While preparing PrefLetter I came across this interesting chart, from a presentation by BoC Deputy Governor Lynn Patterson:

Click for Big

Speaking of the BoC, the Business Outlook Survey is spreading gloom:

The quarterly survey of business executives, published by the central bank Monday, showed that the prolonged oil slump is taking a deepening toll on the mood of the country’s corporate leaders. It also shows that, increasingly, the negative impact and mounting pessimism are infecting parts of the economy beyond the resource sector.

What’s more, the details press on many of the hot buttons for the bank’s decision on interest rates, the next of which comes only days from now (Jan. 20). Spending intentions for new capacity and hiring are at their lowest since the Great Recession; businesses still have ample excess capacity; already-tepid inflation expectations are declining.

…

Neither the bond market nor the majority of economists expect a cut next week, but the Business Outlook Survey has made a cut look like a serious possibility at some point in the next few months. At least one prominent central-bank watcher – Merrill Lynch economist Emanuella Enenajor – is convinced that the survey seals the deal on a quarter-point rate cut next week.

It’s not getting any better! Oil and copper got crushed today:

Oil plunged to its lowest point since 2003 on Monday, as West Texas intermediate (WTI), the North American benchmark, declined to $31.12 (U.S.) a barrel. It has lost 15 per cent of its value in the first few days of 2016.

Copper, meanwhile, tumbled to a six-year low of $1.97 a pound. The metal, used for a wide variety of industrial and construction applications, is down more than 9 per cent in January.

… which is putting the banks under pressure:

Consider the urgency: The price of oil – exploring 12-year lows – is fast-approaching worst-case hypothetical scenarios used in bank stress tests in 2015, raising concerns about whether loan losses will spike as energy companies fail to meet their debt obligations. Big Six loans to the oil and gas sector total nearly $113-billion.

…

The lower prices are nearing, or passing through, some significant thresholds. Canadian Imperial Bank of Commerce used $30 oil in its stress tests a year ago; Bank of Montreal stress-tested its loan portfolio at $35 a barrel in 2015, and assumed that oil would recover to $50 a barrel this year.

Financial 15 Split Corp., proud issuer of FTN.PR.A, has been confirmed at Pfd-4(high) by DBRS:

DBRS Limited (DBRS) has today confirmed the rating of the Preferred Shares (the Preferred Shares) issued by Financial 15 Split Corp. (the Company) at Pfd-4 (high).

…

During 2015, the NAV of the Company has experienced some fluctuation due to volatility in the markets. Downside protection available to holders of the Preferred Shares is 40.7% as of December 15, 2015. The dividend coverage ratio has risen to 0.6 times over the past year. Regular monthly Class A Share distributions will result in an average grind of approximately 3.5% over the next five years.

Happy preferred share investors held a parade in honour of the market today!

Click for Big

It was yet another grim day for the Canadian preferred share market today, with PerpetualDiscounts off 68bp, FixedResets losing a stunning 199bp and DeemedRetractibles down 84bp. The Performance Highlights table is, of course, ridiculous. Volume was well above average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

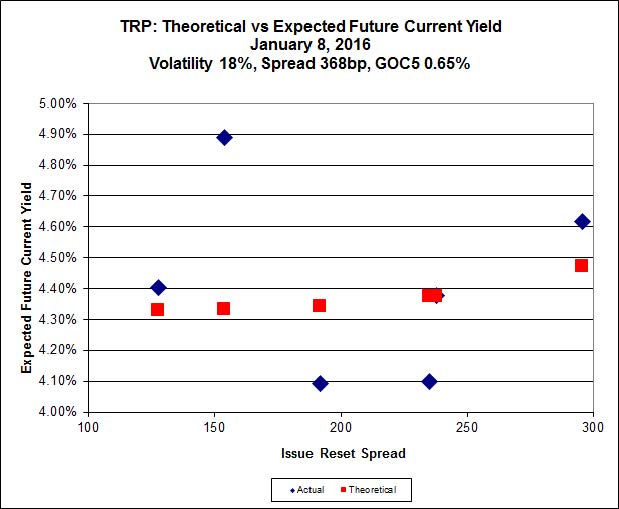

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.51 to be $1.03 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $1.23 cheap at its bid price of 10.85.

