Scotia came out with a Tier 1 Bond last week:

Bank of Nova Scotia saw strong investor demand on Wednesday for an Additional Tier 1 bond, the first offshore deal of its kind out of Canada, which could pave the way for similar deals. The US$1.25bn perpetual non-call five issue, which has a fixed coupon for the initial five years and then switches to floating, saw almost US$8bn of demand at the peak of interest.

With the level of interest so strong – there were roughly 400 line items in early marketing – bookrunners Bank of America Merrill Lynch, Citigroup, Scotia and UBS were able to pull in pricing sharply from IPTs of 5% area to 4.65%.

That looked to be attractive pricing for the borrower, who is looking to diversify its funding outside of Canada.

…

“The deal has a dividend stopper and the concept of MDA doesn’t exist in Canada.”

Dividend stopper language prevents banks from paying equity dividends if they have not paid AT1 coupons, and is prohibited in European AT1 bonds.

Maximum Distributable Amounts (MDA) is also a European concept and is effectively a firm’s distributable profit. If it is too low, banks can be barred from paying AT1 coupons.

“Some European AT1s turn the capital structure upside down,” David Knutson, head of Americas credit research at Schroders, told IFR.

“They are essentially sub equity. In principle, you shouldn’t be able to pay equity if you can’t pay bondholders.”

This may cut into the supply of preferred shares:

The notes were crafted in such a way that the money raised qualifies as additional tier 1 (AT1) capital, which is part of a cash reserve that Canada’s top banking regulator expects banks to hold to maintain a minimum level of financial stability.

The Canadian banks have primarily raised this type of capital by issuing preferred shares into the domestic market, which is heavily dependent on retail demand. But preferred shares have been a tough sell for banks to export beyond Canada because Canada Revenue Agency puts a tax of 25 per cent on any passive income generated by investors who are not residents of Canada.

…

BMO Nesbitt Burns Inc. analyst Kris Somers called Scotiabank’s note a “gamechanger,” adding in a report that the new structure has the potential to result in reduced supply of preferred shares sold by financials.

This type of offering is being billed as a solution to a problem that Canada’s largest financial institutions have been wrestling with for years: The country’s market for preferred shares has become a less reliable and more costly way of sourcing AT1 capital.

There’s no mention of the issue on Scotia’s website that I can see, but the prospectus is on EDGAR – and I can link to it directly because it was subject to the rules of a first-world regulator!

Interest Rate

From and including the Issue Date to, but excluding, October 12, 2022 (the “Fixed Rate Period”), interest will accrue on the Notes at an initial rate equal to 4.650% per annum. From and including October 12, 2022 (the “Floating Rate Period”), interest will accrue on the Notes at a rate per annum equal to three-month LIBOR (as defined herein) plus 2.648% and will reset quarterly.

…

Optional Redemption

The Bank may, at its option, with the prior written approval of the Superintendent of Financial Institutions (Canada) (the “Superintendent”), redeem the Notes, in whole or in part, on any Interest Payment Date on or after October 12, 2022, at a redemption price equal to 100% of the principal amount thereof, plus any accrued and unpaid interest up to, but excluding, the date of redemption (except to the extent such unpaid interest was cancelled).

The Bank may, at its option, with the prior written approval of the Superintendent, redeem the Notes, in whole but not in part, at any time within 90 days following a Regulatory Event Date (as defined herein), at a redemption price equal to 100% of the principal amount thereof, plus any accrued and unpaid interest up to, but excluding, the date of redemption (except to the extent such unpaid interest was cancelled).

Additionally, the Bank may, at its option, with the prior written approval of the Superintendent, redeem the Notes, in whole but not in part, on any date following the occurrence of a Tax Event (as defined herein), at a redemption price equal to 100% of the principal amount thereof, plus any accrued and unpaid interest up to, but excluding, the date of redemption (except to the extent such unpaid interest was cancelled).

