I have no idea how important this service really is … but certainly my projections of sixteen years ago (that the Internet would promote a meritocracy and decrease the importance of brand names) are seeing some acceptance:

Joshua Young started his hedge fund less than a year ago. Last month, he caught a break when a university endowment handed him $20 million, quintupling his assets under management.

How did an obscure Houston fund called Bison Interests land such a big fish?

Young, all of 32, had set up a profile on SumZero, a website that started out as a repository for buy-side research and has more recently morphed into a mashup of LinkedIn and Match.com where institutional investors can find up-and-coming fund managers and choose them based on the quality of their analysis. Using SumZero, Young bypassed an old-boy network that prizes relationships, credentials and word-of-mouth referrals. The company says it has helped generate hundreds of introductions between the more than 12,000 fund managers with SumZero profiles and the 270 institutional investors now using the site, which include the family offices of several big tech executives.

…

Multiple studies have shown that smaller funds tend to do better than larger ones, some of which have performed poorly during the recent market rout. But herd mentality and risk-avoidance prompts many institutional investors to steer their money to big, entrenched players. Firms with more than $5 billion under management represent just 6 percent of all hedge funds but manage about 70 percent of the invested capital, according to Hedge Fund Research.

This trend, if it is a trend, ties in with the Death of a Salesman meme:

Banks are taking a hatchet to their bond-trading businesses and the biggest casualties are proving to be the people with the most experience.

About 70 percent of credit traders cut in London last year at the 12 largest investment banks had worked in the financial industry for more than 10 years, according to data compiled by headhunters Michelangelo Search, which specializes in sales, trading and research roles. That’s increasingly leaving trading desks manned by more junior colleagues.

Experienced, better-compensated staff are falling victim to banks’ efforts to reduce costs as they try to generate profit within constraints imposed by regulators and central banks since the global financial crisis. There’s more to come as banks from Bank of America Corp. to Goldman Sachs Group Inc. consider cuts as soon as this quarter.

“I’ve been in the fixed income business for 35 years but most of my cohort is now missing in action,” said Tim Skeet, who has worked in bond-market roles since 1981, and is currently looking for a new position in the industry. “There’s a ‘juniorization’ of the workplace underway in London as banks focus more on costs than revenues.”

Understanding the connection requires a little explanation. The Masters of the Universe, the fixed income traders/salesmen who pulled down megabucks during the boom, do not achieve that status by being red-hot super-sharp analysts. What they got – and still get – paid for is bringing in business and keeping that inventory turning over while making the full spread (or more!) every time.

You don’t need any understanding of the bond market to do that. In my experience, that doesn’t even help. What you need is a deep voice, a firm handshake, a little charisma, and a great big expense account so entertain the clients. Contacts from prep school or Daddy’s friends are good things to have as well. And presto! You’re a trader!

Old bond traders didn’t make the big bucks for analysis, or helping clients achieve outperformance. As my Assiduous Readers will remember, the average Portfolio Manager has about enough brains to use the right fork when taking clients out to lunch, but that’s about where it ends and that’s all that’s necessary. So they rely extensively on their salesman’s advice. On occasion, that salesman will be the de facto portfolio manager, because the PM of record is a rubber stamp. And once the PM finds a guy he thinks he can trust, that salesman will get a lot of business from him; and that business will follow the salesman if he changes firms. And the bosses know that, so the salesman gets considerable incentive to stay on board and keep producing those lovely, lovely spreads of pure profit.

In Canada, the model started dying, as far as I can tell, some time in the mid-2000s. The banks don’t like having employees who make good money, so they started bringing in high-school students to act as salesmen (well, they sounded like high school students to me!). The selling template went from ‘I can make you look good’ to ‘We’re a bank!’.

And, I think, the same thing is starting to play out globally, helped along by a bit more transparency (even in 1990-odd, Bloomberg took all the fun out of the Eurobond market), a little less influence of the old-boy network when hiring portfolio managers (they’re all bank drones nowadays, too!) and, of course, all the scandals.

Maybe. It would take a team of sociologists to prove I’m right … but it would take the same team to prove I’m wrong! So I’ve said something provocative that is not susceptible to disproof, which is the holy grail of investment writing.

Meanwhile in Canada, the central planners are hard at work:

Canadians looking to buy homes between $500,000 and $1-million will have to put down larger down payments as new federal rules took effect Monday.

Under the changes, home buyers must now put at least 10 per cent down on the portion of a home that costs more than $500,000.

Buyers can still put down five per cent on the first $500,000 of a home purchase. Homes that cost more than $1-million still require a 20 per cent down payment.

Phil Soper, president and CEO of Royal LePage, says the new rules aim to slow the breakneck pace of price growth in the red-hot markets of Toronto and Vancouver without affecting markets that are lagging, such as those in oil-dependent provinces.

“The problem with monetary policy is that it impacts the struggling Calgary market or the just fine Winnipeg market and the overheated Vancouver market in equal amounts,” Soper said.

And in BC, there’s more welfare:

Hours after the Canadian Real Estate Association reported that Greater Vancouver housing prices led the country in growth, climbing on average by more than 20 per cent over the past year, Finance Minister Mike de Jong rose in the legislature to lay out a fiscal plan that he said will help more people realize the dream of owning a house.

In the first major overhaul of the Property Transfer Tax since its inception in 1988, Mr. de Jong has raised the exemption threshold – solely on new houses – to $750,000. The new tax break, available only to Canadian citizens and permanent residents, could mean savings of up to $13,000 on a house.

Element Financial, proud issuer of EFN.PR.A, EFN.PR.C, EFN.PR.E and EFN.PR.G, has announced:

that following the completion of a strategic review of each of the Company’s business units that it initiated in October of last year, the Board of Directors has approved plans to proceed with a transaction that will result in the separation of the current business into two publicly traded companies – a $19.5 billion world class fleet management company (Element Fleet Management) to be led by Bradley Nullmeyer and a $7.0 billion North American commercial finance company (Element Commercial Asset Management) to be led by Steven Hudson.