Click for Big

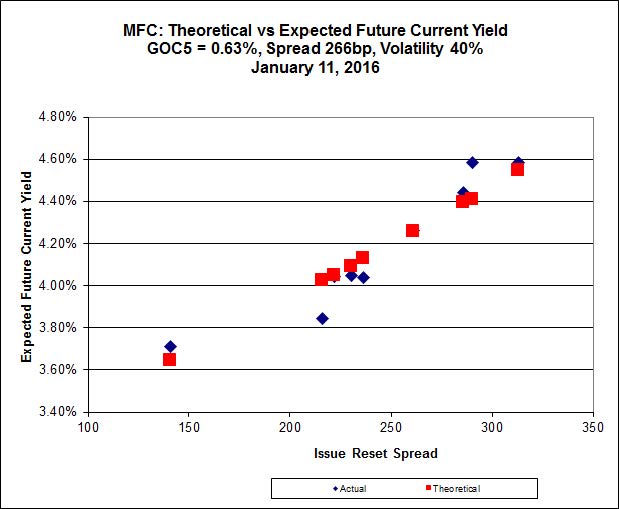

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 18.15 to be 0.82 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 19.25 to be 0.77 cheap.

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 14.60 to be $0.99 cheap. BAM.PR.X, resetting at +180bp on 2017-6-30 is bid at 13.67 and appears to be $0.74 rich.

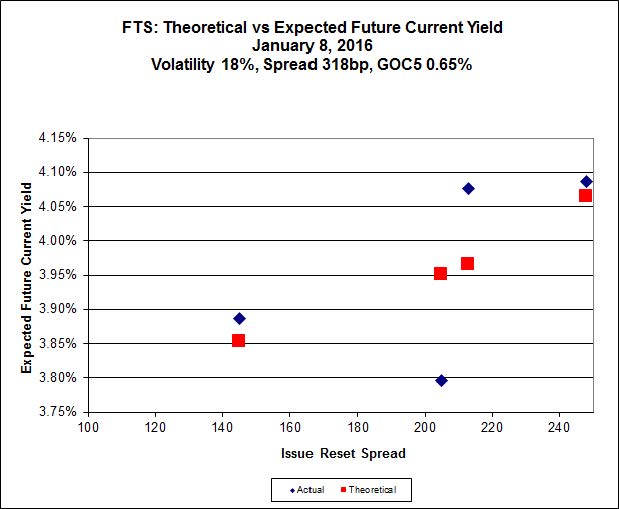

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 17.62, looks $0.84 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 16.51 and is $0.70 cheap.

Click for Big

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.78%, with one outlier above 0.00%. There is one junk outlier below -2.00% and four above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.70 % | 5.69 % | 27,014 | 17.02 | 1 | 1.4035 % | 1,656.8 |

| FixedFloater | 7.14 % | 6.34 % | 32,242 | 15.77 | 1 | 2.4653 % | 2,732.1 |

| Floater | 4.37 % | 4.53 % | 79,818 | 16.38 | 4 | -1.9065 % | 1,747.5 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0137 % | 2,736.1 |

| SplitShare | 4.83 % | 5.79 % | 70,997 | 1.80 | 6 | 0.0137 % | 3,201.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0137 % | 2,498.1 |

| Perpetual-Premium | 5.90 % | 5.81 % | 85,367 | 2.72 | 6 | -0.5476 % | 2,501.6 |

| Perpetual-Discount | 5.76 % | 5.85 % | 94,429 | 14.14 | 34 | -0.6755 % | 2,503.4 |

| FixedReset | 5.44 % | 4.82 % | 237,193 | 15.07 | 81 | -1.9911 % | 1,896.8 |

| Deemed-Retractible | 5.32 % | 5.20 % | 122,011 | 5.27 | 34 | -0.8429 % | 2,531.0 |

| FloatingReset | 2.89 % | 4.79 % | 62,006 | 5.60 | 13 | -0.6169 % | 2,044.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.A | FixedReset | -7.26 % | Not real. The issue traded 5,880 shares today in a range of 15.18-84 before closing at 14.56-24, 1×1. The last trade of the day was at 2:17pm, at 15.18. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 14.56 Evaluated at bid price : 14.56 Bid-YTW : 4.70 % |

| BAM.PF.E | FixedReset | -5.34 % | Sort of real. The issue traded 10,590 shares today in a range of 17.36-33 before closing at 17.36-60, 4×1. The VWAP was 17.68. We’ll give the Exchange and the market maker a pass on this one, largely because I’m such a nice guy. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 17.36 Evaluated at bid price : 17.36 Bid-YTW : 5.05 % |

