The scheduled European hyperinflation has been postponed:

Lower inflation forecasts from the European Commission will put more pressure on the European Central Bank to launch measures to prevent falling prices from destabilizing the weak economic revival.

The EC, the executive arm of the 28-country European Union, predicted on Monday morning that euro zone’s inflation rate will land at 0.8 per cent this year and 1.2 per cent next year. Both figures are well below the ECB’s target rate of close to 2 per cent Less than three months ago, the EC had forecast inflation this year at 1 per cent, and at 1.5 per cent next year. The downward revisions came as more evidence emerged that the euro zone’s deflationary pressures are still fully intact, in spite of rock-bottom interest rates, the end of the euro zone’s recession and slightly lower jobless figures.

So there’s one reason to be bond-bullish. But it takes two to make a market!

Junk-bond investors are accepting yields that are 0.74 percentage point lower than the earnings yield on the Standard & Poor’s 500 index, a measure of profit as a percentage of equity prices.

Historically, debt rated below investment grade has yielded an average 4.2 percentage points more than stocks since March 1995. That relationship has been turned on its head.

Could be a little ‘reaching for yield’ is going on. That always ends in tears.

Meanwhile the feds continue to micro-manage the Canadian economy:

The Conservative government’s bid to ease a multibillion-dollar backlog of Prairie grain is one step closer to becoming law, despite ongoing questions about its details and complaints by Canada’s two major railways.

Bill C-30 was tabled March 26 in an urgent bid to force railways to ship more grain after a bumper crop, and passed third reading in the House of Commons on Monday. That came after a weeks-long delay caused by a complaint over a government error, whereby a committee went too far in altering the bill by adding an amendment the Speaker ruled was out of bounds.

Bill C-30 is aimed at easing a backlog by expanding government power to set minimum shipping levels for railways. It also expands grain sellers’ power to choose a different railway – many had just one choice – and creates a new process for the Canadian Transportation Agency (CTA) to force a railway that fails to hold up its end of a deal to repay certain costs to grain shippers.

I was a little puzzled by the “many had just one choice” part. Apparently:

In most cases, shippers’ grain elevators have nearby access to only one of the two major Canadian railways. And by law, they may not transfer grain to the other railroad unless the elevator is within 30 kilometres of them. Yes, that’s anti-competitive. The bill would raise that limit to 160 km, giving more choice to growers and shippers.

The origins of these regulations on “interswitching” go back to 1904. It’s a relic of the long history of heavy-handed government power over grain and railroads, which included fixed freight rates.

Sounds like a pretty crazy law to me. To at least some extent it’s just another form of protectionism:

“A 160 km interchange limit would open up the southern portion of CNR and CP’s network to competition from U.S. carriers, especially BNSF,” [RBC Capital Markets analyst Walter] Spracklin said in a note to clients.

…

Mr. Spracklin noted that unlike market share shifts between Canadian railways that might also result from the interswitching rule changes, the market share losses to U.S. competitors would be more permanent because there are no reciprocal interchange provisions in the U.S.“Accordingly, cargo losses to U.S. carriers would disappear from the Canadian supply chain altogether weakening all stakeholders’ positions (ports, trucks, etc),” Mr. Spracklin said.

But he said market share losses are not the only issue that might result from the new rules. They also threaten to raise costs for Canadian railways by introducing added complexity to their networks and may require extra infrastructure to be added.

CN said amended interswitching rules would allow U.S. railroads to poach Canadian rail traffic, erode the rate structure and economic viability of Canadian railways and drive traffic to U.S. ports, thus reducing traffic and employment at Canadian ports.

In a March 28 news release, Canadian Pacific Railway said it was disappointed with Ottawa’s decision to introduce legislation that does nothing to improve grain movement but has the potential to cause “great damage” to the Canadian rail transportation system.

“CP … believes that the expansion of regulated interswitching could seriously impact Canada’s competitiveness, as it effectively transfers traffic that normally would move over Canadian railways and ports to U.S. railroads and ports,” it said.

“Interswitching will also lead to double handling of grain shipments, which will slow down the grain supply chain, negatively impacting transit times.”

Federal officials say there are 18 interswitch locations on the Canadian Prairies.

Only 14 primary elevators in Western Canada are affected by interswitching under the current 30 km provisions.

Increasing the interswitch distance to 160 km would give 150 elevators potential access to service by more than one railway, including U.S. railways.

