My old buddy Bing Li is now the proud co-author of a book, Multi-Asset Investing: A Practitioner’s Framework:

Despite the accepted fact that a substantial part of the risk and return of any portfolio comes from asset allocation, we find today that the majority of investment professionals worldwide are focused on security selection. Multi-Asset Investing: A Practitioner’s Framework questions this basic structure of the investment process and investment industry.

- •Who says we have to separate alpha and beta?

- •Are the traditional definitions for risk and risk premium relevant in a multi-asset class world?

- •Do portfolios cater for the ‘real risks’ in their investment processes?

- •Does the whole Emerging Markets demarcation make sense for investing?

- •Why do active Asian managers perform much poorer compared to developed market managers?

- •Can you distinguish how much of a strategy’s performance comes from skill rather than luck?

- •Does having a performance fee for your manager create alignment or misalignment?

- •Why is the asset management transitioning from multi-asset strategies to multi-asset solutions?

These and many other questions are asked, and suggestions provided as potential solutions. Having worked together for fifteen years, the authors’ present implementable solutions which have helped them successfully manage large asset pools.

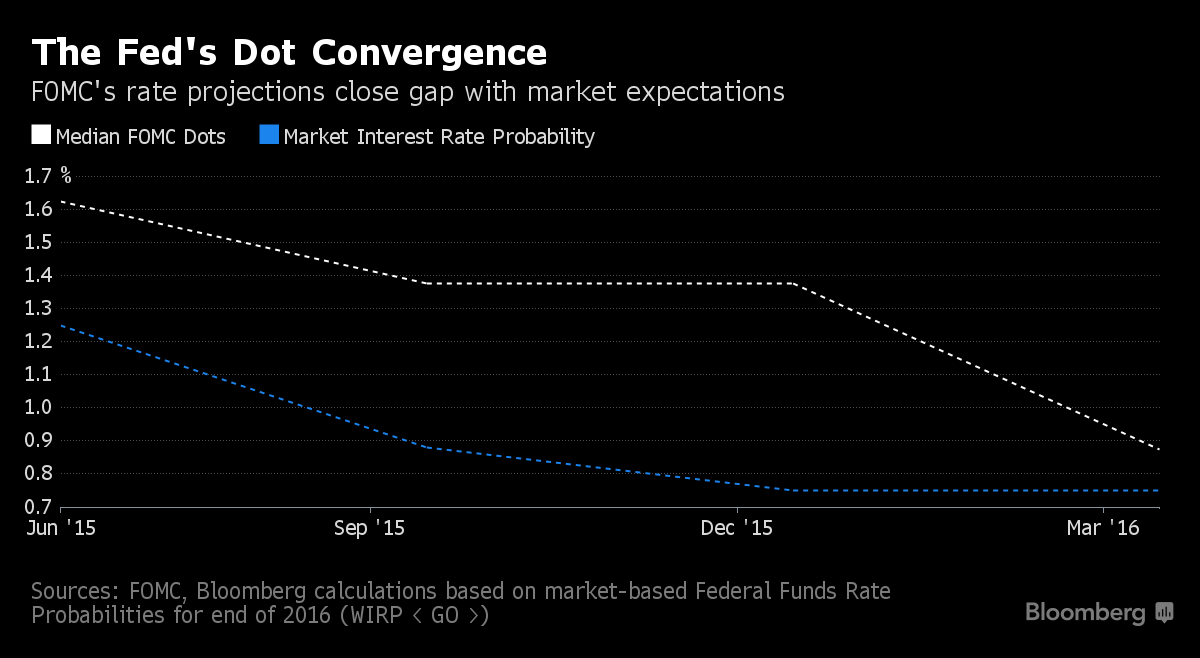

And Yellen has made a major speech:

Federal Reserve Chair Janet Yellen spelled out on Tuesday what she means by data dependence, asserting her leadership of the U.S. central bank with a clear message that interest rates will be raised at a cautious pace.

In one of her most detailed policy discussions this year, Yellen gave investors a list of conditions they need to watch for future rate hikes. Here they are:

- •Foreign economies and their financial markets need to stabilize.

- •The dollar can’t appreciate further. That would depress inflation and exports, and hurt U.S. manufacturing.

