There are mutterings about increasing foreign holdings of Canada bonds:

The Canadian fixed-income market is exposed to foreign investors like never before, said Warren Lovely, head of public-sector research at National Bank. And with Canada’s once-superior economic stature having slouched under the weight of the commodity shock, the appeal of Canadian bonds to global investors could fade, he said.

“If not a full-blown systemic risk, Canada’s leverage to foreign portfolio investors is a notable vulnerability for the country’s capital markets and debt issuers,” he said.

Click for Big

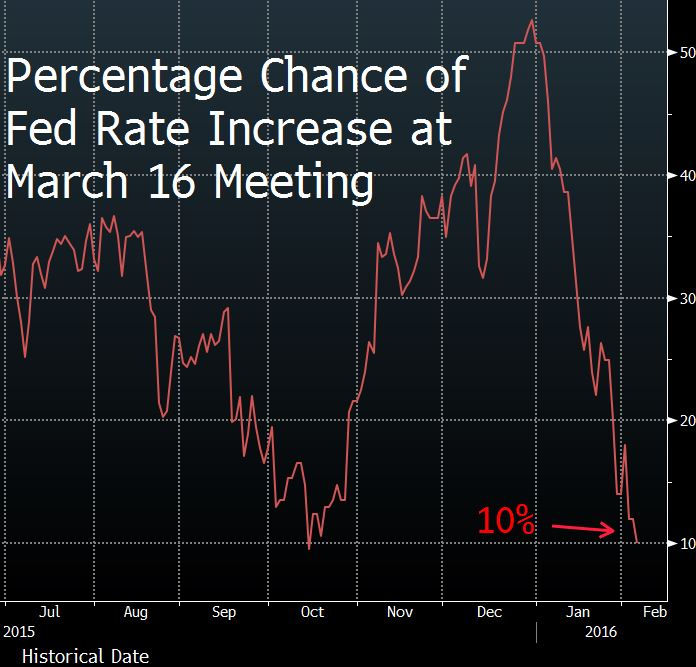

Morgan Stanley has prepared some interesting charts on global monetary policy:

The Bank of England voted unanimously not to raise interest rates Thursday, as the sole dissenter on the Monetary Policy Committee abandoned his recent calls to tighten policy. The European Commission also slashed its inflation forecasts, all but guaranteeing more quantitative easing when the European Central Bank next meets in March. Now, given the world’s deteriorating economic backdrop, that December rate increase from the Federal Reserve looks increasingly anachronistic.

Click for Big

Click for Big

Click for Big

S&P published a review article titled Negative Interest Rates: Why Central Banks Can Defy “Time Preference”. It’s mainly about the BoJ move to negative policy rates, but concluded:

Since the Global Financial Crisis erupted in 2008 and triggered the Great Recession and ushered in a period of secular macro deleveraging, the major central banks of the world have progressively implemented all manner of “unconventional” monetary policy measures. There are now five major central banks implementing some form of negative interest rate policy. Two of those central banks are also implementing full-fledged QE. The Federal Reserve has made one interest rate hike, but it continues to have a balance sheet with a stock of QE on it to the tune of more than $3 trillion. Similarly the Bank of England, while not having raised interest rates yet, maintains a much enlarged balance sheet, thanks to its earlier five rounds of QE. Several major central banks have experimented with various forms of forward guidance too.

When future historians look back on this period, they will likely describe a world in which the major central banks all experimented with new forms of monetary policy easing and learned from one another in the process, as one central bank after another pioneered new policy innovations and others adopted and adapted them, some rapidly, others with long lags. Disentangling cause and effect in the process of cross-fertilization and adaptation will be no simple feat.

There is nothing new in this of course: The 20 years or so preceding the financial crisis were ones in which similar cross-fertilization of ideas and practice occurred, as what become known as “flexible inflation targeting” became the orthodoxy of central banking, before it was confronted by the ghost of Hyman Minsky (14).

It is my compelling sense that this process of cross-pollination of policy learning and institutional evolution is far from over. The journey into uncharted monetary waters continues.

