Assiduous Reader prefobsessed sent me a link to a Barry Critchley piece titled Behind RioCan’s decision to redeem its first-of-its-kind rate reset preferreds. I have updated the post that reported REI.PR.A to be Redeemed.

Meanwhile, Sweden’s gone more deeply negative:

Sweden’s central bank lowered its key interest rate even further below zero and said it’s prepared to use its full toolbox of measures as it battles to revive inflation and keep the krona from appreciating.

The repo rate was reduced to minus 0.50 percent from minus 0.35 percent, the Stockholm-based bank said. A cut was predicted by 10 of the 18 analysts surveyed by Bloomberg, though only three had anticipated this magnitude. The bank said government bond purchases will continue as planned for the first six months of 2016 and that it “will reinvest maturities and coupons from the government bond portfolio until further notice.”

“Uncertainty regarding global developments is still high, with low inflation and several central banks pursuing more expansionary monetary policy,” the Riksbank said. “Swedish monetary policy must relate to this. Otherwise the krona exchange rate is at risk of strengthening at a faster rate than in the forecast, which would make it harder to push up inflation and stabilize it around 2 percent.”

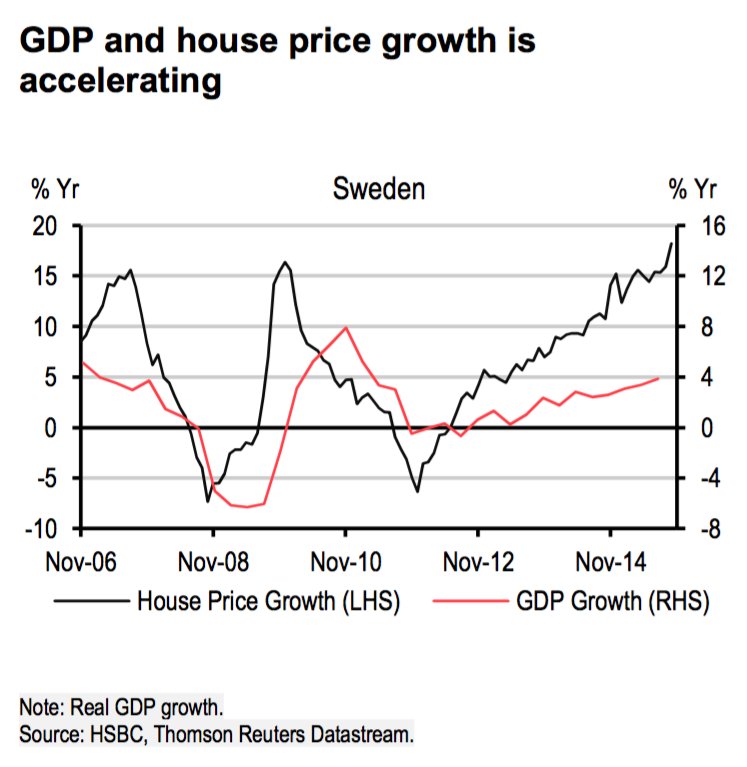

There are fears that this policy will inflate a housing bubble:

HSBC economist James Pomeroy wrote in a recent note:

We’ve long argued that the Swedish economy does not warrant further stimulus, but that the Riksbank would continue to ease given the low inflation rate. The economy is the fastest growing in the developed world (3.9% y-o-y in Q3) and house prices continue to accelerate and are now up 18% y-o-y across the country. Under normal circumstances, one might expect the Riksbank to be hiking rates but – given ultra-loose ECB policy – rates are being kept much lower.

As positive as the story appears for early 2016, there are plenty of reasons to be concerned about the medium term. The pace of acceleration in the housing market points to a bubble.

…

… The housing market continues to pose significant risks for the Swedish economy. With prices now up 18% on the year and no sign of macroprudential measures coming into force, we worry that this is not sustainable. Should the housing market roll over at any point in 2016 (or 2017) the impact on the economy would be severe. Estimates from the National Institute of Economic Research suggest that a 20% fall in house prices would lead to a recession-like impact on consumption and unemployment, with a smaller fall still having severe economic consequences.

