Nervousness regarding a possible US default continues to run high:

Treasury securities are used widely as collateral across markets. A key question for market participants is how would bonds that are maturing next month be treated if a deal is not reached in time and the Treasury is unable to pay principal and interest on debt.

One such area is the $4 trillion repurchase, or repo, market, for short-term funding used by banks, money market funds and others to borrow and lend. Some counterparties, including banks, were shying away from Treasury bills maturing in June in bilateral repos, where the trade is between two parties, said an executive at a U.S. fund manager who decline to be named. There are 14 T-bills maturing in June.

Scott Skyrm, executive vice president for fixed income and repo at broker-dealer Curvature Securities, said some repo buyers or cash lenders did not want to accept any bills maturing within a year. Skyrm said stress began to appear in the market at the start of May, with some lenders refusing to accept Treasury bills that they perceived as at risk of delayed payments in some types of trades. He declined to name buyers who were not accepting T-bills.

…

In the case that it needs to delay payments on some securities that are maturing, expert groups have suggested in the past that Treasury could help markets to keep functioning by extending the so-called “operational maturity date.” The proposal, detailed in a December 2021 contingency planning document prepared by an expert group, calls for extending the maturities of securities at risk of default by one day at a time.That could allow the security to be technically traded and available for settlement on the Fedwire Securities Service system used for government debt. However, the group warned that it would need many broker-dealers to adjust their trading systems to also be able to do so and the consequences of a delay in payments on securities would still be severe.

The broker-dealer executive said the process was cumbersome because maturity dates subsumed several other calculations about the value of the security. Extending the maturities required the firm to “basically break their own system,” the executive said.

The X-Date is now June 5:

Treasury Secretary Janet L. Yellen said on Friday that the United States will run out of money to pay its bills on time by June 5, moving the goal posts back slightly while maintaining the urgency for congressional leaders to reach a deal to raise or suspend the debt limit.

The letter provided the most precise date yet for when the United States is expected to run out of cash. Ms. Yellen had previously said the United States could hit the so-called X-date — the moment when it does not have enough money to pay all of its bills on time — as soon as June 1.

While the letter to lawmakers provides a tiny bit of wiggle room, it also makes clear the dire financial situation that Treasury is facing. The federal government is required to make more than $130 billion in scheduled payments during the first two days of June — including money to veterans and Social Security and Medicare recipients.

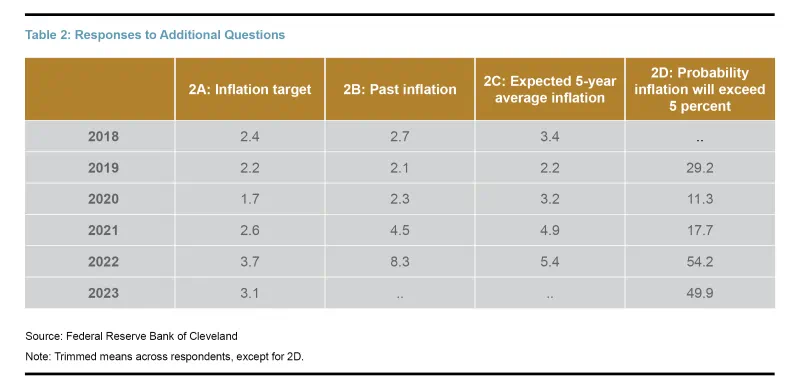

And PCE inflation ticked higher:

The Personal Consumption Expenditures index climbed 4.4 percent in April from a year earlier. That was a slight increase from March, when prices climbed 4.2 percent on an annual basis. Still, prices are not climbing as fast they were in February, when the index rose 5.1 percent on an annual basis.

A “core” measure that tries to gauge underlying inflation trends by stripping out volatile food and energy prices rose 4.7 percent in the year through April, up slightly from 4.6 percent in March.

…

Although Fed officials have noted that inflation has eased in recent months, they have called it “unacceptably high” and far from the central bank’s 2 percent goal.They have also acknowledged some cooling in the labor market, as the number of job openings has fallen recently. But Fed officials have said labor market conditions are still too hot, pointing to solid monthly job gains, steady wage growth and an unemployment rate near historically low levels.

And the IMF has weighed in with a hawkish ‘concluding statement’:

The strength in demand and in labor market outcomes is a double-edged sword, contributing to more persistent inflation. Goods inflation has leveled out and shelter price growth is expected to start moderating in the coming months. However, past nominal wage increases are now feeding into non-shelter services. While core and headline PCE inflation are expected to continue falling during 2023, they will remain materially above the Fed’s 2 percent target throughout 2023 and 2024.

