In the wake of the August jobs number fiasco, it has been suggested that timeliness of delivery of other data should be improved:

It should be noted that the United States doesn’t rely on a household survey to estimate its monthly job numbers. Oh, it conducts one, as a secondary measure; but its primary labour market numbers come from payroll data gathered from employers and government agencies. As such, they are a more accurate measure of actual payroll employment – they reflect things like paycheques issued and taxes paid.

Actually, Statscan does this, too – it’s called the Survey of Employment, Payrolls and Hours (SEPH), and it, too, is published monthly. It relies even more heavily on government payroll-deduction data than the U.S. report, and is considered a highly reliable measure of the labour market.

Notably, the SEPH has diverged considerably from the LFS in recent months. For the first five months of this year, the SEPH shows that employment rose by just 33,600 jobs, or an average of 6,700 a month. But according to the LFS, employment, the gains were almost double that – 62,200, or an average 12,400 a month.

The SEPH’s big drawback is its lack of timeliness. SEPH data lag behind the LFS release by nearly two months; Statscan won’t publish the SEPH for June until Aug. 28. Markets don’t want to wait that long for such a key measure of economic health.

David Watt, chief economist at HSBC Bank Canada, suggests that Statscan should deliver the SEPH at the same time as the LFS, as the U.S. does in its employment report.

The CMHC is crossing its fingers for a soft landing for housing prices:

According to CMHC’s third quarter 2014 Housing Market Outlook, Canada Edition1, housing activity will continue to be supported by economic and demographic fundamentals for the rest of 2014 and into 2015.

…

Multiple Listing Service® (MLS®2) sales are expected to range between 450,800 and 482,700 units in 2014, with a point forecast of 463,600 units. In 2015, sales are expected to range from 455,800 to 502,900 units, with an increase in the point forecast to 474,300 units.The average MLS® price is forecast to be between $394,700 and $405,700 in 2014 and between $396,500 and $416,900 in 2015. CMHC’s point forecast for the average MLS® price calls for a 4.5 per cent gain to $399,800 in 2014 and a further 1.8 per cent gain to $406,800 in 2015.

And, surprisingly, bank holdings of insured mortgages are declining:

Canada’s largest banks, as a whole, have seen almost no growth in their insured mortgage portfolios recently, Macquarie Capital Markets analyst Asim Imran discovered.

He found this out by digging through some data that the banking regulator – the Office of the Superintendent of Financial Institutions – gathers.

The growth that banks have shown in their mortgage portfolios of late has come from a strong uptick in uninsured mortgages, he concluded. Chartered banks saw uninsured mortgages rise 13.5 per cent year over year in May (for the Big Six banks it was 12 per cent). Insured mortgages, in contrast, were down 0.8 per cent month over month, and up just 0.1 per cent year over year.

Economic sanctions against naughty countries are having their intended effect:

Deutsche Bank AG plans to hire about 500 compliance, risk and technology employees in the U.S. by year-end, Jacques Brand, its North American chief executive, said in an interview last month. The bank is under investigation for potential violations of U.S. sanctions.

The hiring spree for compliance executives who understand U.S. sanctions laws comes in part from the trend toward appointing outside monitors as a condition of some settlements.

…

“Having someone who has come directly from those regulatory bodies or otherwise understands the evolving rules and regulations gives firms a significant advantage,” said Justin Mandel, co-founder of JW Michaels & Co., a New York-based recruitment firm that places compliance staff at banks and asset managers. “OFAC is one of those areas where it’s relevant.”That’s led banks to pay up for top talent. Compensation is often the main reason many leave government jobs.

…

Recent Treasury job openings on the federal government’s employment website, www.usajobs.gov, have included an OFAC sanctions compliance officer whose salary range is listed as $63,091 to $116,901 a year, according to the website.At a bank, someone with a similar level of experience as the compliance officer may receive a $170,000 salary, said Stuart Rosenthal, who’s based in Montclair, New Jersey, and runs a recruiting firm focused on placing compliance and regulatory staff.

It was a good day for the Canadian preferred share market, with PerpetualDiscounts gaining 11bp, FixedResets winning 16bp and DeemedRetractibles up 13bp. Volatility was minimal. Volume was below average.