…

The Company is currently analyzing the most efficient method to implement the separation of the two businesses and further details will be provided to the market as Element completes this analysis with its advisors. The separation transaction that will split the Company into these two publicly traded entities is expected to be completed on a tax free basis before the end of 2016. The allocation of the assets, liabilities and capital structure of the Company, as well as the structure of the Board and the deployment of current corporate services staff between the two new entities will be determined as the details of this separation transaction are determined.

We’ll see what happens as details emerge, but I have a hard time envisaging this as being credit-positive for the preferreds!

It was a relatively quiet day overall for the Canadian preferred share market, with PerpetualDiscounts gaining 5bp, FixedResets off 10bp and DeemedRetractibles flat. The overall calm masked significant churn, as shown in the Performance Highlights table. Volume was high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

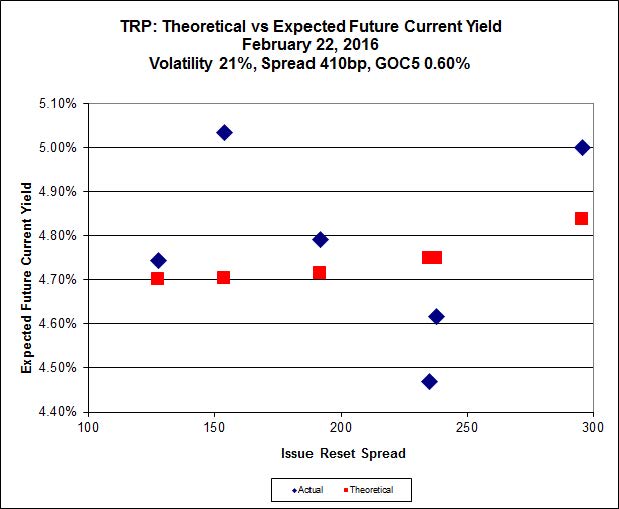

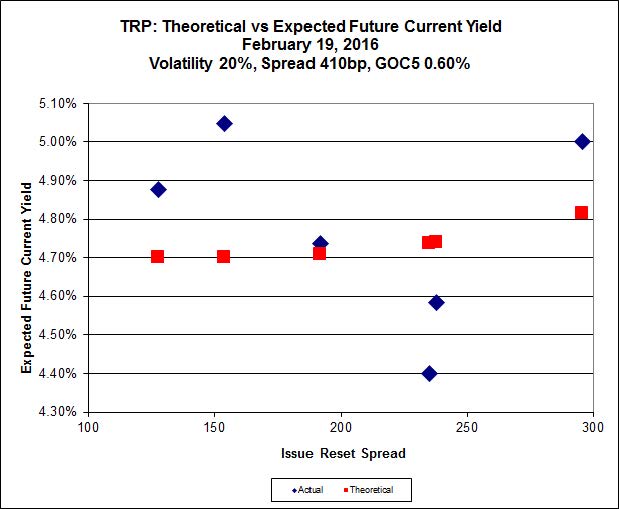

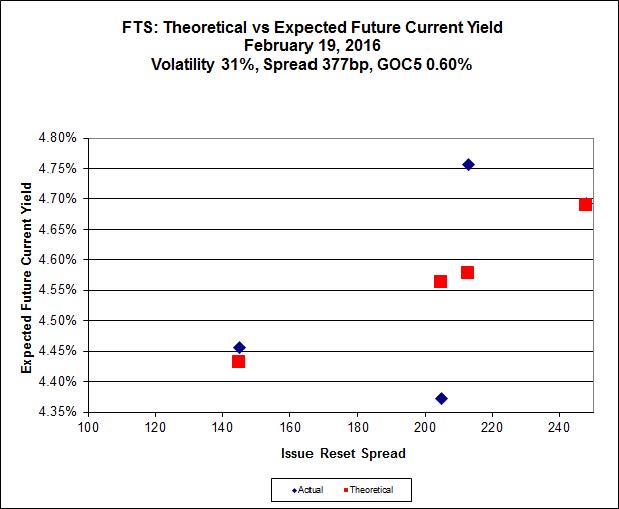

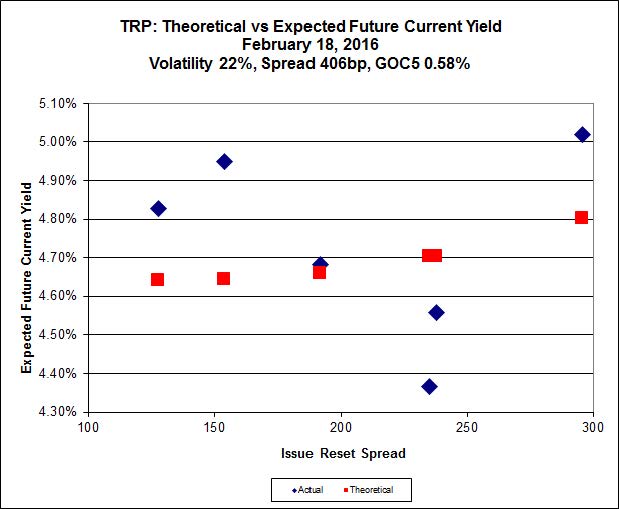

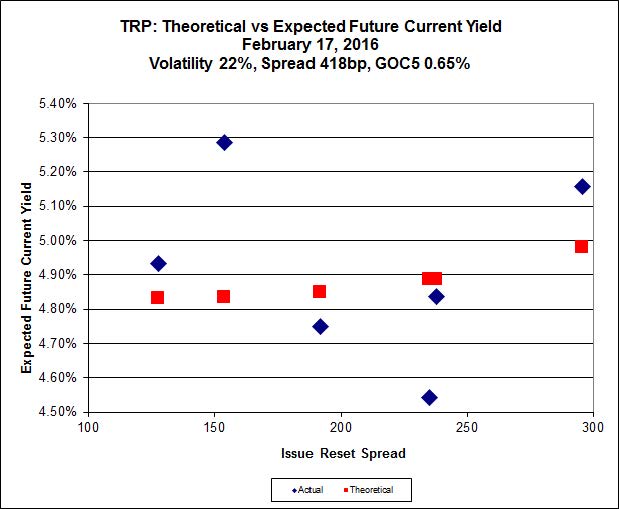

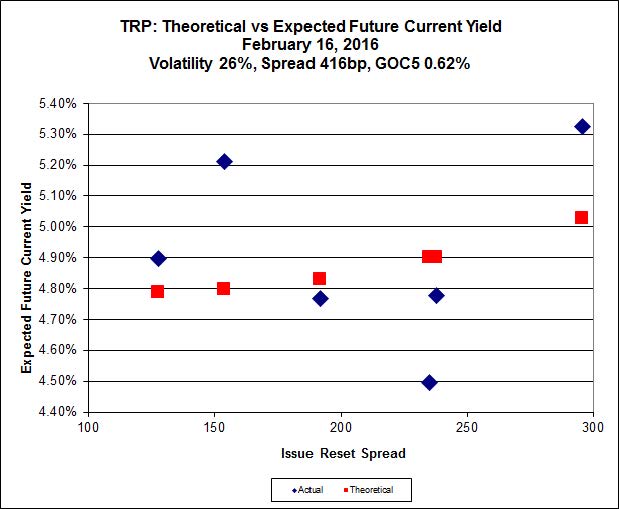

Here’s TRP:

Click for Big

Click for BigTRP.PR.E, which resets 2019-10-30 at +235, is bid at 16.52 to be $1.37 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $1.00 cheap at its bid price of 16.81.

Click for Big

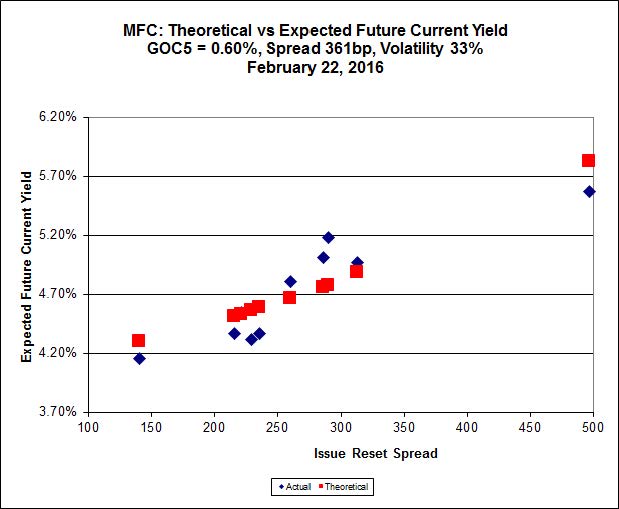

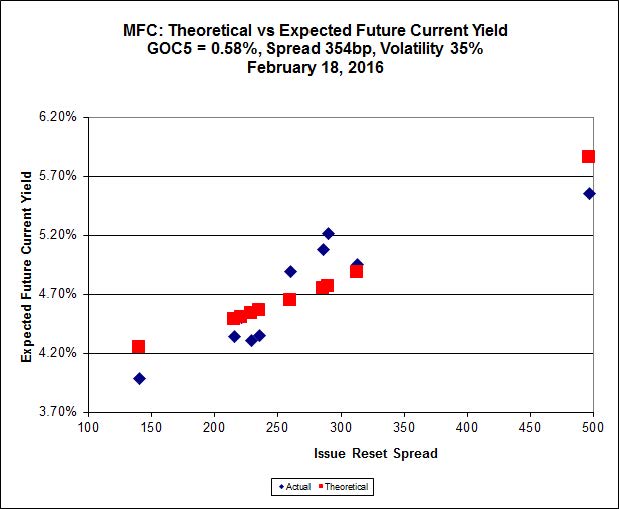

Click for BigThis analysis includes the new issue with a deemed price of 25.00.

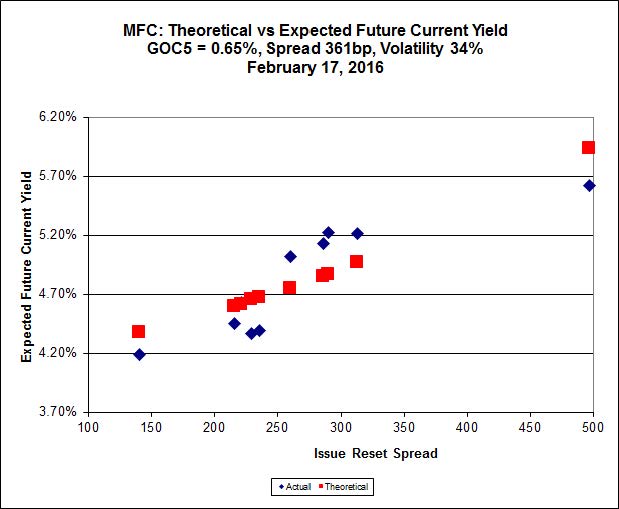

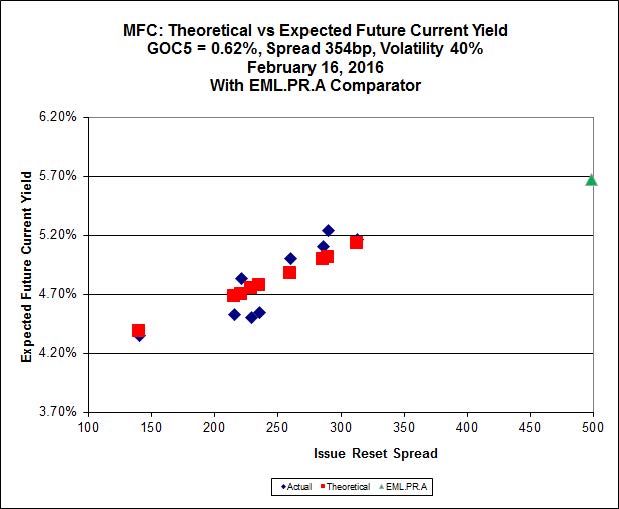

Most expensive is the new issue, resetting at +497bp on 2021-6-19, deemed at 25.00 to be 1.08 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 16.80 to be 1.13 cheap.