It was a good day for the Canadian preferred share market, with PerpetualDiscounts winning 62bp, FixedResets up 54bp and DeemedRetractibles gaining 8bp. The Performance Highlights table is lengthy. Volume was average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

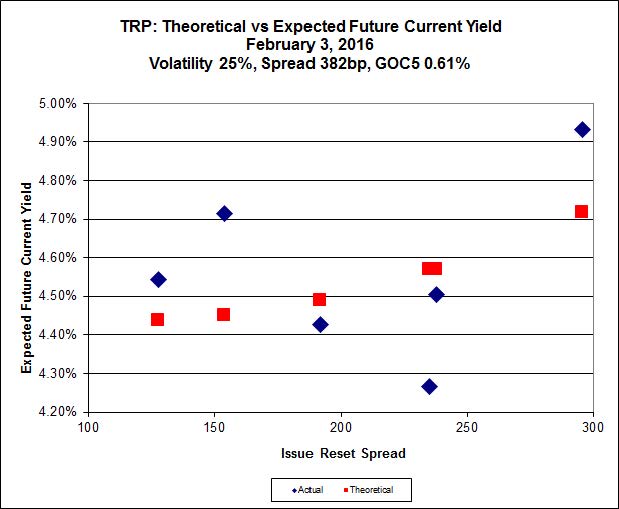

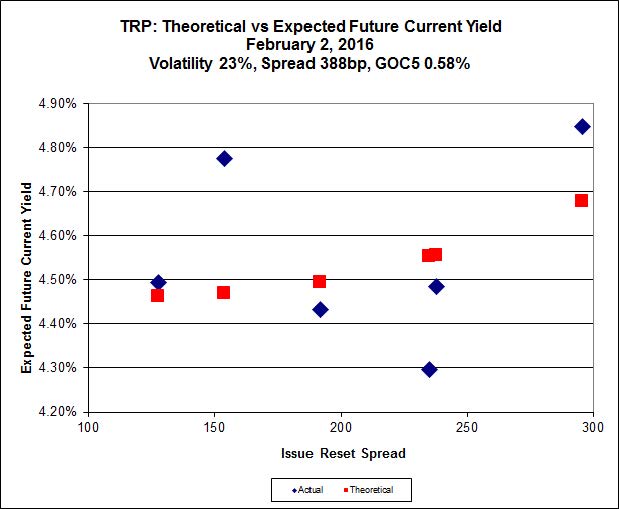

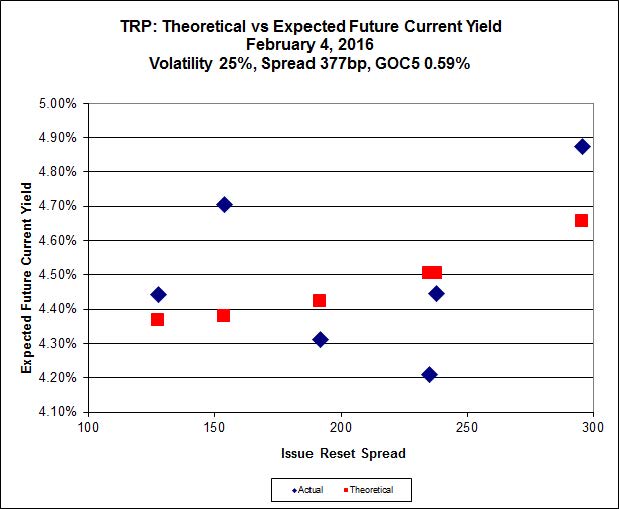

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.46 to be $1.14 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $0.86 cheap at its bid price of 18.21.