Click for Big

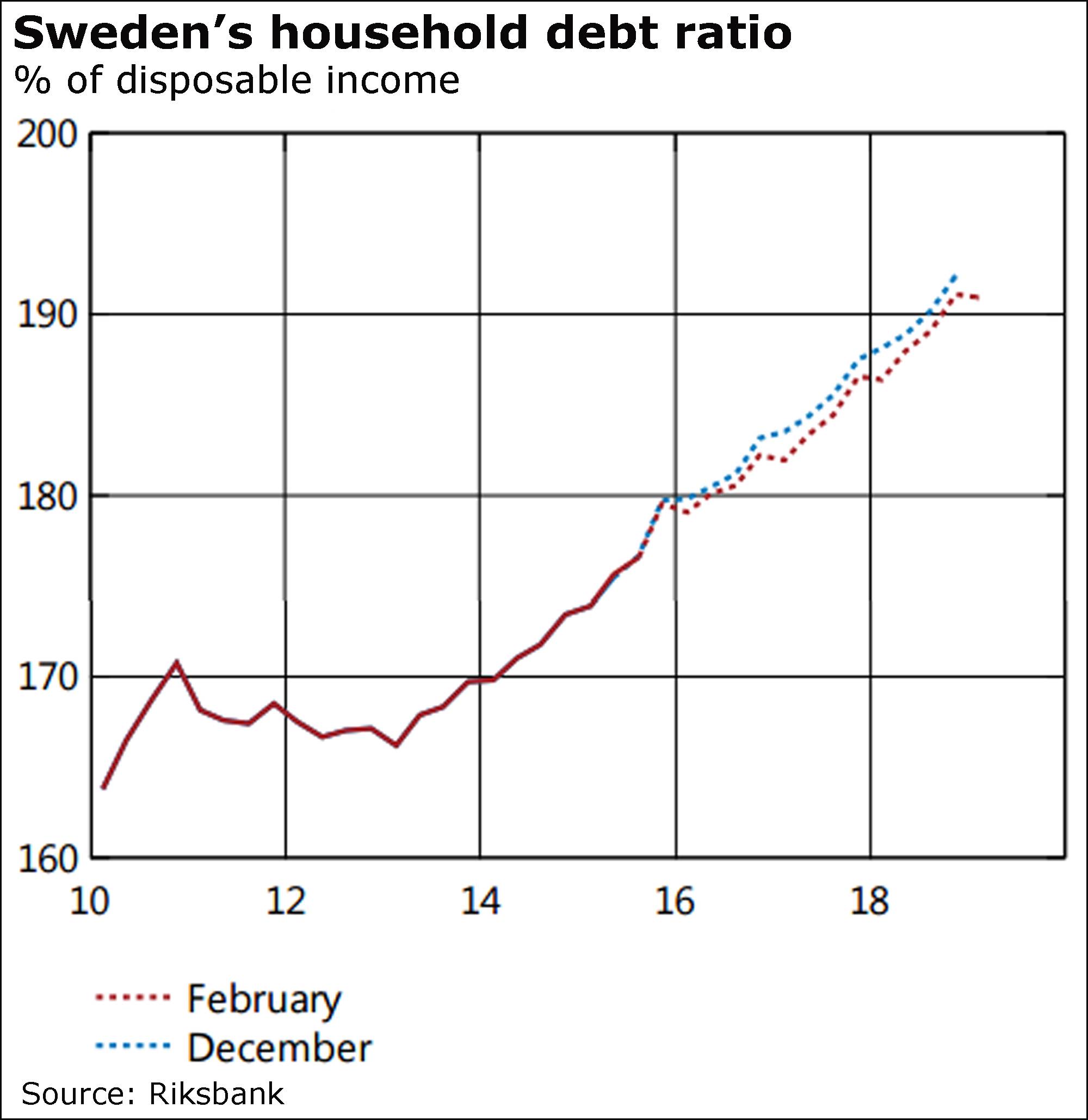

And Michael Babad of the Globe supplies another chart:

Click for Big

The Swedish action has been fingered as one of the triggers for today’s debacle:

The latest culprits picked out of the police lineup: The Swedish central bank’s bigger bet on negative interest rates; Fed chief Janet Yellen’s testimony before largely clueless U.S. legislators; and bearish hedge-fund manager Kyle Bass’s assertion that Chinese banks are facing huge losses that dwarf those of the U.S. financial system in the 2008 crash.

All are fanning fears that another U.S. and global recession looms, that central banks have run out of ammunition to fight it the way they did during the previous financial crisis and that more than a few of the world’s major banks aren’t in good enough shape to withstand the ensuing fallout.

Fearful investors have turned to the health of the global banking system as the latest fixation in a market frenzy that continues to escalate.

Bank equities were trounced worldwide on Thursday, leading the way for an all-consuming stock market selloff that spared no major benchmark.

An overwhelming demand for safety dominated investor attitudes, as the ability of central banks to fend off economic threats seems increasingly doubtful.

While crude oil has been at the crux of the recent outburst of market volatility, bank valuations have now begun to reflect a grim assessment of the global economy.

