The oil crash is being compared to subprime, in appearance if not in effect:

One year ago, analysts at Bank of America Merrill Lynch drew a parallel between the subprime mortgage crash and the disorderly fall in the price of oil.

Led by Chris Flanagan, a veteran of the securitization space, the team drew attention to Markit’s ABX Index, better known as the mother of all synthetic subprime credit indexes.

…

Fast-forward to today and the BofAML analysts provide an update to their previous thesis, which was that the downward spiral in the price of oil was shaping up to look a lot like the negative trend that engulfed the subprime space circa the year 2007.

…Given that both housing and oil prices were fueled to spectacular heights in the two periods by massive credit expansion, it’s probably more than just coincidence that the respective “bubble” bursting patterns are so similar.

…

Lower prices beget accelerated selling, as asset owners need to raise cash. It could be margin calls or it could be producer selling needs, it doesn’t really matter: the selling becomes inevitable and turns into forced selling.

Click for Big

But all that’s boring. What’s really cool is advances in 3D Printing Technology:

Orbital ATK (NYSE: OA), a global leader in aerospace and defense technologies, announced today that it has successfully tested a 3D-printed hypersonic engine combustor at NASA Langley Research Center. The combustor, produced through an additive manufacturing process known as powder bed fusion (PBF), was subjected to a variety of high-temperature hypersonic flight conditions over the course of 20 days, including one of the longest duration propulsion wind tunnel tests ever recorded for a unit of this kind. Analysis confirms the unit met or exceeded all of the test requirements.

One of the most challenging parts of the propulsion system, a scramjet combustor, houses and maintains stable combustion within an extremely volatile environment. The tests were, in part, to ensure that the PBF-produced part would be robust enough to meet mission objectives.

“Additive manufacturing opens up new possibilities for our designers and engineers,” said Pat Nolan, Vice President and General Manager of Orbital ATK’s Missile Products division of the Defense Systems Group. “This combustor is a great example of a component that was impossible to build just a few years ago. This successful test will encourage our engineers to continue to explore new designs and use these innovative tools to lower costs and decrease manufacturing time.”

The test at Langley was an important opportunity to challenge Orbital ATK’s new combustor design, made possible only through the additive manufacturing process. Complex geometries and assemblies that once required multiple components can be simplified to a single, more cost-effective assembly. However, since the components are built one layer at a time, it is now possible to design features and integrated components that could not be easily cast or otherwise machined.

And not just that … now there’s some muttering about 4-D Printing:

Now, scientists say they recently developed innovative 4D-printing methods that involve 3D-printing items that are designed to change shape after they are printed.

…

“Other active research teams exploring 4D printing require multiple materials printed together, with one material that stays rigid while another changes shape and acts like a hinge,” said study co-senior author Jennifer Lewis, a materials scientist at Harvard University.The researchers wanted to create 4D-printed structures that were created more simply, from one kind of material instead of several. They sought inspiration from nature, looking at plants, whose tendrils, leaves and flowers can respond to environmental factors such as light and touch. For instance, “pinecones can open and close depending on their degree of hydration — how wet they are,” Lewis told Live Science.

…

Plant structures largely consist of fibers of a material known as cellulose. Lewis and her colleagues devised 3D-printed structures made of stiff cellulose fibers embedded in a soft hydrogel, the same kind of material from which soft contact lenses are made. This hydrogel swells up when immersed in water.The researchers can control the directions in which these fibers are oriented within the printed structures. In turn, the orientations of these fibers control the way in which these structures swell when they are immersed in water, much like how cellulose fibers control the way plants flex because of pressure exerted by fluids inside them, the researchers said. In essence, the scientists can use the orientation of cellulose fibers in the structures to program how the objects change shape.

The scientists found that they could make the structures they created shift into cone, saddle, ruffle and spiral shapes minutes after they were soaked in water. They had flat sheets bend and twist into complex 3D structures resembling orchids and calla lilies.

What a completely fascinating time to be alive!