I’m prepared to listen, but it seems to me that in situations in which ‘natural monopoly’ conditions exist – such as railways, telecommunications and pipelines – interswitching should be mandatory, but at premium rates (so that, for instance, somebody who built a network and rented it out in toto could make a very good profit on the deal).

Of course, such mandatory carriage has its detractors:

While economic theory suggests that more competition always benefits the consumer, that may not be true in Canada’s telecom industry, where concentration in the hands of BCE, Rogers and Telus is good for customers, argue authors Martin Masse and Paul Beaudry in a 60-page report released Tuesday.

“It may be preferable for financial resources … to be concentrated in the hands of a few strong players willing to invest in new technologies and services rather than scattered among several small and feeble competitors trying to survive by selling at prices barely above marginal costs,” the report said.

…

The government, it added, has “lost sight of the ultimate goal of promoting the development of a dynamic, efficient industry.”For example, Ottawa should drop all remaining foreign ownership restrictions, including in broadcasting, as well as allow the transfer of existing wireless spectrum licenses, the authors said. Even the threat that a major foreign player entering Canada would lead to better service, Mr. Masse said.

The government should also “gradually abandon” so-called mandatory access policies, which allow new entrants to piggy-back on the networks of established players at favourable rates.

I’m all in favour of dropping all remaining foreign ownership restrictions!