…

Withering risk appetite gripped equities on Thursday, as major Asian and European indexes fell by between 2 per cent and 6 per cent, adding to global equity losses in excess of $15-trillion (U.S.) this year.In North America, the S&P 500 index dipped to a new two-year low before a late afternoon rally pared back the losses to end the day down by 1.2 per cent. The Nasdaq composite index meanwhile flirted with a 20-per-cent decline conventionally signifying bear market territory. That’s where the S&P/TSX composite index already resides, with Thursday’s 100-point drop adding to a total decline of 23 per cent since September, 2014.

Overnight markets, at time of writing, seem to be getting worse:

The global equity bear market deepened in Asian trading, with Japanese stocks headed for their worst week since 2008 amid anxiety over central banks’ ability to revive the world economy. U.S. crude rose from a 12-year low.

The Topix index slumped 4.1 percent in Tokyo as traders returned from holiday, pushing the regional Asian benchmark toward its steepest weekly drop since gyrations in Chinese assets at the start of the year. The index pared some of its losses as the yen weakened for the first time this week. U.S. index futures indicated gains after losses there helped the MSCI All-Country Index cap a 20 percent slide from its May record.

Trading in South Korea’s Kosdaq exchange for smaller stocks was temporarily halted after the benchmark gauge plunged more than 8 percent on concern valuations were excessive relative to earnings prospects.

Trading was suspended for 20 minutes at 11:55 a.m. in Seoul after the measure dropped 8.2 percent. The index pared declines to 6.1 percent at the close. Celltrion Inc. was the biggest drag on the small-cap measure after the stock almost tripled in the past 12 months. The Kospi gauge of larger companies closed at its lowest level since August.

The Kosdaq index of more than 1,100 companies jumped 26 percent to outperform the large-cap gauge last year as investors piled into biotech shares and other smaller companies in search of earnings growth as smokestack industries stagnated. Celltrion, which developed an arthritis medicine, trades at 42 times projected 12 month profits, four times the Kospi’s 10.5 times.

And there are, as I always like to point out … unintended consequences:

It seemed like a good idea at the time: Cut interest rates below zero to revive growth.

But as policy makers from Tokyo to Stockholm embrace the notion, investors are close to panic mode. Far from buoying financial markets this year, negative rates have helped to put global stocks on the brink of a bear market, sent the cost of protection against corporate defaults soaring and driven investors to havens such as U.S. Treasury bonds and gold.

Fueling the turmoil is fear that negative rates will slam the world’s banks. In theory, negative rates could be the panacea to cure sluggish global growth: by charging lenders fees for parking money at central banks, policy makers hope banks will use that cash to make loans, jump-starting their economies. In practice, investors worry it may squeeze bank profits and rattle money markets.

“We’re here in an environment where central banks have to learn one message, and that is that negative interest rates are not desirable and they are not workable,” Hans Redeker, head of global foreign-exchange strategy at Morgan Stanley in London, said in a Bloomberg Television interview. “When you cut into negative interest rates you have to think about the profitability of the banking sector.”

About a quarter of the world economy is now in negative-rate territory with more than $7 trillion of government debt offering yields less than zero.

Last October, BIS published a working paper by Claudio Borio, Leonardo Gambacorta and Boris Hofmann titled The influence of monetary policy on bank profitability:

This paper investigates how monetary policy affects bank profitability. We use data for 109 large international banks headquartered in 14 major advanced economies for the period 1995–2012. Overall, we find a positive relationship between the level of short-term rates and the slope of the yield curve (the “interest rate structure”, for short), on the one hand, and bank profitability – return on assets – on the other. This suggests that the positive impact of the interest rate structure on net interest income dominates the negative one on loan loss provisions and on non-interest income. We also find that the effect is stronger when the interest rate level is lower and the slope less steep, ie that non-linearities are present. All this suggests that, over time, unusually low interest rates and an unusually flat term structure erode bank profitability.

…

Abstracting from macroeconomic effects, our findings help shed light on the impact of monetary policy on bank profitability after the crisis. Taking our results at face value, we find that the impact, on balance, was positive in the first two years post-crisis (2009–10) but turned negative in the following four years (2011–14). In the first two years, ROA was boosted by an estimated cumulative 0.3 percentage points: the negative effect on bank profitability linked to the decrease in the short-term rate was more than compensated for by the positive one deriving from the increase in the yield curve slope. In contrast, in the following four years, the further decrease in short-term rates and flattening of the yield curve cut ROA by an estimated cumulative 0.6 percentage points. With an average annual ROA of 0.64 over the sample period (1995-2012, Table 1), this means that over 2011–14, the average bank in the sample lost one year of profits as a consequence of low interest rates and compressed yield spreads.

