Why are we so dependent on foreign brains and foreign capital for technological applications?

One of China’s biggest online companies wants to deploy a fleet of drones in Canada to airlift seafood from East Coast processing plants to the airport, cutting out land-haul costs in its bid to deliver more Atlantic lobsters, prawns and clams to Chinese consumers.

JD.com is also developing plans for a drone network for the Canadian West Coast that could be used to carry local blueberries to cargo aircraft headed for China. It wants to replicate plans for similar drone networks in China, where it believes unmanned aircraft can slash logistics costs by 50 to 70 per cent, CEO Richard Liu said in an interview Tuesday.

Meanwhile, in the Canadian preferred share market …

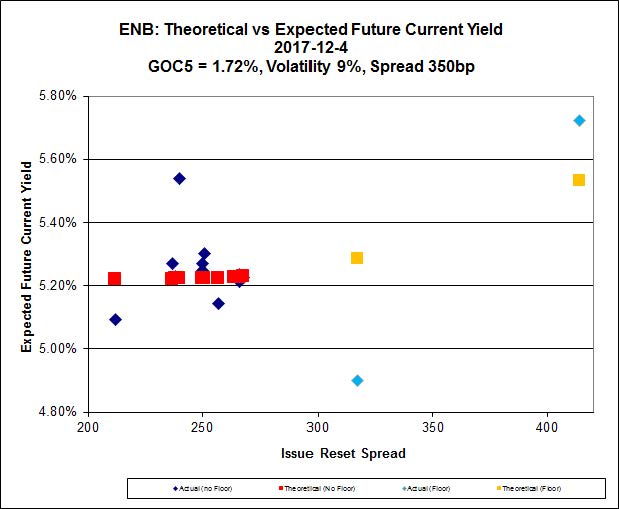

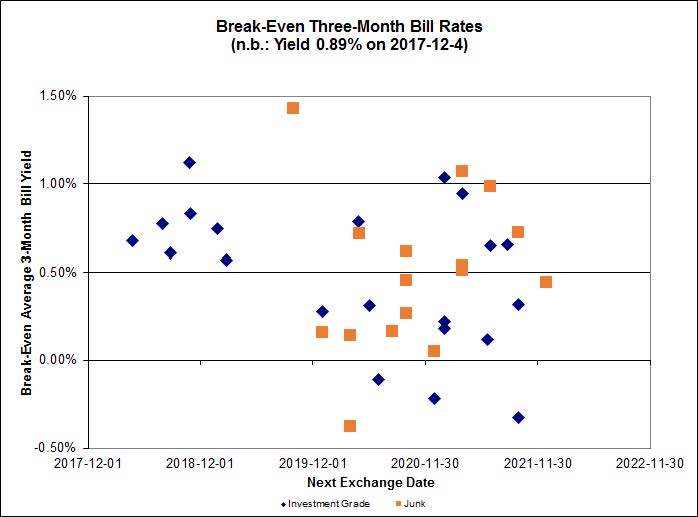

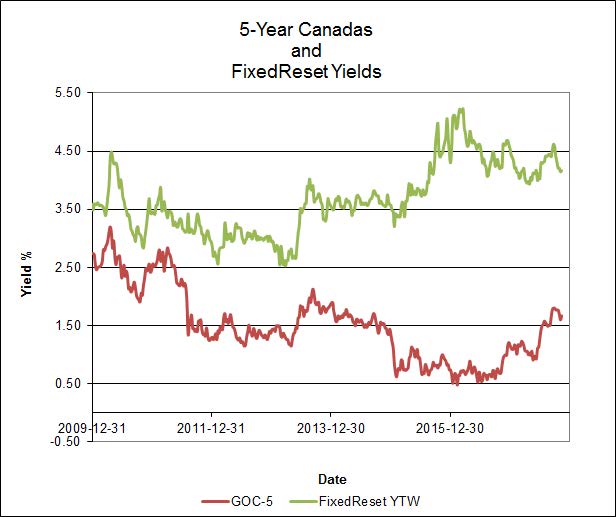

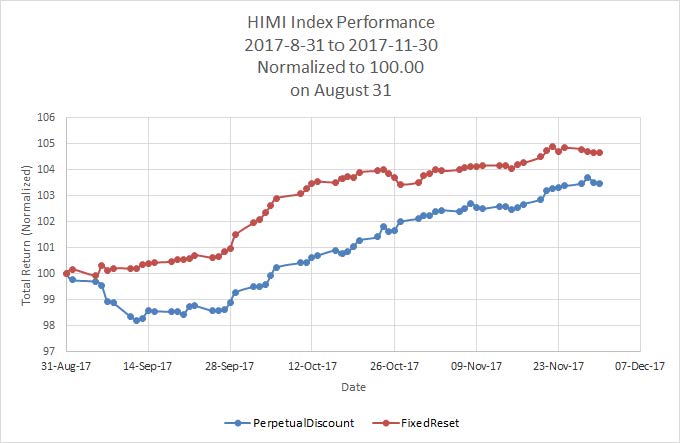

Click for Big

Today’s meltdown is a mystery to me, but in the tradition of market commentators everywhere, I’ll just nod wisely and suggest tax-loss selling. Have to suggest something!

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.7251 % | 2,513.0 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.7251 % | 4,611.3 |

| Floater | 3.64 % | 3.84 % | 33,634 | 17.69 | 4 | -0.7251 % | 2,657.5 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0197 % | 3,121.5 |

| SplitShare | 4.73 % | 3.71 % | 55,336 | 1.07 | 6 | -0.0197 % | 3,727.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0197 % | 2,908.5 |

| Perpetual-Premium | 5.36 % | 4.65 % | 54,925 | 0.16 | 20 | -0.0334 % | 2,838.7 |

| Perpetual-Discount | 5.22 % | 5.27 % | 73,307 | 15.00 | 14 | -0.3961 % | 3,001.6 |

| FixedReset | 4.28 % | 4.43 % | 142,468 | 6.11 | 98 | -0.7264 % | 2,470.3 |

| Deemed-Retractible | 5.05 % | 5.28 % | 90,434 | 5.95 | 30 | -0.2594 % | 2,943.6 |

