On November 24 I mentioned the tender offer for a big chunk of Talisman’s debt securities. Today they announced the pricing:

Talisman Energy Inc. (the “Offeror”) announced today the pricing of its previously announced tender offer (the “Offer”) to purchase for cash up to $1,524,531,000 aggregate principal amount (the “Maximum Tender Amount”) of the 5.85% Senior Notes due 2037 (CUSIP No. 87425E AJ2), 5.50% Senior Notes due 2042 (CUSIP No. 87425E AN3), 6.25% Senior Notes due 2038 (CUSIP No. 87425E AK9), 7.25% Debentures due 2027 (CUSIP No. 87425E AE3) and 5.75% Senior Notes due 2035 (CUSIP No. 87425E AH6) issued by the Offeror (collectively, the “Securities”).

…

The Offeror has accepted for purchase on the Early Settlement Date Securities having an aggregate principal amount equal to the Maximum Tender Amount that were validly tendered and not validly withdrawn on or before the Early Tender Date (as defined below). Settlement for Securities validly tendered on or prior to the Early Tender Date and accepted for purchase pursuant to the Offer is expected to occur on December 11, 2015.The Offer is being made upon the terms and subject to the general conditions set forth in the Offer to Purchase, as amended by the Offeror’s press release dated December 9, 2015 announcing an increase in the Maximum Tender Amount to $1,524,531,000. The Offer will expire at 12:00 midnight, New York City time, on December 22, 2015 (one minute after 11:59 p.m., New York City time, on December 22, 2015), unless extended or earlier terminated by the Offeror (as it may be extended or earlier terminated, the “Expiration Date”). The deadline to validly withdraw tenders of Securities was 5:00 p.m., New York City time, on December 8, 2015; therefore, Securities that have been tendered and not validly withdrawn, and Securities tendered after that date, may not be withdrawn unless otherwise required by applicable law.

Seems to me they just about nailed the pricing of this, which was about 420bp over comparable Treasuries, give or take a few beeps dependent on the issue. They got all they wanted, with no more than 80% take-up for any of the five issues.

The bureaucrats will be happy today! The ‘guilty until proven innocent’ aspect of anti-corruption laws has permitted them to exercise a certain level of direction and control over SNC Lavalin:

The previous Conservative government softened its tough anti-corruption rules for companies doing business with Ottawa last July in the face of intense criticism from business groups. The most contentious part of the rules was an inflexible 10-year contracting ban on companies charged with a long list of offences anywhere in the world, which was softened to five years. Under the new rules, the government could also immediately suspend any company charged.

That last change was of particular concern to SNC, given that it was charged in February with fraud and corruption related to its business in Libya and does significant business with the federal government. The company wanted to be sure it wouldn’t be suspended so entered into talks on an administrative agreement, said SNC spokesman Louis-Antoine Paquin.

The SNC-Lavalin agreement is the first reached under the new regime, and allows the company to continue with existing contracts and any future work with the federal government. As part of the deal, it agreed to strict conditions and third-party oversight of its business practices. The specific terms are confidential, Mr. Paquin said.

And soon life may get even better for the central planners, when everybody’s a Secret Policeman:

A pledge of allegiance to the Islamic State (IS) – otherwise known as Daesh – that might have been posted to Facebook by suspected terrorist Tashfeen Malik has prompted US lawmakers to revive a bill that would require technology companies such as Facebook and Twitter to report suspected online terror activity.

Sen. Dianne Feinstein, a Democrat from California, is sponsoring the legislation along with Sen. Richard Burr, a Republican from North Carolina.

From her statement:

We’re in a new age where terrorist groups like [Islamic State of Iraq and the Levant, or ISIL] are using social media to reinvent how they recruit and plot attacks.

That information can be the key to identifying and stopping terrorist recruitment or a terrorist attack, but we need help from technology companies.

Feinstein said that under the legislation, companies wouldn’t have to go out of their way to uncover terrorist activity. But if they do happen upon it, they’d be required to report it to law enforcement.

Laurentian Bank, proud issuer of LB.PR.F and LB.PR.H, got a vote of confidence from DBRS:

DBRS Limited (DBRS) notes that yesterday Laurentian Bank of Canada (Laurentian or the Bank) (Deposits and Senior Debt, rated A (low)) launched a $65 million common share offering to strengthen its capital ratios after reporting a net loss for Q4 2015 of $18.7 million due to impairment and restructuring charges totalling $61.7 million after tax. Excluding these charges and other adjustments, Laurentian announced good core net earnings of $44.1 million for Q4 2015 and $172.2 million for the full year ended October 31, 2015. The Bank’s year-end CET1 capital ratio of 7.6% would instead be 8.0% pro forma the common share issue. With good underlying results and a net impact-to-capital ratio of only 7 basis points (bps) due to the charges, there is no impact to DBRS current ratings for Laurentian at this time.