Anybody who finds all this depressing should relax; read a nice book instead:

Click for Big

It was a horrible day for the Canadian preferred share market, horribler for some sectors than for others, with PerpetualDiscounts off 25bp, FixedResets losing 234bp and DeemedRetractibles down 65bp. Floaters got destroyed. Volume was high.

For those keeping track of Floaters, the all-time low closing bid for BAM.PR.B was 5.90 on 2008-12-19; for BAM.PR.C it was 6.06 on 2008-12-22; and for BAM.PR.K, 6.40 ON 2018-12-18. So we’re still a way off from my positive comments during the Credit Crunch. But some people, I’m sure, are just discovering the answer to the question: Are Floating Prefs Money Market Vehicles?.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

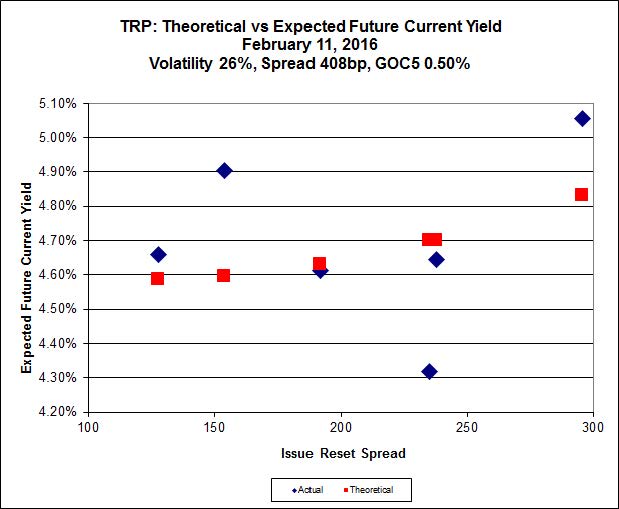

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 16.50 to be $1.34 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $0.80 cheap at its bid price of 17.11.

Click for Big

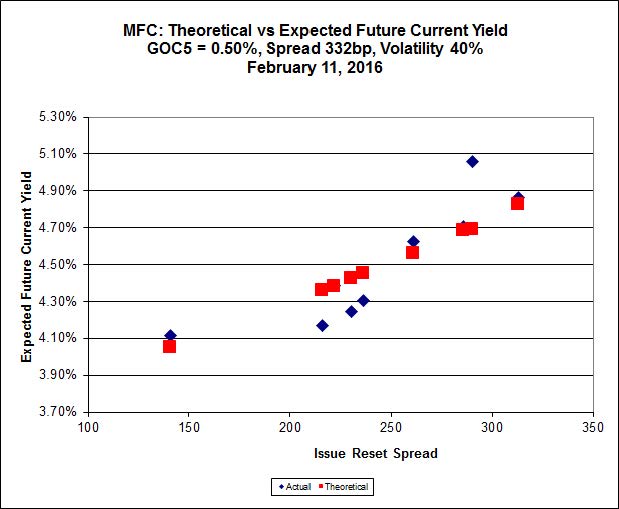

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 15.95 to be 0.70 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 16.80 to be 1.33 cheap.

Click for Big

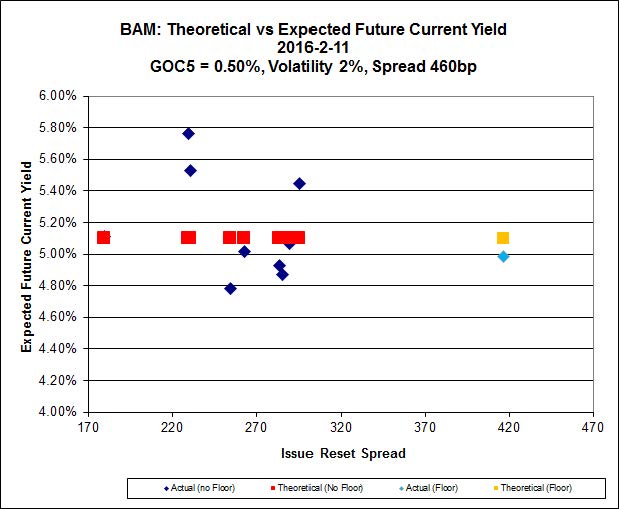

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 12.15 to be $1.58 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 15.95 and appears to be $1.00 rich.

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 14.80, looks $0.49 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 14.25 and is $0.43 cheap.

