Commodities got smacked yesterday. Today it was technology’s turn:

The biggest technology rally since October was knocked cold, as disappointing earnings reports punished Microsoft Corp. and left Apple Inc. in danger of its worst-ever loss of market value.

Five days after Google Inc.’s earnings sparked the largest one-day increase in market capitalization, computer and software shares are tumbling. Apple, Microsoft and Yahoo! Inc. retreated on disappointing results. Apple, the world’s most valuable company, dropped 6.7 percent, a slump that would wipe more than $50 billion from its value.

Hopes were high for the industry as earnings season began, with shares in the sector leading a rebound in U.S. equities after overseas tensions eased. The Nasdaq Composite Index rallied to an all-time high on July 17 after Google surged 16 percent, adding $65 billion to its market cap.

…

Cracks in the facade appeared before Tuesday. Intel Corp., kicking off earnings by the largest U.S. technology companies last week, said it expects the personal-computer market to fall further than expected, spotlighting the challenges for chipmakers. International Business Machines Corp. dropped 5.9 percent during regular trading Tuesday after sales fell for a 13th quarter.

…

Microsoft slid 3.1 percent following its largest-ever quarterly net loss, hurt by a $7.5 billion writedown after the purchase of Nokia’s handset unit failed to rescue the company’s mobile business.

According to Big Taxi funding recipient de Blasio, New York may have too many taxis:

The New York City Council may vote as soon as this week on Mayor Bill de Blasio’s plan to limit the growth of ride-hailing service Uber Technologies Inc.

No decision has been made on whether the measure will come up at the council’s next scheduled meeting Thursday, said Eric Koch, a spokesman for Speaker Melissa Mark-Viverito. The bill would first have to clear the transportation committee, where it has the support of Chairman Ydanis Rodriguez, an outspoken Uber critic backed by the yellow-taxi industry. De Blasio said Monday that he wanted the council to vote “as quickly as possible.”

The measure would restrict the growth of fleets with 500 or more cars to 1 percent while city officials conduct a study on traffic congestion, which would be due April 30. While the limit would affect all for-hire ride services, including traditional black-car companies like Carmel and Dial 7, the biggest loser would be San Francisco-based Uber, which has grown to include 19,000 vehicles and is expanding about 3 percent a month.

…

The legislation is the latest battle in a fight between the traditional taxi and limousine industry, which gave de Blasio’s 2013 mayoral campaign more than $500,000, and digital ride-sharing companies like Uber and Lyft Inc. The taxi industry also donated more than $150,000 to council members, including more than $27,000 this year to [City Council Speaker] Mark-Viverito. [Transportation committee Chairman Ydanis] Rodriguez received $8,500 in 2013.

It was a mixed, but mostly negative, day for the Canadian preferred share market, with PerpetualDiscounts gaining 5bp, FixedResets down 30bp and DeemedRetractibles off 21bp. The Performance Highlights table continues to illustrate a high level of volatility in the marketplace. Volume was average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