…

DBRS does view positively Laurentian’s decision to issue common shares in order to improve the buffer it has relative to regulatory minimums. However, DBRS also reiterates its observation from its November 6, 2015, rating report that, even after the common share issuance, Laurentian’s capitalization levels are closer to regulatory minimums than its peers. Although the Bank has indicated it is raising the capital in order to strengthen its flexibility, including being able to proceed with opportunistic acquisitions consistent with its growth objectives, if they were to present themselves (there are none on the immediate horizon), DBRS believes the Bank will still have a limited buffer to withstand a major problem and continues to have limited financial flexibility.

It was – wait for it – a mixed day for the Canadian preferred share market, with PerpetualDiscounts down 27bp, FixedResets off 9bp and DeemedRetractibles gaining 22bp. The Performance Highlights table continues to reveal a lot of churn. Volume is still enormously high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

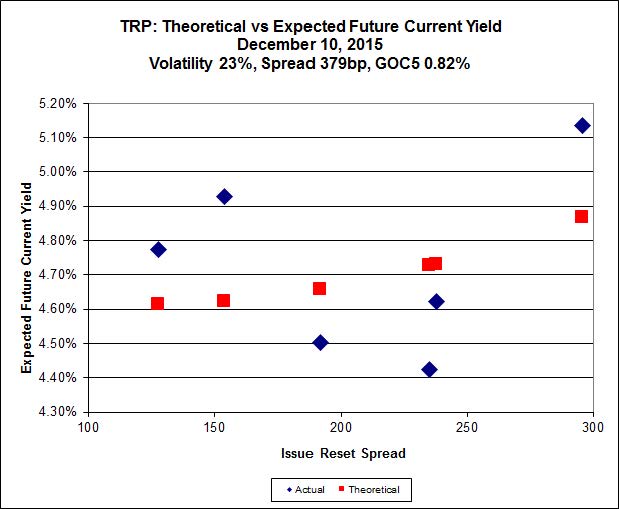

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.91 to be $1.15 rich, while TRP.PR.G, resetting 2020-11-30 at +154, is $1.02 cheap at its bid price of 18.40.

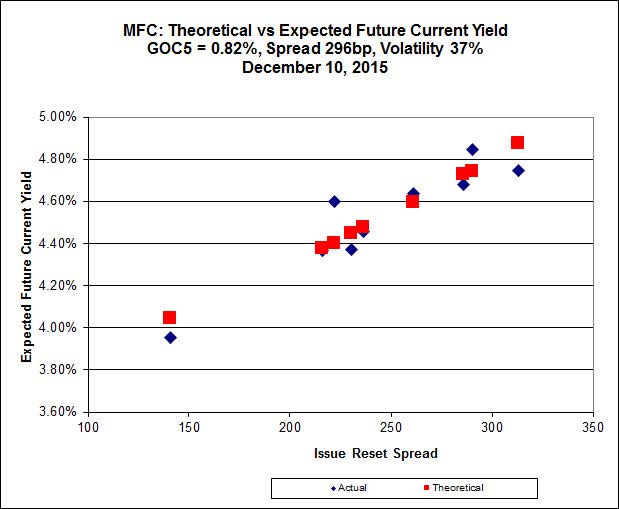

Click for Big

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 20.80 to be 0.54 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 16.53 to be 0.75 cheap.

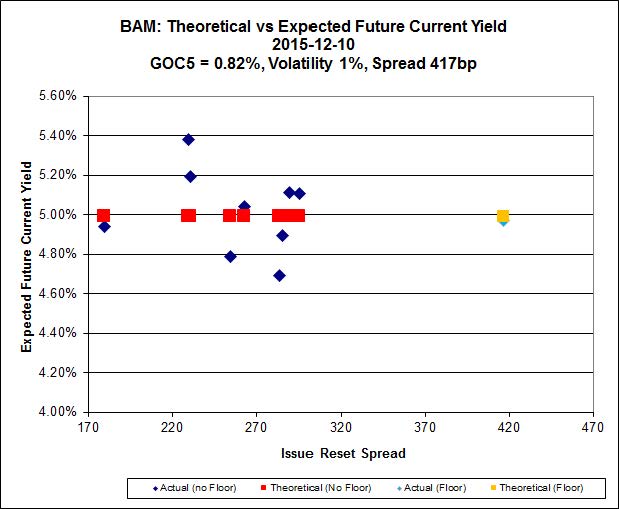

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 14.50 to be $1.13 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 19.50 and appears to be $1.16 rich.