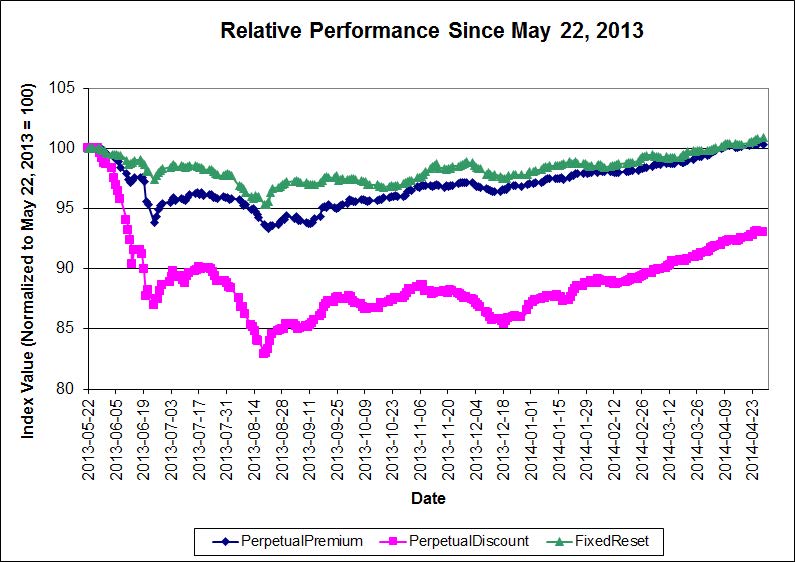

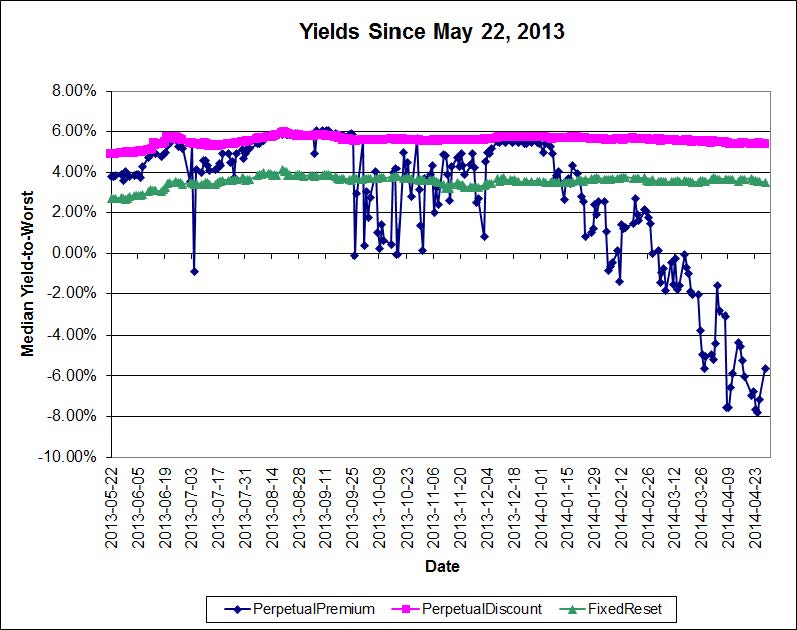

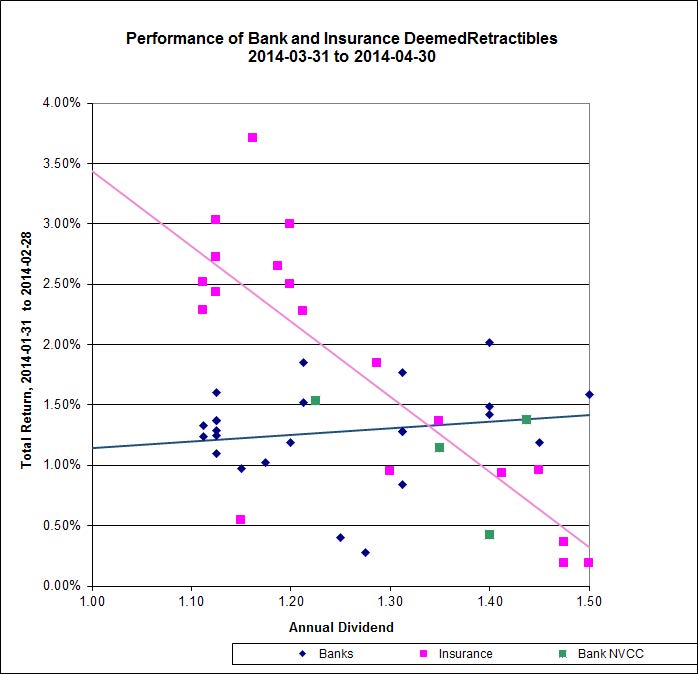

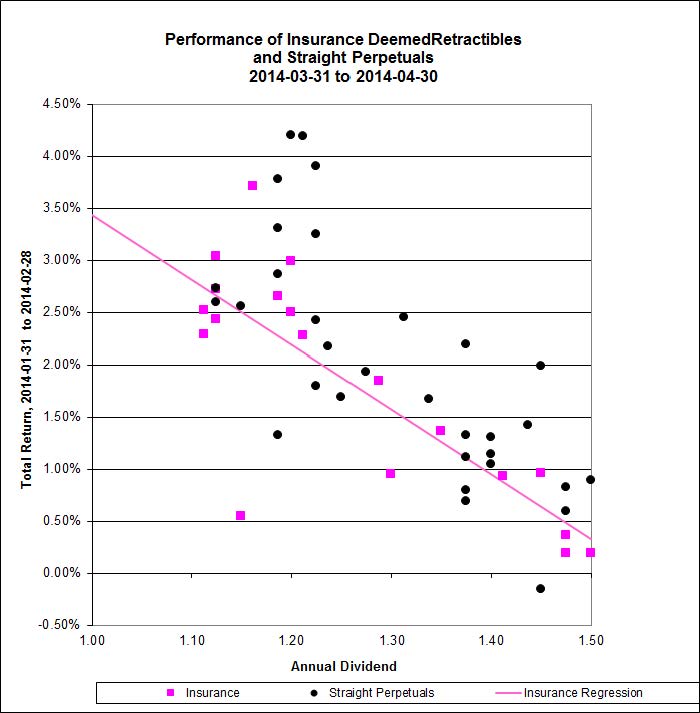

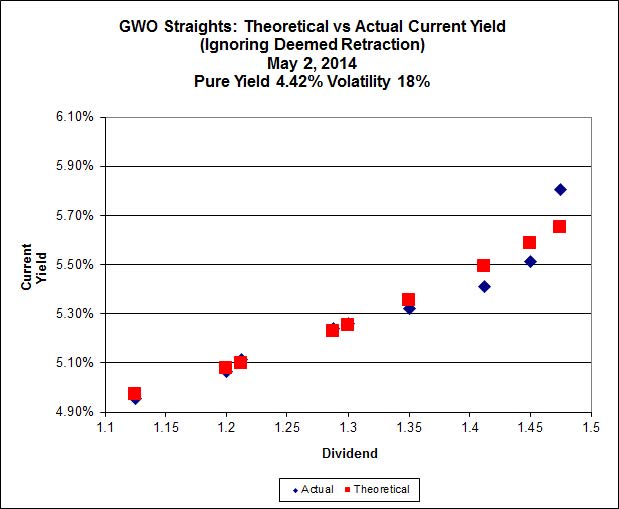

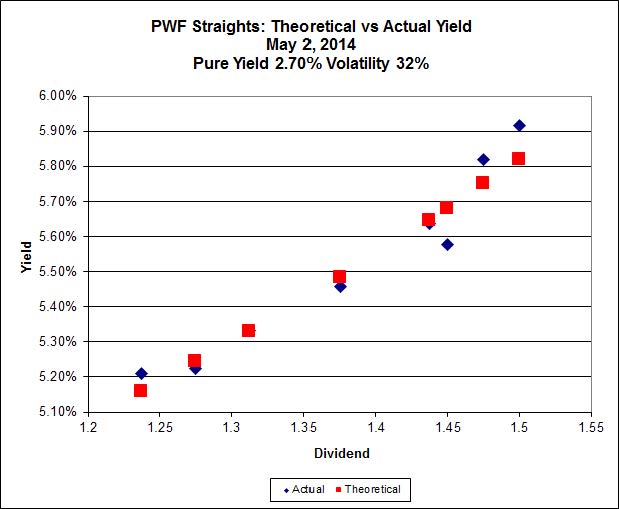

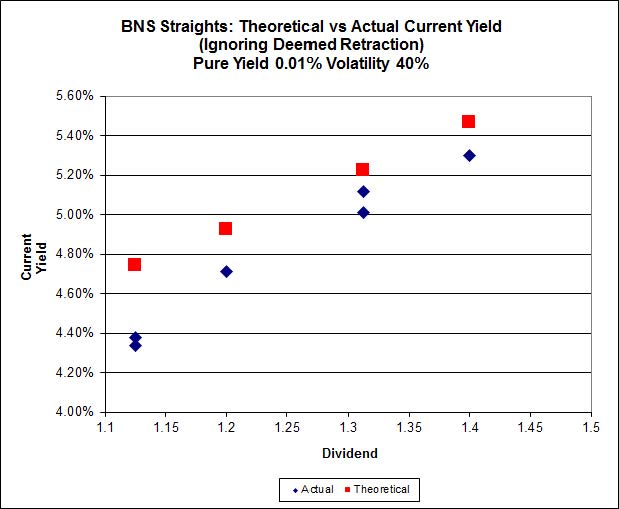

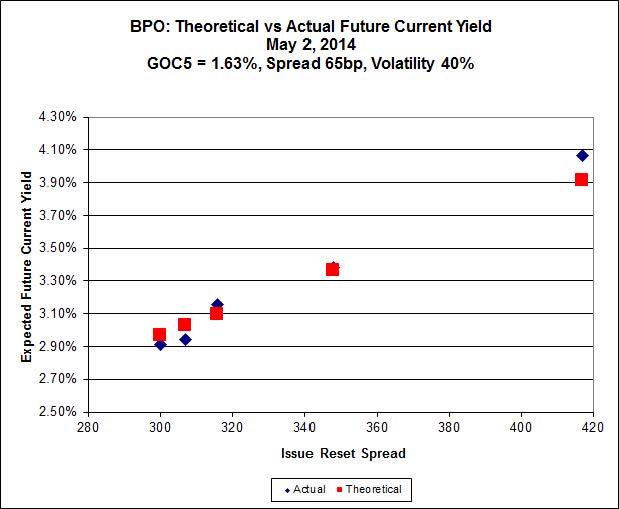

It was another (slightly!) positive day for the Canadian preferred share market, with PerpetualDiscounts gaining 2bp, FixedResets winning 11bp and DeemedRetractibles up 3bp. The Performance Highlights table is lengthy again, with a few losses indicating that some of the recent gains are considered to be out of whack; FixedResets dominated the winners. Volume was quite high.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2449 % | 2,416.1 |

| FixedFloater | 4.59 % | 3.82 % | 30,666 | 17.81 | 1 | 0.7299 % | 3,741.3 |

| Floater | 3.02 % | 3.17 % | 53,500 | 19.28 | 4 | 0.2449 % | 2,608.7 |

| OpRet | 4.34 % | -2.09 % | 33,697 | 0.15 | 2 | 0.0580 % | 2,703.6 |

| SplitShare | 4.79 % | 4.38 % | 62,701 | 4.18 | 5 | -0.0158 % | 3,096.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0580 % | 2,472.2 |