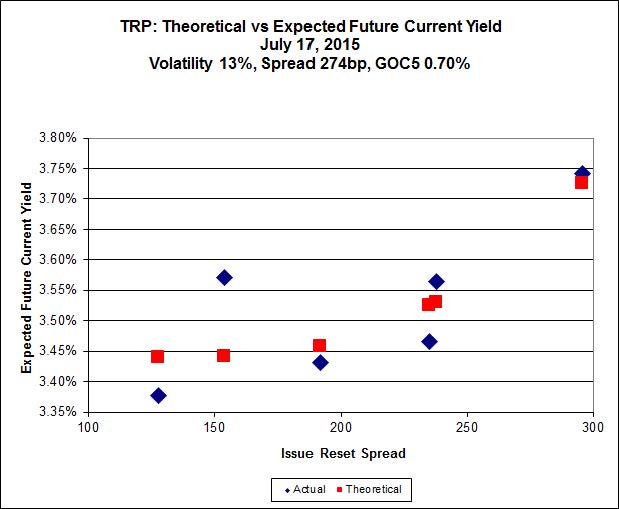

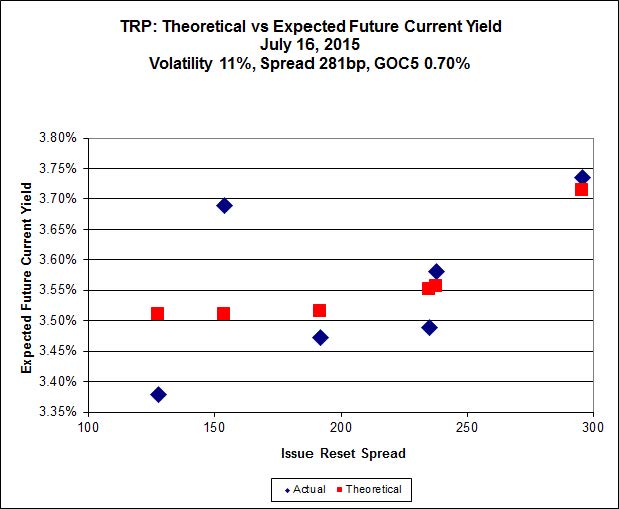

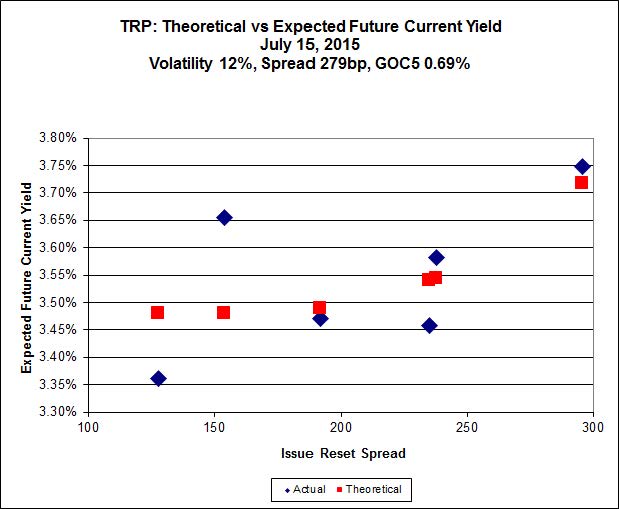

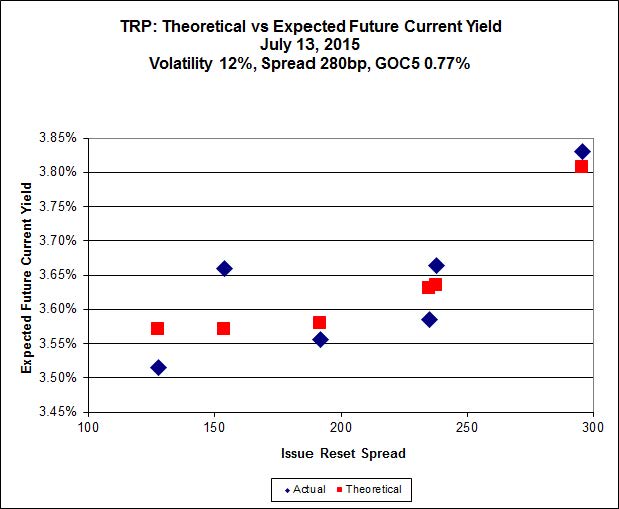

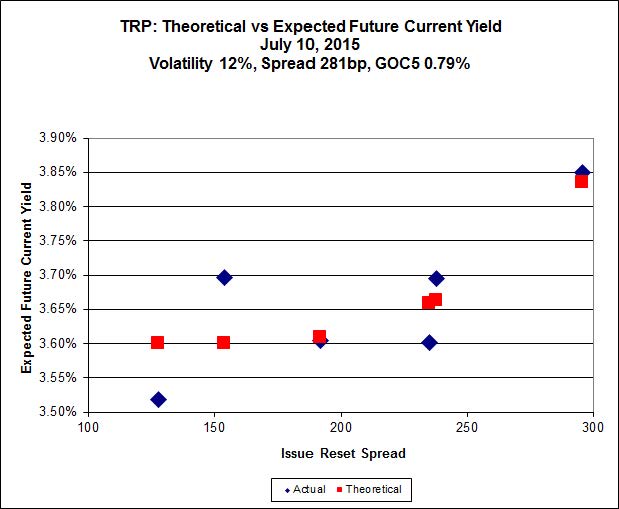

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +128, is bid at 22.30 to be $0.78 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.88 cheap at its bid price of 15.30.

Click for Big

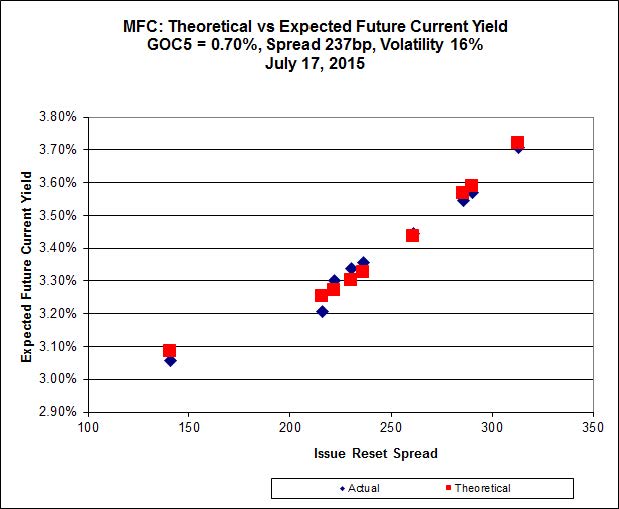

Another good fit today!

