Hurray! Food delivery robots!

When the staff at Starship Technologies in Tallinn, Estonia are ready for lunch, they’ll order a few pizzas just like any other office. But they don’t have a human do the pickup or delivery. Instead, a two-foot high, forty-pound, self-driving robot on wheels will get the job.

The staff made up of engineers and project managers sometimes use a credit line with the local pizzeria. Or they’ll just put cash inside the robot itself. The machine is covered with carefully concealed sensors and nine cameras, so that on a bank of screens in the office, they can get a first-person view of its journey from a couple feet off the ground, traversing pavements and passing by pedestrians to pick up their order. Once they see the robot is in the pizzeria, they’ll hit a button to unlock the hatch so the restaurant can get the cash and put in the hot pizzas.

This is the future of delivery, according to Starship, whose robots are 90-99% automated, according to its CFO, Allan Martinson.

A fascinating example of technological disruption is blockchains in finance:

The risk posed by fraud in the $4 trillion trade-financing industry has prompted banks to start exploring distributed-ledger technology like the one that underpins bitcoin.

Standard Chartered Plc, which lost almost $200 million from a fraud at China’s Qingdao port two years ago, has teamed up with DBS Group Holdings Ltd. to develop an electronic ledger of invoices that uses a parallel platform to the blockchain employed in bitcoin transactions. Lenders such as Bank of America Corp. and HSBC Holdings Plc say they’re looking at blockchain for trade finance and other banking applications.

Blockchain proponents argue that the technology will change the face of banking, helping lenders cut billions of dollars in costs. Trade financing, a centuries-old banking mainstay, may become ground zero for blockchain adoption because it promises to do away with paper invoices and the fraud that accompanies them — if banks can come together around a joint platform.

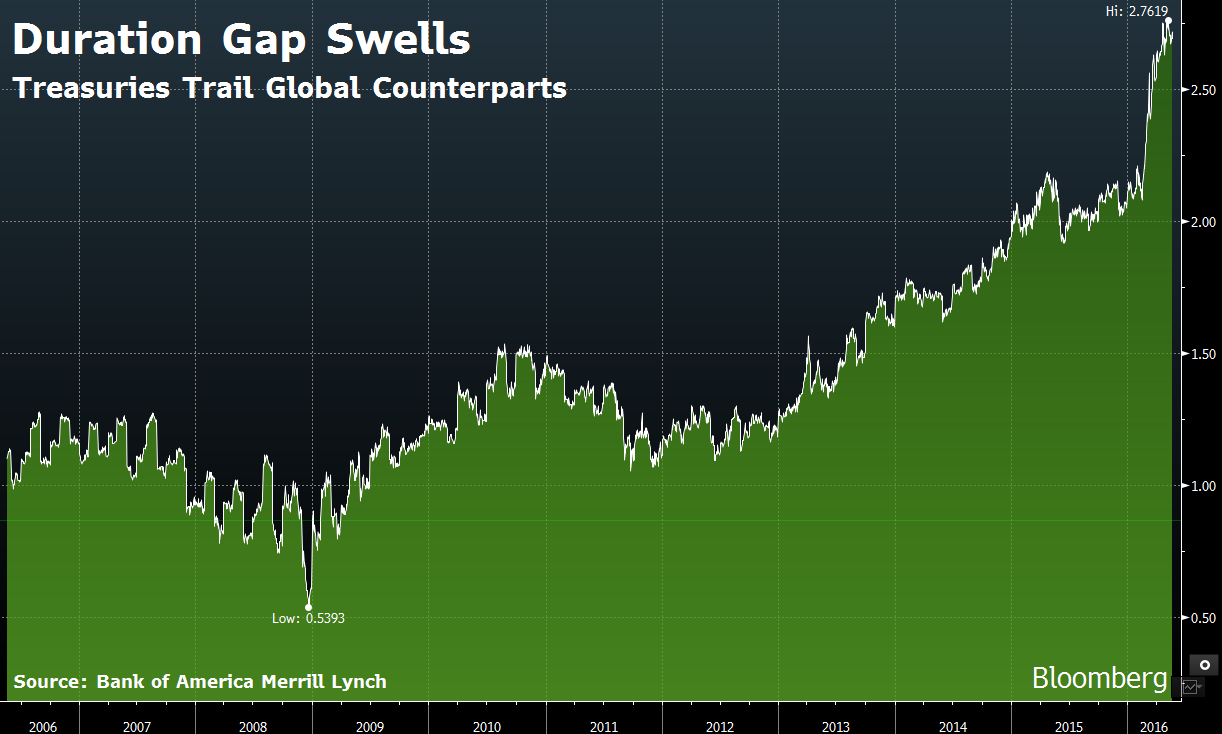

There was a nice article on Bloomberg about Treasury duration management:

To lock in historically low interest rates, Belgium, Canada, France, Mexico, Spain, Switzerland and the U.K. have all sold debt maturing in 40 to 100 years since 2014, even if infrequently. Not the U.S., which in the interest of keeping sales regular has stuck to securities of three decades or less. That policy has made the globe’s biggest debtor a laggard in a key bond-market metric related to the average maturity of its securities. By this measure, the gap between the U.S. and its peers has never been wider.

…

Yet by a gauge known as modified duration, a measure of debt’s price sensitivity to interest-rate changes that rises with maturity, it’s still trailing global peers. Typically, bonds with longer duration gain more when rates fall, and suffer steeper losses when rates rise.For Treasuries, the figure is 6.2, compared with 8.9 for an index that tracks the sovereign securities of more than 20 other nations, Bank of America Merrill Lynch data show. This month, the gap between the two reached the widest since at least 2006. One of the starkest contrasts is with the U.K., which issues long-dated bonds for pensions and insurers. Its debt has a duration above 10, Bank of America data show.

Click for Big

“The Treasury likes to see large, liquid markets, and something like a 50-year bond is not going to be particularly liquid,” said James Moore, head of investment solutions in Newport Beach, California, at Pacific Investment Management Co., which oversees about $1.5 trillion. “The Treasury is thinking about and balancing a multiplicity of objectives when they consider issuance, and liquidity and depth are some of them.”

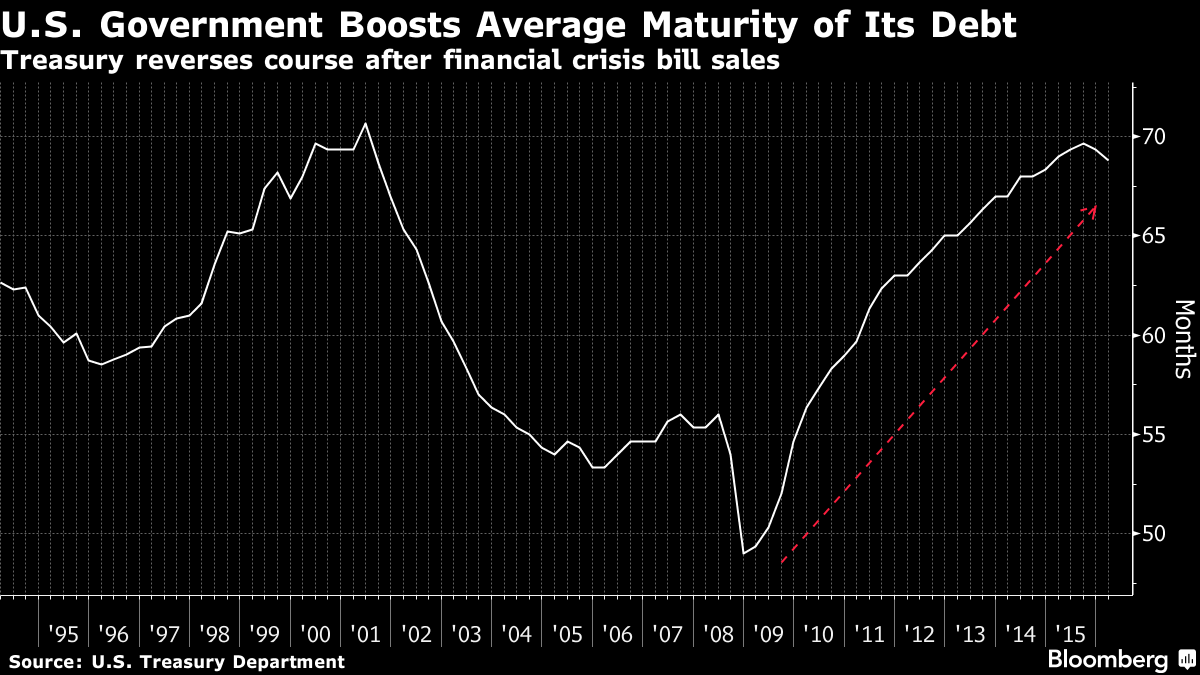

The U.S. hasn’t exactly stood still. The average lifespan of the government’s debt is now about 69 months, up from 49 in December 2008, when it was ramping up short-term bill issuance as part of emergency spending during the financial crisis, Treasury data show.