| TRP.PR.H | FloatingReset | -5.23 % | Reasonably real. The issue traded 8,659 shares in a range of 9.26-80 before closing at 9.25-75, 4×1. VWAP was 9.68. But really, guys a 5%+ quote spread? I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 9.25 Evaluated at bid price : 9.25 Bid-YTW : 4.65 % |

| HSE.PR.C | FixedReset | -5.14 % | Exaggerated. The issue traded 9,300 shares in a range of 16.62-17.95 before closing at 16.79-50, 2×30. VWAP was 17.28; the last trade was at 17.02 for 100 shares, timestamped 2:50pm. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 16.79 Evaluated at bid price : 16.79 Bid-YTW : 5.94 % |

| BAM.PR.T | FixedReset | -5.09 % | Well, OK. The issue traded 13,600 shares today in a range of 15.01-91 before closing at 15.11-30, 5×2. VWAP was 15.49; the last trade was for 500 shares at 15.12 timestamped 3:48. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 15.11 Evaluated at bid price : 15.11 Bid-YTW : 5.10 % |

| BAM.PF.A | FixedReset | -4.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 18.60 Evaluated at bid price : 18.60 Bid-YTW : 5.00 % |

| BAM.PR.K | Floater | -4.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 10.12 Evaluated at bid price : 10.12 Bid-YTW : 4.70 % |

| BAM.PF.F | FixedReset | -4.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 19.02 Evaluated at bid price : 19.02 Bid-YTW : 4.92 % |

| TRP.PR.E | FixedReset | -4.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 17.51 Evaluated at bid price : 17.51 Bid-YTW : 4.65 % |

| HSE.PR.G | FixedReset | -4.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 6.01 % |

| BAM.PR.R | FixedReset | -3.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 14.60 Evaluated at bid price : 14.60 Bid-YTW : 5.16 % |

| TRP.PR.D | FixedReset | -3.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 16.65 Evaluated at bid price : 16.65 Bid-YTW : 4.82 % |

| BAM.PR.X | FixedReset | -3.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 13.67 Evaluated at bid price : 13.67 Bid-YTW : 4.82 % |

| MFC.PR.H | FixedReset | -3.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.50 Bid-YTW : 6.65 % |

| PWF.PR.P | FixedReset | -3.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 12.81 Evaluated at bid price : 12.81 Bid-YTW : 4.41 % |

| BAM.PF.G | FixedReset | -3.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 18.86 Evaluated at bid price : 18.86 Bid-YTW : 4.99 % |

| BAM.PF.B | FixedReset | -3.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 4.96 % |

| IFC.PR.A | FixedReset | -3.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.80 Bid-YTW : 9.82 % |

| BMO.PR.M | FixedReset | -3.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.25 Bid-YTW : 4.21 % |

| FTS.PR.G | FixedReset | -3.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 16.51 Evaluated at bid price : 16.51 Bid-YTW : 4.51 % |

| SLF.PR.H | FixedReset | -3.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.65 Bid-YTW : 9.11 % |

| TRP.PR.C | FixedReset | -3.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 10.85 Evaluated at bid price : 10.85 Bid-YTW : 5.07 % |

| CM.PR.Q | FixedReset | -2.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 4.65 % |

| GWO.PR.N | FixedReset | -2.93 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.91 Bid-YTW : 10.56 % |

| HSE.PR.A | FixedReset | -2.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 10.81 Evaluated at bid price : 10.81 Bid-YTW : 5.56 % |

| MFC.PR.N | FixedReset | -2.74 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.10 Bid-YTW : 7.77 % |

| SLF.PR.B | Deemed-Retractible | -2.74 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.59 Bid-YTW : 7.60 % |

| TRP.PR.B | FixedReset | -2.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 10.66 Evaluated at bid price : 10.66 Bid-YTW : 4.69 % |

| FTS.PR.J | Perpetual-Discount | -2.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 21.21 Evaluated at bid price : 21.21 Bid-YTW : 5.68 % |

| SLF.PR.C | Deemed-Retractible | -2.69 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.50 Bid-YTW : 7.97 % |

| TRP.PR.G | FixedReset | -2.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 19.03 Evaluated at bid price : 19.03 Bid-YTW : 4.87 % |

| SLF.PR.A | Deemed-Retractible | -2.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.62 Bid-YTW : 7.52 % |

| PWF.PR.S | Perpetual-Discount | -2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 20.40 Evaluated at bid price : 20.40 Bid-YTW : 5.90 % |