- •Commodity prices need to stabilize to help foreign producers find a better footing for growth.

- •The housing sector needs to make a larger contribution to U.S. output.

- •Inflation is a two-sided risk: Yellen is skeptical that the recent rise in core inflation, which strips out food and energy, “will prove durable.” She is watching closely.

It would be interesting, to say the least, if real-estate were to become a tradeable commodity:

Canadian house prices climbed 27 per cent over the five years from February, 2011, to February, 2016, according to the Teranet-National Bank Composite House Price index. But many foreign buyers are seeing price declines, after currency conversion (see chart below).

The currencies of China, the United States and Switzerland have gained so much against the Canadian dollar that they have outrun the increase in Canadian house prices. As a result, the citizens of these countries can buy at a lower price than in 2011: For the Chinese and Americans, it is nearly 10 per cent less; for the Swiss, it is 5 per cent less.

In most other countries, currencies rose less than Canadian house prices. Some, like the

British pound, came up just a bit short – leaving a small price increase of 2.6 per cent. Others were further behind.

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

5.10 % |

6.20 % |

10,953 |

16.46 |

1 |

1.3118 % |

1,542.8 |

| FixedFloater |

6.93 % |

6.10 % |

24,689 |

16.18 |

1 |

0.3663 % |

2,867.1 |

| Floater |

4.57 % |

4.69 % |

62,018 |

16.06 |

4 |

3.0378 % |

1,694.8 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.3100 % |

2,782.8 |

| SplitShare |

4.76 % |

5.50 % |

82,133 |

1.61 |

6 |

0.3100 % |

3,256.4 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.3100 % |

2,540.7 |

| Perpetual-Premium |

5.78 % |

-7.00 % |

84,944 |

0.09 |

6 |

0.2565 % |

2,565.7 |

| Perpetual-Discount |

5.61 % |

5.61 % |

95,746 |

14.41 |

33 |

0.0364 % |

2,587.8 |

| FixedReset |

5.30 % |

4.80 % |

186,095 |

13.85 |

87 |

0.0797 % |

1,927.7 |

| Deemed-Retractible |

5.21 % |

5.65 % |

125,473 |

5.08 |

34 |

0.0475 % |

2,613.3 |

| FloatingReset |

3.03 % |

4.93 % |

37,154 |

5.40 |

16 |

0.5563 % |

2,022.1 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| HSE.PR.G |

FixedReset |

-3.95 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 18.25

Evaluated at bid price : 18.25

Bid-YTW : 5.95 % |

| TRP.PR.D |

FixedReset |

-1.96 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 17.27

Evaluated at bid price : 17.27

Bid-YTW : 4.68 % |

| TD.PR.Y |

FixedReset |

-1.84 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.49

Bid-YTW : 4.23 % |

| PWF.PR.P |

FixedReset |

-1.80 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 12.53

Evaluated at bid price : 12.53

Bid-YTW : 4.67 % |

| TRP.PR.G |

FixedReset |

-1.54 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 19.20

Evaluated at bid price : 19.20

Bid-YTW : 4.87 % |

| BNS.PR.F |

FloatingReset |

-1.28 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.77

Bid-YTW : 8.19 % |

| GWO.PR.M |

Deemed-Retractible |

-1.17 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2018-03-31

Maturity Price : 25.25

Evaluated at bid price : 25.30

Bid-YTW : 5.65 % |

| BAM.PF.E |

FixedReset |

-1.13 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 18.31

Evaluated at bid price : 18.31

Bid-YTW : 4.81 % |

| SLF.PR.I |

FixedReset |

-1.09 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.15

Bid-YTW : 7.89 % |

| RY.PR.M |

FixedReset |

1.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 19.63

Evaluated at bid price : 19.63

Bid-YTW : 4.36 % |

| RY.PR.H |

FixedReset |

1.04 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 18.46

Evaluated at bid price : 18.46

Bid-YTW : 4.28 % |

| BAM.PR.E |

Ratchet |

1.31 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 25.00

Evaluated at bid price : 13.26

Bid-YTW : 6.20 % |

| NA.PR.S |

FixedReset |

1.32 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 18.39

Evaluated at bid price : 18.39

Bid-YTW : 4.50 % |

| BMO.PR.T |

FixedReset |

