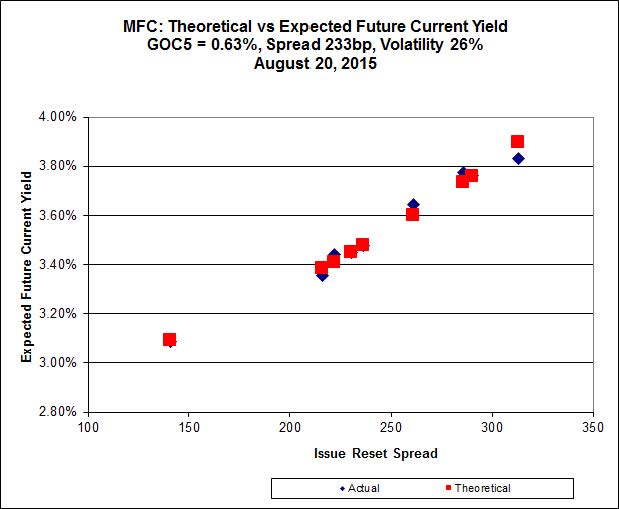

Another good fit today!

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 24.54 to be 0.40 rich, while MFC.PR.J, resetting at +261bp on 2018-3-19, bid at 22.24 to be 0.26 cheap.

Click for Big

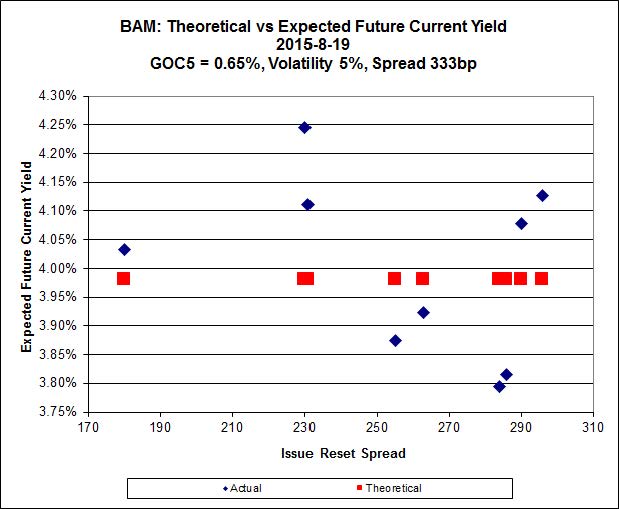

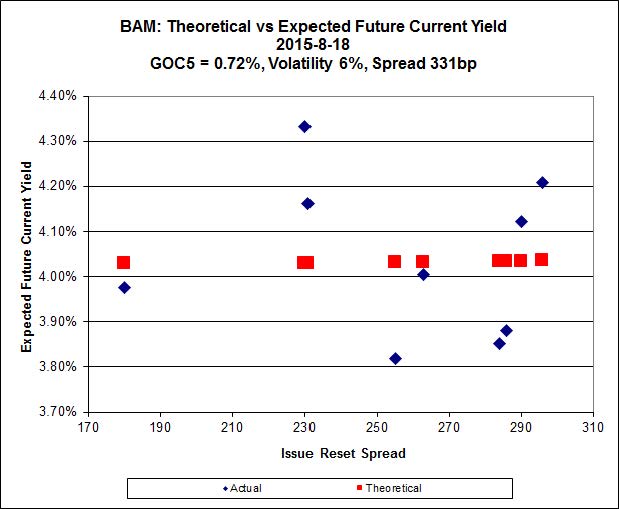

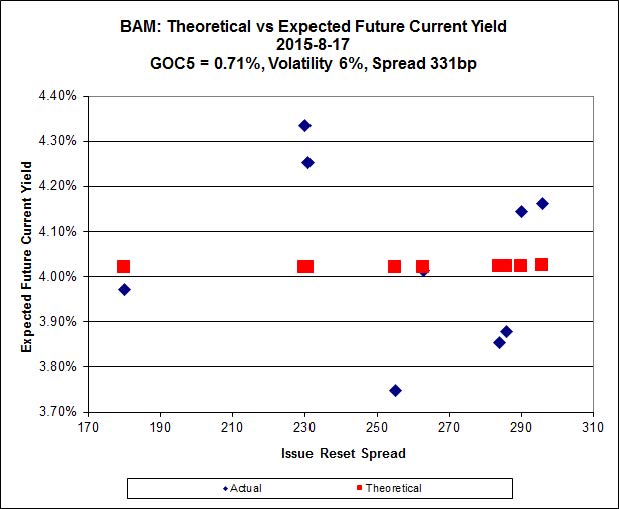

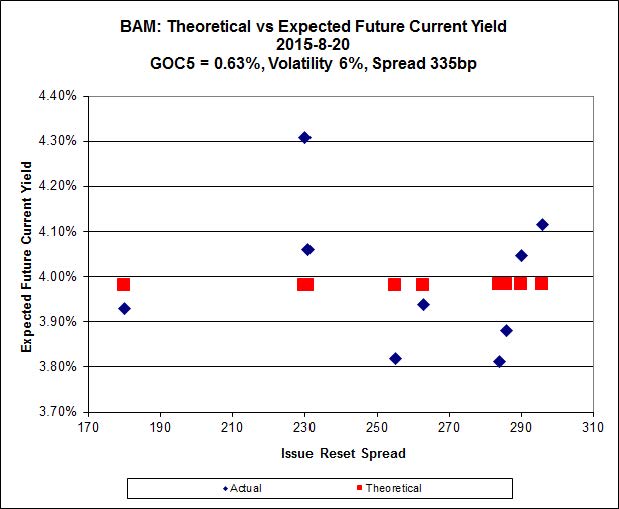

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 17.00 to be $1.40 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 22.76 and appears to be $0.97 rich.