| BMO.PR.Q | FixedReset | -2.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.10 Bid-YTW : 6.97 % |

| BNS.PR.P | FixedReset | -2.56 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.58 Bid-YTW : 4.01 % |

| MFC.PR.M | FixedReset | -2.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.50 Bid-YTW : 7.54 % |

| BMO.PR.S | FixedReset | -2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 18.05 Evaluated at bid price : 18.05 Bid-YTW : 4.44 % |

| MFC.PR.C | Deemed-Retractible | -2.42 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.76 Bid-YTW : 7.87 % |

| BAM.PR.Z | FixedReset | -2.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 5.04 % |

| SLF.PR.E | Deemed-Retractible | -2.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.68 Bid-YTW : 7.90 % |

| MFC.PR.J | FixedReset | -2.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.00 Bid-YTW : 7.19 % |

| BNS.PR.Q | FixedReset | -2.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.04 Bid-YTW : 4.44 % |

| BNS.PR.R | FixedReset | -2.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.52 Bid-YTW : 4.32 % |

| TD.PF.D | FixedReset | -2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 18.85 Evaluated at bid price : 18.85 Bid-YTW : 4.62 % |

| GWO.PR.S | Deemed-Retractible | -2.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.58 Bid-YTW : 6.14 % |

| SLF.PR.I | FixedReset | -2.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.11 Bid-YTW : 7.84 % |

| CM.PR.P | FixedReset | -2.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 17.28 Evaluated at bid price : 17.28 Bid-YTW : 4.47 % |

| IFC.PR.C | FixedReset | -2.19 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.90 Bid-YTW : 7.88 % |

| CIU.PR.C | FixedReset | -2.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 11.65 Evaluated at bid price : 11.65 Bid-YTW : 4.43 % |

| TD.PR.S | FixedReset | -2.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.50 Bid-YTW : 3.85 % |

| MFC.PR.I | FixedReset | -2.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.65 Bid-YTW : 7.00 % |

| CU.PR.F | Perpetual-Discount | -2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 19.66 Evaluated at bid price : 19.66 Bid-YTW : 5.81 % |

| MFC.PR.B | Deemed-Retractible | -2.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.13 Bid-YTW : 7.78 % |

| FTS.PR.M | FixedReset | -2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 18.76 Evaluated at bid price : 18.76 Bid-YTW : 4.50 % |

| TD.PF.C | FixedReset | -1.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 17.27 Evaluated at bid price : 17.27 Bid-YTW : 4.47 % |

| SLF.PR.G | FixedReset | -1.96 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.02 Bid-YTW : 9.58 % |

| BMO.PR.W | FixedReset | -1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 17.53 Evaluated at bid price : 17.53 Bid-YTW : 4.43 % |

| IAG.PR.A | Deemed-Retractible | -1.92 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.40 Bid-YTW : 7.50 % |

| PWF.PR.H | Perpetual-Premium | -1.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 23.89 Evaluated at bid price : 24.14 Bid-YTW : 5.96 % |

| BAM.PR.C | Floater | -1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 10.30 Evaluated at bid price : 10.30 Bid-YTW : 4.62 % |

| GWO.PR.P | Deemed-Retractible | -1.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.29 Bid-YTW : 6.48 % |

| TD.PF.B | FixedReset | -1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 17.65 Evaluated at bid price : 17.65 Bid-YTW : 4.37 % |

| CM.PR.O | FixedReset | -1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 4.39 % |

| SLF.PR.D | Deemed-Retractible | -1.62 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.48 Bid-YTW : 7.98 % |

| RY.PR.I | FixedReset | -1.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.27 Bid-YTW : 4.51 % |

| CU.PR.G | Perpetual-Discount | -1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 19.76 Evaluated at bid price : 19.76 Bid-YTW : 5.78 % |

| BMO.PR.Y | FixedReset | -1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 19.30 Evaluated at bid price : 19.30 Bid-YTW : 4.55 % |

| HSE.PR.E | FixedReset | -1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 18.10 Evaluated at bid price : 18.10 Bid-YTW : 5.98 % |

| GWO.PR.R | Deemed-Retractible | -1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.80 Bid-YTW : 7.45 % |

| RY.PR.J | FixedReset | -1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 18.94 Evaluated at bid price : 18.94 Bid-YTW : 4.60 % |

| BIP.PR.B | FixedReset | -1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 22.62 Evaluated at bid price : 23.66 Bid-YTW : 5.84 % |