Click for Big

The Treasury’s Borrowing Advisory Committee, which includes some dealers, voiced concern over that risk in 2011, when the department last asked the group to consider ultra-long bonds. The topic has been discussed several times at quarterly gatherings since.

The primary buyers of very long-dated debt — pensions and insurers — tend to prefer higher-yielding corporate bonds. Microsoft’s 40-year bond last year was priced to yield 1.8 percentage points above 30-year Treasuries. And other investors may deem ultra-long debt too perilous because of the steep losses they’d incur should yields rise.

It’s interesting to see the car manufacturers jockeying for the new opportunities in fleet management – first, there’s Gett and Volkswagen:

Gett Inc., a taxi-ordering application that competes with Uber Technologies Inc., raised $300 million in a strategic investment from German carmaker Volkswagen AG to fund its growth in Europe and New York City.

Gett, based in Tel Aviv, Israel, has offered rides for as low as $1 and expanded its services to include deliveries of goods. The company hired Wells Fargo & Co. to find investors for the round, people familiar with the matter said in February. Volkswagen’s contribution brings total funds raised by Gett to more than $520 million, the taxi service said Tuesday in an e-mailed statement.

Volkswagen made the investment as part of a push to boost digital offerings and move beyond its diesel-engine manipulation scandal. Mobility services promise strong growth prospects and earnings potential in coming years, VW said Tuesday in a statement.

…

With operations in over 60 cities worldwide, including London, Moscow and New York, Gett is a major ride-hailing provider and services will be expanded further as part of the alliance with VW. Last month, it completed its bid to buy London’s Radio Taxis in a move that brought Gett’s car fleet in the city to 11,500, a number the company says amounts to half of all licensed taxis in the city.

…

Expanding digital services in connected cars is a cornerstone of VW’s strategy through 2025, which will be presented in mid-June. More than 250 employees are developing the plan, which will comprise eight key initiatives across the group, Mueller said last week at an internal management meeting at the carmaker’s Wolfsburg, Germany, headquarters.Volkswagen is not the first car manufacturer to get involved in the ride-hailing business. General Motors Co. bought a 9 percent stake in Lyft for $500 million in January and Apple Inc. made a $1 billion investment in China’s Didi this month.

And, of course, Car2Go is a subsidiary of Daimler, while Zipcar is, perhaps more logically, subsidiary of the old-line car rental company Avis Budget, while Hertz is trying to develop the business as a sideline. Meanwhile, Toyota is investing in Uber:

Toyota Motor Corp. said it is making a strategic investment in Uber Technologies Inc. and will offer auto leases to the ride-hailing company’s drivers.

Uber declined to disclose the size of the investment. Toyota wasn’t immediately available for comment. By leasing Toyota cars, Uber will expand its existing program, which also includes Enterprise Holdings Inc.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.74 % | 5.77 % | 11,622 | 16.92 | 1 | -1.7241 % | 1,664.5 |

| FixedFloater | 6.67 % | 5.79 % | 18,730 | 16.72 | 1 | 1.0638 % | 3,031.5 |

| Floater | 4.52 % | 4.74 % | 44,034 | 15.91 | 4 | -0.1671 % | 1,717.7 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2113 % | 2,824.3 |

| SplitShare | 4.96 % | 5.17 % | 79,136 | 3.93 | 7 | 0.2113 % | 3,305.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2113 % | 2,578.7 |

| Perpetual-Premium | 5.75 % | -11.46 % | 78,921 | 0.09 | 6 | 0.1180 % | 2,603.3 |

| Perpetual-Discount | 5.47 % | 5.57 % | 101,783 | 14.51 | 33 | 0.1485 % | 2,682.9 |

| FixedReset | 5.20 % | 4.68 % | 164,828 | 13.81 | 88 | 0.2169 % | 1,968.2 |

| Deemed-Retractible | 5.12 % | 5.57 % | 133,036 | 6.75 | 33 | 0.0745 % | 2,682.1 |

