I just noticed we’ve passed a milestone of sorts … both today and 2017-10-4, the “Median Duration-to-Worst” of the FixedReset subindex is less than 5, indicating that the average (see note, below) investment-grade FixedReset will now be called in the worst-case scenario … for a long time it has been insurance sector “Deemed Retractions” that have been medians. October 4 was the first time since November 28, 2014 that this has happened … it will be remembered that although December 1, 2014 was only a moderately negative day, but it was shortly followed by the reset of TRP.PR.A TO 3.266%. This reset was a wake-up call for the (surprisingly many) who hadn’t been paying attention to projected reset rates and I consider this to be the start of the bear market that reached its nadir in February 2016.

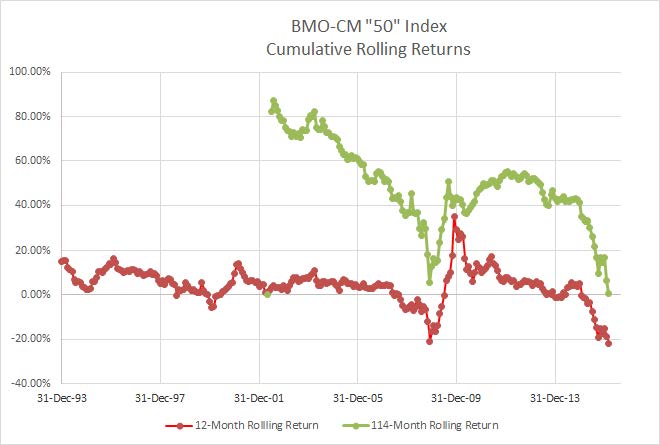

So in honour of this momentous event, let’s republish the chart showing the “Rolling 114 Month Cumulative Return”, with its commentary:

When I wrote eMail To A Client towards the end of July, one had to go back to January, 2011, to find a starting point that would give you a positive return through the holding period. As of the end of September, the required starting point moved back again, to July month-end, 2010. The debacle of the last two months, in which the BMO-CM index lost another 12.66% has extended this period to ludicrous lengths: the total cumulative return since August 31, 2006, a period of nine-and-a-half years, is now a mere 0.73%. And note the word cumulative. I don’t mean annualized. Cumulative.

The current 114-month total cumulative return of basically zero was not exceeded during the Credit Crunch. Neither was the current 12-month total return of -22.09%, since the worst 12-month cumulative return prior to this was for the year ending November 28, 2008, for which the total return was a relatively healthy -20.93%. The discussion in eMail To A Client still applies … but more so, now!

Click for Big

… and update it with the nineteen months of returns since then …

Click for Big

Looks a little better now, eh?

*Note that medians are calculated by weight, not by count, so that if you have an index that is comprised of one issue with a weight of 60% and 40 issues with a weight of 1% each, any median measured will take its value from the big issue. The median issue for the duration calculation is NA.PR.C, which is presumed by the YTW calculation to be called on economic grounds; it is ranked #47 in order of ascending Modified Duration – YTW. Of the 46 issues with a lower calculated Modified Duration – YTW:

- One has been called, price of 24.95

- Twenty-two are bank issues, presumed to be called on economic grounds, average price 25.74

- Thirteen are unregulated issues, presumed to be called on economic grounds, average price 25.83

- Two are insurance issues, presumed to be called on economic grounds, average price 26.30

- Eight are bank issues, considered to be subject to a “Deemed Retraction”, average price 24.08

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3705 % | 2,413.1 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3705 % | 4,427.9 |

| Floater | 3.79 % | 3.95 % | 25,848 | 17.55 | 4 | -0.3705 % | 2,551.8 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2379 % | 3,072.4 |

| SplitShare | 4.75 % | 4.78 % | 79,325 | 4.40 | 6 | 0.2379 % | 3,669.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2379 % | 2,862.8 |

| Perpetual-Premium | 5.38 % | 4.66 % | 60,255 | 2.35 | 17 | 0.2320 % | 2,810.4 |

| Perpetual-Discount | 5.36 % | 5.33 % | 63,173 | 14.94 | 19 | 0.3199 % | 2,935.6 |