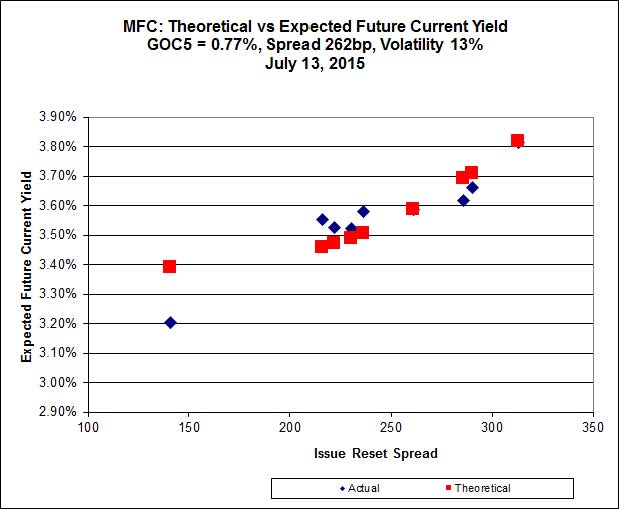

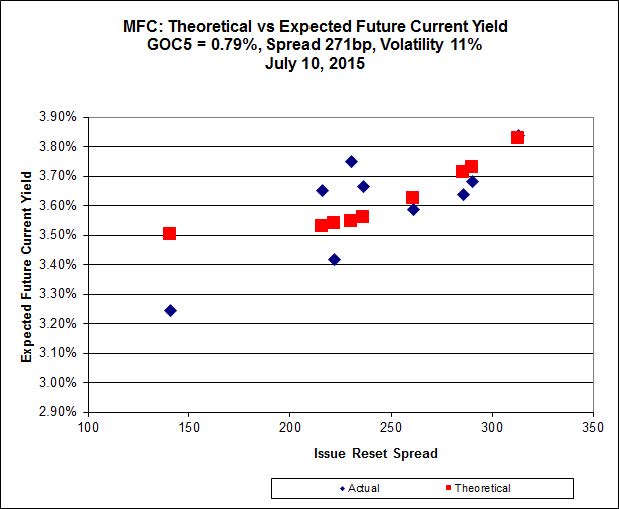

Most expensive is MFC.PR.J, resetting at +261bp on 2018-3-19, bid at 24.31 to be $0.33 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 22.00 to be $0.22 cheap.