| FloatingReset | 2.74 % | 2.76 % | 39,780 | 3.92 | 8 | -0.2442 % | 2,679.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| MFC.PR.R | FixedReset | -4.32 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-03-19 Maturity Price : 25.00 Evaluated at bid price : 24.83 Bid-YTW : 5.01 % |

| PWF.PR.P | FixedReset | -2.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 17.43 Evaluated at bid price : 17.43 Bid-YTW : 4.56 % |

| BAM.PF.G | FixedReset | -2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 23.08 Evaluated at bid price : 24.08 Bid-YTW : 4.74 % |

| IFC.PR.A | FixedReset | -2.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.64 Bid-YTW : 7.56 % |

| BAM.PF.F | FixedReset | -2.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 23.88 Evaluated at bid price : 24.21 Bid-YTW : 4.78 % |

| IAG.PR.G | FixedReset | -1.89 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.40 Bid-YTW : 5.11 % |

| TRP.PR.F | FloatingReset | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 3.64 % |

| BAM.PF.A | FixedReset | -1.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 23.73 Evaluated at bid price : 24.30 Bid-YTW : 4.79 % |

| BAM.PF.E | FixedReset | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 22.74 Evaluated at bid price : 23.35 Bid-YTW : 4.63 % |

| MFC.PR.H | FixedReset | -1.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.60 Bid-YTW : 5.12 % |

| SLF.PR.G | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.25 Bid-YTW : 7.78 % |

| MFC.PR.F | FixedReset | -1.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.77 Bid-YTW : 8.01 % |

| W.PR.M | FixedReset | -1.52 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-15 Maturity Price : 25.00 Evaluated at bid price : 25.90 Bid-YTW : 4.41 % |

| NA.PR.W | FixedReset | -1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 21.75 Evaluated at bid price : 22.23 Bid-YTW : 4.46 % |

| IFC.PR.C | FixedReset | -1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.17 Bid-YTW : 5.16 % |

