The Greek tragedy is approaching a climax:

The European Central Bank plans to hold an emergency session of its Governing Council on Friday to discuss the deteriorating liquidity situation of Greek banks, three people familiar with the matter said.

The call is scheduled for noon Frankfurt time on Friday, and the officials will consider a Bank of Greece request for an increase of more than 3 billion euros in Emergency Liquidity Assistance, one of the people said. All three asked not to be identified as the plans aren’t public. An ECB spokesman declined to comment.

The request comes just a day after Greece received an increase in its liquidity line of 1.1. billion euros ($1.25 billion), which raised the limit to 84.1 billion euros.

The short interval may be a signal that deposit flight is accelerating as the latest bailout talks ended without progress on Thursday.

Frankly, I’m surprised that there’s any money left in the Greek banking system to take flight.

And it looks like there’s a lot of internal politicking in Athens:

Prime Minister Alexis Tsipras’s government said there was an effort under way to spur capital flight, with Finance Minister Yanis Varoufakis later accusing the central bank of stoking fears.

The scaremongering seeks to undermine the financial system and strengthen the position of the country’s creditors, a Greek government official said in an e-mail to reporters.

“These tactics facilitate creditors who want to further blackmail the Greek government,” the official said in the statement. “Greece won’t be blackmailed.”

Further to the discussion of the OSC’s Brondesbury Report on June 16, today saw the publication of the Kenmar Commentary on CSA Fund Fee Report. This polemic does not address the question of new issue commissions, proxy solicitation fees, the willingness of small investors to pay advisors directly or the effects on capital markets of a change in fee schedules; changes are advocated as a method of smuggling in the concept of fiduciary duty.

On a related note, Michael P Regan of Bloomberg passes on a very bullish prediction on robo-advice:

Their popularity is going to explode even more, if new projections from consulting firm A.T. Kearney are in the right ballpark. Assets under management by robo advisers are estimated to increase 68 percent annually to about $2.2 trillion in five years, according to a forecast from the firm. About half of that is expected to come from money that’s already invested and the rest from non-invested assets.

As far as I can tell, Bloomberg just got a review copy of the paper; while the A.T. Kearney website features a front page link to the Bloomberg piece, the paper itself does not appear to be on the site.

I can’t resist passing on another shot at supply management:

Faced with a stagnant domestic market, Montreal-based Saputo Inc. and other major Canadian dairy producers have been investing heavily outside the country, where growth opportunities are better. This has exacerbated the skim milk surplus because dairies aren’t expanding their Canadian production of butter, cream or milk powder.

Martha Hall Findlay, a former Liberal MP and fellow at the University of Calgary School of Public Policy, said the real victims of the wastage are low-income Canadians, who aren’t getting the benefit of lower prices.

In a free market, surpluses would typically lead to lower consumer prices, but that isn’t the case in Canada because prices are fixed, she pointed out. “The system can’t accommodate fluctuations in demand,” said Ms. Findlay, who has written a series of reports advocating the dismantling of the supply management system.

It was another negative day for the Canadian preferred share market, with PerpetualDiscounts losing 59bp, FixedResets off 5bp and DeemedRetractibles down 14bp. PerpetualDiscounts are, predictably, overweighted in the bad part of the Performance Highlights table, while FixedResets are conspicuous on both sides. Volume was slightly above average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