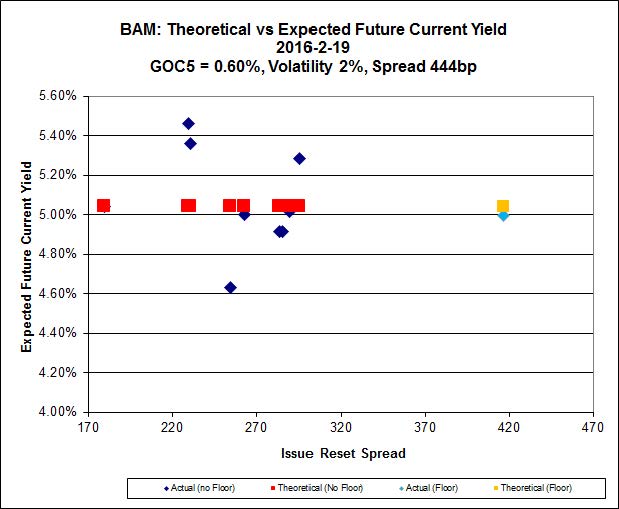

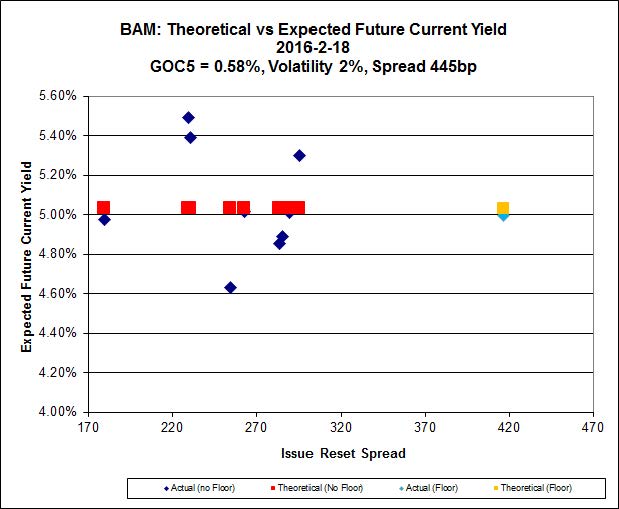

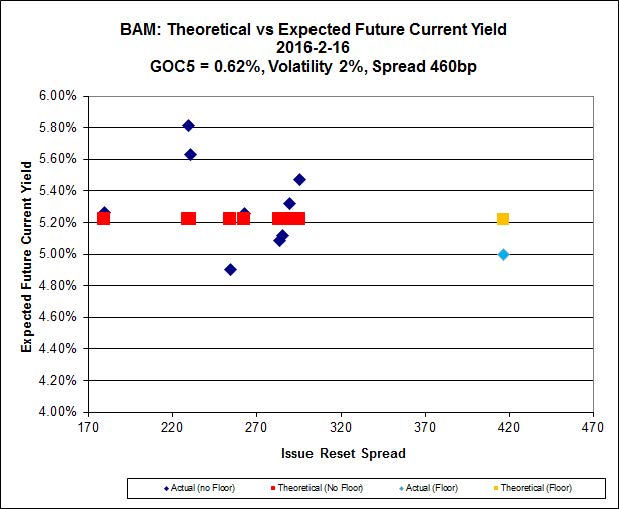

Click for Big

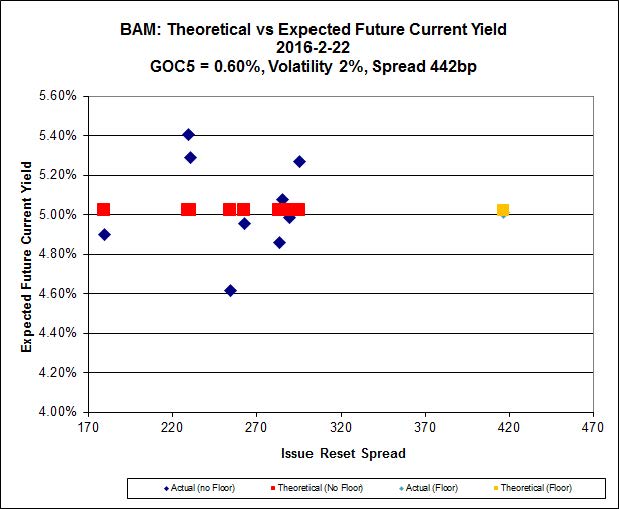

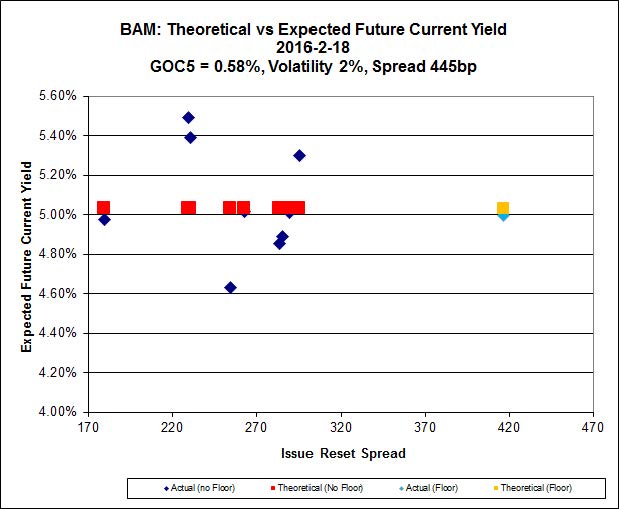

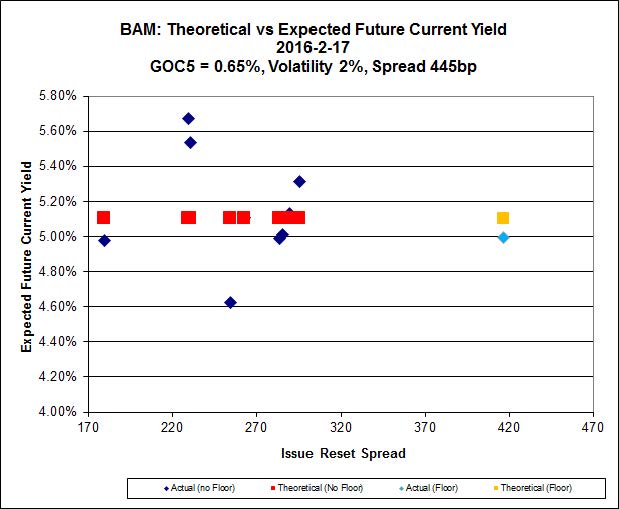

Click for BigThe cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 12.56 to be $1.42 