| Perpetual-Premium | 5.51 % | -9.60 % | 97,017 | 0.09 | 15 | 0.0914 % | 2,401.0 |

| Perpetual-Discount | 5.29 % | 5.34 % | 119,890 | 14.93 | 21 | 0.0222 % | 2,542.0 |

| FixedReset | 4.50 % | 3.32 % | 210,334 | 4.14 | 75 | 0.1130 % | 2,570.0 |

| Deemed-Retractible | 4.97 % | -5.69 % | 138,328 | 0.14 | 42 | 0.0293 % | 2,528.5 |

| FloatingReset | 2.67 % | 2.30 % | 135,928 | 4.21 | 6 | 0.0066 % | 2,497.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.A | FixedReset | -1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-06 Maturity Price : 23.33 Evaluated at bid price : 24.01 Bid-YTW : 3.72 % |

| PWF.PR.P | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-06 Maturity Price : 23.98 Evaluated at bid price : 24.31 Bid-YTW : 3.43 % |

| FTS.PR.F | Perpetual-Discount | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-06 Maturity Price : 24.01 Evaluated at bid price : 24.31 Bid-YTW : 5.11 % |

| CU.PR.E | Perpetual-Discount | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-06 Maturity Price : 24.40 Evaluated at bid price : 24.81 Bid-YTW : 5.00 % |

| BAM.PR.Z | FixedReset | 1.45 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-12-31 Maturity Price : 25.00 Evaluated at bid price : 26.64 Bid-YTW : 3.04 % |

| GWO.PR.N | FixedReset | 1.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.59 Bid-YTW : 3.75 % |

| SLF.PR.G | FixedReset | 1.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.71 Bid-YTW : 3.84 % |

| BAM.PR.X | FixedReset | 1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-06 Maturity Price : 22.04 Evaluated at bid price : 22.42 Bid-YTW : 4.06 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| SLF.PR.F | FixedReset | 450,280 | TD crossed two blocks of 225,000 each, both at 25.34. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-06-30 Maturity Price : 25.00 Evaluated at bid price : 25.33 Bid-YTW : 1.04 % |

| BNS.PR.P | FixedReset | 118,819 | RBC crossed 113,700 at 25.50. YTW SCENARIO Maturity Type : Call Maturity Date : 2018-04-25 Maturity Price : 25.00 Evaluated at bid price : 25.50 Bid-YTW : 2.84 % |

| MFC.PR.A | OpRet | 111,793 | RBC crossed 107,200 at 25.90. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-06-19 Maturity Price : 25.25 Evaluated at bid price : 25.80 Bid-YTW : -9.22 % |

| BNS.PR.Z | FixedReset | 100,461 | Scotia bought 20,100 from RBC at 24.75 and crossed 10,800 at 24.80. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.76 Bid-YTW : 3.32 % |

| MFC.PR.D | FixedReset | 91,954 | RBC crossed 78,000 at 25.40. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-06-19 Maturity Price : 25.00 Evaluated at bid price : 25.41 Bid-YTW : 0.18 % |

| ENB.PR.B | FixedReset | 62,798 | TD crossed 50,000 at 25.32. YTW SCENARIO Maturity Type : Call Maturity Date : 2017-06-01 Maturity Price : 25.00 Evaluated at bid price : 25.32 Bid-YTW : 3.82 % |

| There were 50 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.I | FixedReset | Quote: 26.31 – 26.75 Spot Rate : 0.4400 Average : 0.2482 YTW SCENARIO |

| PWF.PR.G | Perpetual-Premium | Quote: 25.50 – 25.94 Spot Rate : 0.4400 Average : 0.2529 YTW SCENARIO |

| MFC.PR.J | FixedReset | Quote: 25.98 – 26.43 Spot Rate : 0.4500 Average : 0.2844 YTW SCENARIO |

| IFC.PR.C | FixedReset | Quote: 26.06 – 26.43 Spot Rate : 0.3700 Average : 0.2419 YTW SCENARIO |

| TD.PR.Q | Deemed-Retractible | Quote: 26.50 – 26.84 Spot Rate : 0.3400 Average : 0.2316 YTW SCENARIO |

| RY.PR.A | Deemed-Retractible | Quote: 25.75 – 26.03 Spot Rate : 0.2800 Average : 0.1874 YTW SCENARIO |