The scavenging of the corpse of Nortel is approaching an end:

Canadian pensioners at Nortel Networks Corp. are heading into a rare cross-border trial in May to try to ensure more of the defunct company’s remaining assets are allocated to the Canadian division in an effort to boost the company’s underfunded pension plan.

The hearing, which runs from May 12 to June 27, will be conducted using video links before two judges – one in Toronto and one in Delaware – and will hear arguments from lawyers from Canada, the U.S. and Britain about how the remaining Nortel assets should be divided among the three jurisdictions.

Creditors, including Nortel pension funds and bondholders, have submitted claims worth $36-billion, while estimated assets currently total about $9-billion, including $7.3-billion raised from asset sales.

Canadian pensioners say the heart of their battle is a dispute with Nortel’s bondholders, who they accuse of manoeuvring to have more assets assigned to Nortel’s U.S. estate in an effort to improve their odds of receiving more than $1-billion of unpaid interest on their bonds from the time Nortel filed for bankruptcy protection in 2009.

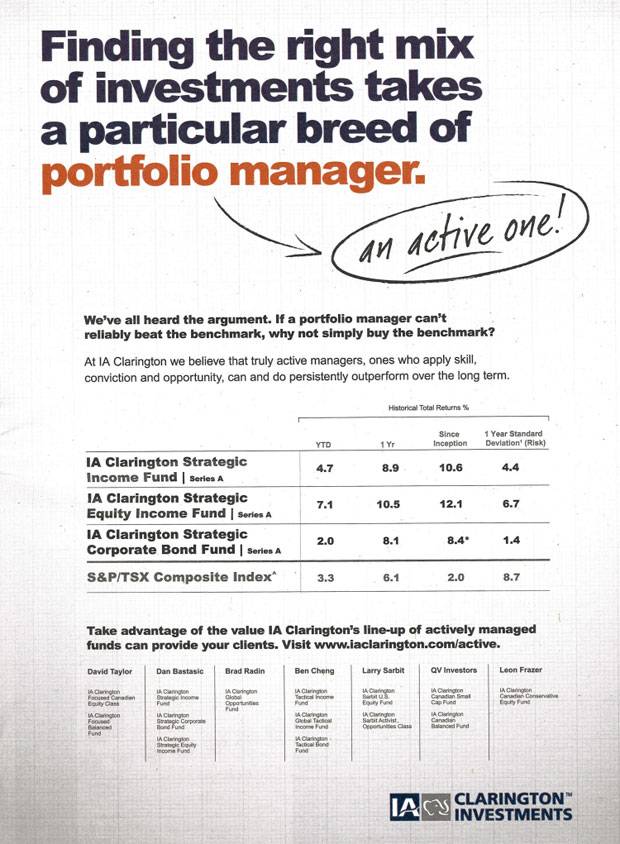

Andrew Hallam points out in the Globe that IA Clarington is being naughty:

Click for Big

Click for BigIn a recent advertisement, they claim market-beating performance for three of their funds. They compared their Strategic Income Fund, Strategic Equity Income and their Strategic Corporate Bond Fund to a Canadian stock index. By doing so, however, they compared toasters to microwaves. None of IA Clarington’s advertised market-beating funds hold significant amounts of Canadian stocks. So why compare them to a Canadian stock index? Investors should be wary of advertorial sleight of hand.

The advertisement states, “At IA Clarington we believe that truly active managers, ones who apply skill, conviction and opportunity, can and do consistently outperform [indexes] over the long term.” But the funds in the advertisement are less than three years old.

…

I examined each of their funds with 10-year track records in six separate categories: Canadian Equity, Balanced, U.S. Equity, International Equity, Canadian Bond and Canadian Short Term Government Bond. Over the decade, IA Clarington’s fund performances fell 22.5 per cent short. They’re also the only firm I’ve compared in this series so far to underperform retail indexes in all six categories.

It was a strong day for the Canadian preferred share market, with PerpetualDiscounts winning 29bp, FixedResets gaining 13bp and DeemedRetractibles up 20bp. This burst the dam on the performance report, which features a fine host of winners; mostly FixedResets. Volume was high, with a big crop of six-figure volumes.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3312 % | 2,419.2 |

| FixedFloater | 4.64 % | 3.88 % | 32,102 | 17.74 | 1 | 0.2940 % | 3,699.7 |

| Floater | 3.01 % | 3.15 % | 50,783 | 19.34 | 4 | 0.3312 % | 2,612.1 |

| OpRet | 4.35 % | -4.71 % | 34,126 | 0.09 | 2 | -0.0967 % | 2,697.3 |

| SplitShare | 4.80 % | 4.41 % | 65,171 | 4.20 | 5 | 0.0873 % | 3,093.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0967 % | 2,466.4 |