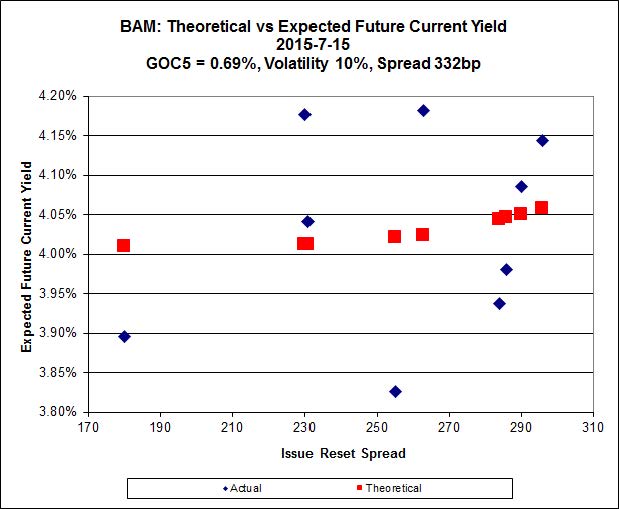

Click for Big

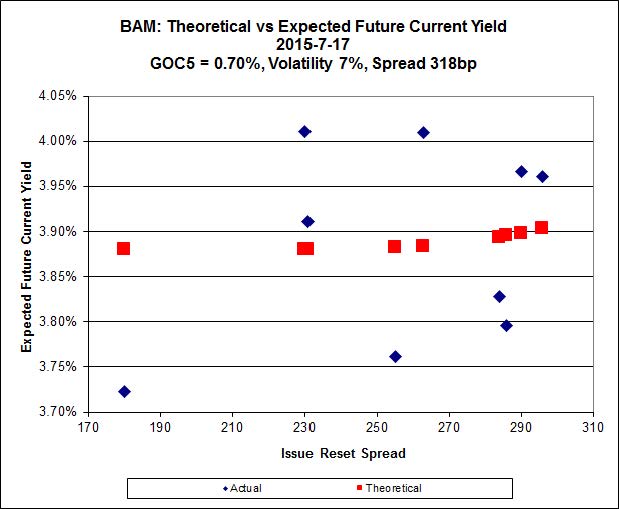

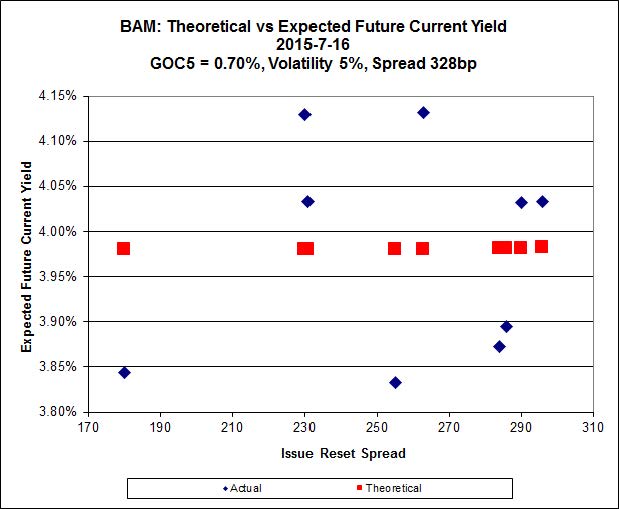

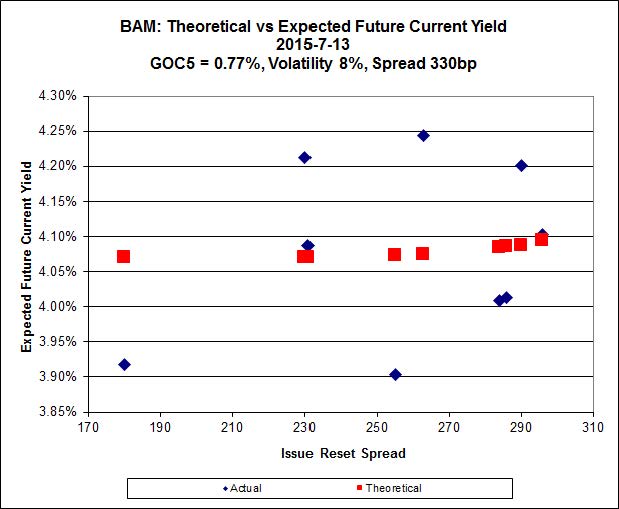

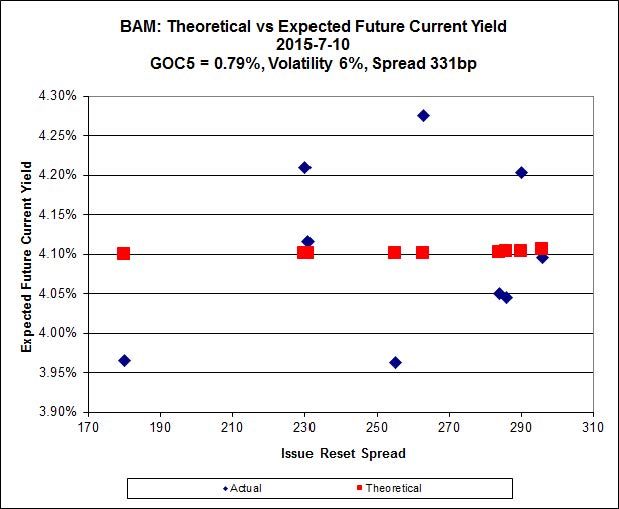

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-06-30, bid at 18.68 to be $0.83 cheap. BAM.PR.X, resetting at +180bp on 2017-6-30 is bid at 17.20 and appears to be $0.95 rich.