Click for Big

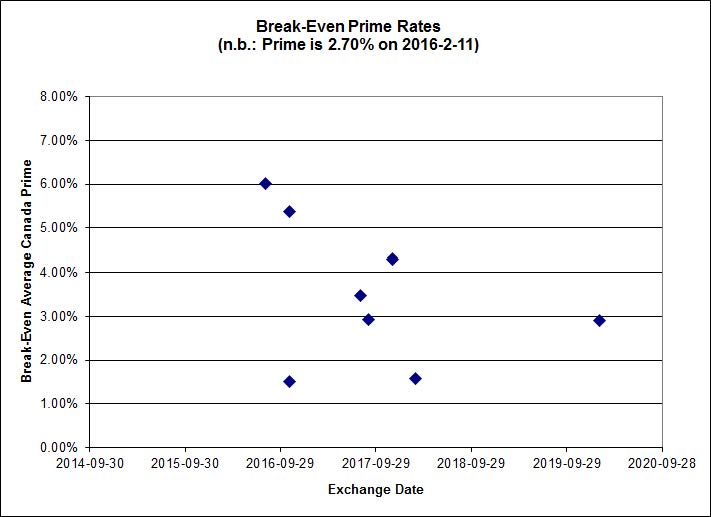

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.56%, with two outliers above 0.00%. There are four junk outliers above 0.00% and one below -2.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.83 % | 7.07 % | 17,116 | 15.38 | 1 | -9.2969 % | 1,337.6 |

| FixedFloater | 7.92 % | 6.91 % | 24,790 | 15.28 | 1 | -2.8340 % | 2,511.3 |

| Floater | 5.33 % | 5.46 % | 72,273 | 14.68 | 4 | -11.9821 % | 1,439.4 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0484 % | 2,715.6 |

| SplitShare | 4.86 % | 6.13 % | 74,068 | 2.68 | 6 | 0.0484 % | 3,177.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0484 % | 2,479.5 |

| Perpetual-Premium | 5.87 % | 5.85 % | 85,307 | 13.97 | 6 | 0.3488 % | 2,513.2 |

| Perpetual-Discount | 5.82 % | 5.86 % | 100,435 | 14.08 | 33 | -0.2549 % | 2,483.5 |

| FixedReset | 5.77 % | 5.07 % | 214,342 | 14.37 | 83 | -2.3397 % | 1,758.2 |

| Deemed-Retractible | 5.36 % | 5.89 % | 125,449 | 5.19 | 34 | -0.6488 % | 2,517.8 |

| FloatingReset | 3.08 % | 4.83 % | 50,523 | 5.53 | 16 | 0.3917 % | 1,974.5 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.K | Floater | -18.37 % | Only half real, but many will consider half to be rather more than enough! The issue traded 9,000 shares in a range of 8.99-85 before closing at 8.00-9.01, 5×1. The day’s low had been 9.58 until five trades totalling 600 shares took the price down to the day’s low in the last ten minutes of the day. It’s a good thing there was a market maker on duty to maintain an orderly market, eh? I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers.

YTW SCENARIO |

| BAM.PR.B | Floater | -11.52 % | Entirely real. The issue traded 10,420 shares in a range of 9.00-73 before closing at 8.76-00, 1×252. Not a typo! There were 25,200 shares being offered at 9.00 at the close!

YTW SCENARIO |

| BAM.PR.C | Floater | -10.66 % | Totally real. The issue traded 8,990 shares in a range of 8.85-9.65 before closing at 8.72-85, 2×504. Yup … 504. There were 50,400 shares offered at 8.85 at the close.

YTW SCENARIO |

| BAM.PR.E | Ratchet | -9.30 % | Not really all that real, since the issue traded 1,675 shares in a range of 12.40-80 before closing at 11.61-12.86 (!) 12×3. However, the bid probably dropped in sympathy with BAM’s floaters, above.

YTW SCENARIO |

| PWF.PR.A | Floater | -7.83 % | Not real, since the issue traded 1,966 shares in a range of 10.19-86 before closing at 10.00-45, 1×1. As above, however, it’s reasonable to assume that bidders backed off when they saw what was happening to BAM’s floaters. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 10.00 Evaluated at bid price : 10.00 Bid-YTW : 4.73 % |

| BAM.PR.Z | FixedReset | -7.62 % | Not real. The issue traded 7,410 shares in a range of 16.45-34 before closing at 15.89-16.90 (!) 8×5. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers.

YTW SCENARIO |

| SLF.PR.H | FixedReset | -6.73 % | Not real. The issue traded 11,590 shares in a range of 13.75-10 before closing at 13.30-92, 5×6. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers.