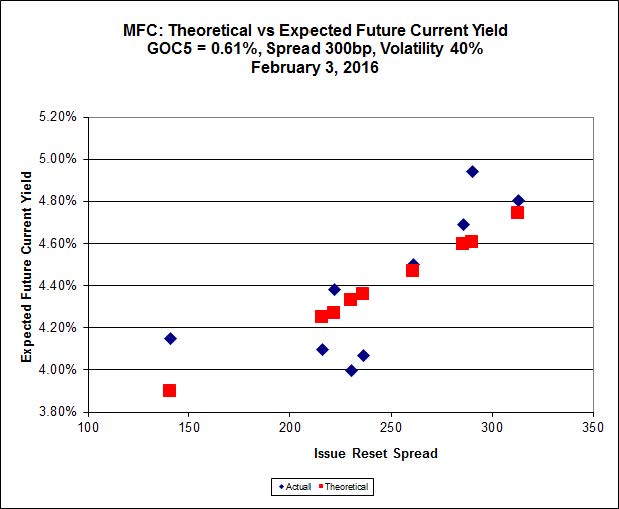

Click for Big

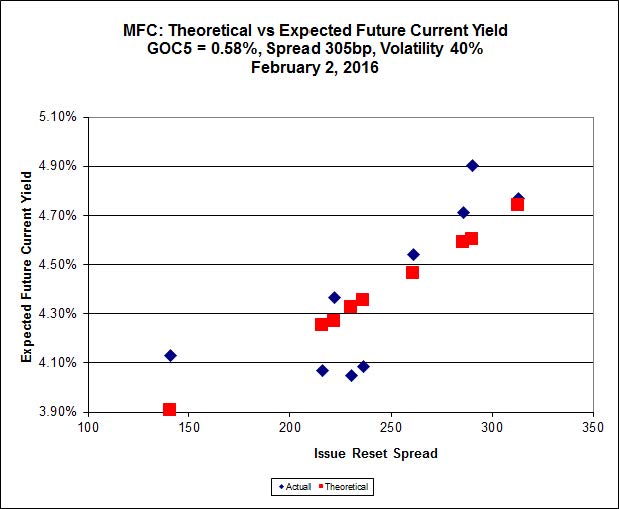

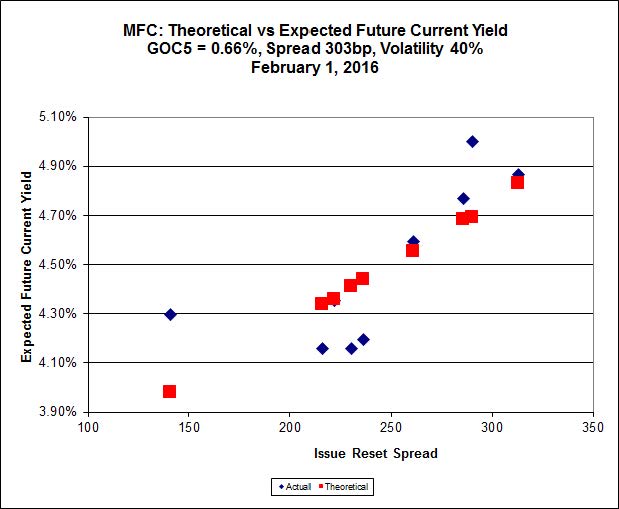

Most expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 18.35 to be 1.36 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 18.15 to be 1.20 cheap.

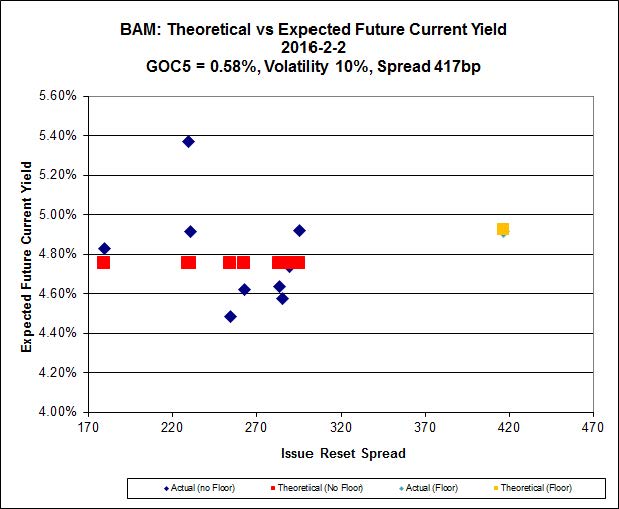

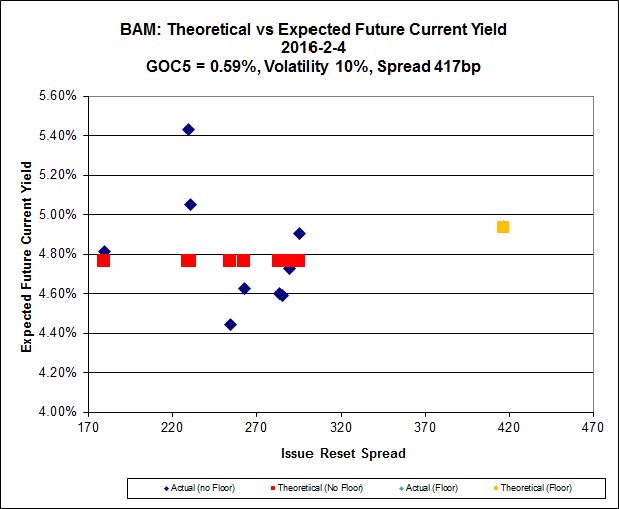

Click for Big

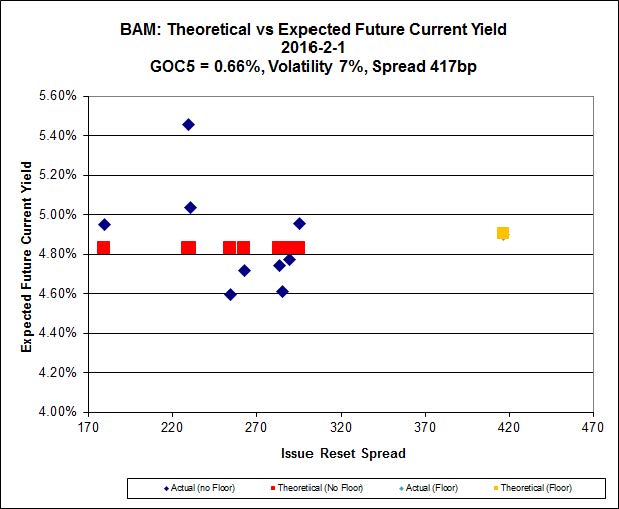

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 13.30 to be $1.88 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 17.66 and appears to be $1.17 rich.