…

Upon the occurrence of a Trigger Event (as defined below), each outstanding Note will automatically and immediately be converted, on a full and permanent basis, without the consent of the holders thereof, into that number of Common Shares determined by dividing (a) the product of the Multiplier and the Note Value, by (b) the Conversion Price (an “NVCC Automatic Conversion”). See “Description of the Notes—NVCC Automatic Conversion.”

“Conversion Price” means, in respect of each Note, the greater of (i) the Floor Price and (ii) the Current Market Price.

“Current Market Price” means the volume weighted average trading price of the Common Shares on the TSX or, if not then listed on the TSX, on another exchange or market chosen by the board of directors of the Bank on which the Common Shares are then traded, for the 10 consecutive trading days ending on the trading day immediately prior to the date on which the Trigger Event occurs (with the conversion occurring as of the start of business on the date on which the Trigger Event occurs), converted (if not denominated in U.S. dollars) into U.S. dollars at the Prevailing Rate on the day immediately prior to the date on which the Trigger Event occurs. If no such trading prices are available, Current Market Price shall be the Floor Price.

“Floor Price” means the U.S. dollar equivalent of CAD$5.00 converted into U.S. dollars at the Prevailing Rate on the day immediately prior to the date on which the Trigger Event occurs, subject to adjustment in the event of (i) the issuance of Common Shares or securities exchangeable for or convertible into Common Shares to all holders of Common Shares as a stock dividend, (ii) the subdivision, redivision or change of the Common Shares into a greater number of Common Shares, or (iii) the reduction, combination or consolidation of the Common Shares into a lesser number of Common Shares. The adjustment shall be calculated to the nearest one-tenth of one cent provided that no adjustment of the Floor Price shall be required unless such adjustment would require an increase or decrease of at least 1% of the Floor Price then in effect; provided, however, that in such case any adjustment that would otherwise be required to be made will be carried forward and will be made at the time of and together with the next subsequent adjustment which, together with any adjustments so carried forward, will amount to at least 1% of the Floor Price.

“Multiplier” means 1.25.

Note that the multiplier for sub-debt is 1.5 and the multiplier for preferred shares is 1.0. So preferred shares are effectively junior to this debt.