YTW SCENARIO |

| FTS.PR.M | FixedReset | -6.16 % | Real enough, as the issue traded 13,016 shares in a range of 15.80-05 before closing at 15.85-25, 2×10. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 15.85 Evaluated at bid price : 15.85 Bid-YTW : 5.21 % |

| SLF.PR.I | FixedReset | -5.37 % | Real enough, since the issue traded 3,392 shares in a range of 15.76-58 before closing at 15.85-29, 5×4. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.85 Bid-YTW : 9.66 % |

| BAM.PF.F | FixedReset | -4.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 17.25 Evaluated at bid price : 17.25 Bid-YTW : 5.31 % |

| MFC.PR.I | FixedReset | -4.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.85 Bid-YTW : 8.31 % |

| BAM.PF.A | FixedReset | -4.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 16.78 Evaluated at bid price : 16.78 Bid-YTW : 5.41 % |

| MFC.PR.J | FixedReset | -4.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.82 Bid-YTW : 8.87 % |

| IFC.PR.C | FixedReset | -4.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.30 Bid-YTW : 10.02 % |

| MFC.PR.G | FixedReset | -4.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.80 Bid-YTW : 9.08 % |

| MFC.PR.H | FixedReset | -4.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.65 Bid-YTW : 7.92 % |

| TRP.PR.A | FixedReset | -3.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 13.12 Evaluated at bid price : 13.12 Bid-YTW : 5.05 % |

| IFC.PR.A | FixedReset | -3.88 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.36 Bid-YTW : 11.26 % |

| TRP.PR.D | FixedReset | -3.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 15.50 Evaluated at bid price : 15.50 Bid-YTW : 5.02 % |

| TD.PF.D | FixedReset | -3.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 4.72 % |

| BAM.PF.G | FixedReset | -3.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 16.95 Evaluated at bid price : 16.95 Bid-YTW : 5.45 % |

| MFC.PR.L | FixedReset | -3.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.95 Bid-YTW : 9.43 % |

| TRP.PR.B | FixedReset | -3.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 9.55 Evaluated at bid price : 9.55 Bid-YTW : 4.99 % |

| HSE.PR.A | FixedReset | -3.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 8.01 Evaluated at bid price : 8.01 Bid-YTW : 7.13 % |

| IAG.PR.G | FixedReset | -3.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.15 Bid-YTW : 8.77 % |

| NA.PR.Q | FixedReset | -3.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.32 Bid-YTW : 5.34 % |

| MFC.PR.M | FixedReset | -3.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.61 Bid-YTW : 9.07 % |

| BAM.PF.B | FixedReset | -3.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 15.60 Evaluated at bid price : 15.60 Bid-YTW : 5.43 % |

| TD.PF.E | FixedReset | -3.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.59 % |

| BAM.PR.T | FixedReset | -3.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 12.70 Evaluated at bid price : 12.70 Bid-YTW : 5.87 % |

| HSE.PR.G | FixedReset | -3.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 15.06 Evaluated at bid price : 15.06 Bid-YTW : 7.09 % |

| NA.PR.S | FixedReset | -3.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 16.75 Evaluated at bid price : 16.75 Bid-YTW : 4.68 % |

| RY.PR.M | FixedReset | -2.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 17.45 Evaluated at bid price : 17.45 Bid-YTW : 4.67 % |

| MFC.PR.N | FixedReset | -2.94 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.50 Bid-YTW : 9.10 % |

| BNS.PR.Y | FixedReset | -2.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.75 Bid-YTW : 6.95 % |

| SLF.PR.G | FixedReset | -2.88 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.48 Bid-YTW : 11.19 % |

| NA.PR.W | FixedReset | -2.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 15.55 Evaluated at bid price : 15.55 Bid-YTW : 4.87 % |

| BAM.PR.G | FixedFloater | -2.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 25.00 Evaluated at bid price : 12.00 Bid-YTW : 6.91 % |

| FTS.PR.G | FixedReset | -2.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 14.25 Evaluated at bid price : 14.25 Bid-YTW : 5.06 % |

| MFC.PR.K | FixedReset | -2.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.50 Bid-YTW : 9.68 % |

| BNS.PR.Z | FixedReset | -2.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.40 Bid-YTW : 7.66 % |

| HSE.PR.E | FixedReset | -2.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 14.80 Evaluated at bid price : 14.80 Bid-YTW : 7.22 % |

| FTS.PR.K | FixedReset | -2.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 14.80 Evaluated at bid price : 14.80 Bid-YTW : 4.85 % |

| BMO.PR.T | FixedReset | -2.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 16.51 Evaluated at bid price : 16.51 Bid-YTW : 4.50 % |