Click for Big

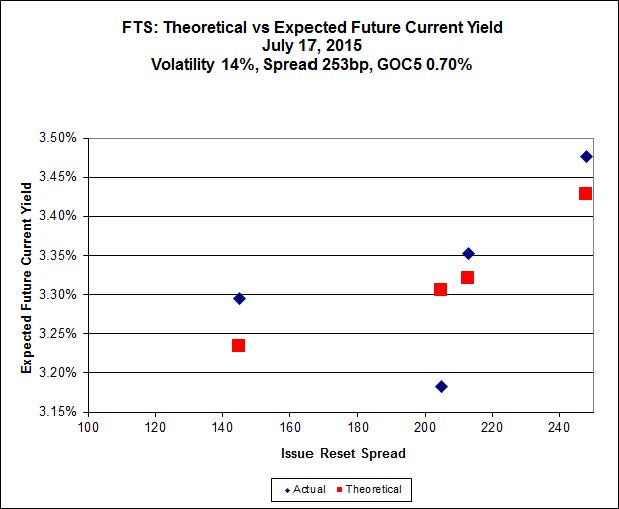

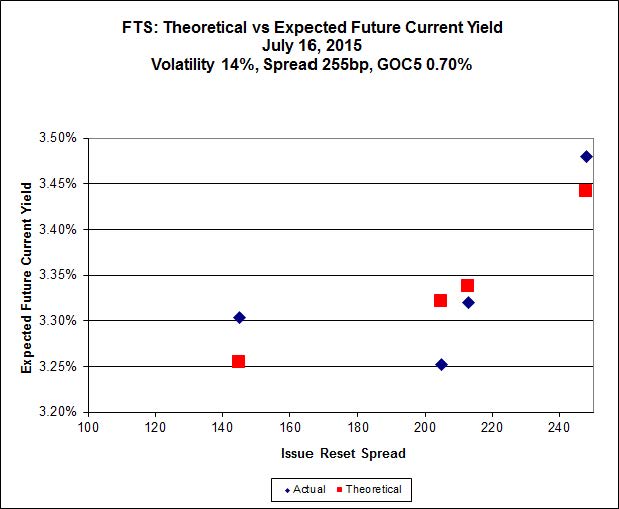

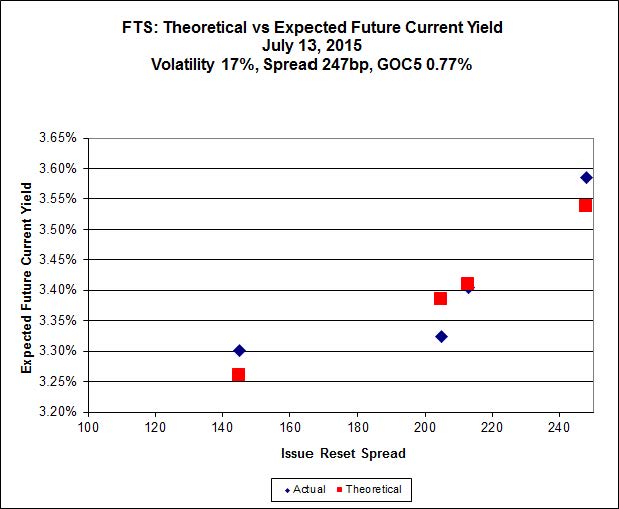

FTS.PR.K, with a spread of +205bp, and bid at 21.63, looks $0.79 expensive and resets 2019-3-1. FTS.PR.M, with a spread of +248bp and resetting 2019-12-1, is bid at 23.00 and is $0.30 cheap.