It was a good solid day for the Canadian preferred share market, with PerpetualDiscounts up 22bp, FixedResets winning 39bp and DeemedRetractibles gaining 21bp. The relatively calm numbers mask a lot of churn on the Performance Highlights table, though! Volume was well below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

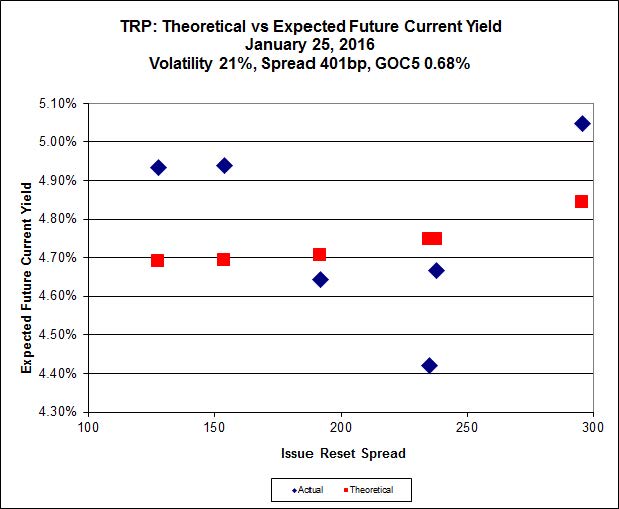

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.14 to be $1.18 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $0.76 cheap at its bid price of 18.03.

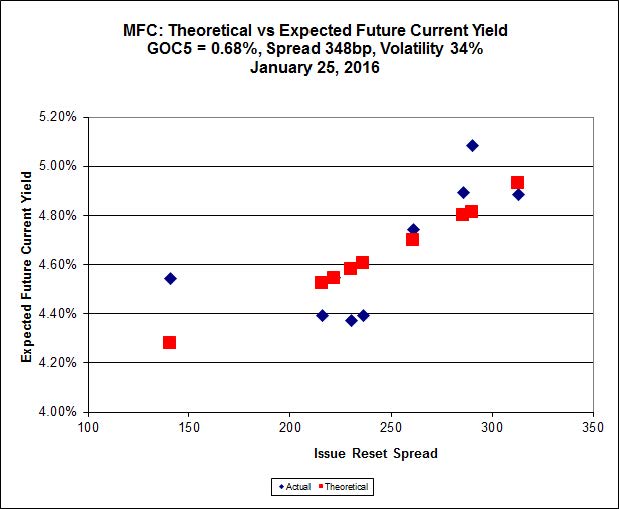

Click for Big

Most expensive is MFC.PR.M, resetting at +236bp on 2019-12-19, bid at 17.31 to be 0.80 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 17.60 to be 1.01 cheap.

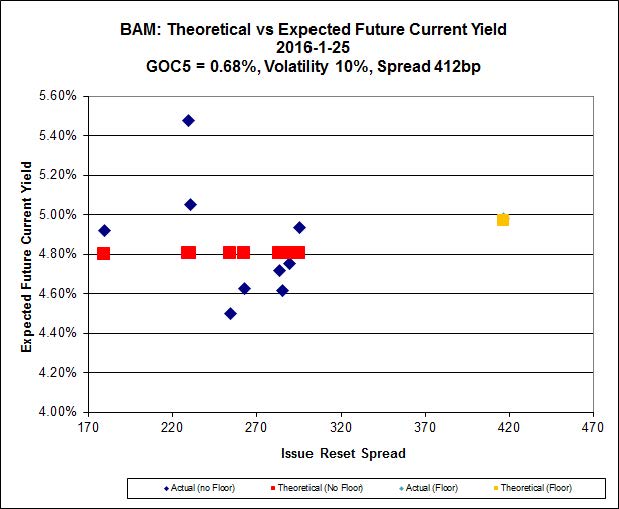

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 13.61 to be $1.91 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 17.95 and appears to be $1.13 rich.

