Manulife Financial Corporation has announced (emphasis added):

the applicable dividend rates for its Non-cumulative Rate Reset Class 1 Shares Series 11 (the “Series 11 Preferred Shares”) (TSX: MFC.PR.J) and Non-cumulative Floating Rate Class 1 Shares Series 12 (the “Series 12 Preferred Shares”).

With respect to any Series 11 Preferred Shares that remain outstanding after March 19, 2018, holders thereof will be entitled to receive fixed rate non-cumulative preferential cash dividends on a quarterly basis, as and when declared by the Board of Directors of Manulife and subject to the provisions of the Insurance Companies Act (Canada). The dividend rate for the five-year period commencing on March 20, 2018, and ending on March 19, 2023, will be 4.73100% per annum or $0.295688 per share per quarter, being equal to the sum of the five-year Government of Canada bond yield as at February 20, 2018, plus 2.61%, as determined in accordance with the terms of the Series 11 Preferred Shares.

With respect to any Series 11 Preferred Shares that may be issued on March 19, 2018 in connection with the conversion of the Series 11 Preferred Shares into the Series 12 Preferred Shares, holders thereof will be entitled to receive floating rate non-cumulative preferential cash dividends on a quarterly basis, calculated on the basis of actual number of days elapsed in each quarterly floating rate period divided by 365, as and when declared by the Board of Directors of Manulife and subject to the provisions of the Insurance Companies Act (Canada). The dividend rate for the three-month period commencing on March 20, 2018, and ending on June 19, 2018, will be 0.96209% (3.81700% on an annualized basis) or $0.240523 per share, being equal to the sum of the three-month Government of Canada Treasury bill yield as at February 20, 2018, plus 2.61%, as determined in accordance with the terms of the Series 12 Preferred Shares.

Beneficial owners of Series 11 Preferred Shares who wish to exercise their right of conversion should instruct their broker or other nominee to exercise such right before 5:00 p.m. (Toronto time) on March 5, 2018. The news release announcing such conversion right was issued on February 12, 2018 and can be viewed on SEDAR or Manulife’s website. Conversion inquiries should be directed to Manulife’s Registrar and Transfer Agent, AST Trust Company (Canada), at 1‑800-783-9495.

The Toronto Stock Exchange (“TSX”) has conditionally approved the listing of the Series 12 Preferred Shares effective upon conversion. Listing of the Series 12 Preferred Shares is subject to Manulife fulfilling all the listing requirements of the TSX and, upon approval, the Series 12 Preferred Shares will be listed on the TSX under the trading symbol “MFC.PR.S”.

MFC.PR.J is a FixedReset, 4.00%+261, that commenced trading 2012-12-4 after being announced 2012-11-27. It is tracked by HIMIPref™ and is assigned to the FixedReset sub-index.

As this issue is not NVCC compliant and it is an insurance issue, it is analyzed as having a Deemed Retraction, effective 2025-1-31 (this date may change in the future).

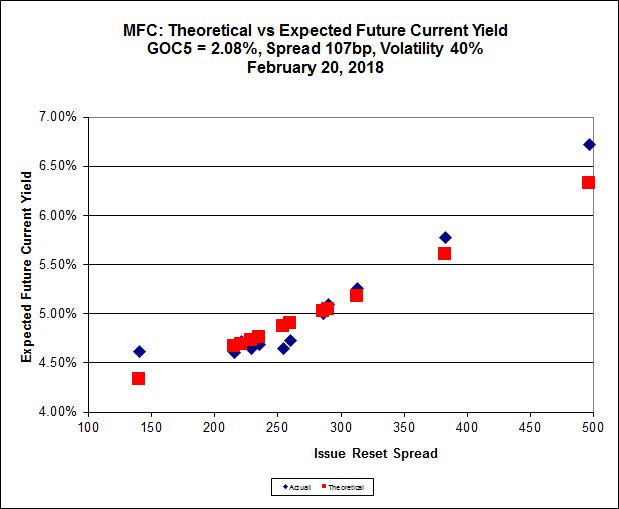

The most logical way to analyze the question of whether or not to convert is through the theory of Preferred Pairs, for which a calculator is available. Briefly, a Strong Pair is defined as a pair of securities that can be interconverted in the future (e.g., MFC.PR.J and the FloatingReset MFC.PR.S that will exist if enough holders convert). Since they will be interconvertible on this future date, it may be assumed that they will be priced identically on this date (if they aren’t then holders will simply convert en masse to the higher-priced issue). And since they will be priced identically on a given date in the future, any current difference in price must be offset by expectations of an equal and opposite value of dividends to be received in the interim. And since the dividend rate on one element of the pair is both fixed and known, the implied average rate of the other, floating rate, instrument can be determined. Finally, we say, we may compare these average rates and take a view regarding the actual future course of that rate relative to the implied rate, which will provide us with guidance on which element of the pair is likely to outperform the other until the next interconversion date, at which time the process will be repeated.