cheap. BAM.PF.H, resetting at +417M500bp on 2020-12-31 is bid at 25.03 and appears to be $1.08 rich.

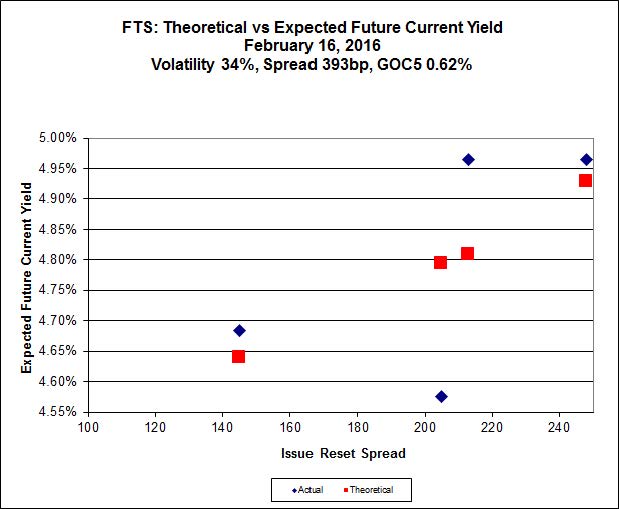

Click for Big

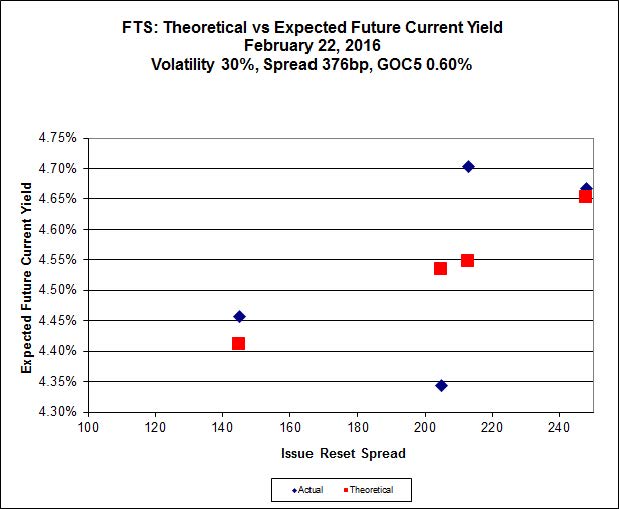

Click for BigFTS.PR.K, with a spread of +205bp, and bid at 14.59, looks $0.67 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 13.85 and is $0.44 cheap.