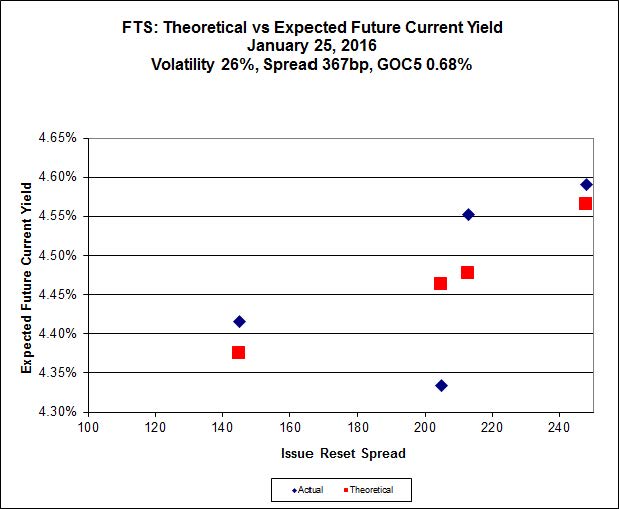

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 15.75, looks $0.46 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 15.43 and is $0.26 cheap.

Click for Big

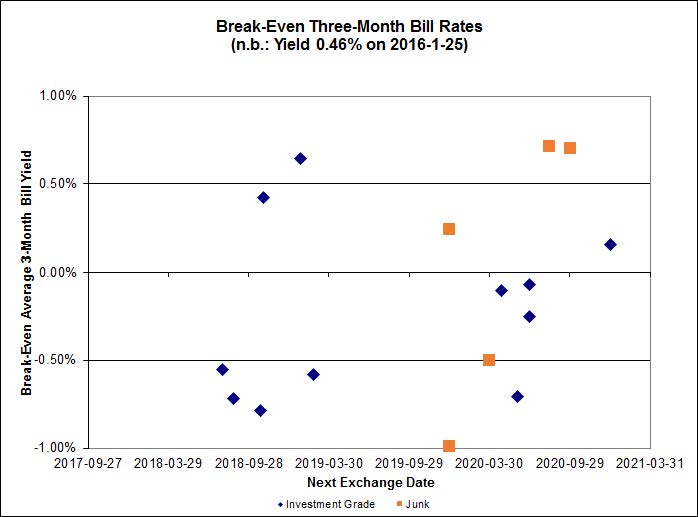

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.43%, with two outliers below -1.00%. There are five junk outliers below -1.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.21 % | 6.35 % | 20,645 | 16.20 | 1 | 1.1673 % | 1,490.6 |

| FixedFloater | 7.69 % | 6.71 % | 30,026 | 15.58 | 1 | -0.7229 % | 2,586.6 |

| Floater | 4.83 % | 5.08 % | 74,139 | 15.36 | 4 | -0.1240 % | 1,588.3 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1464 % | 2,688.8 |

| SplitShare | 4.91 % | 6.77 % | 78,359 | 2.72 | 6 | -0.1464 % | 3,146.4 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1464 % | 2,455.0 |

| Perpetual-Premium | 5.94 % | 5.90 % | 91,758 | 13.99 | 6 | -0.2294 % | 2,483.7 |

| Perpetual-Discount | 5.88 % | 5.89 % | 101,901 | 14.07 | 33 | 0.2162 % | 2,452.6 |

| FixedReset | 5.71 % | 5.02 % | 242,324 | 14.71 | 83 | 0.3861 % | 1,808.1 |

| Deemed-Retractible | 5.31 % | 5.80 % | 132,504 | 6.96 | 34 | 0.2115 % | 2,543.5 |

| FloatingReset | 2.99 % | 4.86 % | 62,285 | 5.57 | 13 | -0.0936 % | 2,005.8 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| GWO.PR.O | FloatingReset | -4.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 11.50 Bid-YTW : 11.62 % |

| SLF.PR.J | FloatingReset | -3.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 11.65 Bid-YTW : 11.62 % |

| HSE.PR.A | FixedReset | -2.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 8.32 Evaluated at bid price : 8.32 Bid-YTW : 7.44 % |