PerpetualDiscounts now yield 5.18%, equivalent to 6.73% interest at the standard conversion factor of 1.3x. Long corporates now yield about 4.2%, so the pre-tax interest-equivalent spread is now about 255bp, unchanged from August 6.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0691 % | 2,643.6 |

| FixedFloater | 4.17 % | 3.41 % | 27,211 | 18.58 | 1 | 0.0000 % | 4,156.5 |

| Floater | 2.90 % | 3.02 % | 45,089 | 19.65 | 4 | 0.0691 % | 2,733.7 |

| OpRet | 4.02 % | -1.02 % | 76,753 | 0.08 | 1 | 0.1570 % | 2,721.1 |

| SplitShare | 4.23 % | 3.82 % | 67,624 | 3.96 | 6 | 0.0794 % | 3,135.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1570 % | 2,488.2 |

| Perpetual-Premium | 5.49 % | -4.14 % | 82,054 | 0.08 | 19 | 0.0855 % | 2,436.6 |

| Perpetual-Discount | 5.22 % | 5.18 % | 113,893 | 15.17 | 17 | 0.1114 % | 2,599.6 |

| FixedReset | 4.29 % | 3.57 % | 197,477 | 8.53 | 75 | 0.1643 % | 2,564.3 |

| Deemed-Retractible | 4.98 % | -1.02 % | 107,799 | 0.12 | 42 | 0.1260 % | 2,560.6 |

| FloatingReset | 2.65 % | 2.07 % | 80,236 | 3.83 | 6 | -0.1574 % | 2,520.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TD.PR.P | Deemed-Retractible | 1.27 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2014-09-12 Maturity Price : 25.75 Evaluated at bid price : 26.23 Bid-YTW : -14.64 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| PWF.PR.A | Floater | 304,335 | Desjardins crossed three blocks; 100,000 shares, 42,600 and 50,000, all at 20.10. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-08-13 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 2.62 % |

| BMO.PR.W | FixedReset | 215,710 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-08-13 Maturity Price : 23.14 Evaluated at bid price : 25.00 Bid-YTW : 3.57 % |

| RY.PR.H | FixedReset | 116,375 | Nesbitt crossed 100,000 at 25.35. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-08-13 Maturity Price : 23.26 Evaluated at bid price : 25.32 Bid-YTW : 3.55 % |

| ENB.PF.C | FixedReset | 88,262 | RBC crossed 30,000 at 24.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-08-13 Maturity Price : 23.09 Evaluated at bid price : 24.89 Bid-YTW : 4.06 % |

| TD.PF.B | FixedReset | 74,553 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-08-13 Maturity Price : 23.17 Evaluated at bid price : 25.03 Bid-YTW : 3.60 % |

| PWF.PR.L | Perpetual-Discount | 68,846 | TD crossed 65,000 at 24.89. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-08-13 Maturity Price : 24.54 Evaluated at bid price : 24.85 Bid-YTW : 5.16 % |

| There were 26 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| CIU.PR.C | FixedReset | Quote: 21.25 – 22.19 Spot Rate : 0.9400 Average : 0.7298 YTW SCENARIO |

| PVS.PR.C | SplitShare | Quote: 26.16 – 27.00 Spot Rate : 0.8400 Average : 0.6410 YTW SCENARIO |

| TD.PR.Z | FloatingReset | Quote: 25.18 – 25.48 Spot Rate : 0.3000 Average : 0.2086 YTW SCENARIO |

| CU.PR.C | FixedReset | Quote: 25.70 – 25.99 Spot Rate : 0.2900 Average : 0.2015 YTW SCENARIO |

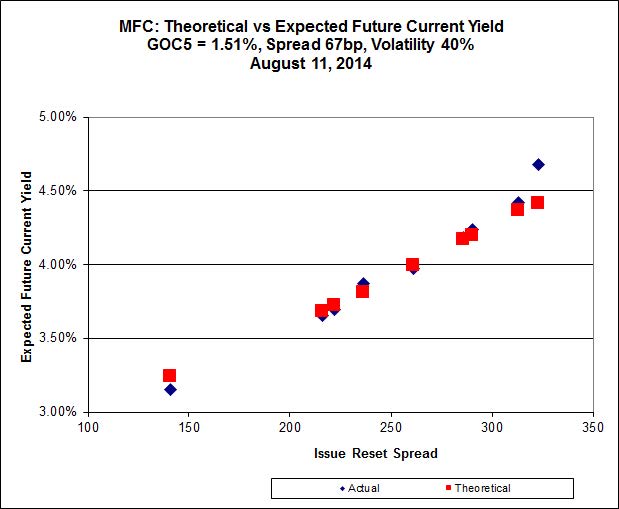

| MFC.PR.L | FixedReset | Quote: 24.91 – 25.15 Spot Rate : 0.2400 Average : 0.1639 YTW SCENARIO |

| RY.PR.L | FixedReset | Quote: 26.56 – 26.84 Spot Rate : 0.2800 Average : 0.2142 YTW SCENARIO |