Click for Big

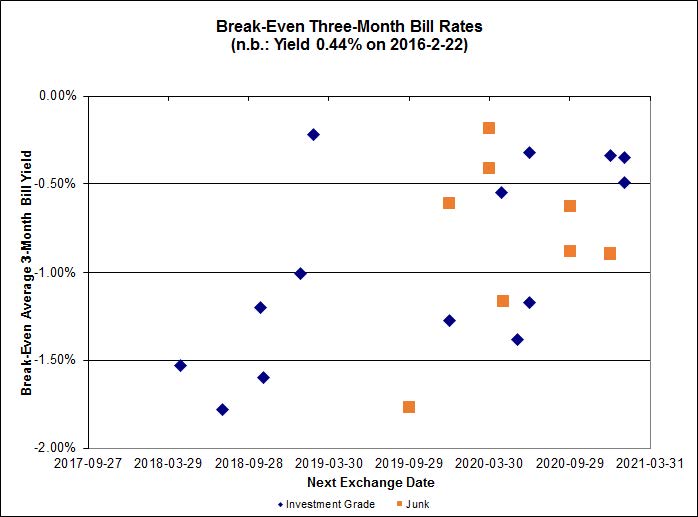

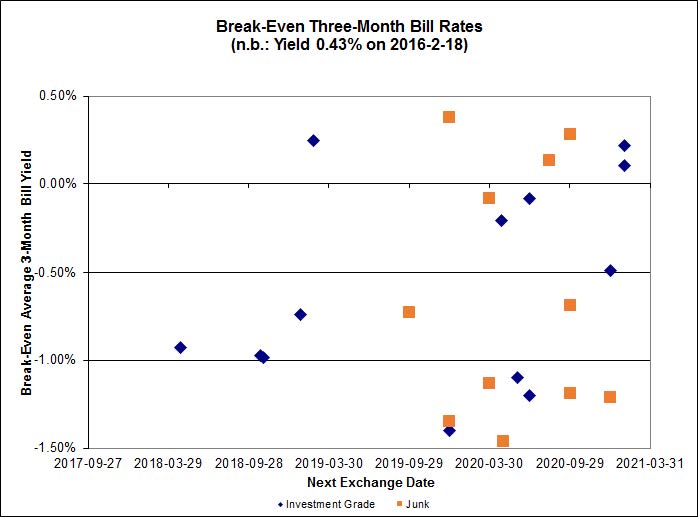

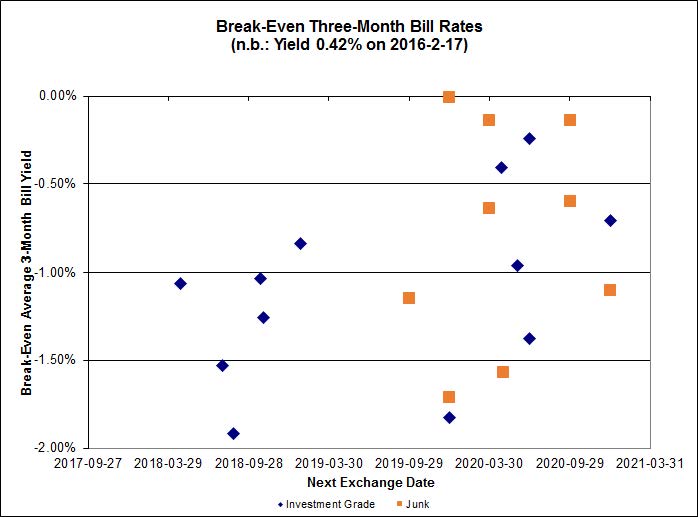

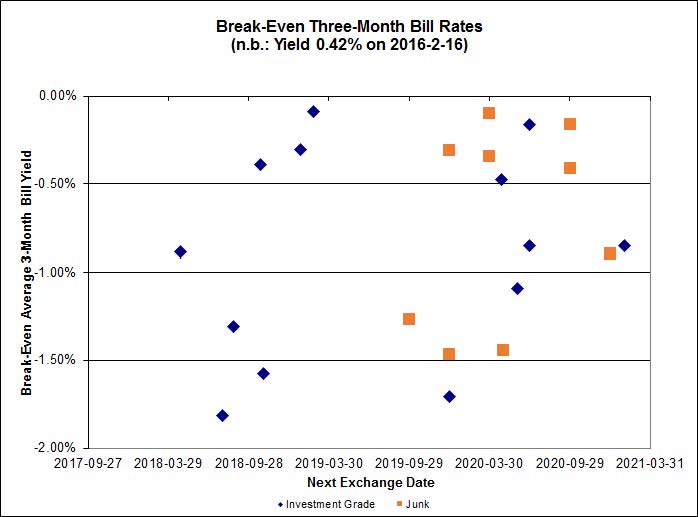

Click for BigInvestment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.62%, with three outliers above 0.50%. Note that the range of the y-axis has been changed. There are two junk outliers above 0.00%.

