AltaGas Ltd. has announced:

that it will issue 4,000,000 Cumulative 5-Year Minimum Rate Reset Redeemable Preferred Shares, Series I (the “Series I Preferred Shares”), at a price of $25.00 per Series I Preferred Share (the “Offering”) for aggregate gross proceeds of $100 million on a bought deal basis. The Series I Preferred Shares will be offered to the public through a syndicate of underwriters co-led by RBC Capital Markets, BMO Capital Markets and Scotiabank.

Holders of the Series I Preferred Shares will be entitled to receive a cumulative quarterly fixed dividend for the initial period ending on but excluding December 31, 2020 (the “Initial Period”) at an annual rate of 5.25%, payable on the last day of March, June, September and December, as and when declared by the Board of Directors of AltaGas. The first quarterly dividend payment is payable on March 31, 2016 and shall be $0.46387 per Series I Preferred Share. The dividend rate will reset on December 31, 2020 and every five years thereafter at a rate equal to the sum of the then five-year Government of Canada bond yield plus 4.19%, provided that, in any event, such rate shall not be less than 5.25% per annum. The Series I Preferred Shares are redeemable by AltaGas, at its option, on December 31, 2020 and on December 31 of every fifth year thereafter.

Holders of Series I Preferred Shares will have the right to convert all or any part of their shares into Cumulative Redeemable Floating Rate Preferred Shares, Series J (the “Series J Preferred Shares”), subject to certain conditions, on December 31, 2020 and on December 31 every fifth year thereafter. Holders of Series J Preferred Shares will be entitled to receive a cumulative quarterly floating dividend at a rate equal to the sum of the then 90-day Government of Canada Treasury Bill yield plus 4.19%, as and when declared by the Board of Directors of AltaGas.

The Offering is expected to close on or about November 23, 2015. Net proceeds will be used to reduce outstanding indebtedness and for general corporate purposes. AltaGas has granted to the underwriters an option, exercisable in whole or in part at any time up to 48 hours prior to closing of the Offering, to purchase up to an additional 2,000,000 Series I Preferred Shares at a price of $25.00 per share.

The Series I Preferred Shares will be issued pursuant to a prospectus supplement that will be filed with securities regulatory authorities in Canada under AltaGas’ short form base shelf prospectus dated August 10, 2015. The Offering is only being made by way of a prospectus. The prospectus contains important detailed information about the securities being offered. The Offering is subject to receipt of all necessary regulatory and stock exchange approvals.

Later, they announced:

that as a result of strong investor demand for its previously announced offering of Cumulative 5-Year Minimum Rate Reset Redeemable Preferred Shares, Series I (the “Series I Preferred Shares”), the size of the offering has been increased to 8,000,000 Series I Preferred Shares, for aggregate gross proceeds of $200,000,000. The syndicate of underwriters is being co-led by RBC Capital Markets, BMO Capital Markets, and Scotiabank.

So this is the third new issue to come with a reset floor, following BAM.PF.H and CU.PR.I. The structure is proving popular!

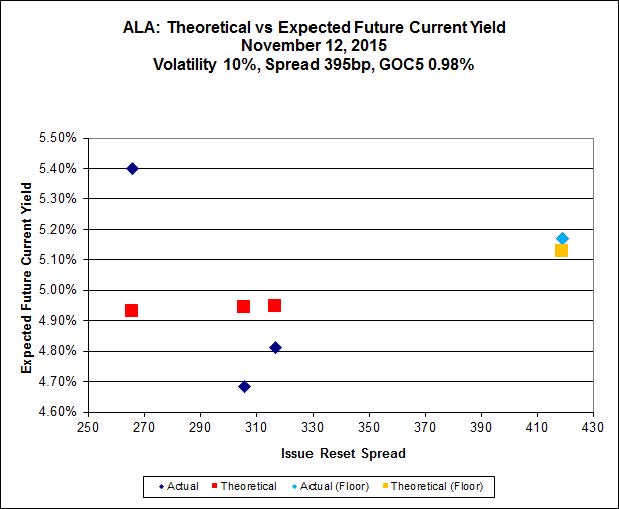

This issue joins the ALA.PR.A, ALA.PR.E and ALA.PR.G FixedResets, which have Issue Reset Spreads of +266, +317 and +308, respectively (also trading is ALA.PR.B, the Strong Pair with ALA.PR.A). Four issues with a wide range of spreads is enough to make an approximation of an Implied Volatility calculation, but it’s not terribly informative:

Click for Big

Probably not entirely coincidentally, the ALA was confirmed at Pfd-3 by DBRS today:

DBRS Limited (DBRS) has today confirmed the Issuer Rating and the Medium-Term Notes (MTNs) rating of AltaGas Ltd. (AltaGas or the Company) at BBB and its Preferred Shares – Cumulative rating at Pfd-3, all with Stable trends. The ratings reflect the Company’s well-diversified business risk profile with nearly 90% of the Company’s earnings generated from relatively low-risk predictable regulated utility returns and fee-based medium- to long-term contacts in the power and gas segments with investment-grade counterparties.

…

DBRS believes that the Company’s credit metrics are at reasonable levels for the current rating based on its business risk profile. Company’s capital expenditures (excluding acquisitions) for 2016 are expected to be comparable with the $600 million to $700 million range expected for the full year 2015, primarily for the completion of the Townsend gas processing facility (expected in service in mid-2016) in the gas segment and system betterment programs and upgrades in the utilities segment. DBRS expects leverage to rise modestly in the near term but become more manageable once projects are placed in service and provide incremental cash flow. DBRS expects AltaGas to fund its growth projects and acquisitions with a prudent mix of debt and equity in order to maintain company’s debt-to-capital ratio in the low-50% range.