Today’s big news is the FOMC policy rate decision:

The Committee expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market conditions will strengthen somewhat further. Inflation is expected to remain low in the near term, in part because of earlier declines in energy prices, but to rise to 2 percent over the medium term as the transitory effects of past declines in energy and import prices dissipate and the labor market strengthens further. Near-term risks to the economic outlook appear roughly balanced. The Committee continues to closely monitor inflation indicators and global economic and financial developments.

Against this backdrop, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent. The Committee judges that the case for an increase in the federal funds rate has strengthened but decided, for the time being, to wait for further evidence of continued progress toward its objectives. The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation.

…

Voting against the action were: Esther L. George, Loretta J. Mester, and Eric Rosengren, each of whom preferred at this meeting to raise the target range for the federal funds rate to 1/2 to 3/4 percent.

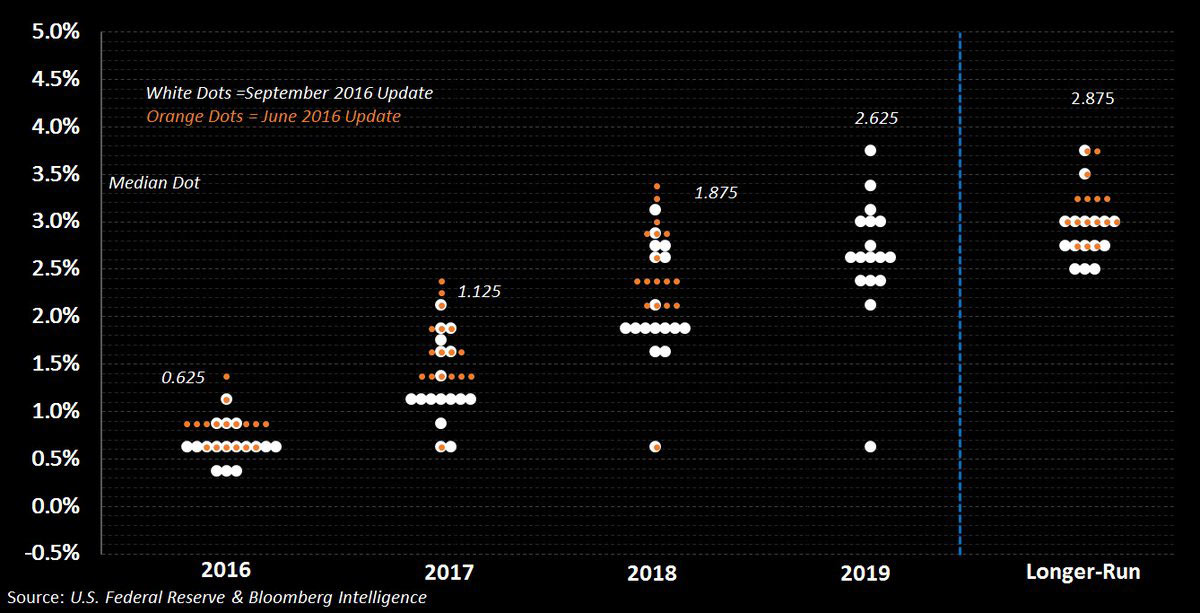

Projections for the future course of rates eased slightly but remained skewed upwards:

The central bank’s so-called “dot plot”, which it uses to signal its outlook for the path of interest rates, showed that officials expected one quarter-point rate increase this year. Three policy makers projected that keeping rates unchanged this year would be most appropriate. Officials scaled back expectations for hikes in 2017 and over the longer run.

Policy makers see two rate hikes next year, down from their June median projection of three.

Click for Big

Click for BigIt’s interesting to see more argument that technology, not globalization, is the bug-bear of the middle class:

In the realm of international trade, it is a truism seemingly as consistent as gravity: Jobs and investment flow from north to south, while manufactured goods travel the other way around. Factories in the United States and Canada shutter as work shifts to Mexico and Central America, where human hands do it more cheaply.

So the established order of trade was by all appearances turned upside down on Tuesday, as General Motors agreed to cease manufacturing an automobile engine at a factory in Mexico while moving jobs to a plant in Canada.

…

In an era of increasingly sophisticated manufacturing that relies more on computers and robotics than low-wage hands, centers of innovation like Canada and the United States will exert a greater pull than before.

…

Given that state-of-the-art products fetch a higher price, it is presumably worth paying a premium to the limited numbers of humans involved in their creation — and especially since this buys proximity to the minds that dream up lucrative new visions. The Canadian plant getting the jobs sits near Waterloo, the birthplace of the BlackBerry, which is something like Canada’s Silicon Valley.

…

Above all, the deal underscores the potency of markets in shaping what happens in commercial life, a force far more powerful than demagogues making dubious promises about tearing up trade deals.

CalPERS, the giant pension fund that doesn’t do credit analysis, is the subject of some sharp commentary by Megan McArdle:

For example, Calpers, which uses a 7.5 percent discount rate, has a funding level of about 75 percent. It is currently contemplating lowering that discount rate all the way to 6.5 percent, but only over two decades.