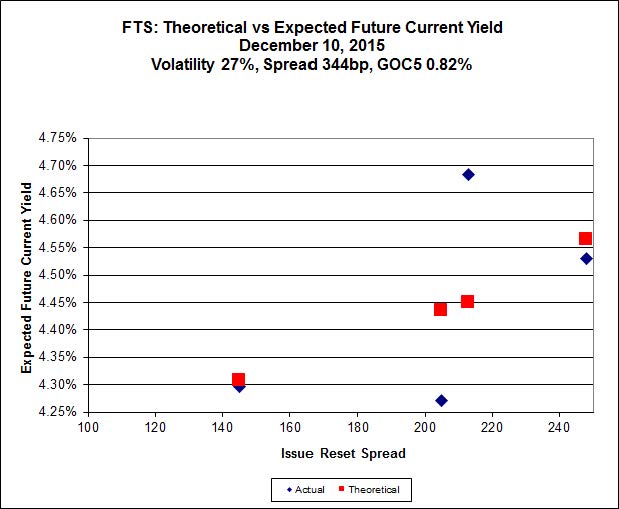

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 16.80, looks $0.62 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 15.75 and is $0.83 cheap.

Click for Big

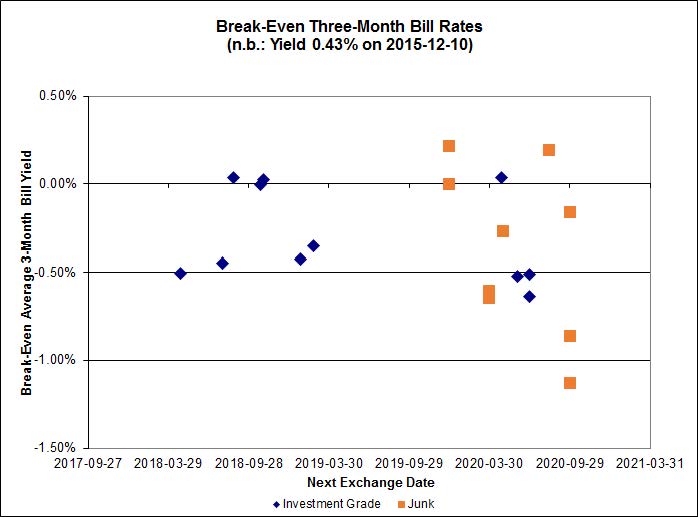

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.41%, with one outlier below -1.50%. There is one junk outlier below -1.50%.

Click for Big

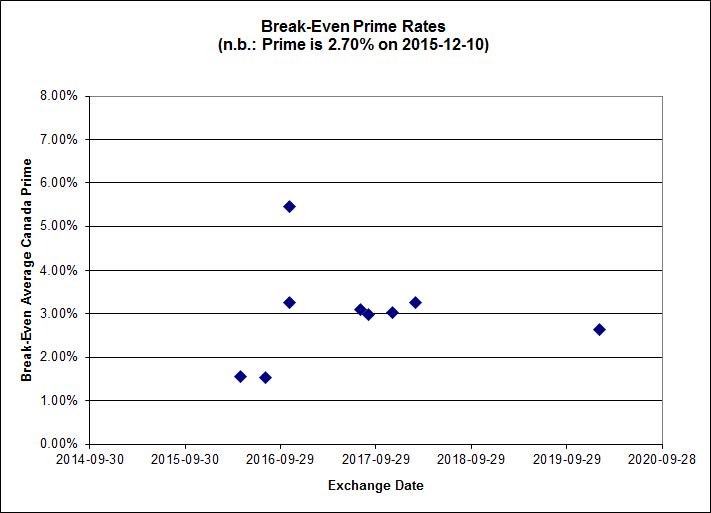

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.17 % | 6.28 % | 33,816 | 16.31 | 1 | -3.5897 % | 1,502.1 |

| FixedFloater | 7.21 % | 6.38 % | 33,212 | 15.78 | 1 | -0.9023 % | 2,707.5 |

| Floater | 4.34 % | 4.56 % | 80,043 | 16.21 | 4 | -3.2889 % | 1,743.5 |

| OpRet | 4.87 % | 4.18 % | 26,709 | 0.71 | 1 | 0.0000 % | 2,734.3 |

| SplitShare | 4.82 % | 5.46 % | 83,698 | 2.86 | 6 | 0.0342 % | 3,203.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0342 % | 2,499.3 |