1.49 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 18.38

Evaluated at bid price : 18.38

Bid-YTW : 4.28 % |

| MFC.PR.N |

FixedReset |

1.60 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.40

Bid-YTW : 7.61 % |

| MFC.PR.M |

FixedReset |

1.69 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.65

Bid-YTW : 7.49 % |

| FTS.PR.H |

FixedReset |

1.69 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 12.62

Evaluated at bid price : 12.62

Bid-YTW : 4.46 % |

| BNS.PR.D |

FloatingReset |

2.07 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.78

Bid-YTW : 7.74 % |

| PWF.PR.A |

Floater |

2.27 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 11.25

Evaluated at bid price : 11.25

Bid-YTW : 4.24 % |

| TRP.PR.A |

FixedReset |

2.34 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 15.30

Evaluated at bid price : 15.30

Bid-YTW : 4.51 % |

| CIU.PR.C |

FixedReset |

2.65 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 11.25

Evaluated at bid price : 11.25

Bid-YTW : 4.63 % |

| TRP.PR.H |

FloatingReset |

2.67 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 9.60

Evaluated at bid price : 9.60

Bid-YTW : 4.48 % |

| BAM.PR.K |

Floater |

3.08 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 10.05

Evaluated at bid price : 10.05

Bid-YTW : 4.71 % |

| BAM.PR.B |

Floater |

3.17 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 10.09

Evaluated at bid price : 10.09

Bid-YTW : 4.69 % |

| BAM.PF.A |

FixedReset |

3.66 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 19.00

Evaluated at bid price : 19.00

Bid-YTW : 4.93 % |

| BAM.PR.C |

Floater |

3.74 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 9.99

Evaluated at bid price : 9.99

Bid-YTW : 4.74 % |

| TRP.PR.I |

FloatingReset |

12.89 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 11.50

Evaluated at bid price : 11.50

Bid-YTW : 4.29 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| RY.PR.R |

FixedReset |

162,400 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-08-24

Maturity Price : 25.00

Evaluated at bid price : 25.95

Bid-YTW : 4.80 % |

| BNS.PR.Z |

FixedReset |

145,598 |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.10

Bid-YTW : 7.16 % |

| MFC.PR.L |

FixedReset |

110,500 |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.65

Bid-YTW : 8.07 % |

| TD.PF.G |

FixedReset |

68,810 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-04-30

Maturity Price : 25.00

Evaluated at bid price : 25.94

Bid-YTW : 4.94 % |

| RY.PR.Q |

FixedReset |

67,600 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-05-24

Maturity Price : 25.00

Evaluated at bid price : 26.11

Bid-YTW : 4.89 % |

| RY.PR.J |

FixedReset |

59,600 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 19.83

Evaluated at bid price : 19.83

Bid-YTW : 4.43 % |

| There were 34 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| PWF.PR.T |

FixedReset |

Quote: 19.11 – 20.00

Spot Rate : 0.8900

Average : 0.6569

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 19.11

Evaluated at bid price : 19.11

Bid-YTW : 4.31 % |

| ALB.PR.C |

SplitShare |

Quote: 25.91 – 26.44

Spot Rate : 0.5300

Average : 0.3110

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2017-02-28

Maturity Price : 25.67

Evaluated at bid price : 25.91

Bid-YTW : 4.12 % |

| BMO.PR.R |

FloatingReset |

Quote: 21.65 – 22.30

Spot Rate : 0.6500

Average : 0.4322

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.65

Bid-YTW : 4.73 % |

| BAM.PR.E |

Ratchet |

Quote: 13.26 – 14.40

Spot Rate : 1.1400

Average : 0.9285

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 25.00

Evaluated at bid price : 13.26

Bid-YTW : 6.20 % |

| TD.PF.E |

FixedReset |

Quote: 20.40 – 21.12

Spot Rate : 0.7200

Average : 0.5244

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 20.40

Evaluated at bid price : 20.40

Bid-YTW : 4.48 % |

| PWF.PR.P |

FixedReset |

Quote: 12.53 – 12.95

Spot Rate : 0.4200

Average : 0.2799

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-03-29

Maturity Price : 12.53

Evaluated at bid price : 12.53

Bid-YTW : 4.67 % |