| BAM.PR.C | Floater | -2.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 9.20 Evaluated at bid price : 9.20 Bid-YTW : 5.19 % |

| SLF.PR.I | FixedReset | -2.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.27 Bid-YTW : 9.46 % |

| PVS.PR.D | SplitShare | -2.43 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 21.71 Bid-YTW : 7.56 % |

| TD.PF.A | FixedReset | -2.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 16.62 Evaluated at bid price : 16.62 Bid-YTW : 4.75 % |

| BAM.PR.B | Floater | -2.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 9.40 Evaluated at bid price : 9.40 Bid-YTW : 5.08 % |

| BNS.PR.D | FloatingReset | -1.88 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.26 Bid-YTW : 6.98 % |

| BNS.PR.B | FloatingReset | -1.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.01 Bid-YTW : 5.21 % |

| VNR.PR.A | FixedReset | -1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 16.41 Evaluated at bid price : 16.41 Bid-YTW : 5.53 % |

| BAM.PF.F | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 19.18 Evaluated at bid price : 19.18 Bid-YTW : 4.95 % |

| PWF.PR.O | Perpetual-Premium | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 23.95 Evaluated at bid price : 24.46 Bid-YTW : 5.94 % |

| BNS.PR.P | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.42 Bid-YTW : 4.20 % |

| CU.PR.I | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 23.18 Evaluated at bid price : 25.01 Bid-YTW : 4.45 % |

| BAM.PR.X | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 12.61 Evaluated at bid price : 12.61 Bid-YTW : 5.37 % |

| BAM.PF.G | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 18.66 Evaluated at bid price : 18.66 Bid-YTW : 5.13 % |

| GWO.PR.L | Deemed-Retractible | 1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.90 Bid-YTW : 5.80 % |

| RY.PR.N | Perpetual-Discount | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 21.82 Evaluated at bid price : 22.15 Bid-YTW : 5.52 % |

| BNS.PR.A | FloatingReset | 1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.09 Bid-YTW : 4.67 % |

| PVS.PR.C | SplitShare | 1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2017-12-10 Maturity Price : 25.00 Evaluated at bid price : 24.70 Bid-YTW : 5.94 % |

| TD.PR.Z | FloatingReset | 1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 4.35 % |

| BNS.PR.C | FloatingReset | 1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.65 Bid-YTW : 4.86 % |

| RY.PR.W | Perpetual-Discount | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 22.22 Evaluated at bid price : 22.50 Bid-YTW : 5.44 % |

| RY.PR.O | Perpetual-Discount | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 21.96 Evaluated at bid price : 22.24 Bid-YTW : 5.50 % |

| BAM.PR.E | Ratchet | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 25.00 Evaluated at bid price : 13.00 Bid-YTW : 6.35 % |

| NA.PR.W | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 16.55 Evaluated at bid price : 16.55 Bid-YTW : 4.79 % |

| CIU.PR.C | FixedReset | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 10.59 Evaluated at bid price : 10.59 Bid-YTW : 5.04 % |

| MFC.PR.H | FixedReset | 1.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.50 Bid-YTW : 7.45 % |

| BAM.PR.R | FixedReset | 1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 13.61 Evaluated at bid price : 13.61 Bid-YTW : 5.67 % |

| CM.PR.O | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 17.24 Evaluated at bid price : 17.24 Bid-YTW : 4.67 % |

| BAM.PF.E | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 17.95 Evaluated at bid price : 17.95 Bid-YTW : 4.96 % |

| MFC.PR.K | FixedReset | 1.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.95 Bid-YTW : 9.38 % |

| FTS.PR.G | FixedReset | 1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 15.43 Evaluated at bid price : 15.43 Bid-YTW : 4.93 % |

| TRP.PR.D | FixedReset | 1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 16.39 Evaluated at bid price : 16.39 Bid-YTW : 4.99 % |

| CM.PR.Q | FixedReset | 1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 19.11 Evaluated at bid price : 19.11 Bid-YTW : 4.63 % |