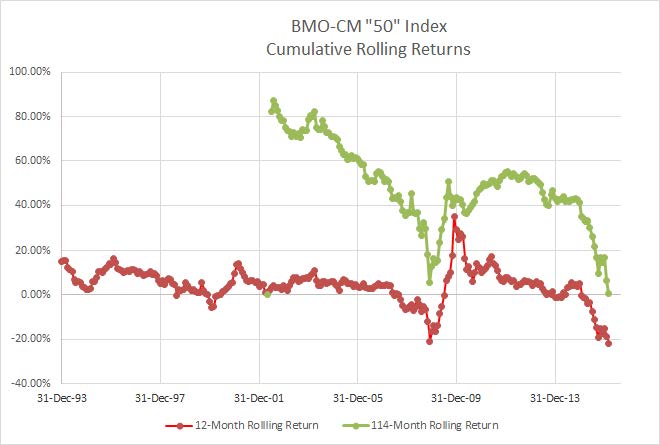

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.3550 % |

2,421.6 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.3550 % |

4,443.6 |

| Floater |

3.77 % |

3.93 % |

27,932 |

17.60 |

4 |

0.3550 % |

2,560.9 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0659 % |

3,074.4 |

| SplitShare |

4.74 % |

4.75 % |

76,674 |

4.39 |

6 |

0.0659 % |

3,671.5 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0659 % |

2,864.6 |

| Perpetual-Premium |

5.37 % |

4.66 % |

62,940 |

2.34 |

17 |

0.1693 % |

2,815.2 |

| Perpetual-Discount |

5.36 % |

5.32 % |

63,300 |

14.93 |

19 |

0.1676 % |

2,940.5 |

| FixedReset |

4.26 % |

4.32 % |

151,943 |

6.10 |

99 |

0.1538 % |

2,465.1 |

| Deemed-Retractible |

5.09 % |

5.56 % |

100,808 |

6.02 |

30 |

0.1860 % |

2,891.5 |

| FloatingReset |

2.77 % |

2.80 % |

50,419 |

4.07 |

8 |

0.4206 % |

2,673.4 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| TRP.PR.B |

FixedReset |

-1.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-10-10

Maturity Price : 15.84

Evaluated at bid price : 15.84

Bid-YTW : 4.63 % |

| MFC.PR.G |

FixedReset |

1.04 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.25

Bid-YTW : 4.75 % |

| SLF.PR.G |

FixedReset |

1.06 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.09

Bid-YTW : 7.89 % |

| TRP.PR.A |

FixedReset |

1.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-10-10

Maturity Price : 20.14

Evaluated at bid price : 20.14

Bid-YTW : 4.53 % |

| BMO.PR.Z |

Perpetual-Premium |

1.19 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2024-08-25

Maturity Price : 25.00

Evaluated at bid price : 25.60

Bid-YTW : 4.72 % |

| MFC.PR.N |

FixedReset |

1.27 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.05

Bid-YTW : 5.33 % |

| CM.PR.O |

FixedReset |

1.30 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-10-10

Maturity Price : 23.03

Evaluated at bid price : 23.40

Bid-YTW : 4.32 % |

| MFC.PR.M |

FixedReset |

1.30 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.30

Bid-YTW : 5.25 % |

| SLF.PR.J |

FloatingReset |

1.33 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.58

Bid-YTW : 7.73 % |

| BAM.PR.X |

FixedReset |

1.79 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-10-10

Maturity Price : 17.60

Evaluated at bid price : 17.60

Bid-YTW : 4.79 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| TRP.PR.K |

FixedReset |

162,355 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2022-05-31

Maturity Price : 25.00

Evaluated at bid price : 25.98

Bid-YTW : 4.12 % |

| MFC.PR.O |

FixedReset |

102,942 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-06-19

Maturity Price : 25.00

Evaluated at bid price : 26.73

Bid-YTW : 3.70 % |

| GWO.PR.T |

Deemed-Retractible |

83,200 |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.35

Bid-YTW : 5.65 % |

| GWO.PR.P |

Deemed-Retractible |

80,013 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-03-31

Maturity Price : 25.00

Evaluated at bid price : 25.33

Bid-YTW : 5.07 % |

| GWO.PR.S |

Deemed-Retractible |

72,076 |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 25.03

Bid-YTW : 5.29 % |

| BMO.PR.B |

FixedReset |

69,313 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2022-02-25

Maturity Price : 25.00

Evaluated at bid price : 26.27

Bid-YTW : 3.75 % |

| There were 31 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| RY.PR.D |

Deemed-Retractible |

Quote: 25.42 – 26.00

Spot Rate : 0.5800

Average : 0.3395

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2017-11-09

Maturity Price : 25.00

Evaluated at bid price : 25.42

Bid-YTW : -8.60 % |

| CCS.PR.C |

Deemed-Retractible |

Quote: 23.60 – 24.25

Spot Rate : 0.6500

Average : 0.4331

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.60

Bid-YTW : 6.02 % |

| RY.PR.J |

FixedReset |

Quote: 24.61 – 25.00

Spot Rate : 0.3900

Average : 0.2624

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-10-10

Maturity Price : 23.30

Evaluated at bid price : 24.61

Bid-YTW : 4.41 % |

| TRP.PR.B |

FixedReset |

Quote: 15.84 – 16.38

Spot Rate : 0.5400

Average : 0.4186

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-10-10

Maturity Price : 15.84

Evaluated at bid price : 15.84

Bid-YTW : 4.63 % |

| ELF.PR.H |

Perpetual-Premium |

Quote: 24.80 – 25.10

Spot Rate : 0.3000

Average : 0.2092

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-10-10

Maturity Price : 24.47

Evaluated at bid price : 24.80

Bid-YTW : 5.56 % |

| BMO.PR.T |

FixedReset |

Quote: 23.16 – 23.50

Spot Rate : 0.3400

Average : 0.2589

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-10-10

Maturity Price : 22.80

Evaluated at bid price : 23.16

Bid-YTW : 4.34 % |