Click for Big

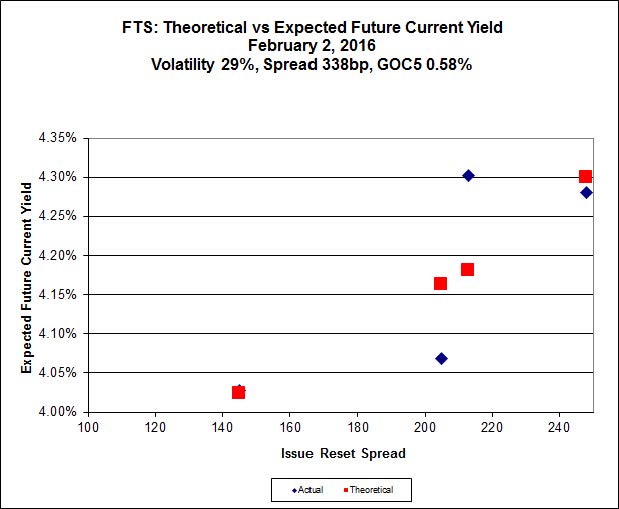

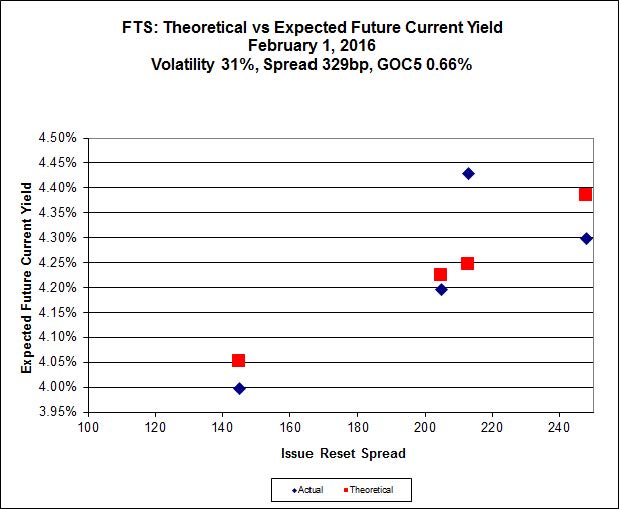

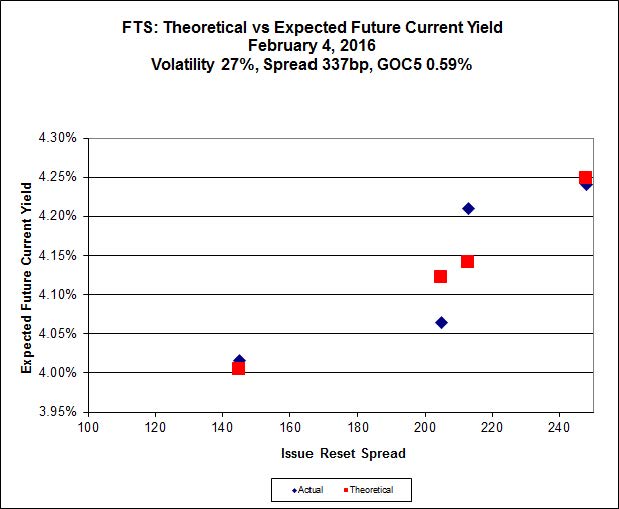

FTS.PR.K, with a spread of +205bp, and bid at 16.24, looks $0.23 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 16.15 and is $0.27 cheap.