| FloatingReset | 3.19 % | 5.00 % | 26,062 | 5.26 | 17 | 0.3195 % | 2,096.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| GWO.PR.O | FloatingReset | -3.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.00 Bid-YTW : 10.45 % |

| BAM.PR.E | Ratchet | -1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 25.00 Evaluated at bid price : 14.25 Bid-YTW : 5.77 % |

| CU.PR.C | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 17.75 Evaluated at bid price : 17.75 Bid-YTW : 4.54 % |

| BAM.PR.X | FixedReset | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 13.89 Evaluated at bid price : 13.89 Bid-YTW : 4.93 % |

| BAM.PR.G | FixedFloater | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 25.00 Evaluated at bid price : 14.25 Bid-YTW : 5.79 % |

| TD.PF.F | Perpetual-Discount | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 24.16 Evaluated at bid price : 24.54 Bid-YTW : 5.02 % |

| TRP.PR.F | FloatingReset | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 13.50 Evaluated at bid price : 13.50 Bid-YTW : 4.63 % |

| SLF.PR.H | FixedReset | 1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.47 Bid-YTW : 8.79 % |

| RY.PR.M | FixedReset | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 19.12 Evaluated at bid price : 19.12 Bid-YTW : 4.52 % |

| CM.PR.Q | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 19.71 Evaluated at bid price : 19.71 Bid-YTW : 4.57 % |

| BMO.PR.Y | FixedReset | 1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 20.15 Evaluated at bid price : 20.15 Bid-YTW : 4.43 % |

| FTS.PR.H | FixedReset | 2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 13.20 Evaluated at bid price : 13.20 Bid-YTW : 4.33 % |

| TRP.PR.I | FloatingReset | 2.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 11.25 Evaluated at bid price : 11.25 Bid-YTW : 4.69 % |

| FTS.PR.I | FloatingReset | 2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 11.67 Evaluated at bid price : 11.67 Bid-YTW : 4.29 % |

| HSE.PR.B | FloatingReset | 3.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 10.70 Evaluated at bid price : 10.70 Bid-YTW : 5.40 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TRP.PR.J | FixedReset | 51,779 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-31 Maturity Price : 25.00 Evaluated at bid price : 25.73 Bid-YTW : 4.85 % |

| RY.PR.Q | FixedReset | 38,165 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-24 Maturity Price : 25.00 Evaluated at bid price : 26.16 Bid-YTW : 4.48 % |

| SLF.PR.I | FixedReset | 36,900 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.60 Bid-YTW : 7.07 % |

| RY.PR.W | Perpetual-Discount | 33,222 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 24.23 Evaluated at bid price : 24.53 Bid-YTW : 5.01 % |

| RY.PR.R | FixedReset | 30,239 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-08-24 Maturity Price : 25.00 Evaluated at bid price : 26.26 Bid-YTW : 4.69 % |

| RY.PR.M | FixedReset | 26,200 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-05-24 Maturity Price : 19.12 Evaluated at bid price : 19.12 Bid-YTW : 4.52 % |

| There were 14 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| GWO.PR.O | FloatingReset | Quote: 13.00 – 13.79 Spot Rate : 0.7900 Average : 0.5107 YTW SCENARIO |

| TRP.PR.D | FixedReset | Quote: 17.36 – 17.75 Spot Rate : 0.3900 Average : 0.2476 YTW SCENARIO |

| BAM.PR.E | Ratchet | Quote: 14.25 – 14.75 Spot Rate : 0.5000 Average : 0.3795 YTW SCENARIO |

| TD.PF.B | FixedReset | Quote: 18.03 – 18.38 Spot Rate : 0.3500 Average : 0.2378 YTW SCENARIO |

| TD.PR.S | FixedReset | Quote: 22.75 – 23.24 Spot Rate : 0.4900 Average : 0.3841 YTW SCENARIO |

| ELF.PR.G | Perpetual-Discount | Quote: 21.10 – 21.50 Spot Rate : 0.4000 Average : 0.2985 YTW SCENARIO |

Beware the next industrial revolution (or embrace it and see the advantage)

http://www.bbc.com/news/technology-36376966

http://www.foxnews.com/leisure/2016/05/25/pizza-hut-rolling-out-robot-servers-in-japan/

Need a serious re-think on employment and unemployment models.