Click for Big

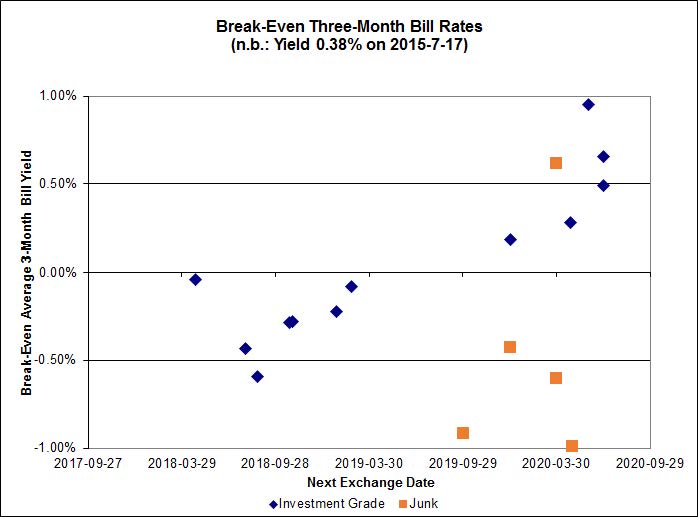

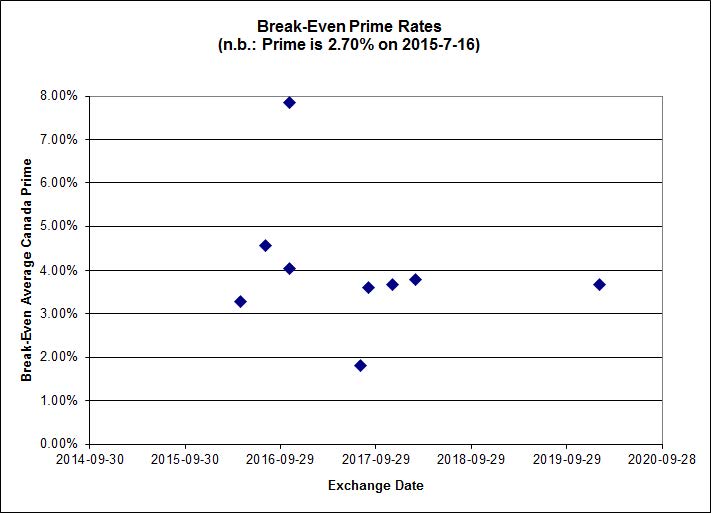

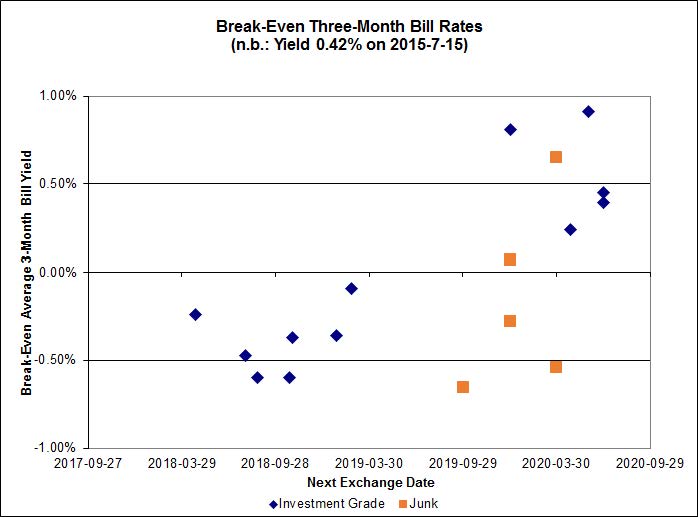

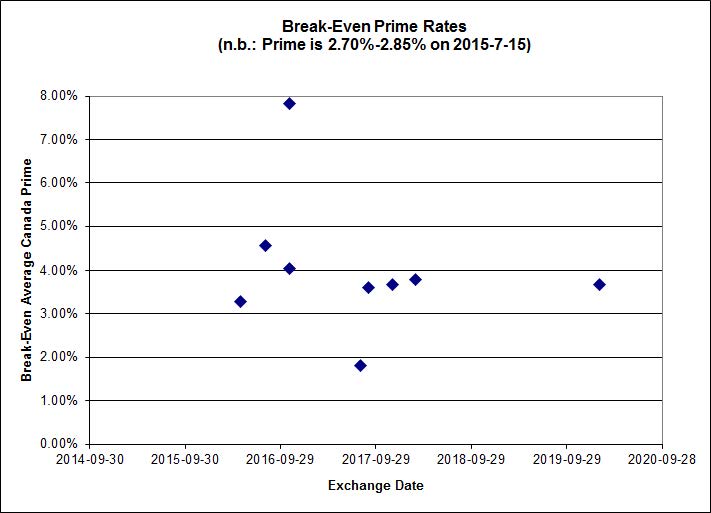

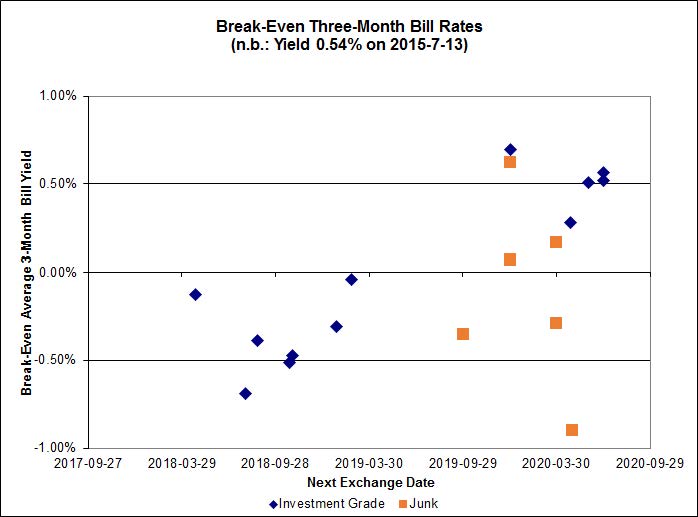

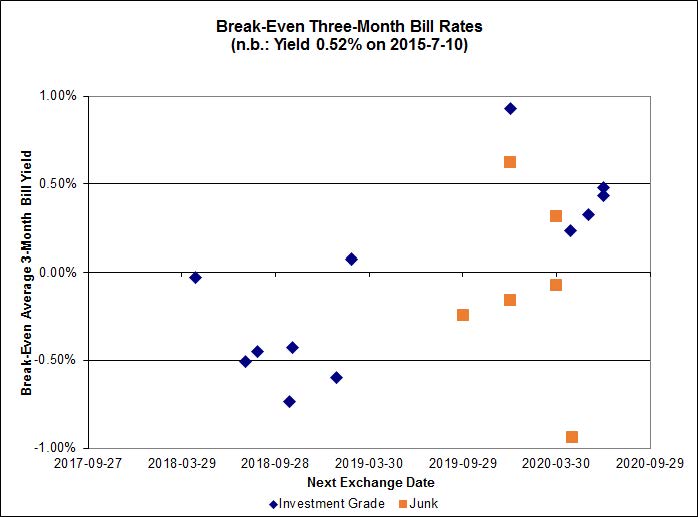

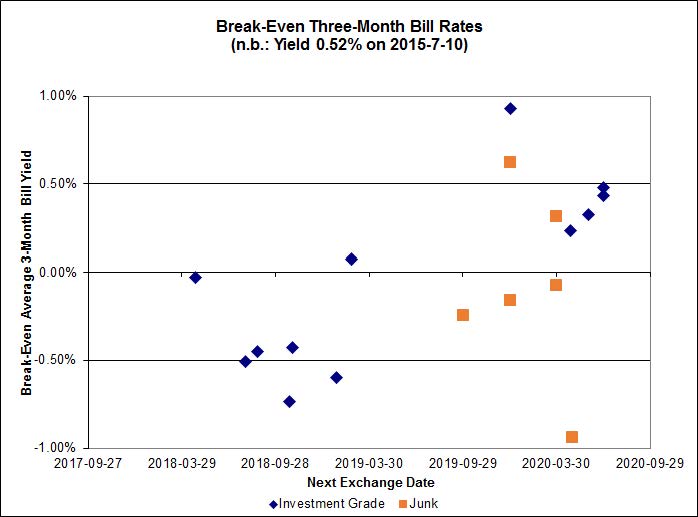

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of 0.05%, with one outliers above 1.00%. There is also one junk pair below -1.00%.

Click for Big

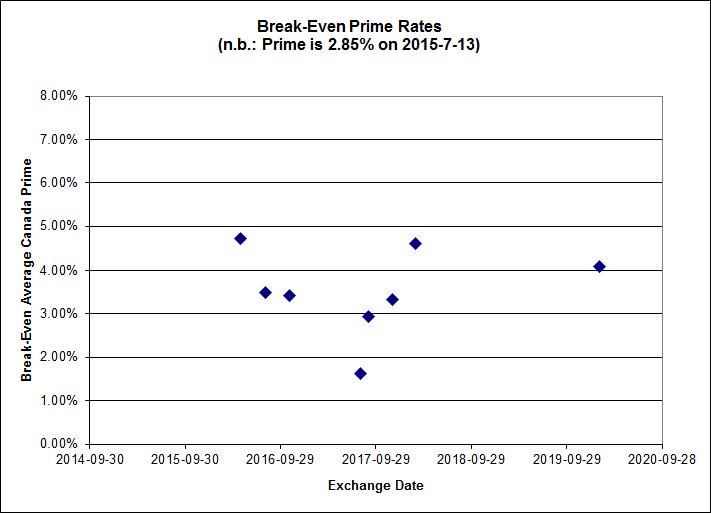

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.7243 % | 2,057.5 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.7243 % | 3,597.4 |

| Floater | 3.57 % | 3.62 % | 62,440 | 18.26 | 3 | -0.7243 % | 2,187.2 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2961 % | 2,768.1 |

| SplitShare | 4.60 % | 4.94 % | 67,020 | 3.19 | 3 | 0.2961 % | 3,244.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2961 % | 2,531.1 |

| Perpetual-Premium | 5.52 % | 3.69 % | 74,284 | 0.28 | 13 | -0.1188 % | 2,510.3 |

| Perpetual-Discount | 5.33 % | 5.31 % | 87,558 | 14.89 | 22 | 0.0489 % | 2,676.4 |

| FixedReset | 4.61 % | 3.69 % | 221,426 | 16.29 | 88 | -0.3021 % | 2,280.2 |

| Deemed-Retractible | 5.03 % | 4.97 % | 112,282 | 5.51 | 34 | -0.2071 % | 2,613.1 |

| FloatingReset | 2.36 % | 3.07 % | 45,059 | 6.07 | 10 | -0.1881 % | 2,280.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PWF.PR.P | FixedReset | -2.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 16.55 Evaluated at bid price : 16.55 Bid-YTW : 3.54 % |