Achieving a sustained disinflation will necessitate a loosening of labor market conditions that, so far, has not been evident in the data. To bring inflation firmly back to target will require an extended period of tight monetary policy, with the federal funds rate remaining at 5¼–5½ percent until late in 2024. Model estimates suggest such a path would be sufficient to slow demand, restore balance to the labor market, and lower wage and price inflation. However, insofar as models are calibrated on past experiences, they offer only an imperfect guide to the current conjuncture.

…

The resilience of the economy and the robustness of labor markets are good news. However, it is possible that the large and rapid increase in interest rates that has already been put in place may not be sufficient to expeditiously bring inflation back to target. With a large share of household and corporate debt contracted at relatively long duration and fixed rates, household consumption and corporate investment have proven less interest-sensitive than in past tightening cycles. This creates a material risk that the Federal Reserve will have to raise the policy rate by significantly more than is currently expected to return inflation to 2 percent. On the positive side, near-term growth outcomes could be better than currently anticipated. However, this would only mean that the economy would slow more abruptly at a later stage (possibly in 2024), creating a recession as tighter monetary policy takes hold. The combination of higher U.S. interest rates, a stronger dollar, and a sharper slowdown in U.S. activity would have significant negative macro-financial spillovers to the rest of the world.The downside risks associated with a less effective monetary transmission, and a more protracted disinflation, could be further complicated by two additional considerations:

First, a higher path for interest rates could reveal larger, more systemic balance sheet problems in banks, nonbanks, or corporates than we have seen to-date. Unrealized losses from holdings of long duration securities would increase in both banks and nonbanks and the cost of new financing for both households and corporates could become unmanageable. Such a tightening of financial conditions could trigger an increase in bankruptcies, worsen credit quality, and heighten stress for those entities carrying high levels of leverage and with large near-term gross financing needs. These financial stability problems could be further exacerbated if the functioning of the Treasury market also becomes compromised. The longer that higher interest rates persist, the greater the likelihood that such fractures will be revealed. Recent failures of large, non-internationally active banks—which have, so far, only had a modest effect on credit conditions—could potentially be a prelude to more serious and ingrained systemic financial stability problems.

Second, brinkmanship over the federal debt ceiling could create a further, entirely avoidable systemic risk to both the U.S. and the global economy at a time when there are already visible strains. To avoid exacerbating downside risks, the debt ceiling should be immediately raised or suspended by Congress, allowing negotiations over the FY2024 budget to begin in earnest. Furthermore, a more permanent solution to this recurring stand-off should be found through institutional changes that ensure that, once appropriations are approved, the corresponding space on the debt ceiling is automatically provided to finance that spending.

Credit losses, whether real or projected, have been in the news lately – and BIS has released a Working Paper by Li Lian Ong, Christian Schmieder and Min Wei titled Insights into Credit Loss Rates: A Global Database:

Focus

Credit risk was a key factor in the Great Financial Crisis and numerous other crises. Banks’ overall credit losses tend to increase suddenly during a crisis from the typically low levels seen during “normal” times. The Covid-19 pandemic underscored the need for accurate credit risk assessments of bank balance sheets. In this paper, we present alternative micro- and macroprudential concepts and metrics to establish actual credit loss rates as well as forward-looking market- and macro-implied credit loss rate estimates for most jurisdictions worldwide. We also provide a public dashboard featuring 10 downloadable economy-level credit loss rate metrics, which will be updated regularly.Contribution

This project aims to help close the long-standing data gap issue on economy-level credit loss information by providing a valuable public resource for researchers, policymakers and practitioners. Building upon previous work by Daniel Hardy and Christian Schmieder, we combine time series of actual credit losses with forward-looking market- and macro-implied credit loss estimates. We provide various credit loss rate series for as many jurisdictions worldwide as possible, which will be updated as new information becomes available. The estimates are available in a dashboard, and users can easily download the data sets of credit loss metrics for the desired jurisdictions and time periods. Additionally, we provide a tool for users to run simplified scenario analyses based on projected GDP growth paths.Findings

The paper presents various metrics of credit loss rates derived from multiple sources, each with its own unique purpose and usefulness. While granular information, such as sector-level statistics, would be ideal for precise loss estimation, such data remain scarce. The economy-specific time series estimated in the paper can be valuable for credit loss analyses and projections, but future work on calibrations may be necessary. Given the challenges associated with anticipating peaks in credit loss rates, one option presented in this paper is to use GDP-implied loss rate simulations, akin to those typically applied in stress tests.Abstract

Credit risk has played a significant role in many financial crises, including the great financial crisis. The COVID-19 pandemic also highlighted bank credit losses to the private sector. However, there remains a significant gap in terms of reliable economy-level credit risk data for financial stability analysis, given that such information is not readily available to the public in any systematic manner. Building upon the work of Hardy and Schmieder (2020), we derive time series of actual as well as forward-looking market- and macro-implied credit loss rates for the majority of jurisdictions around the world. Our database, intended as a public good, is available through a user-friendly interactive dashboard, which allows downloads of credit loss rate time series for the desired jurisdiction(s). Users are also able to run simple scenario analyses based on their projected GDP paths. The data series will be updated on an ongoing basis as new information is published by the original sources.