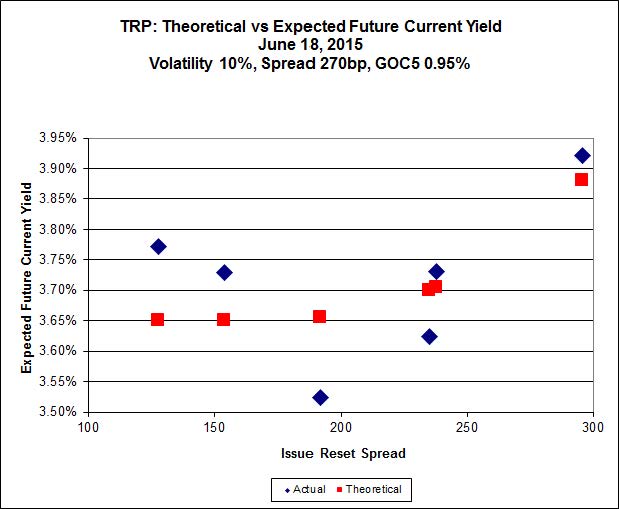

Here’s TRP:

Click for Big

TRP.PR.A, which resets 2019-12-31 at +192, is bid at 20.36 to be $0.73 rich, while TRP.PR.B, which will reset June 30 at 2.152% (+128), is $0.49 cheap at its bid price of 14.78

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule). Note that the lowest spread issue, MFC.PR.F, is again clearly off the line defined by the other issues.

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 22.70 to be $0.53 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 25.40 to be $0.44 cheap.

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 19.53 to be $0.94 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 24.50 and appears to be $0.65 rich.

Click for Big

FTS.PR.H, with a spread of +145bp, and bid at 16.60, looks $0.40 cheap and resets 2020-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 21.50 and is $0.25 rich.

Click for Big

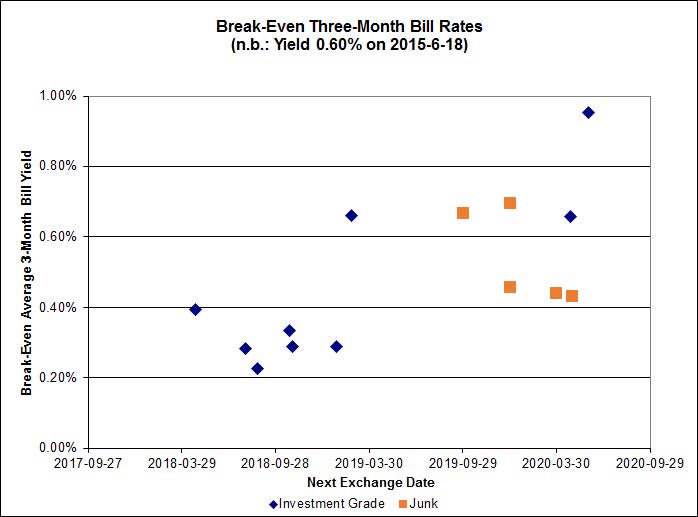

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of about 0.35%, including the outliers TRP.PR.A / TRP.PR.F at -0.54% and FTS.PR.H / FTS.PR.I at +0.95%. On the junk side there’s only one outlier: FFH.PR.E / FFH.PR.F at -0.93%.

Click for Big

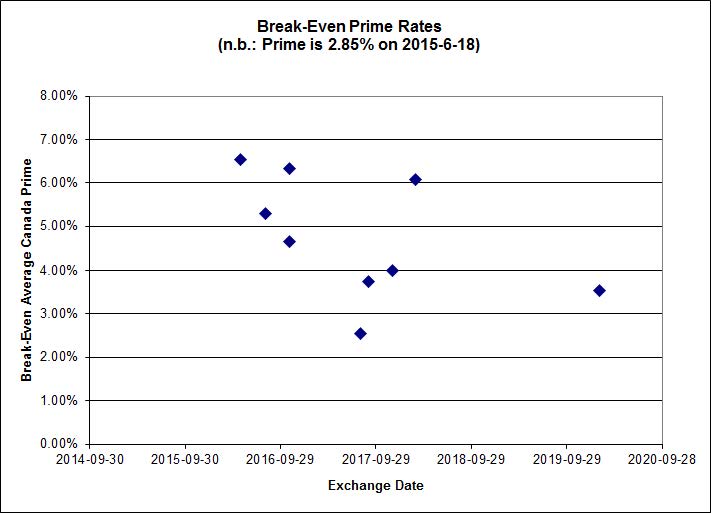

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.8845 % | 2,210.7 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.8845 % | 3,865.2 |