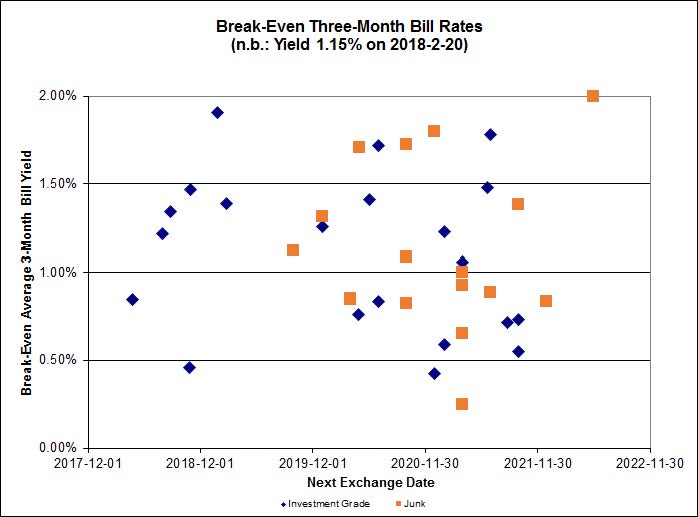

We can show the break-even rates for each FixedReset / FloatingReset Strong Pair graphically by plotting the implied average 3-month bill rate against the next Exchange Date (which is the date to which the average will be calculated).

Click for Big

Click for BigThe market appears to be relatively uninterested in floating rate product; most of the implied rates until the next interconversion are scattered around the current 3-month bill rate and the averages for investment-grade and junk issues are slightly below current market rates, at +1.23% and +0.93%, respectively – although these break-even rates are much closer to the market rate than has been case for recent resets! Whatever might be the result of the next few Bank of Canada overnight rate decisions, I suggest that it is unlikely that the average rate over the next five years will be lower than current – but if you disagree, of course, you may interpret the data any way you like.

Since credit quality of each element of the pair is equal to the other element, it should not make any difference whether the pair examined is investment-grade or junk, although we might expect greater variation of implied rates between junk issues on grounds of lower liquidity, and this is just what we see.

If we plug in the current bid price of the MFC.PR.J FixedReset, we may construct the following table showing consistent prices for its soon-may-be-issued FloatingReset counterpart, MFC.PR.S, given a variety of Implied Breakeven yields consistent with issues currently trading:

| Estimate of FloatingReset MFC.PR.S (received in exchange for MFC.PR.J) Trading Price In Current Conditions |

| |

Assumed FloatingReset

Price if Implied Bill

is equal to |

| FixedReset |

Bid Price |

Spread |

1.75% |

1.25% |

0.75% |

| MFC.PR.J |

24.80 |

261bp |

24.42 |

23.91 |

23.40 |

Based on current market conditions, I suggest that the FloatingResets that will result from conversion are likely to be cheap and trading below the price of their FixedReset counterparts. Therefore, it seems likely that I will recommend that holders of MFC.PR.J continue to hold the issue and not to convert, but I will wait until it’s closer to the March 5, 2018 notification deadline before making a final pronouncement. I will note that once the FloatingResets commence trading (if, in fact, they do) it may be a good trade to swap the FixedReset for the FloatingReset in the market once both elements of each pair are trading and you can – presumably, according to this analysis – do it with a reasonably good take-out in price, rather than doing it through the company on a 1:1 basis. But that, of course, will depend on the prices at that time and your forecast for the path of policy rates over the next five years. There are no guarantees – my recommendation is based on the assumption that current market conditions with respect to the pairs will continue until the FloatingResets commence trading and that the relative pricing of the two new pairs will reflect these conditions.