…

The possible uses of the estimated data series are illustrated with a variety of examples, covering the majority of jurisdictions worldwide (https://www.amro-asia.org/credit-lossrates/).

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3600 % | 2,127.7 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3600 % | 4,081.0 |

| Floater | 10.59 % | 10.84 % | 48,878 | 8.81 | 2 | -0.3600 % | 2,351.9 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1649 % | 3,351.9 |

| SplitShare | 5.02 % | 7.08 % | 38,580 | 2.55 | 7 | -0.1649 % | 4,002.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1649 % | 3,123.2 |

| Perpetual-Premium | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.4692 % | 2,638.0 |

| Perpetual-Discount | 6.47 % | 6.56 % | 43,136 | 13.10 | 34 | -0.4692 % | 2,876.6 |

| FixedReset Disc | 6.10 % | 8.49 % | 85,870 | 11.17 | 63 | -0.0656 % | 2,040.6 |

| Insurance Straight | 6.34 % | 6.52 % | 59,429 | 13.10 | 19 | 0.0997 % | 2,834.6 |

| FloatingReset | 10.86 % | 11.58 % | 51,700 | 8.31 | 2 | -0.1727 % | 2,345.7 |

| FixedReset Prem | 6.99 % | 6.88 % | 324,030 | 12.48 | 1 | -0.2776 % | 2,313.6 |

| FixedReset Bank Non | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0656 % | 2,085.9 |

| FixedReset Ins Non | 6.18 % | 7.67 % | 81,984 | 11.67 | 11 | -0.2874 % | 2,254.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| ELF.PR.F | Perpetual-Discount | -16.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 17.10 Evaluated at bid price : 17.10 Bid-YTW : 7.90 % |

| SLF.PR.E | Insurance Straight | -8.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 17.37 Evaluated at bid price : 17.37 Bid-YTW : 6.61 % |

| BN.PF.F | FixedReset Disc | -5.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 14.41 Evaluated at bid price : 14.41 Bid-YTW : 10.75 % |

| BN.PR.R | FixedReset Disc | -2.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 12.60 Evaluated at bid price : 12.60 Bid-YTW : 10.33 % |

| BN.PR.M | Perpetual-Discount | -2.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 17.01 Evaluated at bid price : 17.01 Bid-YTW : 7.13 % |

| BN.PF.D | Perpetual-Discount | -2.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 17.55 Evaluated at bid price : 17.55 Bid-YTW : 7.13 % |

| BN.PR.T | FixedReset Disc | -2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 12.85 Evaluated at bid price : 12.85 Bid-YTW : 10.27 % |

| BN.PF.B | FixedReset Disc | -2.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 15.17 Evaluated at bid price : 15.17 Bid-YTW : 10.09 % |

| PWF.PR.S | Perpetual-Discount | -2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 18.61 Evaluated at bid price : 18.61 Bid-YTW : 6.54 % |

| GWO.PR.T | Insurance Straight | -1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 20.06 Evaluated at bid price : 20.06 Bid-YTW : 6.54 % |

| BN.PR.K | Floater | -1.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 11.00 Evaluated at bid price : 11.00 Bid-YTW : 10.98 % |

| MFC.PR.L | FixedReset Ins Non | -1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 15.51 Evaluated at bid price : 15.51 Bid-YTW : 8.88 % |

| BN.PR.N | Perpetual-Discount | -1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 17.21 Evaluated at bid price : 17.21 Bid-YTW : 7.04 % |

| GWO.PR.Q | Insurance Straight | -1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 6.61 % |

| CU.PR.C | FixedReset Disc | -1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 17.85 Evaluated at bid price : 17.85 Bid-YTW : 8.00 % |

| CM.PR.S | FixedReset Disc | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 20.56 Evaluated at bid price : 20.56 Bid-YTW : 7.28 % |

| BN.PR.Z | FixedReset Disc | -1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 18.65 Evaluated at bid price : 18.65 Bid-YTW : 8.65 % |

| ELF.PR.G | Perpetual-Discount | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 18.25 Evaluated at bid price : 18.25 Bid-YTW : 6.61 % |

| PWF.PR.O | Perpetual-Discount | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 21.75 Evaluated at bid price : 22.00 Bid-YTW : 6.67 % |

| MFC.PR.J | FixedReset Ins Non | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 21.11 Evaluated at bid price : 21.11 Bid-YTW : 7.24 % |