| Floater | 3.50 % | 3.52 % | 63,308 | 18.49 | 3 | 1.8845 % | 2,350.1 |

| OpRet | 4.45 % | -8.98 % | 24,337 | 0.08 | 2 | -0.0987 % | 2,780.2 |

| SplitShare | 4.59 % | 4.89 % | 71,608 | 3.28 | 3 | 0.2956 % | 3,249.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0987 % | 2,542.2 |

| Perpetual-Premium | 5.45 % | 4.77 % | 59,653 | 4.92 | 19 | 0.1160 % | 2,518.2 |

| Perpetual-Discount | 5.18 % | 5.12 % | 117,337 | 15.22 | 15 | -0.5936 % | 2,716.4 |

| FixedReset | 4.52 % | 3.88 % | 241,212 | 16.36 | 88 | -0.0527 % | 2,344.4 |

| Deemed-Retractible | 5.01 % | 3.40 % | 112,577 | 0.77 | 34 | -0.1441 % | 2,623.7 |

| FloatingReset | 2.52 % | 2.93 % | 58,555 | 6.11 | 9 | 0.0590 % | 2,337.5 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| HSE.PR.A | FixedReset | -1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 4.41 % |

| BAM.PF.C | Perpetual-Discount | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 21.44 Evaluated at bid price : 21.44 Bid-YTW : 5.68 % |

| CU.PR.G | Perpetual-Discount | -1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 21.82 Evaluated at bid price : 22.11 Bid-YTW : 5.12 % |

| SLF.PR.G | FixedReset | -1.72 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.03 Bid-YTW : 7.80 % |

| BAM.PF.D | Perpetual-Discount | -1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 21.62 Evaluated at bid price : 21.94 Bid-YTW : 5.59 % |

| GWO.PR.G | Deemed-Retractible | -1.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.21 Bid-YTW : 5.64 % |

| ENB.PR.F | FixedReset | -1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 5.03 % |

| RY.PR.H | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 22.36 Evaluated at bid price : 23.06 Bid-YTW : 3.65 % |

| BAM.PR.N | Perpetual-Discount | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 21.20 Evaluated at bid price : 21.20 Bid-YTW : 5.63 % |

| ENB.PR.H | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 17.05 Evaluated at bid price : 17.05 Bid-YTW : 4.84 % |

| PWF.PR.P | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 18.34 Evaluated at bid price : 18.34 Bid-YTW : 3.69 % |

| FTS.PR.J | Perpetual-Discount | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 23.28 Evaluated at bid price : 23.65 Bid-YTW : 5.04 % |

| IFC.PR.A | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.47 Bid-YTW : 6.32 % |

| IFC.PR.C | FixedReset | -1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.25 Bid-YTW : 4.65 % |

| ENB.PF.E | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 4.90 % |

| TRP.PR.E | FixedReset | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 22.18 Evaluated at bid price : 22.77 Bid-YTW : 3.90 % |

| BAM.PF.F | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 23.04 Evaluated at bid price : 24.50 Bid-YTW : 3.99 % |

| TRP.PR.G | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 23.11 Evaluated at bid price : 24.93 Bid-YTW : 3.83 % |

| BAM.PF.E | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 22.02 Evaluated at bid price : 22.55 Bid-YTW : 4.15 % |

| TRP.PR.D | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 21.91 Evaluated at bid price : 22.31 Bid-YTW : 3.94 % |

| TRP.PR.B | FixedReset | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 14.78 Evaluated at bid price : 14.78 Bid-YTW : 3.88 % |

| BAM.PR.K | Floater | 1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 14.10 Evaluated at bid price : 14.10 Bid-YTW : 3.53 % |