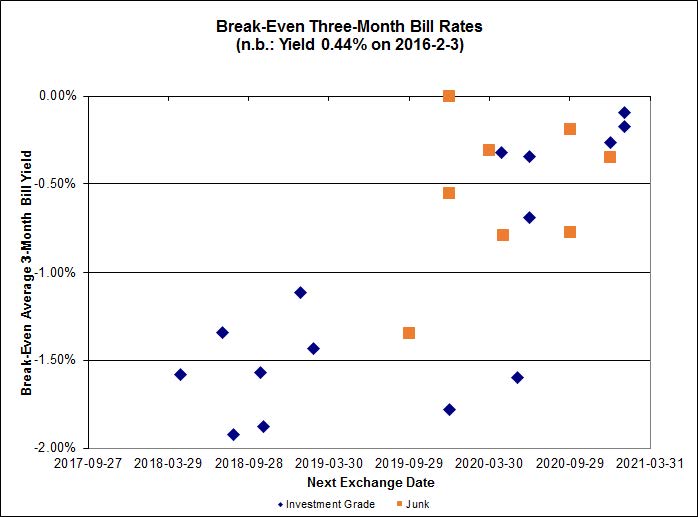

Click for Big

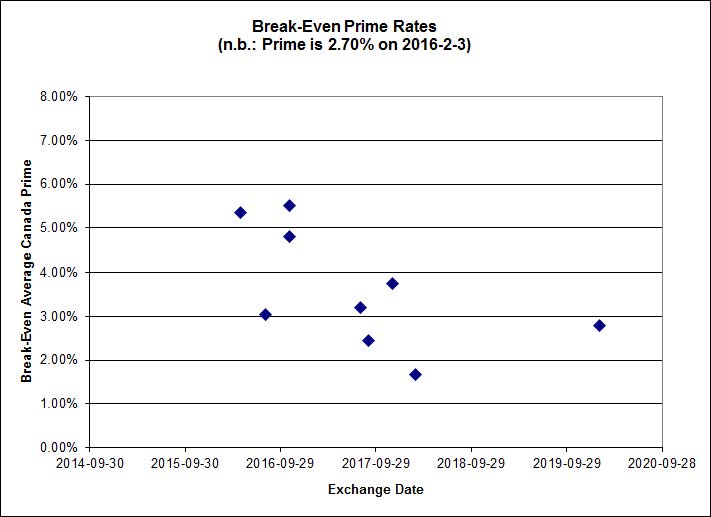

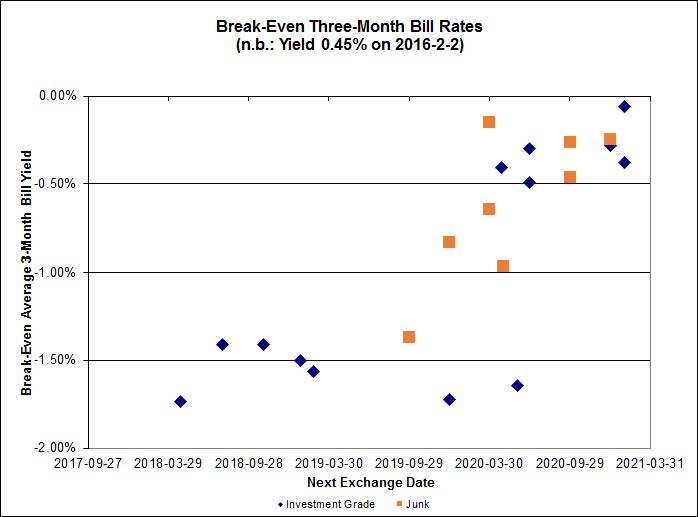

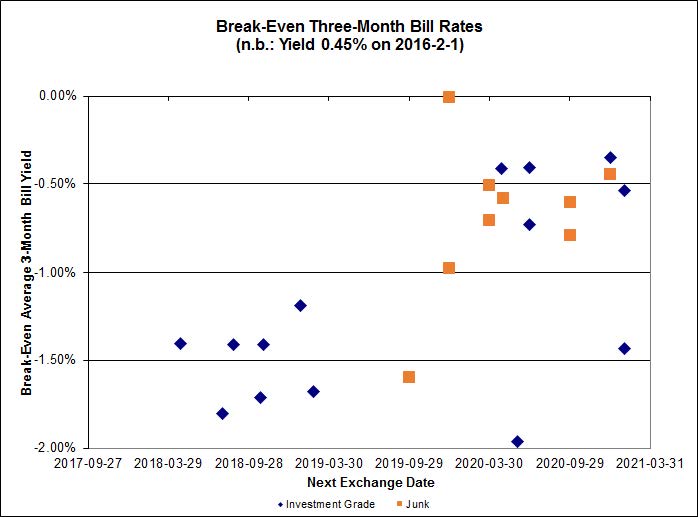

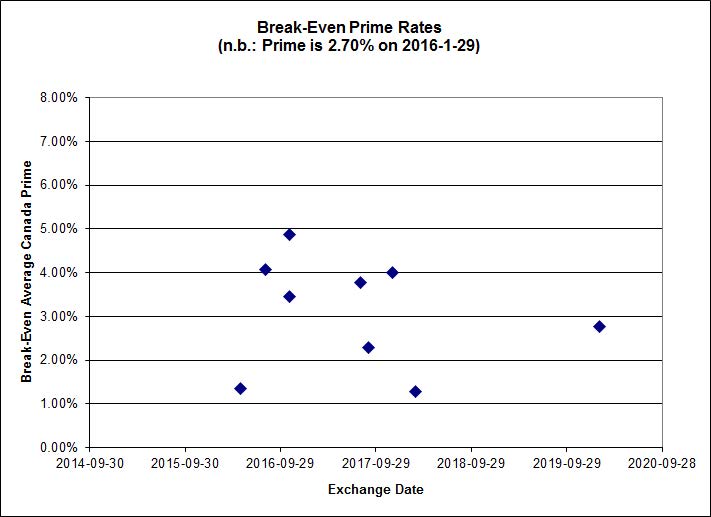

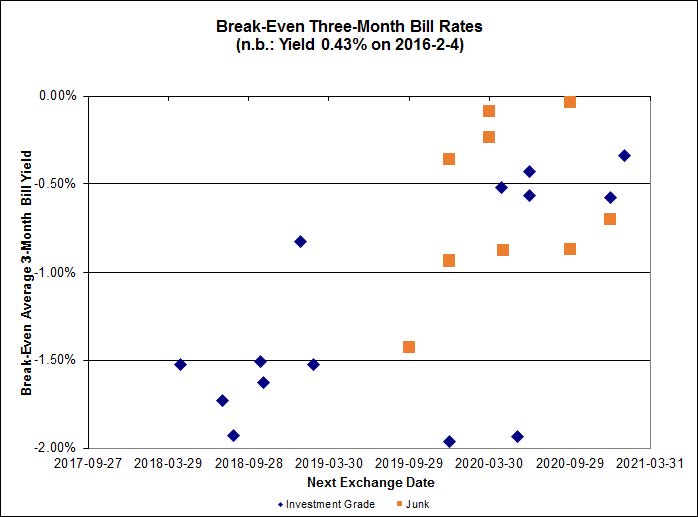