| FixedReset | 4.27 % | 4.34 % | 151,561 | 4.58 | 99 | 0.2793 % | 2,461.3 |

| Deemed-Retractible | 5.10 % | 5.59 % | 99,162 | 6.03 | 30 | 0.2533 % | 2,886.1 |

| FloatingReset | 2.85 % | 3.02 % | 50,637 | 4.07 | 8 | 0.1587 % | 2,662.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.X | FixedReset | -1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-10-06 Maturity Price : 17.29 Evaluated at bid price : 17.29 Bid-YTW : 4.89 % |

| BMO.PR.S | FixedReset | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-10-06 Maturity Price : 23.32 Evaluated at bid price : 23.72 Bid-YTW : 4.34 % |

| PWF.PR.T | FixedReset | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-10-06 Maturity Price : 23.18 Evaluated at bid price : 23.65 Bid-YTW : 4.35 % |

| TRP.PR.F | FloatingReset | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-10-06 Maturity Price : 19.80 Evaluated at bid price : 19.80 Bid-YTW : 3.68 % |

| PWF.PR.L | Perpetual-Discount | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-10-06 Maturity Price : 23.64 Evaluated at bid price : 23.91 Bid-YTW : 5.33 % |

| MFC.PR.J | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.24 Bid-YTW : 4.92 % |

| HSE.PR.E | FixedReset | 1.19 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-03-31 Maturity Price : 25.00 Evaluated at bid price : 24.60 Bid-YTW : 5.26 % |

| BAM.PR.R | FixedReset | 1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-10-06 Maturity Price : 20.60 Evaluated at bid price : 20.60 Bid-YTW : 4.72 % |

| CU.PR.E | Perpetual-Discount | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-10-06 Maturity Price : 22.91 Evaluated at bid price : 23.35 Bid-YTW : 5.29 % |

| GWO.PR.H | Deemed-Retractible | 1.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.00 Bid-YTW : 6.28 % |

| SLF.PR.G | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.90 Bid-YTW : 8.05 % |

| BAM.PF.G | FixedReset | 1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-10-06 Maturity Price : 23.17 Evaluated at bid price : 24.34 Bid-YTW : 4.68 % |

| BAM.PR.T | FixedReset | 1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-10-06 Maturity Price : 21.09 Evaluated at bid price : 21.09 Bid-YTW : 4.69 % |

| IFC.PR.A | FixedReset | 2.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.00 Bid-YTW : 7.12 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| NA.PR.Q | FixedReset | 316,300 | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-11-15 Maturity Price : 25.00 Evaluated at bid price : 24.95 Bid-YTW : 1.84 % |

| NA.PR.X | FixedReset | 111,299 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-15 Maturity Price : 25.00 Evaluated at bid price : 26.52 Bid-YTW : 3.63 % |

| MFC.PR.H | FixedReset | 91,683 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.83 Bid-YTW : 5.08 % |

| CM.PR.R | FixedReset | 79,792 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-07-31 Maturity Price : 25.00 Evaluated at bid price : 25.35 Bid-YTW : 4.04 % |

| BAM.PR.K | Floater | 59,300 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-10-06 Maturity Price : 14.21 Evaluated at bid price : 14.21 Bid-YTW : 3.96 % |

| IAG.PR.G | FixedReset | 27,559 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.39 Bid-YTW : 5.16 % |

| There were 30 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PF.D | Perpetual-Discount | Quote: 22.06 – 22.58 Spot Rate : 0.5200 Average : 0.3319 YTW SCENARIO |

| BAM.PR.X | FixedReset | Quote: 17.29 – 17.65 Spot Rate : 0.3600 Average : 0.2210 YTW SCENARIO |

| MFC.PR.N | FixedReset | Quote: 22.76 – 23.16 Spot Rate : 0.4000 Average : 0.2611 YTW SCENARIO |

| MFC.PR.M | FixedReset | Quote: 23.00 – 23.36 Spot Rate : 0.3600 Average : 0.2445 YTW SCENARIO |

| CU.PR.D | Perpetual-Discount | Quote: 23.60 – 23.86 Spot Rate : 0.2600 Average : 0.1576 YTW SCENARIO |

| CM.PR.O | FixedReset | Quote: 23.10 – 23.50 Spot Rate : 0.4000 Average : 0.3061 YTW SCENARIO |