| Perpetual-Premium | 5.89 % | 5.96 % | 95,099 | 13.84 | 7 | -0.1387 % | 2,458.5 |

| Perpetual-Discount | 5.84 % | 5.94 % | 100,369 | 13.95 | 33 | -0.2700 % | 2,448.2 |

| FixedReset | 5.50 % | 5.04 % | 259,405 | 14.40 | 78 | -0.0913 % | 1,873.0 |

| Deemed-Retractible | 5.31 % | 5.48 % | 137,966 | 5.32 | 33 | 0.2263 % | 2,521.5 |

| FloatingReset | 2.83 % | 4.33 % | 66,482 | 5.69 | 11 | -0.8330 % | 2,079.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| HSE.PR.A | FixedReset | -3.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 11.69 Evaluated at bid price : 11.69 Bid-YTW : 5.63 % |

| BAM.PR.E | Ratchet | -3.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 25.00 Evaluated at bid price : 13.16 Bid-YTW : 6.28 % |

| BAM.PR.K | Floater | -3.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 10.51 Evaluated at bid price : 10.51 Bid-YTW : 4.56 % |

| BAM.PR.B | Floater | -3.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 10.51 Evaluated at bid price : 10.51 Bid-YTW : 4.56 % |

| PWF.PR.A | Floater | -3.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 12.00 Evaluated at bid price : 12.00 Bid-YTW : 3.97 % |

| BNS.PR.D | FloatingReset | -2.96 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.35 Bid-YTW : 6.79 % |

| BAM.PR.C | Floater | -2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 10.50 Evaluated at bid price : 10.50 Bid-YTW : 4.56 % |

| HSE.PR.C | FixedReset | -2.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 17.20 Evaluated at bid price : 17.20 Bid-YTW : 6.03 % |

| BAM.PR.Z | FixedReset | -2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 5.48 % |

| BNS.PR.Y | FixedReset | -2.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.26 Bid-YTW : 6.48 % |

| BNS.PR.B | FloatingReset | -2.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.56 Bid-YTW : 4.72 % |

| BNS.PR.Z | FixedReset | -1.95 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.10 Bid-YTW : 7.25 % |

| SLF.PR.J | FloatingReset | -1.93 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.70 Bid-YTW : 10.25 % |

| CU.PR.F | Perpetual-Discount | -1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 5.91 % |

| ENB.PR.A | Perpetual-Discount | -1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 22.01 Evaluated at bid price : 22.25 Bid-YTW : 6.23 % |

| MFC.PR.K | FixedReset | -1.72 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.53 Bid-YTW : 8.87 % |

| BNS.PR.C | FloatingReset | -1.67 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.73 Bid-YTW : 4.77 % |

| IAG.PR.G | FixedReset | -1.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.43 Bid-YTW : 7.21 % |

| TD.PR.S | FixedReset | -1.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.15 Bid-YTW : 4.36 % |

| TRP.PR.C | FixedReset | -1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 11.97 Evaluated at bid price : 11.97 Bid-YTW : 5.15 % |

| BAM.PF.A | FixedReset | -1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 18.20 Evaluated at bid price : 18.20 Bid-YTW : 5.48 % |

| MFC.PR.F | FixedReset | -1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.10 Bid-YTW : 9.71 % |

| PWF.PR.R | Perpetual-Discount | -1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 22.93 Evaluated at bid price : 23.32 Bid-YTW : 5.96 % |

| TD.PF.E | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 19.30 Evaluated at bid price : 19.30 Bid-YTW : 4.91 % |

| CU.PR.E | Perpetual-Discount | -1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 20.73 Evaluated at bid price : 20.73 Bid-YTW : 5.96 % |

| CU.PR.D | Perpetual-Discount | -1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 20.86 Evaluated at bid price : 20.86 Bid-YTW : 5.93 % |

| TD.PF.F | Perpetual-Discount | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 21.86 Evaluated at bid price : 22.20 Bid-YTW : 5.58 % |

| ELF.PR.G | Perpetual-Discount | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 19.95 Evaluated at bid price : 19.95 Bid-YTW : 6.06 % |

| TRP.PR.A | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 15.21 Evaluated at bid price : 15.21 Bid-YTW : 4.79 % |

| BAM.PR.R | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 14.50 Evaluated at bid price : 14.50 Bid-YTW : 5.76 % |