| TRP.PR.F | FloatingReset | -2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 3.31 % |

| ENB.PR.J | FixedReset | -2.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 18.31 Evaluated at bid price : 18.31 Bid-YTW : 4.85 % |

| IFC.PR.A | FixedReset | -2.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.36 Bid-YTW : 6.91 % |

| IAG.PR.G | FixedReset | -1.81 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.40 Bid-YTW : 4.07 % |

| MFC.PR.L | FixedReset | -1.79 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 4.99 % |

| ENB.PR.N | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 18.08 Evaluated at bid price : 18.08 Bid-YTW : 4.87 % |

| BNS.PR.Z | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.92 Bid-YTW : 3.68 % |

| TRP.PR.G | FixedReset | -1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 22.78 Evaluated at bid price : 24.06 Bid-YTW : 3.79 % |

| TRP.PR.E | FixedReset | -1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 21.88 Evaluated at bid price : 22.30 Bid-YTW : 3.68 % |

| ENB.PF.E | FixedReset | -1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 18.96 Evaluated at bid price : 18.96 Bid-YTW : 4.87 % |

| MFC.PR.N | FixedReset | -1.45 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.47 Bid-YTW : 4.82 % |

| BAM.PR.K | Floater | -1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 13.15 Evaluated at bid price : 13.15 Bid-YTW : 3.62 % |