Click for Big

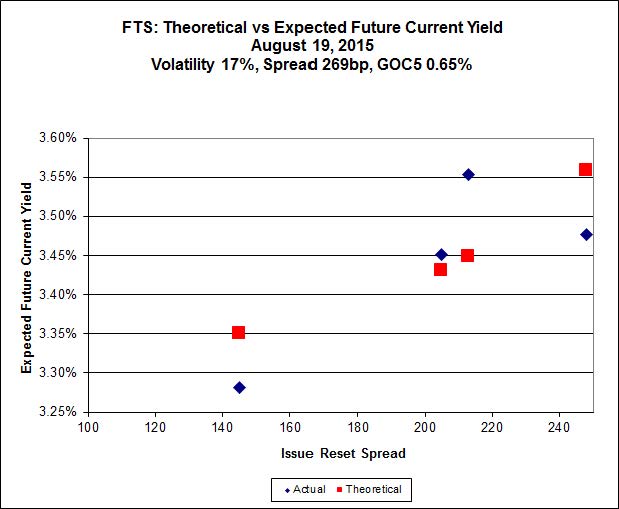

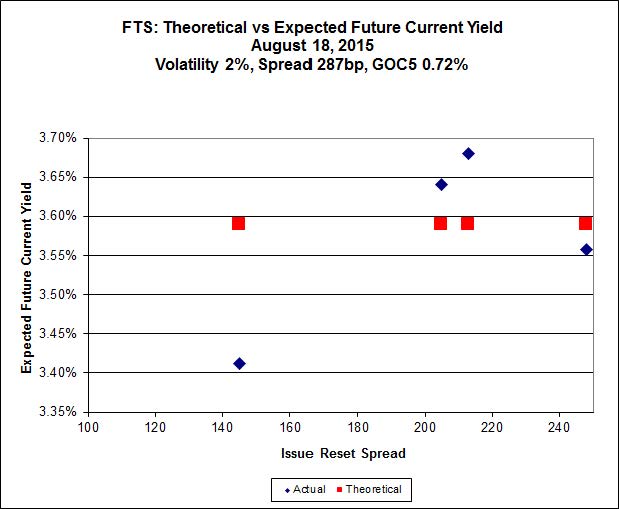

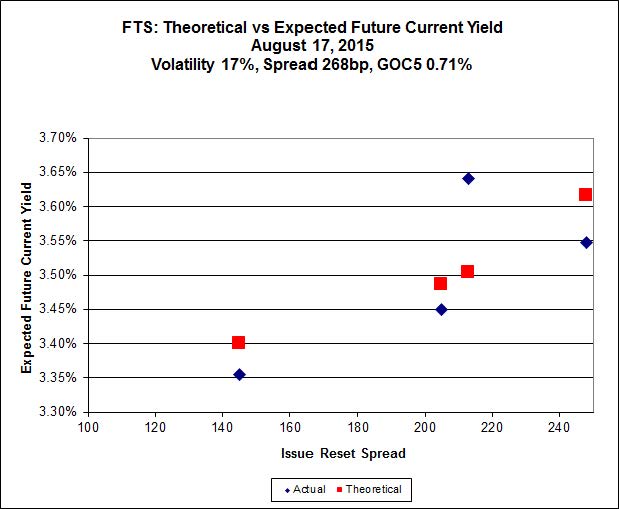

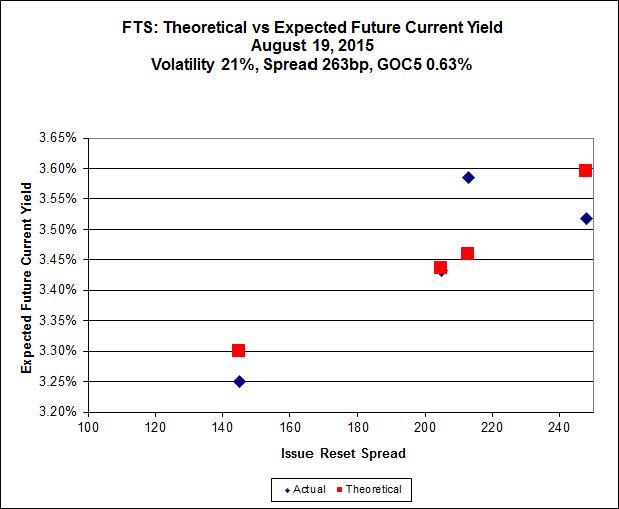

FTS.PR.M, with a spread of +248bp, and bid at 22.10, looks $0.47 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 19.25 and is $0.70 cheap.