| CIU.PR.A | Perpetual-Discount | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 5.66 % |

| BMO.PR.Z | Perpetual-Discount | -1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 22.30 Evaluated at bid price : 22.59 Bid-YTW : 5.57 % |

| TRP.PR.B | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 11.00 Evaluated at bid price : 11.00 Bid-YTW : 4.93 % |

| PWF.PR.O | Perpetual-Premium | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 23.99 Evaluated at bid price : 24.46 Bid-YTW : 5.99 % |

| BMO.PR.W | FixedReset | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 16.88 Evaluated at bid price : 16.88 Bid-YTW : 4.87 % |

| RY.PR.B | Deemed-Retractible | 1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.81 Bid-YTW : 4.91 % |

| TD.PF.C | FixedReset | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 17.03 Evaluated at bid price : 17.03 Bid-YTW : 4.88 % |

| GWO.PR.H | Deemed-Retractible | 1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.05 Bid-YTW : 7.24 % |

| FTS.PR.J | Perpetual-Discount | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 21.03 Evaluated at bid price : 21.03 Bid-YTW : 5.70 % |

| RY.PR.H | FixedReset | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 17.29 Evaluated at bid price : 17.29 Bid-YTW : 4.82 % |

| RY.PR.W | Perpetual-Discount | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 21.50 Evaluated at bid price : 21.76 Bid-YTW : 5.67 % |

| NA.PR.W | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 16.54 Evaluated at bid price : 16.54 Bid-YTW : 5.07 % |

| RY.PR.J | FixedReset | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 18.28 Evaluated at bid price : 18.28 Bid-YTW : 5.00 % |

| BAM.PR.N | Perpetual-Discount | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 19.16 Evaluated at bid price : 19.16 Bid-YTW : 6.34 % |

| FTS.PR.F | Perpetual-Discount | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 21.59 Evaluated at bid price : 21.85 Bid-YTW : 5.64 % |

| RY.PR.Z | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 17.28 Evaluated at bid price : 17.28 Bid-YTW : 4.77 % |

| IAG.PR.A | Deemed-Retractible | 1.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.50 Bid-YTW : 7.34 % |

| BMO.PR.S | FixedReset | 1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 17.71 Evaluated at bid price : 17.71 Bid-YTW : 4.79 % |

| BAM.PR.T | FixedReset | 2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 15.07 Evaluated at bid price : 15.07 Bid-YTW : 5.60 % |

| BIP.PR.A | FixedReset | 4.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 19.01 Evaluated at bid price : 19.01 Bid-YTW : 5.89 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.C | FloatingReset | 184,623 | TD crossed 182,600 shares at 21.80. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.73 Bid-YTW : 4.77 % |

| PWF.PR.H | Perpetual-Premium | 106,684 | RBC crossed 97,900 at 24.46. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 24.02 Evaluated at bid price : 24.27 Bid-YTW : 6.00 % |

| TD.PR.T | FloatingReset | 105,364 | TD crossed 100,000 at 22.15. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.15 Bid-YTW : 4.13 % |

| RY.PR.Z | FixedReset | 90,536 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 17.28 Evaluated at bid price : 17.28 Bid-YTW : 4.77 % |

| FTS.PR.M | FixedReset | 76,669 | Nesbitt crossed 50,000 at 18.10. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 18.21 Evaluated at bid price : 18.21 Bid-YTW : 4.88 % |

| RY.PR.J | FixedReset | 70,415 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-10 Maturity Price : 18.28 Evaluated at bid price : 18.28 Bid-YTW : 5.00 % |

| There were 86 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PR.K | Floater | Quote: 10.51 – 11.30 Spot Rate : 0.7900 Average : 0.5157 YTW SCENARIO |

| BAM.PR.E | Ratchet | Quote: 13.16 – 14.00 Spot Rate : 0.8400 Average : 0.6874 YTW SCENARIO |

| MFC.PR.N | FixedReset | Quote: 17.85 – 18.40 Spot Rate : 0.5500 Average : 0.4130 YTW SCENARIO |

| PWF.PR.A | Floater | Quote: 12.00 – 12.74 Spot Rate : 0.7400 Average : 0.6068 YTW SCENARIO |

| PWF.PR.R | Perpetual-Discount | Quote: 23.32 – 23.81 Spot Rate : 0.4900 Average : 0.3569 YTW SCENARIO |

| TRP.PR.H | FloatingReset | Quote: 9.71 – 10.17 Spot Rate : 0.4600 Average : 0.3278 YTW SCENARIO |