| CU.PR.E | Perpetual-Discount | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 21.23 Evaluated at bid price : 21.23 Bid-YTW : 5.86 % |

| TD.PR.T | FloatingReset | -1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.40 Bid-YTW : 4.71 % |

| FTS.PR.F | Perpetual-Discount | -1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 21.86 Evaluated at bid price : 22.10 Bid-YTW : 5.61 % |

| IAG.PR.G | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.50 Bid-YTW : 7.02 % |

| GWO.PR.H | Deemed-Retractible | -1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.00 Bid-YTW : 7.37 % |

| TD.PF.A | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 17.78 Evaluated at bid price : 17.78 Bid-YTW : 4.35 % |

| SLF.PR.J | FloatingReset | -1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.75 Bid-YTW : 10.32 % |

| BMO.PR.T | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 17.51 Evaluated at bid price : 17.51 Bid-YTW : 4.47 % |

| BNS.PR.Z | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.85 Bid-YTW : 7.11 % |

| BMO.PR.R | FloatingReset | -1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.76 Bid-YTW : 4.56 % |

| BAM.PF.C | Perpetual-Discount | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 19.98 Evaluated at bid price : 19.98 Bid-YTW : 6.13 % |

| GWO.PR.I | Deemed-Retractible | -1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.00 Bid-YTW : 7.67 % |

| CU.PR.D | Perpetual-Discount | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 21.33 Evaluated at bid price : 21.33 Bid-YTW : 5.83 % |

| GWO.PR.G | Deemed-Retractible | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.45 Bid-YTW : 6.79 % |

| POW.PR.D | Perpetual-Discount | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 21.32 Evaluated at bid price : 21.59 Bid-YTW : 5.81 % |

| RY.PR.M | FixedReset | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 18.81 Evaluated at bid price : 18.81 Bid-YTW : 4.52 % |

| GWO.PR.F | Deemed-Retractible | 1.11 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2016-02-10 Maturity Price : 25.00 Evaluated at bid price : 25.40 Bid-YTW : -10.98 % |

| BAM.PR.E | Ratchet | 1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 25.00 Evaluated at bid price : 14.45 Bid-YTW : 5.69 % |

| RY.PR.K | FloatingReset | 1.87 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.75 Bid-YTW : 4.87 % |

| BAM.PR.G | FixedFloater | 2.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 25.00 Evaluated at bid price : 13.30 Bid-YTW : 6.34 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.Z | FixedReset | 218,179 | Scotia crossed 100,000 at 19.06. RBC crossed 50,000 at the same price. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.85 Bid-YTW : 7.11 % |

| BNS.PR.L | Deemed-Retractible | 209,671 | RBC crossed 192,000 at 24.54. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.46 Bid-YTW : 4.90 % |

| MFC.PR.I | FixedReset | 103,000 | Nesbitt crossed 100,000 at 19.93. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.65 Bid-YTW : 7.00 % |

| RY.PR.C | Deemed-Retractible | 73,612 | RBC crossed 50,000 at 24.89, then bought 13,900 at the same price from TD. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.83 Bid-YTW : 4.87 % |

| TD.PF.C | FixedReset | 55,135 | Scotia crossed 40,000 at 17.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 17.27 Evaluated at bid price : 17.27 Bid-YTW : 4.47 % |

| BMO.PR.T | FixedReset | 51,827 | TD crossed 25,700 at 17.80. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-11 Maturity Price : 17.51 Evaluated at bid price : 17.51 Bid-YTW : 4.47 % |

| There were 42 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BNS.PR.R | FixedReset | Quote: 23.52 – 24.49 Spot Rate : 0.9700 Average : 0.5572 YTW SCENARIO |

| BMO.PR.M | FixedReset | Quote: 23.25 – 24.00 Spot Rate : 0.7500 Average : 0.4770 YTW SCENARIO |

| CIU.PR.C | FixedReset | Quote: 11.65 – 12.90 Spot Rate : 1.2500 Average : 0.9946 YTW SCENARIO |

| TRP.PR.A | FixedReset | Quote: 14.56 – 15.24 Spot Rate : 0.6800 Average : 0.4286 YTW SCENARIO |

| HSE.PR.C | FixedReset | Quote: 16.79 – 17.50 Spot Rate : 0.7100 Average : 0.4596 YTW SCENARIO |

| TD.PR.T | FloatingReset | Quote: 21.40 – 22.04 Spot Rate : 0.6400 Average : 0.4292 YTW SCENARIO |