| FTS.PR.I | FloatingReset | 1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 3.14 % |

| BAM.PR.B | Floater | 1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 14.46 Evaluated at bid price : 14.46 Bid-YTW : 3.44 % |

| MFC.PR.L | FixedReset | 1.79 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.70 Bid-YTW : 4.71 % |

| BAM.PR.C | Floater | 2.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 14.15 Evaluated at bid price : 14.15 Bid-YTW : 3.52 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| HSE.PR.G | FixedReset | 250,190 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 23.01 Evaluated at bid price : 24.59 Bid-YTW : 4.54 % |

| TD.PF.E | FixedReset | 192,193 | TD crossed blocks of 100,000 and 75,000, both at 25.10. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 23.15 Evaluated at bid price : 25.04 Bid-YTW : 3.73 % |

| GWO.PR.F | Deemed-Retractible | 100,938 | Scotia crossed 100,000 at 25.42. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-07-18 Maturity Price : 25.00 Evaluated at bid price : 25.40 Bid-YTW : -15.19 % |

| BMO.PR.Y | FixedReset | 100,072 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-18 Maturity Price : 23.03 Evaluated at bid price : 24.66 Bid-YTW : 3.69 % |

| BMO.PR.L | Deemed-Retractible | 90,150 | Nesbitt crossed 84,100 at 25.71. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-07-18 Maturity Price : 25.50 Evaluated at bid price : 25.70 Bid-YTW : 0.68 % |

| BMO.PR.R | FloatingReset | 68,382 | TD crossed 65,000 at 24.15. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.11 Bid-YTW : 2.83 % |

| There were 38 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.N | FixedReset | Quote: 22.60 – 23.60 Spot Rate : 1.0000 Average : 0.6362 YTW SCENARIO |

| HSE.PR.A | FixedReset | Quote: 16.00 – 16.47 Spot Rate : 0.4700 Average : 0.3318 YTW SCENARIO |

| TD.PF.A | FixedReset | Quote: 23.38 – 23.78 Spot Rate : 0.4000 Average : 0.2729 YTW SCENARIO |

| MFC.PR.F | FixedReset | Quote: 17.39 – 17.83 Spot Rate : 0.4400 Average : 0.3207 YTW SCENARIO |

| BAM.PF.C | Perpetual-Discount | Quote: 21.44 – 21.76 Spot Rate : 0.3200 Average : 0.2027 YTW SCENARIO |

| IFC.PR.C | FixedReset | Quote: 23.25 – 23.75 Spot Rate : 0.5000 Average : 0.3856 YTW SCENARIO |

This Greek tragedy is like hoping your 35 year old son is going to eventually move out of the basement and get a job. You hope for the best but expect the worst. Sadly the lovely Greek people have not ,nor will they ever, accept that living off a single industry ( tourism) will never work and that the hate for paying tax , while noble, is not realistic while expecting health care, pensions, be fully funded. We were in Greece in 2011 and I had a chance to talk to a fellow who was really wound up by the government wanting to raise income tax from 8 to 12 % , little did he realize that would be a tax system that the rest of the world would kill for. Sadly my lovely Greek people have forgotten that when they went into the Eurozone asset prices such as houses and all property skyrocketed and the reverse will be true if they go back to the Drachma. Couple their expectactions of the nanny state supported by Germany and the Germans finally getting tired of supporting the Greeks it will end even more sadly than realizng your jobless son will never move out of the basement.

As far as I can tell, the big problem with Greece was that the inefficiency was so pervasive. Other countries – including Canada – have been able to make austerity work because it was targeted … I certainly can’t remember the austerity budgets of the 1990’s, either federally or provincially, having any direct effect on me whatsoever.

In Greece, though, it seems like every single citizen has been living somewhat above his means and has therefore come to believe that they deserve it (how many among us would be happy at being told we were to take a $10,000 p.a. pay-cut because we don’t deserve our current salary?).