Click for Big

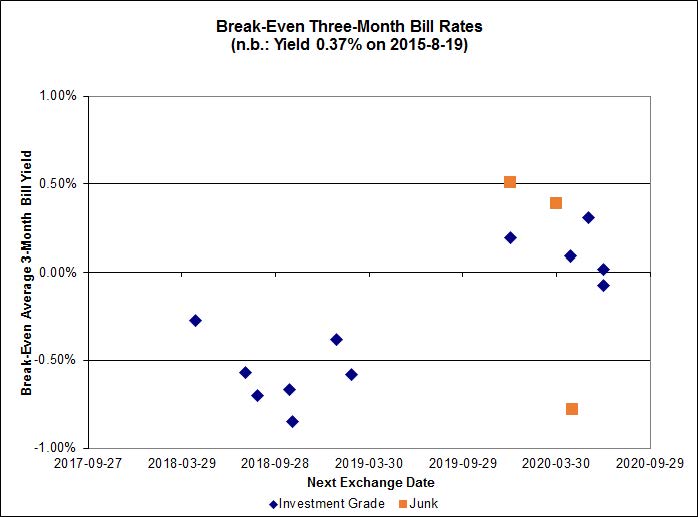

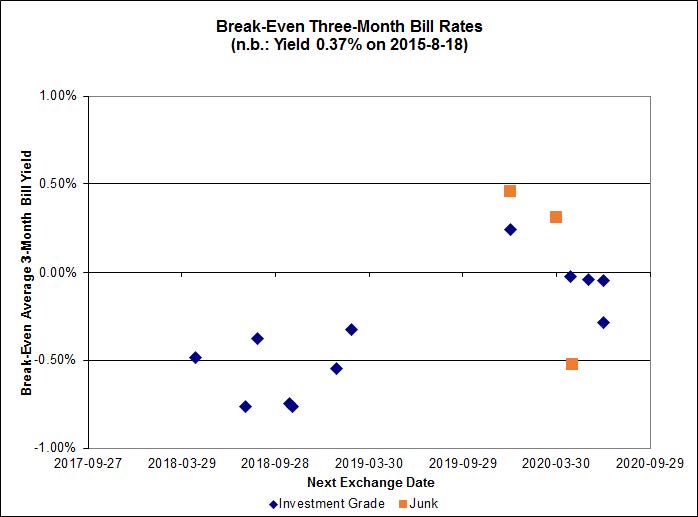

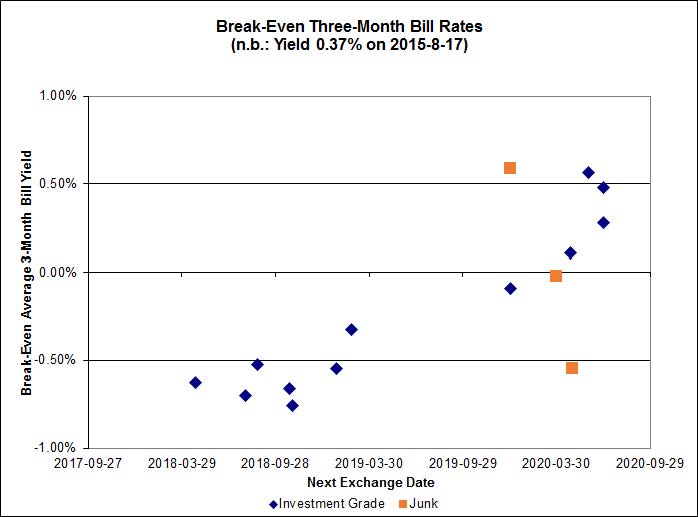

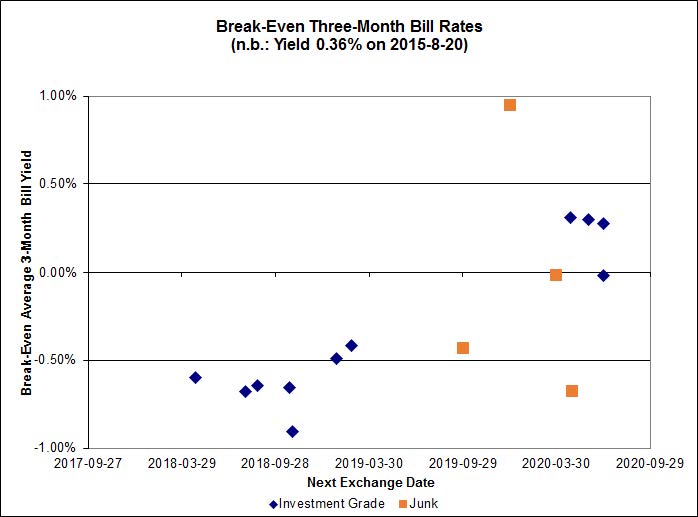

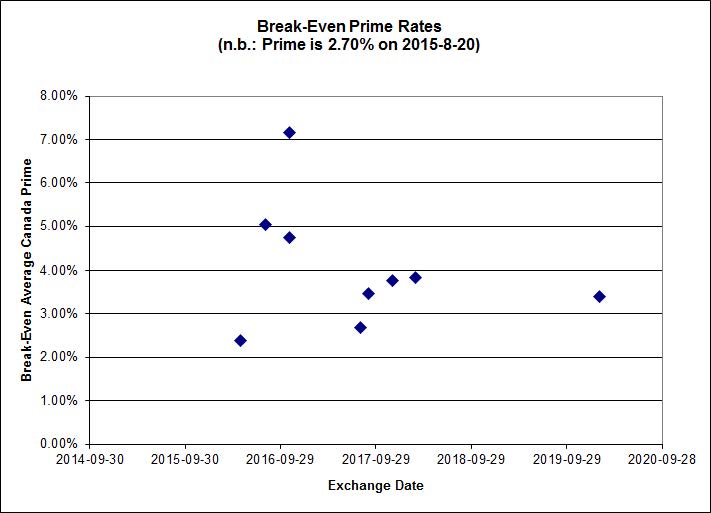

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.29%, with one outlier above +1.00%. Note that the distribution is bimodal, with NVCC non-compliant bank issues averaging -0.40% and the unregulated issues averaging +0.21%. There are two junk outliers below -1.00%.