Click for Big

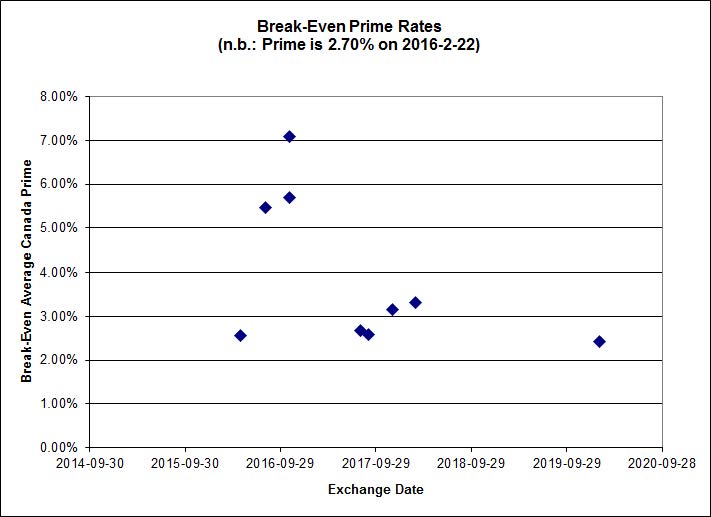

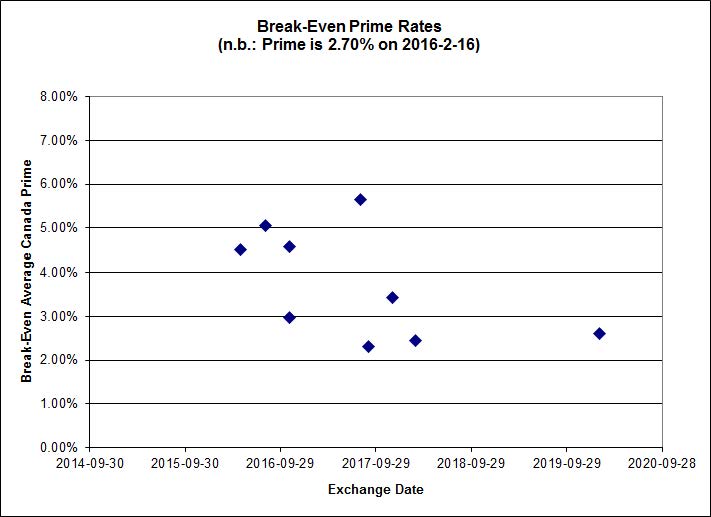

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

5.78 % |

7.02 % |

16,155 |

15.43 |

1 |

-3.6214 % |

1,349.1 |

| FixedFloater |

8.02 % |

7.00 % |

25,969 |

15.17 |

1 |

0.0000 % |

2,479.9 |

| Floater |

5.37 % |

5.64 % |

77,140 |

14.39 |

4 |

-0.3400 % |

1,426.8 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.3717 % |

2,736.8 |

| SplitShare |

4.83 % |

5.91 % |

74,395 |

2.68 |

6 |

0.3717 % |

3,202.6 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.3717 % |

2,498.8 |

| Perpetual-Premium |

5.86 % |

5.83 % |

84,124 |

13.88 |

6 |

0.4957 % |

2,519.9 |

| Perpetual-Discount |

5.81 % |

5.83 % |

98,483 |

14.10 |

33 |

0.0488 % |

2,488.4 |

| FixedReset |

5.82 % |

5.12 % |

210,031 |

14.13 |

84 |

-0.1013 % |

1,743.7 |

| Deemed-Retractible |

5.34 % |

5.89 % |

123,748 |

6.89 |

34 |

0.0000 % |

2,526.8 |

| FloatingReset |

3.12 % |

4.91 % |

49,989 |

5.51 |

16 |

-0.4494 % |

1,958.6 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| PWF.PR.Q |

FloatingReset |

-6.98 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 10.00

Evaluated at bid price : 10.00

Bid-YTW : 5.15 % |

| BAM.PR.E |

Ratchet |

-3.62 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 25.00

Evaluated at bid price : 11.71

Bid-YTW : 7.02 % |

| TD.PF.E |

FixedReset |

-3.52 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 18.07

Evaluated at bid price : 18.07

Bid-YTW : 4.92 % |

| CM.PR.O |

FixedReset |

-3.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 16.00

Evaluated at bid price : 16.00

Bid-YTW : 4.91 % |

| MFC.PR.K |

FixedReset |

-2.97 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 14.70

Bid-YTW : 10.54 % |

| FTS.PR.I |

FloatingReset |

-2.65 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 9.20

Evaluated at bid price : 9.20

Bid-YTW : 5.14 % |

| NA.PR.S |

FixedReset |

-2.07 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 16.05

Evaluated at bid price : 16.05

Bid-YTW : 5.00 % |

| PWF.PR.T |

FixedReset |

-1.96 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 19.02

Evaluated at bid price : 19.02

Bid-YTW : 4.17 % |

| TD.PF.F |

Perpetual-Discount |

-1.96 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 21.76

Evaluated at bid price : 22.06

Bid-YTW : 5.59 % |

| RY.PR.M |

FixedReset |

-1.81 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 16.83

Evaluated at bid price : 16.83

Bid-YTW : 4.94 % |

| NA.PR.Q |

FixedReset |

-1.77 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.15

Bid-YTW : 5.56 % |

| MFC.PR.N |

FixedReset |

-1.70 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.22

Bid-YTW : 9.41 % |

| MFC.PR.L |

FixedReset |

-1.60 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 15.35

Bid-YTW : 10.06 % |

| BAM.PR.B |

Floater |

-1.54 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 8.32

Evaluated at bid price : 8.32

Bid-YTW : 5.76 % |

| BMO.PR.Y |

FixedReset |

-1.52 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 18.12

Evaluated at bid price : 18.12

Bid-YTW : 4.74 % |

| BAM.PF.F |

FixedReset |

-1.45 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 17.00

Evaluated at bid price : 17.00

Bid-YTW : 5.49 % |

| MFC.PR.M |

FixedReset |

-1.44 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.40

Bid-YTW : 9.33 % |

| TD.PF.D |

FixedReset |

-1.40 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 17.55

Evaluated at bid price : 17.55

Bid-YTW : 4.93 % |

| MFC.PR.I |

FixedReset |

-1.33 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.05

Bid-YTW : 9.07 % |

| BMO.PR.T |

FixedReset |

-1.28 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 16.20

Evaluated at bid price : 16.20

Bid-YTW : 4.70 % |

| BNS.PR.R |

FixedReset |

-1.27 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.23

Bid-YTW : 4.61 % |

| BNS.PR.Q |

FixedReset |

-1.26 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.80

Bid-YTW : 4.68 % |

| MFC.PR.H |

FixedReset |

-1.20 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.15

Bid-YTW : 8.42 % |

| BAM.PR.K |

Floater |

-1.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 8.50

Evaluated at bid price : 8.50

Bid-YTW : 5.64 % |

| TD.PR.Z |

FloatingReset |

-1.11 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.45

Bid-YTW : 4.85 % |

| BAM.PR.C |

Floater |

-1.07 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 8.30

Evaluated at bid price : 8.30

Bid-YTW : 5.78 % |

| TD.PR.T |

FloatingReset |

-1.07 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.28

Bid-YTW : 4.91 % |

| BMO.PR.M |

FixedReset |

-1.03 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.01

Bid-YTW : 4.27 % |

| HSE.PR.G |

FixedReset |

-1.02 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 14.60

Evaluated at bid price : 14.60

Bid-YTW : 7.44 % |

| RY.PR.A |

Deemed-Retractible |

-1.01 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.56

Bid-YTW : 5.61 % |

| BAM.PF.E |

FixedReset |

1.00 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 16.16

Evaluated at bid price : 16.16

Bid-YTW : 5.41 % |

| TD.PF.A |

FixedReset |

1.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 16.65

Evaluated at bid price : 16.65

Bid-YTW : 4.61 % |

| NA.PR.W |

FixedReset |

1.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 15.27

Evaluated at bid price : 15.27

Bid-YTW : 5.07 % |

| BIP.PR.B |

FixedReset |

1.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 22.72