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.98%, with two outliers above 0.00%. There are two junk outliers above 0.00%.

Click for Big

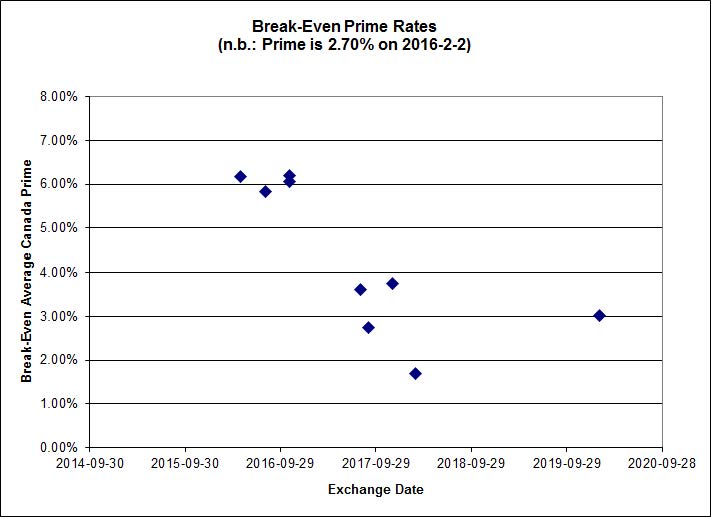

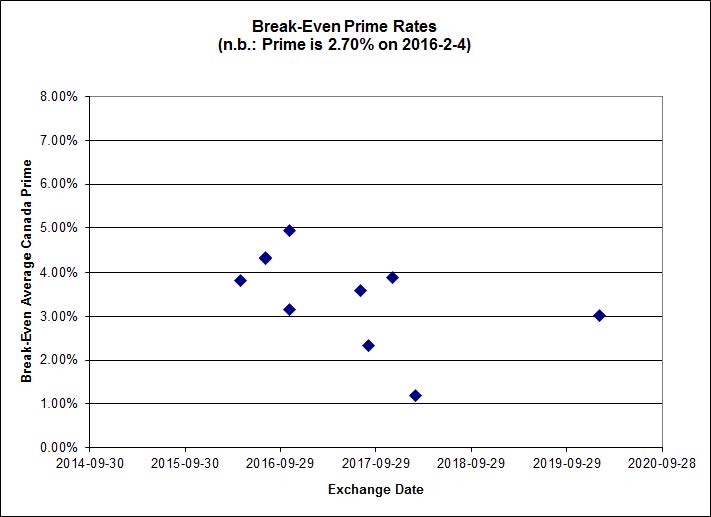

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.29 % | 6.43 % | 17,743 | 16.16 | 1 | 0.0000 % | 1,474.7 |