Click for Big

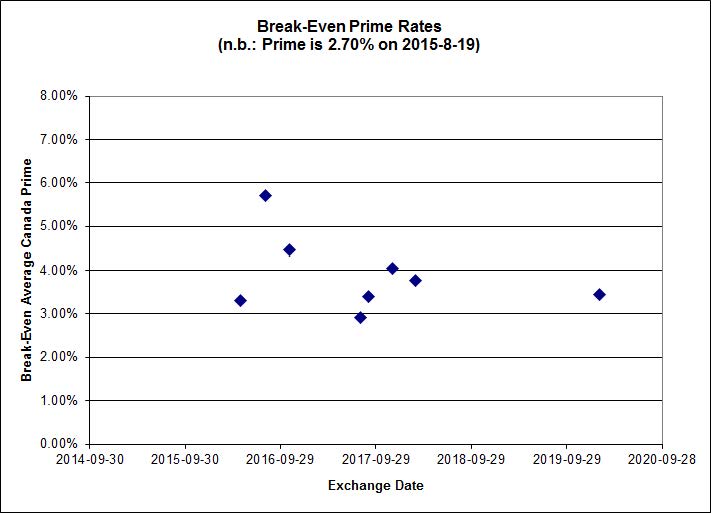

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -3.9634 % | 1,793.5 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -3.9634 % | 3,135.8 |

| Floater | 4.09 % | 4.15 % | 54,336 | 17.06 | 3 | -3.9634 % | 1,906.6 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3644 % | 2,773.8 |

| SplitShare | 4.64 % | 5.05 % | 56,318 | 3.14 | 3 | -0.3644 % | 3,250.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3644 % | 2,536.3 |

| Perpetual-Premium | 5.71 % | 5.21 % | 60,072 | 2.05 | 9 | -0.0044 % | 2,488.7 |

| Perpetual-Discount | 5.44 % | 5.48 % | 79,029 | 14.65 | 29 | -0.2887 % | 2,599.7 |

| FixedReset | 4.87 % | 4.06 % | 196,661 | 15.78 | 87 | -0.8789 % | 2,168.7 |

| Deemed-Retractible | 5.12 % | 5.19 % | 97,471 | 5.42 | 34 | -0.2494 % | 2,579.8 |

| FloatingReset | 2.36 % | 3.38 % | 49,070 | 5.98 | 9 | -0.3791 % | 2,236.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.A | FixedReset | -6.14 % | Real enough, I guess! Volume was 4,300 shares, the low for the day was 16.06 and the closing quote was 16.04-07, 2×3. The VWAP, on the other hand, was 16.85 and only 550 shares actually changed hands at prices less than 16.50, so who knows? Maybe the market maker looked at the market, looked at his inventories, thought hard … and then remembered he had a doctor’s appointment in the afternoon. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 16.04 Evaluated at bid price : 16.04 Bid-YTW : 4.20 % |

| BAM.PR.B | Floater | -5.32 % | This one is quite real. Volume was 4,893 and the day’s range was 11.71-40 with a closing quote of 11.74-06, 1×3. The VWAP was 12.00 and the last 17 trades of the day were all below this figure. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 11.74 Evaluated at bid price : 11.74 Bid-YTW : 4.07 % |

| MFC.PR.I | FixedReset | -4.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.11 Bid-YTW : 4.62 % |

| BAM.PR.C | Floater | -4.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 11.40 Evaluated at bid price : 11.40 Bid-YTW : 4.19 % |