Evaluated at bid price : 23.85

Bid-YTW : 5.82 % |

| PVS.PR.D |

SplitShare |

1.10 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2021-10-08

Maturity Price : 25.00

Evaluated at bid price : 22.90

Bid-YTW : 6.53 % |

| TD.PF.C |

FixedReset |

1.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 16.61

Evaluated at bid price : 16.61

Bid-YTW : 4.60 % |

| BMO.PR.K |

Deemed-Retractible |

1.21 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2016-11-25

Maturity Price : 25.00

Evaluated at bid price : 25.15

Bid-YTW : 4.32 % |

| SLF.PR.J |

FloatingReset |

1.27 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 11.14

Bid-YTW : 12.29 % |

| BAM.PR.X |

FixedReset |

1.32 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 11.50

Evaluated at bid price : 11.50

Bid-YTW : 5.69 % |

| PWF.PR.O |

Perpetual-Premium |

1.34 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 24.49

Evaluated at bid price : 25.00

Bid-YTW : 5.83 % |

| GWO.PR.N |

FixedReset |

1.34 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 12.12

Bid-YTW : 11.53 % |

| FTS.PR.M |

FixedReset |

1.36 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 15.61

Evaluated at bid price : 15.61

Bid-YTW : 5.29 % |

| HSE.PR.A |

FixedReset |

1.61 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 8.18

Evaluated at bid price : 8.18

Bid-YTW : 7.24 % |

| FTS.PR.K |

FixedReset |

1.67 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 14.59

Evaluated at bid price : 14.59

Bid-YTW : 4.93 % |

| TRP.PR.A |

FixedReset |

1.68 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 13.32

Evaluated at bid price : 13.32

Bid-YTW : 5.10 % |

| BAM.PF.B |

FixedReset |

1.71 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 15.46

Evaluated at bid price : 15.46

Bid-YTW : 5.60 % |

| TRP.PR.B |

FixedReset |

1.78 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 9.70

Evaluated at bid price : 9.70

Bid-YTW : 5.07 % |

| BAM.PR.R |

FixedReset |

1.95 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 12.56

Evaluated at bid price : 12.56

Bid-YTW : 5.94 % |

| PWF.PR.A |

Floater |

2.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 10.05

Evaluated at bid price : 10.05

Bid-YTW : 4.73 % |

| HSE.PR.C |

FixedReset |

2.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 13.54

Evaluated at bid price : 13.54

Bid-YTW : 7.40 % |

| BAM.PR.T |

FixedReset |

2.04 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 13.01

Evaluated at bid price : 13.01

Bid-YTW : 5.88 % |

| IAG.PR.A |

Deemed-Retractible |

2.09 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.00

Bid-YTW : 7.18 % |

| TRP.PR.H |

FloatingReset |

2.21 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 8.79

Evaluated at bid price : 8.79

Bid-YTW : 4.95 % |

| SLF.PR.I |

FixedReset |

2.52 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.30

Bid-YTW : 9.37 % |

| SLF.PR.H |

FixedReset |

3.42 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.91

Bid-YTW : 10.82 % |

| MFC.PR.F |

FixedReset |

4.20 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 11.67

Bid-YTW : 12.13 % |

| SLF.PR.G |

FixedReset |

5.92 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 12.71

Bid-YTW : 11.01 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| EML.PR.A |

FixedReset |

351,820 |

New issue settled today.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.73

Bid-YTW : 5.88 % |

| BMO.PR.Q |

FixedReset |

234,685 |

Desjardins crossed blocks of 200,000 and 19,900, both at 17.85.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.85

Bid-YTW : 8.05 % |

| PWF.PR.L |

Perpetual-Discount |

206,022 |

Nesbitt and TD crossed 100,000 shares each, both at 22.05.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 21.81

Evaluated at bid price : 22.05

Bid-YTW : 5.83 % |

| TD.PF.G |

FixedReset |

110,273 |

RBC crossed 10,000 at 25.40.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 23.26

Evaluated at bid price : 25.35

Bid-YTW : 5.20 % |

| PWF.PR.K |

Perpetual-Discount |

101,110 |

Nesbitt crossed 100,000 at 21.40.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 21.50

Evaluated at bid price : 21.50

Bid-YTW : 5.82 % |

| RY.PR.Q |

FixedReset |

86,662 |

TD crossed 11,500 at 25.41. RBC crossed 10,000 at 25.42.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 23.27

Evaluated at bid price : 25.40

Bid-YTW : 5.12 % |

| There were 44 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| NA.PR.Q |

FixedReset |

Quote: 22.15 – 22.98

Spot Rate : 0.8300

Average : 0.5693

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.15

Bid-YTW : 5.56 % |

| HSE.PR.G |

FixedReset |

Quote: 14.60 – 15.50

Spot Rate : 0.9000

Average : 0.6424

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 14.60

Evaluated at bid price : 14.60

Bid-YTW : 7.44 % |

| TD.PF.F |

Perpetual-Discount |

Quote: 22.06 – 22.67

Spot Rate : 0.6100

Average : 0.3760

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 21.76

Evaluated at bid price : 22.06

Bid-YTW : 5.59 % |

| TD.PR.Z |

FloatingReset |

Quote: 21.45 – 22.17

Spot Rate : 0.7200

Average : 0.5311

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.45

Bid-YTW : 4.85 % |

| PWF.PR.Q |

FloatingReset |

Quote: 10.00 – 11.90

Spot Rate : 1.9000

Average : 1.7164

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-02-16

Maturity Price : 10.00

Evaluated at bid price : 10.00

Bid-YTW : 5.15 % |

| TD.PR.T |

FloatingReset |

Quote: 21.28 – 21.88

Spot Rate : 0.6000

Average : 0.4366

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.28

Bid-YTW : 4.91 % |