| CU.PR.C | FixedReset | -2.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 15.30 Evaluated at bid price : 15.30 Bid-YTW : 4.88 % |

| FTS.PR.H | FixedReset | -2.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 11.70 Evaluated at bid price : 11.70 Bid-YTW : 4.54 % |

| TRP.PR.C | FixedReset | -2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 10.40 Evaluated at bid price : 10.40 Bid-YTW : 5.11 % |

| PWF.PR.T | FixedReset | -2.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 19.45 Evaluated at bid price : 19.45 Bid-YTW : 3.98 % |

| HSE.PR.C | FixedReset | -2.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 13.55 Evaluated at bid price : 13.55 Bid-YTW : 7.27 % |

| TRP.PR.E | FixedReset | -2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 4.80 % |

| BNS.PR.D | FloatingReset | -2.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.42 Bid-YTW : 7.87 % |

| TD.PF.A | FixedReset | -2.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 16.70 Evaluated at bid price : 16.70 Bid-YTW : 4.49 % |

| CM.PR.Q | FixedReset | -2.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 18.13 Evaluated at bid price : 18.13 Bid-YTW : 4.69 % |

| SLF.PR.J | FloatingReset | -2.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 11.25 Bid-YTW : 12.12 % |

| TRP.PR.G | FixedReset | -2.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 17.11 Evaluated at bid price : 17.11 Bid-YTW : 5.31 % |

| BAM.PR.X | FixedReset | -2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 11.25 Evaluated at bid price : 11.25 Bid-YTW : 5.64 % |

| BIP.PR.A | FixedReset | -2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 17.27 Evaluated at bid price : 17.27 Bid-YTW : 6.16 % |

| BMO.PR.W | FixedReset | -2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 16.41 Evaluated at bid price : 16.41 Bid-YTW : 4.50 % |

| RY.PR.I | FixedReset | -2.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.30 Bid-YTW : 4.30 % |

| GWO.PR.H | Deemed-Retractible | -2.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.15 Bid-YTW : 7.35 % |

| TD.PF.B | FixedReset | -2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 16.61 Evaluated at bid price : 16.61 Bid-YTW : 4.50 % |

| CM.PR.O | FixedReset | -2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 16.80 Evaluated at bid price : 16.80 Bid-YTW : 4.56 % |

| BMO.PR.Q | FixedReset | -1.92 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.85 Bid-YTW : 7.94 % |

| BNS.PR.Q | FixedReset | -1.88 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.02 Bid-YTW : 4.45 % |

| BNS.PR.P | FixedReset | -1.88 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.55 Bid-YTW : 4.01 % |

| BMO.PR.R | FloatingReset | -1.83 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.40 Bid-YTW : 4.83 % |

| FTS.PR.I | FloatingReset | -1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 9.55 Evaluated at bid price : 9.55 Bid-YTW : 5.00 % |

| RY.PR.H | FixedReset | -1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 16.90 Evaluated at bid price : 16.90 Bid-YTW : 4.42 % |

| RY.PR.J | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 17.85 Evaluated at bid price : 17.85 Bid-YTW : 4.68 % |

| CM.PR.P | FixedReset | -1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 16.20 Evaluated at bid price : 16.20 Bid-YTW : 4.63 % |

| GWO.PR.Q | Deemed-Retractible | -1.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.31 Bid-YTW : 6.91 % |

| RY.PR.Z | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 16.92 Evaluated at bid price : 16.92 Bid-YTW : 4.36 % |

| PWF.PR.P | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 11.51 Evaluated at bid price : 11.51 Bid-YTW : 4.74 % |

| SLF.PR.E | Deemed-Retractible | -1.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.98 Bid-YTW : 7.77 % |

| BMO.PR.M | FixedReset | -1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.25 Bid-YTW : 4.02 % |

| BAM.PR.R | FixedReset | -1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 12.15 Evaluated at bid price : 12.15 Bid-YTW : 5.98 % |

| SLF.PR.D | Deemed-Retractible | -1.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.78 Bid-YTW : 7.86 % |

| BMO.PR.S | FixedReset | -1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 16.95 Evaluated at bid price : 16.95 Bid-YTW : 4.50 % |

| TD.PR.T | FloatingReset | -1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.50 Bid-YTW : 4.69 % |

| MFC.PR.F | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 11.60 Bid-YTW : 12.07 % |

| GWO.PR.I | Deemed-Retractible | -1.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.05 Bid-YTW : 7.72 % |

| BMO.PR.Y | FixedReset | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 18.60 Evaluated at bid price : 18.60 Bid-YTW : 4.53 % |