| VNR.PR.A | FixedReset | -4.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 19.88 Evaluated at bid price : 19.88 Bid-YTW : 4.42 % |

| ENB.PR.N | FixedReset | -3.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 16.25 Evaluated at bid price : 16.25 Bid-YTW : 5.17 % |

| ENB.PR.T | FixedReset | -3.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 15.75 Evaluated at bid price : 15.75 Bid-YTW : 5.18 % |

| HSE.PR.A | FixedReset | -3.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 13.65 Evaluated at bid price : 13.65 Bid-YTW : 4.42 % |

| TRP.PR.B | FixedReset | -2.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 12.30 Evaluated at bid price : 12.30 Bid-YTW : 3.93 % |

| ENB.PF.E | FixedReset | -2.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 17.35 Evaluated at bid price : 17.35 Bid-YTW : 5.10 % |

| MFC.PR.G | FixedReset | -2.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.45 Bid-YTW : 4.37 % |

| PWF.PR.P | FixedReset | -2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 16.30 Evaluated at bid price : 16.30 Bid-YTW : 3.37 % |

| MFC.PR.J | FixedReset | -2.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.24 Bid-YTW : 4.86 % |

| ENB.PF.C | FixedReset | -2.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 5.07 % |

| ENB.PF.A | FixedReset | -2.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 17.25 Evaluated at bid price : 17.25 Bid-YTW : 5.08 % |

| ENB.PR.P | FixedReset | -2.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 15.77 Evaluated at bid price : 15.77 Bid-YTW : 5.16 % |

| BAM.PF.F | FixedReset | -2.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 22.02 Evaluated at bid price : 22.49 Bid-YTW : 4.07 % |

| ENB.PR.J | FixedReset | -2.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 16.60 Evaluated at bid price : 16.60 Bid-YTW : 5.10 % |

| BAM.PR.R | FixedReset | -2.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 4.43 % |

| TRP.PR.G | FixedReset | -2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 21.05 Evaluated at bid price : 21.05 Bid-YTW : 4.28 % |

| BAM.PR.K | Floater | -2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 11.51 Evaluated at bid price : 11.51 Bid-YTW : 4.15 % |

| TRP.PR.C | FixedReset | -2.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 13.02 Evaluated at bid price : 13.02 Bid-YTW : 4.11 % |

| MFC.PR.C | Deemed-Retractible | -1.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.14 Bid-YTW : 6.72 % |

| IAG.PR.G | FixedReset | -1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.25 Bid-YTW : 4.06 % |

| FTS.PR.M | FixedReset | -1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 21.74 Evaluated at bid price : 22.10 Bid-YTW : 3.66 % |

| ENB.PF.G | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 17.61 Evaluated at bid price : 17.61 Bid-YTW : 5.06 % |

| BNS.PR.Y | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.90 Bid-YTW : 3.98 % |

| MFC.PR.M | FixedReset | -1.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.50 Bid-YTW : 5.29 % |

| ENB.PR.D | FixedReset | -1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 14.81 Evaluated at bid price : 14.81 Bid-YTW : 5.21 % |

| FTS.PR.G | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 3.72 % |

| MFC.PR.K | FixedReset | -1.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.72 Bid-YTW : 5.47 % |

| MFC.PR.B | Deemed-Retractible | -1.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.86 Bid-YTW : 6.43 % |

| BIP.PR.A | FixedReset | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 21.57 Evaluated at bid price : 21.90 Bid-YTW : 4.86 % |

| IFC.PR.A | FixedReset | -1.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.50 Bid-YTW : 7.50 % |

| SLF.PR.A | Deemed-Retractible | -1.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.21 Bid-YTW : 6.48 % |

| PWF.PR.T | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 22.48 Evaluated at bid price : 23.15 Bid-YTW : 3.35 % |

| NA.PR.Q | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.70 Bid-YTW : 3.51 % |

| SLF.PR.C | Deemed-Retractible | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.20 Bid-YTW : 6.78 % |

| BMO.PR.Y | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 22.72 Evaluated at bid price : 23.87 Bid-YTW : 3.52 % |