| FixedFloater | 7.54 % | 6.59 % | 27,398 | 15.69 | 1 | 0.8000 % | 2,636.9 |

| Floater | 4.60 % | 4.74 % | 73,652 | 15.95 | 4 | 1.0079 % | 1,667.0 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1181 % | 2,703.8 |

| SplitShare | 4.88 % | 6.33 % | 80,663 | 2.70 | 6 | 0.1181 % | 3,164.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1181 % | 2,468.7 |

| Perpetual-Premium | 5.83 % | 5.83 % | 81,018 | 13.99 | 6 | 0.3798 % | 2,530.2 |

| Perpetual-Discount | 5.76 % | 5.80 % | 99,183 | 14.18 | 33 | 0.6211 % | 2,511.3 |

| FixedReset | 5.46 % | 4.86 % | 225,799 | 14.39 | 83 | 0.5445 % | 1,856.7 |

| Deemed-Retractible | 5.24 % | 5.75 % | 131,429 | 6.94 | 34 | 0.0779 % | 2,576.4 |

| FloatingReset | 3.04 % | 4.54 % | 52,268 | 5.56 | 16 | 0.3644 % | 2,018.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| FTS.PR.I | FloatingReset | -2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 10.04 Evaluated at bid price : 10.04 Bid-YTW : 4.80 % |

| CIU.PR.C | FixedReset | -1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 10.29 Evaluated at bid price : 10.29 Bid-YTW : 4.97 % |

| TD.PF.E | FixedReset | -1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 19.56 Evaluated at bid price : 19.56 Bid-YTW : 4.61 % |

| HSE.PR.C | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 14.90 Evaluated at bid price : 14.90 Bid-YTW : 6.80 % |

| BNS.PR.D | FloatingReset | -1.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.01 Bid-YTW : 7.25 % |

| HSE.PR.G | FixedReset | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 15.90 Evaluated at bid price : 15.90 Bid-YTW : 6.89 % |

| BNS.PR.F | FloatingReset | -1.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.77 Bid-YTW : 7.98 % |

| MFC.PR.F | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.02 Bid-YTW : 11.81 % |

| PWF.PR.T | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 20.78 Evaluated at bid price : 20.78 Bid-YTW : 3.89 % |

| W.PR.K | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 22.69 Evaluated at bid price : 23.80 Bid-YTW : 5.54 % |

| BAM.PF.C | Perpetual-Discount | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 19.72 Evaluated at bid price : 19.72 Bid-YTW : 6.24 % |

| RY.PR.N | Perpetual-Discount | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 22.35 Evaluated at bid price : 22.65 Bid-YTW : 5.41 % |

| BNS.PR.P | FixedReset | 1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.26 Bid-YTW : 3.55 % |

| FTS.PR.M | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 18.10 Evaluated at bid price : 18.10 Bid-YTW : 4.72 % |

| CIU.PR.A | Perpetual-Discount | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 19.71 Evaluated at bid price : 19.71 Bid-YTW : 5.85 % |

| BMO.PR.Z | Perpetual-Discount | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 22.73 Evaluated at bid price : 23.10 Bid-YTW : 5.41 % |

| BMO.PR.W | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 17.22 Evaluated at bid price : 17.22 Bid-YTW : 4.48 % |

| CU.PR.F | Perpetual-Discount | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 19.68 Evaluated at bid price : 19.68 Bid-YTW : 5.73 % |

| CM.PR.O | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 17.80 Evaluated at bid price : 17.80 Bid-YTW : 4.49 % |

| BAM.PF.A | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 18.46 Evaluated at bid price : 18.46 Bid-YTW : 5.10 % |

| TRP.PR.B | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 10.52 Evaluated at bid price : 10.52 Bid-YTW : 4.83 % |

| BAM.PR.C | Floater | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 9.96 Evaluated at bid price : 9.96 Bid-YTW : 4.79 % |

| BNS.PR.A | FloatingReset | 1.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.80 Bid-YTW : 4.10 % |

| BIP.PR.B | FixedReset | 1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 22.70 Evaluated at bid price : 23.81 Bid-YTW : 5.82 % |

| RY.PR.M | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 4.52 % |

| VNR.PR.A | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 5.31 % |

| CM.PR.Q | FixedReset | 1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 19.03 Evaluated at bid price : 19.03 Bid-YTW : 4.63 % |