| TD.PF.C | FixedReset | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 21.67 Evaluated at bid price : 22.01 Bid-YTW : 3.53 % |

| ENB.PF.A | FixedReset | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.82 % |

| BAM.PR.Z | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 22.81 Evaluated at bid price : 23.51 Bid-YTW : 4.04 % |

| ENB.PF.C | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 18.90 Evaluated at bid price : 18.90 Bid-YTW : 4.85 % |

| TRP.PR.D | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 21.31 Evaluated at bid price : 21.60 Bid-YTW : 3.75 % |

| HSB.PR.C | Deemed-Retractible | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.05 Bid-YTW : 5.15 % |

| ENB.PR.T | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 17.92 Evaluated at bid price : 17.92 Bid-YTW : 4.77 % |

| HSB.PR.D | Deemed-Retractible | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.80 Bid-YTW : 5.23 % |

| HSE.PR.E | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 22.72 Evaluated at bid price : 23.83 Bid-YTW : 4.51 % |

| TRP.PR.C | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 15.27 Evaluated at bid price : 15.27 Bid-YTW : 3.74 % |

| ENB.PR.Y | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 17.47 Evaluated at bid price : 17.47 Bid-YTW : 4.78 % |

| MFC.PR.F | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.00 Bid-YTW : 7.07 % |

| HSE.PR.G | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 22.67 Evaluated at bid price : 23.75 Bid-YTW : 4.53 % |

| TRP.PR.H | FloatingReset | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 2.79 % |

| BNS.PR.Y | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.52 Bid-YTW : 3.50 % |

| NA.PR.W | FixedReset | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 21.92 Evaluated at bid price : 22.38 Bid-YTW : 3.49 % |

| CU.PR.G | Perpetual-Discount | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 21.92 Evaluated at bid price : 22.24 Bid-YTW : 5.11 % |

| HSE.PR.C | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 22.22 Evaluated at bid price : 22.85 Bid-YTW : 4.36 % |

| BAM.PR.R | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 18.68 Evaluated at bid price : 18.68 Bid-YTW : 4.19 % |

| CM.PR.P | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 21.80 Evaluated at bid price : 22.20 Bid-YTW : 3.50 % |

| IFC.PR.C | FixedReset | 1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.15 Bid-YTW : 5.04 % |

| BAM.PR.X | FixedReset | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 17.20 Evaluated at bid price : 17.20 Bid-YTW : 3.96 % |

| FTS.PR.J | Perpetual-Discount | 1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 23.84 Evaluated at bid price : 24.25 Bid-YTW : 4.94 % |

| RY.PR.M | FixedReset | 2.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 22.94 Evaluated at bid price : 24.44 Bid-YTW : 3.43 % |

| MFC.PR.J | FixedReset | 2.62 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.31 Bid-YTW : 3.93 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.F | Perpetual-Discount | 464,790 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 24.29 Evaluated at bid price : 24.66 Bid-YTW : 4.98 % |

| ENB.PF.A | FixedReset | 108,792 | Nesbitt crossed 100,000 at 19.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.82 % |

| ENB.PF.C | FixedReset | 80,465 | Nesbitt crossed 50,000 at 19.00 and sold 13,000 to RBC at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 18.90 Evaluated at bid price : 18.90 Bid-YTW : 4.85 % |

| ENB.PR.N | FixedReset | 80,040 | TD crossed 71,000 at 18.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 18.08 Evaluated at bid price : 18.08 Bid-YTW : 4.87 % |

| ENB.PR.F | FixedReset | 76,866 | Secotia crossed three blocks, one of 50,000 and two of 10,000, all at 17.40. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-21 Maturity Price : 17.38 Evaluated at bid price : 17.38 Bid-YTW : 4.87 % |

| RY.PR.A | Deemed-Retractible | 73,225 | RBC crossed 50,000 at 25.22. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.16 Bid-YTW : 4.48 % |

| There were 30 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.P | FixedReset | Quote: 16.55 – 17.48 Spot Rate : 0.9300 Average : 0.6637 YTW SCENARIO |

| IAG.PR.G | FixedReset | Quote: 24.40 – 24.96 Spot Rate : 0.5600 Average : 0.3579 YTW SCENARIO |

| ELF.PR.G | Perpetual-Discount | Quote: 22.15 – 22.83 Spot Rate : 0.6800 Average : 0.4919 YTW SCENARIO |

| CM.PR.O | FixedReset | Quote: 22.82 – 23.49 Spot Rate : 0.6700 Average : 0.5098 YTW SCENARIO |

| HSE.PR.E | FixedReset | Quote: 23.83 – 24.45 Spot Rate : 0.6200 Average : 0.4619 YTW SCENARIO |

| MFC.PR.N | FixedReset | Quote: 22.47 – 23.00 Spot Rate : 0.5300 Average : 0.3888 YTW SCENARIO |