| ELF.PR.F | Perpetual-Discount | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 22.74 Evaluated at bid price : 23.03 Bid-YTW : 5.82 % |

| SLF.PR.B | Deemed-Retractible | -1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.54 Bid-YTW : 6.33 % |

| MFC.PR.H | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.54 Bid-YTW : 4.05 % |

| PVS.PR.B | SplitShare | -1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2019-01-10 Maturity Price : 25.00 Evaluated at bid price : 24.72 Bid-YTW : 4.67 % |

| CM.PR.O | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 21.97 Evaluated at bid price : 22.40 Bid-YTW : 3.42 % |

| TD.PF.D | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 22.60 Evaluated at bid price : 23.60 Bid-YTW : 3.55 % |

| CU.PR.C | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 21.54 Evaluated at bid price : 21.92 Bid-YTW : 3.44 % |

| NA.PR.S | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 21.72 Evaluated at bid price : 22.02 Bid-YTW : 3.57 % |

| SLF.PR.E | Deemed-Retractible | -1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.37 Bid-YTW : 6.73 % |

| BAM.PF.G | FixedReset | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 22.14 Evaluated at bid price : 22.76 Bid-YTW : 4.03 % |

| ELF.PR.G | Perpetual-Discount | 1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 21.65 Evaluated at bid price : 21.90 Bid-YTW : 5.48 % |

| TD.PF.A | FixedReset | 1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 21.31 Evaluated at bid price : 21.31 Bid-YTW : 3.56 % |

| TRP.PR.D | FixedReset | 1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 4.23 % |

| BAM.PR.X | FixedReset | 1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 15.46 Evaluated at bid price : 15.46 Bid-YTW : 4.22 % |

| IAG.PR.A | Deemed-Retractible | 1.94 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.65 Bid-YTW : 6.04 % |

| TD.PF.B | FixedReset | 2.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 21.45 Evaluated at bid price : 21.45 Bid-YTW : 3.53 % |

| BMO.PR.W | FixedReset | 2.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 3.56 % |

| CM.PR.Q | FixedReset | 3.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 22.59 Evaluated at bid price : 23.59 Bid-YTW : 3.56 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| CM.PR.O | FixedReset | 72,200 | TD crossed 32,500 at 22.65, then sold 10,000 to RBC at 22.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 21.97 Evaluated at bid price : 22.40 Bid-YTW : 3.42 % |

| TD.PR.T | FloatingReset | 61,568 | Desjardins crossed 47,200 at 23.10; Nesbitt sold 10,000 to anonymous at 23.12. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.06 Bid-YTW : 3.28 % |

| CU.PR.H | Perpetual-Discount | 44,370 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 23.47 Evaluated at bid price : 23.78 Bid-YTW : 5.55 % |

| ENB.PR.N | FixedReset | 28,510 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 16.25 Evaluated at bid price : 16.25 Bid-YTW : 5.17 % |

| BAM.PR.T | FixedReset | 27,400 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 18.10 Evaluated at bid price : 18.10 Bid-YTW : 4.23 % |

| TRP.PR.D | FixedReset | 24,392 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-20 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 4.23 % |

| There were 36 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.T | FixedReset | Quote: 23.15 – 23.99 Spot Rate : 0.8400 Average : 0.5546 YTW SCENARIO |

| MFC.PR.G | FixedReset | Quote: 23.45 – 24.02 Spot Rate : 0.5700 Average : 0.3489 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 19.88 – 20.68 Spot Rate : 0.8000 Average : 0.5947 YTW SCENARIO |

| BMO.PR.W | FixedReset | Quote: 21.00 – 21.35 Spot Rate : 0.3500 Average : 0.2129 YTW SCENARIO |

| BAM.PF.E | FixedReset | Quote: 20.82 – 21.75 Spot Rate : 0.9300 Average : 0.8003 YTW SCENARIO |

| RY.PR.Z | FixedReset | Quote: 21.45 – 21.90 Spot Rate : 0.4500 Average : 0.3203 YTW SCENARIO |