| BAM.PF.D | Perpetual-Discount | 1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 19.99 Evaluated at bid price : 19.99 Bid-YTW : 6.22 % |

| BAM.PR.M | Perpetual-Discount | 1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 19.52 Evaluated at bid price : 19.52 Bid-YTW : 6.17 % |

| MFC.PR.H | FixedReset | 1.80 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.81 Bid-YTW : 7.22 % |

| BAM.PR.K | Floater | 1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 10.08 Evaluated at bid price : 10.08 Bid-YTW : 4.74 % |

| TRP.PR.A | FixedReset | 1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 14.55 Evaluated at bid price : 14.55 Bid-YTW : 4.77 % |

| BAM.PR.N | Perpetual-Discount | 1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 19.58 Evaluated at bid price : 19.58 Bid-YTW : 6.15 % |

| MFC.PR.J | FixedReset | 1.84 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.22 Bid-YTW : 7.87 % |

| IAG.PR.G | FixedReset | 1.93 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.51 Bid-YTW : 7.84 % |

| NA.PR.W | FixedReset | 1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 16.56 Evaluated at bid price : 16.56 Bid-YTW : 4.76 % |

| HSE.PR.A | FixedReset | 1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 8.79 Evaluated at bid price : 8.79 Bid-YTW : 6.97 % |

| W.PR.J | Perpetual-Discount | 2.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 22.62 Evaluated at bid price : 22.87 Bid-YTW : 6.18 % |

| MFC.PR.I | FixedReset | 2.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.90 Bid-YTW : 7.64 % |

| MFC.PR.G | FixedReset | 2.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.15 Bid-YTW : 8.15 % |

| GWO.PR.N | FixedReset | 2.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.50 Bid-YTW : 11.10 % |

| W.PR.H | Perpetual-Discount | 2.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 22.50 Evaluated at bid price : 22.76 Bid-YTW : 6.10 % |

| BAM.PF.E | FixedReset | 3.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 17.66 Evaluated at bid price : 17.66 Bid-YTW : 5.02 % |

| BAM.PF.G | FixedReset | 3.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 18.65 Evaluated at bid price : 18.65 Bid-YTW : 5.11 % |

| FTS.PR.G | FixedReset | 4.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 16.15 Evaluated at bid price : 16.15 Bid-YTW : 4.67 % |

| BAM.PF.B | FixedReset | 5.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 17.40 Evaluated at bid price : 17.40 Bid-YTW : 5.05 % |

| TRP.PR.I | FloatingReset | 9.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 11.52 Evaluated at bid price : 11.52 Bid-YTW : 4.35 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| NA.PR.X | FixedReset | 372,600 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 23.14 Evaluated at bid price : 24.98 Bid-YTW : 5.54 % |

| TD.PF.G | FixedReset | 127,910 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-30 Maturity Price : 25.00 Evaluated at bid price : 25.52 Bid-YTW : 5.14 % |

| BNS.PR.Z | FixedReset | 127,490 | Desjardins crossed blocks of 40,000 and 29,100, both at 18.82. TD crossed 50,000 at 18.85. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.94 Bid-YTW : 7.12 % |

| RY.PR.Q | FixedReset | 117,729 | RBC crossed two blocks of 25,000 each and one of 30,000, all at 25.63. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 23.32 Evaluated at bid price : 25.56 Bid-YTW : 5.13 % |

| HSB.PR.D | Deemed-Retractible | 101,940 | Nesbitt crossed 99,700 at 24.90. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.85 Bid-YTW : 5.24 % |

| NA.PR.W | FixedReset | 85,609 | Scotia crossed blocks of 32,200 and 40,000, both at 16.30. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-04 Maturity Price : 16.56 Evaluated at bid price : 16.56 Bid-YTW : 4.76 % |

| There were 35 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PF.F | FixedReset | Quote: 18.80 – 20.00 Spot Rate : 1.2000 Average : 0.9477 YTW SCENARIO |

| W.PR.K | FixedReset | Quote: 23.80 – 24.49 Spot Rate : 0.6900 Average : 0.4580 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 17.00 – 17.64 Spot Rate : 0.6400 Average : 0.4179 YTW SCENARIO |

| W.PR.J | Perpetual-Discount | Quote: 22.87 – 23.40 Spot Rate : 0.5300 Average : 0.3652 YTW SCENARIO |

| FTS.PR.I | FloatingReset | Quote: 10.04 – 10.57 Spot Rate : 0.5300 Average : 0.3980 YTW SCENARIO |

| BAM.PR.N | Perpetual-Discount | Quote: 19.58 – 19.98 Spot Rate : 0.4000 Average : 0.2794 YTW SCENARIO |