| SLF.PR.C | Deemed-Retractible | -1.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.04 Bid-YTW : 7.67 % |

| TD.PR.Y | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.55 Bid-YTW : 3.98 % |

| SLF.PR.A | Deemed-Retractible | -1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.25 Bid-YTW : 7.17 % |

| ELF.PR.H | Perpetual-Discount | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 22.28 Evaluated at bid price : 22.57 Bid-YTW : 6.15 % |

| CCS.PR.C | Deemed-Retractible | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.11 Bid-YTW : 7.55 % |

| TD.PF.C | FixedReset | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 16.60 Evaluated at bid price : 16.60 Bid-YTW : 4.50 % |

| RY.PR.L | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.51 Bid-YTW : 4.11 % |

| GWO.PR.R | Deemed-Retractible | -1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.00 Bid-YTW : 7.40 % |

| BAM.PR.N | Perpetual-Discount | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 19.27 Evaluated at bid price : 19.27 Bid-YTW : 6.26 % |

| BNS.PR.N | Deemed-Retractible | -1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.85 Bid-YTW : 5.43 % |

| SLF.PR.B | Deemed-Retractible | -1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.40 Bid-YTW : 7.12 % |

| CIU.PR.C | FixedReset | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 9.90 Evaluated at bid price : 9.90 Bid-YTW : 4.75 % |

| PWF.PR.O | Perpetual-Premium | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 24.40 Evaluated at bid price : 24.91 Bid-YTW : 5.85 % |

| PWF.PR.H | Perpetual-Premium | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 24.57 Evaluated at bid price : 24.82 Bid-YTW : 5.83 % |

| GWO.PR.N | FixedReset | 1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.32 Bid-YTW : 11.24 % |

| RY.PR.W | Perpetual-Discount | 1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 22.66 Evaluated at bid price : 22.90 Bid-YTW : 5.36 % |

| BAM.PF.E | FixedReset | 2.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 15.95 Evaluated at bid price : 15.95 Bid-YTW : 5.38 % |

| PWF.PR.Q | FloatingReset | 32.39 % | Just a pullback from yesterday‘s nonsense. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 10.75 Evaluated at bid price : 10.75 Bid-YTW : 4.76 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| NA.PR.X | FixedReset | 167,480 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 23.08 Evaluated at bid price : 24.81 Bid-YTW : 5.47 % |

| RY.PR.Q | FixedReset | 167,128 | Scotia crossed blocks of 20,000 and 91,500, both at 25.42. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 23.26 Evaluated at bid price : 25.35 Bid-YTW : 5.07 % |

| TD.PF.G | FixedReset | 94,653 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 23.26 Evaluated at bid price : 25.35 Bid-YTW : 5.13 % |

| POW.PR.C | Perpetual-Premium | 78,100 | TD crossed 67,800 at 24.80. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 24.50 Evaluated at bid price : 24.75 Bid-YTW : 5.92 % |

| BMO.PR.R | FloatingReset | 61,900 | Scotia crossed blocks of 20,000 and 40,000, both at 21.50. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.40 Bid-YTW : 4.83 % |

| BNS.PR.E | FixedReset | 50,782 | Scotia crossed 29,000 at 25.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-11 Maturity Price : 23.24 Evaluated at bid price : 25.27 Bid-YTW : 5.07 % |

| There were 47 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PR.E | Ratchet | Quote: 11.61 – 12.86 Spot Rate : 1.2500 Average : 0.6887 YTW SCENARIO |

| BAM.PR.K | Floater | Quote: 8.00 – 9.01 Spot Rate : 1.0100 Average : 0.6016 YTW SCENARIO |

| BAM.PF.G | FixedReset | Quote: 16.95 – 18.00 Spot Rate : 1.0500 Average : 0.6512 YTW SCENARIO |

| RY.PR.K | FloatingReset | Quote: 22.00 – 22.83 Spot Rate : 0.8300 Average : 0.5400 YTW SCENARIO |

| BAM.PR.Z | FixedReset | Quote: 15.89 – 16.90 Spot Rate : 1.0100 Average : 0.7364 YTW SCENARIO |

| FTS.PR.K | FixedReset | Quote: 14.80 – 15.50 Spot Rate : 0.7000 Average : 0.4491 YTW SCENARIO |

re:

REI

The first of more to come as debt becomes the focus to appreciate the common shares and maintain credit ratings in a soft (not depressed) market.

Case in point this week:

Deutsche Bank AG said it would buy back $5.4 billion of its debt, in a move designed to bolster investor confidence in the German lender’s finances.