| BMO.PR.M | FixedReset | 2.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.10 Bid-YTW : 4.39 % |

| BAM.PR.K | Floater | 2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 9.40 Evaluated at bid price : 9.40 Bid-YTW : 5.08 % |

| TD.PF.F | Perpetual-Discount | 2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 21.87 Evaluated at bid price : 22.21 Bid-YTW : 5.53 % |

| PWF.PR.A | Floater | 2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 11.15 Evaluated at bid price : 11.15 Bid-YTW : 4.23 % |

| TRP.PR.C | FixedReset | 2.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 11.24 Evaluated at bid price : 11.24 Bid-YTW : 5.05 % |

| BAM.PR.T | FixedReset | 2.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 14.80 Evaluated at bid price : 14.80 Bid-YTW : 5.32 % |

| TRP.PR.E | FixedReset | 2.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 17.14 Evaluated at bid price : 17.14 Bid-YTW : 4.84 % |

| BAM.PR.Z | FixedReset | 2.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 18.45 Evaluated at bid price : 18.45 Bid-YTW : 5.20 % |

| TD.PF.C | FixedReset | 2.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 4.54 % |

| PWF.PR.S | Perpetual-Discount | 2.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 20.65 Evaluated at bid price : 20.65 Bid-YTW : 5.85 % |

| RY.PR.K | FloatingReset | 3.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.55 Bid-YTW : 4.99 % |

| RY.PR.I | FixedReset | 3.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.05 Bid-YTW : 4.57 % |

| BIP.PR.B | FixedReset | 3.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 22.22 Evaluated at bid price : 22.90 Bid-YTW : 6.07 % |

| TRP.PR.B | FixedReset | 4.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 9.93 Evaluated at bid price : 9.93 Bid-YTW : 5.17 % |

| BAM.PF.B | FixedReset | 4.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 17.89 Evaluated at bid price : 17.89 Bid-YTW : 4.93 % |

| BAM.PF.A | FixedReset | 4.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 18.83 Evaluated at bid price : 18.83 Bid-YTW : 5.02 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| NA.PR.X | FixedReset | 298,282 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 23.05 Evaluated at bid price : 24.72 Bid-YTW : 5.62 % |

| RY.PR.Q | FixedReset | 82,192 | TD crossed 15,900 at 25.40; Scotia crossed 40,000 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 23.25 Evaluated at bid price : 25.35 Bid-YTW : 5.20 % |

| BMO.PR.S | FixedReset | 62,563 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 17.42 Evaluated at bid price : 17.42 Bid-YTW : 4.70 % |

| BNS.PR.Z | FixedReset | 46,222 | RBC crossed 40,000 at 18.65. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.64 Bid-YTW : 7.44 % |

| RY.PR.J | FixedReset | 27,691 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 18.16 Evaluated at bid price : 18.16 Bid-YTW : 4.80 % |

| RY.PR.Z | FixedReset | 27,661 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-25 Maturity Price : 17.15 Evaluated at bid price : 17.15 Bid-YTW : 4.53 % |

| There were 20 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| CCS.PR.C | Deemed-Retractible | Quote: 21.25 – 23.15 Spot Rate : 1.9000 Average : 1.1381 YTW SCENARIO |

| TD.PF.A | FixedReset | Quote: 16.62 – 17.55 Spot Rate : 0.9300 Average : 0.6834 YTW SCENARIO |

| BAM.PF.F | FixedReset | Quote: 19.18 – 19.99 Spot Rate : 0.8100 Average : 0.6465 YTW SCENARIO |

| BMO.PR.Q | FixedReset | Quote: 18.25 – 19.00 Spot Rate : 0.7500 Average : 0.5936 YTW SCENARIO |

| BNS.PR.B | FloatingReset | Quote: 21.01 – 21.44 Spot Rate : 0.4300 Average : 0.2771 YTW SCENARIO |

| BMO.PR.M | FixedReset | Quote: 23.10 – 23.88 Spot Rate : 0.7800 Average : 0.6312 YTW SCENARIO |