| Perpetual-Premium | 5.54 % | -7.35 % | 106,617 | 0.09 | 13 | 0.0483 % | 2,389.5 |

| Perpetual-Discount | 5.37 % | 5.37 % | 110,747 | 14.62 | 23 | 0.2881 % | 2,509.0 |

| FixedReset | 4.61 % | 3.54 % | 205,087 | 4.38 | 78 | 0.1271 % | 2,547.0 |

| Deemed-Retractible | 5.01 % | -2.51 % | 143,342 | 0.15 | 42 | 0.1951 % | 2,506.4 |

| FloatingReset | 2.67 % | 2.44 % | 179,031 | 4.09 | 5 | 0.0551 % | 2,486.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| MFC.PR.F | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.22 Bid-YTW : 4.23 % |

| TRP.PR.B | FixedReset | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-04-29 Maturity Price : 20.64 Evaluated at bid price : 20.64 Bid-YTW : 3.69 % |

| BAM.PR.X | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-04-29 Maturity Price : 21.50 Evaluated at bid price : 21.87 Bid-YTW : 4.20 % |

| ENB.PR.N | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2018-12-01 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : 3.88 % |

| BAM.PR.N | Perpetual-Discount | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-04-29 Maturity Price : 21.27 Evaluated at bid price : 21.27 Bid-YTW : 5.65 % |

| IAG.PR.A | Deemed-Retractible | 1.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.65 Bid-YTW : 5.87 % |

| TRP.PR.A | FixedReset | 1.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-04-29 Maturity Price : 23.23 Evaluated at bid price : 23.91 Bid-YTW : 3.78 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| IAG.PR.G | FixedReset | 346,612 | Nesbitt crossed blocks of 58,900 shares, 175,000 and 100,000, all at 25.90. YTW SCENARIO Maturity Type : Call Maturity Date : 2017-06-30 Maturity Price : 25.00 Evaluated at bid price : 25.88 Bid-YTW : 3.25 % |

| TRP.PR.A | FixedReset | 172,685 | Nesbitt crossed blocks of 110,000 and 51,800, both at 23.70. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-04-29 Maturity Price : 23.23 Evaluated at bid price : 23.91 Bid-YTW : 3.78 % |

| BAM.PR.Z | FixedReset | 169,488 | RBC crossed blocks of 71,000 and 83,000, both at 25.85. YTW SCENARIO Maturity Type : Call Maturity Date : 2017-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.88 Bid-YTW : 3.89 % |

| BMO.PR.S | FixedReset | 151,844 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2019-05-25 Maturity Price : 25.00 Evaluated at bid price : 25.46 Bid-YTW : 3.63 % |

| BAM.PR.R | FixedReset | 136,986 | RBC crossed blocks of 65,000 and 11,900 at 26.00, and another 50,000 at 26.07. YTW SCENARIO Maturity Type : Call Maturity Date : 2016-06-30 Maturity Price : 25.00 Evaluated at bid price : 25.92 Bid-YTW : 3.84 % |

| CIU.PR.B | FixedReset | 109,047 | Nesbitt crossed 108,700 at 25.40. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-06-01 Maturity Price : 25.00 Evaluated at bid price : 25.37 Bid-YTW : 2.27 % |

| RY.PR.Y | FixedReset | 108,169 | TD crossed 94,000 at 25.66. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-11-24 Maturity Price : 25.00 Evaluated at bid price : 25.60 Bid-YTW : 1.14 % |

| HSE.PR.A | FixedReset | 104,272 | Nesbitt crossed 100,000 at 23.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-04-29 Maturity Price : 22.60 Evaluated at bid price : 22.94 Bid-YTW : 3.83 % |

| SLF.PR.F | FixedReset | 103,401 | TD crossed 102,200 at 25.34. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-06-30 Maturity Price : 25.00 Evaluated at bid price : 25.32 Bid-YTW : 1.16 % |

| There were 43 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.G | FixedReset | Quote: 26.14 – 26.90 Spot Rate : 0.7600 Average : 0.4720 YTW SCENARIO |

| PWF.PR.L | Perpetual-Discount | Quote: 24.10 – 24.39 Spot Rate : 0.2900 Average : 0.1884 YTW SCENARIO |

| BNS.PR.R | FixedReset | Quote: 25.75 – 26.08 Spot Rate : 0.3300 Average : 0.2307 YTW SCENARIO |

| MFC.PR.L | FixedReset | Quote: 24.95 – 25.20 Spot Rate : 0.2500 Average : 0.1529 YTW SCENARIO |

| PWF.PR.R | Perpetual-Premium | Quote: 25.40 – 25.66 Spot Rate : 0.2600 Average : 0.1675 YTW SCENARIO |

| CIU.PR.C | FixedReset | Quote: 21.32 – 21.68 Spot Rate : 0.3600 Average : 0.2777 YTW SCENARIO |