| BN.PF.J | FixedReset Disc | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 20.55 Evaluated at bid price : 20.55 Bid-YTW : 8.02 % |

| GWO.PR.L | Insurance Straight | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 21.29 Evaluated at bid price : 21.56 Bid-YTW : 6.67 % |

| CM.PR.O | FixedReset Disc | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 16.11 Evaluated at bid price : 16.11 Bid-YTW : 8.76 % |

| BN.PR.X | FixedReset Disc | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 13.51 Evaluated at bid price : 13.51 Bid-YTW : 9.57 % |

| MFC.PR.I | FixedReset Ins Non | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 21.29 Evaluated at bid price : 21.57 Bid-YTW : 7.22 % |

| CM.PR.Y | FixedReset Disc | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 21.85 Evaluated at bid price : 22.37 Bid-YTW : 7.79 % |

| TRP.PR.A | FixedReset Disc | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 12.70 Evaluated at bid price : 12.70 Bid-YTW : 10.23 % |

| BN.PR.B | Floater | 1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 11.14 Evaluated at bid price : 11.14 Bid-YTW : 10.84 % |

| BMO.PR.E | FixedReset Disc | 1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 20.30 Evaluated at bid price : 20.30 Bid-YTW : 7.59 % |

| FTS.PR.G | FixedReset Disc | 1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 16.90 Evaluated at bid price : 16.90 Bid-YTW : 8.32 % |

| RY.PR.Z | FixedReset Disc | 2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 16.48 Evaluated at bid price : 16.48 Bid-YTW : 8.48 % |

| CM.PR.T | FixedReset Disc | 2.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 21.61 Evaluated at bid price : 22.00 Bid-YTW : 7.64 % |

| RY.PR.N | Perpetual-Discount | 2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 21.18 Evaluated at bid price : 21.18 Bid-YTW : 5.83 % |

| BN.PF.I | FixedReset Disc | 2.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 8.84 % |

| MFC.PR.F | FixedReset Ins Non | 2.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 11.71 Evaluated at bid price : 11.71 Bid-YTW : 9.16 % |

| CU.PR.I | FixedReset Disc | 3.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 22.34 Evaluated at bid price : 22.75 Bid-YTW : 7.39 % |

| IFC.PR.F | Insurance Straight | 4.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 21.32 Evaluated at bid price : 21.32 Bid-YTW : 6.33 % |

| BMO.PR.Y | FixedReset Disc | 5.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 16.69 Evaluated at bid price : 16.69 Bid-YTW : 8.54 % |

| GWO.PR.P | Insurance Straight | 9.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 6.62 % |

| PWF.PR.F | Perpetual-Discount | 20.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 20.28 Evaluated at bid price : 20.28 Bid-YTW : 6.56 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| CU.PR.G | Perpetual-Discount | 170,910 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 18.35 Evaluated at bid price : 18.35 Bid-YTW : 6.17 % |

| BMO.PR.E | FixedReset Disc | 55,211 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 20.30 Evaluated at bid price : 20.30 Bid-YTW : 7.59 % |

| GWO.PR.H | Insurance Straight | 27,400 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 18.90 Evaluated at bid price : 18.90 Bid-YTW : 6.54 % |

| RY.PR.H | FixedReset Disc | 22,000 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 16.55 Evaluated at bid price : 16.55 Bid-YTW : 8.45 % |

| BN.PF.B | FixedReset Disc | 21,445 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 15.17 Evaluated at bid price : 15.17 Bid-YTW : 10.09 % |

| TRP.PR.A | FixedReset Disc | 20,690 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2053-05-26 Maturity Price : 12.70 Evaluated at bid price : 12.70 Bid-YTW : 10.23 % |

| There were 17 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| ELF.PR.F | Perpetual-Discount | Quote: 17.10 – 20.60 Spot Rate : 3.5000 Average : 1.9546 YTW SCENARIO |

| SLF.PR.E | Insurance Straight | Quote: 17.37 – 18.96 Spot Rate : 1.5900 Average : 0.9275 YTW SCENARIO |

| CU.PR.J | Perpetual-Discount | Quote: 18.63 – 22.00 Spot Rate : 3.3700 Average : 2.9208 YTW SCENARIO |

| MFC.PR.N | FixedReset Ins Non | Quote: 15.21 – 16.52 Spot Rate : 1.3100 Average : 0.9278 YTW SCENARIO |

| TD.PF.D | FixedReset Disc | Quote: 17.01 – 18.34 Spot Rate : 1.3300 Average : 0.9939 YTW SCENARIO |

| PWF.PR.Z | Perpetual-Discount | Quote: 19.87 – 20.99 Spot Rate : 1.1200 Average : 0.8058 YTW SCENARIO |