| TD.PF.C | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 22.46 Evaluated at bid price : 22.75 Bid-YTW : 4.36 % |

| BAM.PR.K | Floater | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 14.65 Evaluated at bid price : 14.65 Bid-YTW : 3.87 % |

| CM.PR.O | FixedReset | -1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 22.99 Evaluated at bid price : 23.39 Bid-YTW : 4.32 % |

| BAM.PF.B | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 23.18 Evaluated at bid price : 23.65 Bid-YTW : 4.63 % |

| CM.PR.P | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 22.69 Evaluated at bid price : 23.00 Bid-YTW : 4.30 % |

| TD.PF.A | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 22.80 Evaluated at bid price : 23.15 Bid-YTW : 4.29 % |

| TRP.PR.C | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 17.01 Evaluated at bid price : 17.01 Bid-YTW : 4.59 % |

| NA.PR.C | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-11-15 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : 4.26 % |

| MFC.PR.K | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.27 Bid-YTW : 5.82 % |

| MFC.PR.G | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.25 Bid-YTW : 4.69 % |

| BAM.PR.R | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 20.06 Evaluated at bid price : 20.06 Bid-YTW : 4.84 % |

| TD.PF.B | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 22.64 Evaluated at bid price : 23.03 Bid-YTW : 4.33 % |

| CU.PR.E | Perpetual-Discount | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 23.68 Evaluated at bid price : 24.13 Bid-YTW : 5.09 % |

| BAM.PR.Z | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 23.09 Evaluated at bid price : 24.20 Bid-YTW : 4.85 % |

| TRP.PR.A | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 19.89 Evaluated at bid price : 19.89 Bid-YTW : 4.53 % |

| TRP.PR.E | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 22.51 Evaluated at bid price : 22.85 Bid-YTW : 4.50 % |

| NA.PR.S | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 22.67 Evaluated at bid price : 23.10 Bid-YTW : 4.47 % |

| SLF.PR.H | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.62 Bid-YTW : 5.61 % |

| HSE.PR.E | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-03-31 Maturity Price : 25.00 Evaluated at bid price : 24.56 Bid-YTW : 5.20 % |

| MFC.PR.I | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.47 Bid-YTW : 4.78 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PR.Y | FixedReset | 122,834 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.92 Bid-YTW : 3.62 % |

| NA.PR.W | FixedReset | 87,803 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 21.75 Evaluated at bid price : 22.23 Bid-YTW : 4.46 % |

| TD.PF.G | FixedReset | 72,547 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-30 Maturity Price : 25.00 Evaluated at bid price : 26.69 Bid-YTW : 3.55 % |

| BMO.PR.S | FixedReset | 67,338 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-05 Maturity Price : 23.06 Evaluated at bid price : 23.50 Bid-YTW : 4.30 % |

| TRP.PR.K | FixedReset | 43,216 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-05-31 Maturity Price : 25.00 Evaluated at bid price : 26.04 Bid-YTW : 3.92 % |

| CM.PR.R | FixedReset | 36,811 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-07-31 Maturity Price : 25.00 Evaluated at bid price : 25.45 Bid-YTW : 4.10 % |

| There were 40 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.R | FixedReset | Quote: 24.83 – 26.01 Spot Rate : 1.1800 Average : 0.6647 YTW SCENARIO |

| BAM.PF.G | FixedReset | Quote: 24.08 – 24.60 Spot Rate : 0.5200 Average : 0.3301 YTW SCENARIO |

| CU.PR.E | Perpetual-Discount | Quote: 24.13 – 24.52 Spot Rate : 0.3900 Average : 0.2544 YTW SCENARIO |

| CU.PR.F | Perpetual-Discount | Quote: 22.05 – 22.49 Spot Rate : 0.4400 Average : 0.3103 YTW SCENARIO |

| IFC.PR.C | FixedReset | Quote: 23.17 – 23.65 Spot Rate : 0.4800 Average : 0.3506 YTW SCENARIO |

| MFC.PR.F | FixedReset | Quote: 17.77 – 18.18 Spot Rate : 0.4100 Average : 0.2928 YTW SCENARIO |