It’s hard to believe that 20 years was chosen for mathematical reasons. After all, the wave of boomer retirements, which will be the greatest stressor our national retirement systems have ever seen, should be well over by 2035. Rather, one suspects it was chosen because Calpers doesn’t dare change it faster. Changing it faster would mean big increases in current contributions.

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.8273 % |

1,698.3 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.8273 % |

3,102.4 |

| Floater |

4.87 % |

4.59 % |

93,930 |

16.27 |

4 |

0.8273 % |

1,787.9 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0953 % |

2,882.0 |

| SplitShare |

5.05 % |

4.80 % |

76,122 |

2.17 |

5 |

0.0953 % |

3,441.7 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0953 % |

2,685.3 |

| Perpetual-Premium |

5.50 % |

4.59 % |

64,217 |

1.96 |

12 |

0.2545 % |

2,684.7 |

| Perpetual-Discount |

5.14 % |

5.15 % |

89,206 |

15.00 |

26 |

0.1231 % |

2,905.0 |

| FixedReset |

4.98 % |

4.44 % |

147,743 |

6.95 |

92 |

0.2045 % |

2,044.3 |

| Deemed-Retractible |

5.03 % |

4.49 % |

112,649 |

3.20 |

32 |

0.1480 % |

2,796.4 |

| FloatingReset |

2.84 % |

4.41 % |

32,056 |

4.99 |

12 |

0.1840 % |

2,203.5 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| MFC.PR.H |

FixedReset |

1.04 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.35

Bid-YTW : 6.19 % |

| VNR.PR.A |

FixedReset |

1.04 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 18.40

Evaluated at bid price : 18.40

Bid-YTW : 4.97 % |

| TRP.PR.H |

FloatingReset |

1.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 10.67

Evaluated at bid price : 10.67

Bid-YTW : 4.24 % |

| BMO.PR.A |

FloatingReset |

1.18 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.50

Bid-YTW : 4.65 % |

| TRP.PR.F |

FloatingReset |

1.31 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 13.88

Evaluated at bid price : 13.88

Bid-YTW : 4.41 % |

| BAM.PR.S |

FloatingReset |

1.36 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 14.95

Evaluated at bid price : 14.95

Bid-YTW : 4.74 % |

| BAM.PR.B |

Floater |

1.37 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 10.38

Evaluated at bid price : 10.38

Bid-YTW : 4.55 % |

| SLF.PR.H |

FixedReset |

1.37 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.30

Bid-YTW : 8.92 % |

| BAM.PR.C |

Floater |

1.48 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 10.31

Evaluated at bid price : 10.31

Bid-YTW : 4.59 % |

| BAM.PF.G |

FixedReset |

1.65 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 20.35

Evaluated at bid price : 20.35

Bid-YTW : 4.64 % |

| BAM.PR.K |

Floater |

2.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 10.40

Evaluated at bid price : 10.40

Bid-YTW : 4.55 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| TD.PF.H |

FixedReset |

986,699 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-10-31

Maturity Price : 25.00

Evaluated at bid price : 25.48

Bid-YTW : 4.52 % |

| BNS.PR.H |

FixedReset |

907,815 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2022-01-26

Maturity Price : 25.00

Evaluated at bid price : 25.48

Bid-YTW : 4.48 % |

| NA.PR.A |

FixedReset |

236,165 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-08-15

Maturity Price : 25.00

Evaluated at bid price : 26.45

Bid-YTW : 4.44 % |

| TD.PF.A |

FixedReset |

221,900 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 18.80

Evaluated at bid price : 18.80

Bid-YTW : 4.21 % |

| RY.PR.H |

FixedReset |

136,200 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 18.83

Evaluated at bid price : 18.83

Bid-YTW : 4.19 % |

| BAM.PR.K |

Floater |

80,300 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 10.40

Evaluated at bid price : 10.40

Bid-YTW : 4.55 % |

| There were 21 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| MFC.PR.O |

FixedReset |

Quote: 26.62 – 26.98

Spot Rate : 0.3600

Average : 0.2211

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-06-19

Maturity Price : 25.00

Evaluated at bid price : 26.62

Bid-YTW : 4.12 % |

| BAM.PR.S |

FloatingReset |

Quote: 14.95 – 15.35

Spot Rate : 0.4000

Average : 0.2710

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 14.95

Evaluated at bid price : 14.95

Bid-YTW : 4.74 % |

| CU.PR.H |

Perpetual-Discount |

Quote: 25.09 – 25.50

Spot Rate : 0.4100

Average : 0.2869

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 24.68

Evaluated at bid price : 25.09

Bid-YTW : 5.26 % |

| BIP.PR.C |

FixedReset |

Quote: 25.30 – 25.53

Spot Rate : 0.2300

Average : 0.1411

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-09-30

Maturity Price : 25.00

Evaluated at bid price : 25.30

Bid-YTW : 5.08 % |

| TRP.PR.G |

FixedReset |

Quote: 20.32 – 20.60

Spot Rate : 0.2800

Average : 0.2027

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 20.32

Evaluated at bid price : 20.32

Bid-YTW : 4.61 % |

| CU.PR.G |

Perpetual-Discount |

Quote: 22.73 – 22.98

Spot Rate : 0.2500

Average : 0.1728

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-09-21

Maturity Price : 22.44

Evaluated at bid price : 22.73

Bid-YTW : 4.98 % |