The FOMC release was ‘steady as she goes’:

Information received since the Federal Open Market Committee met in December suggests that economic activity has been expanding at a solid pace. Labor market conditions have improved further, with strong job gains and a lower unemployment rate. On balance, a range of labor market indicators suggests that underutilization of labor resources continues to diminish. Household spending is rising moderately; recent declines in energy prices have boosted household purchasing power. Business fixed investment is advancing, while the recovery in the housing sector remains slow. Inflation has declined further below the Committee’s longer-run objective, largely reflecting declines in energy prices. Market-based measures of inflation compensation have declined substantially in recent months; survey-based measures of longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace, with labor market indicators continuing to move toward levels the Committee judges consistent with its dual mandate. The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced. Inflation is anticipated to decline further in the near term, but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of lower energy prices and other factors dissipate. The Committee continues to monitor inflation developments closely.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate.

…

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

… but markets were hoping for more gloom (which makes sense, right? Ummmm….):

U.S. stocks fell, sending the Dow Jones Industrial Average to its biggest two-day loss in a year, as energy shares plunged and concern grew about international risks to the American economy and weakness in multinational earnings.

Energy companies slumped 3.9 percent as a group after oil retreated. Apple Inc. climbed 5.7 percent after reporting a record $18 billion in quarterly profit, one of the biggest in corporate history. Boeing Co. advanced 5.4 percent as it posted a quarterly profit that beat analysts’ estimates.

The Standard & Poor’s 500 Index fell 1.4 percent to 2,002.16 at 4 p.m. in New York. The Dow Jones Industrial Average lost 195.84 points, or 1.1 percent, to 17,191.37. The gauge fell 2.8 percent over two days, the most since February 2014. The Nasdaq 100 Index dropped 0.6 percent, erasing an earlier rally of 1.7 percent. The Chicago Board Options Exchange Volatility Index, known as the VIX, added 19 percent to 20.44, its biggest jump of the year.

…

U.S. stocks turned lower after the Fed boosted its assessment of the economy and downplayed low inflation readings while repeating a pledge to remain “patient” on raising interest rates. Losses accelerated in the final hour, pushing declines in the Dow and S&P 500 beyond 1 percent and wiping out gains in the Nasdaq.

Karl Marx’ ghost is chuckling quietly about the inherent contradictions of capitalism:

This year, at least a dozen elite colleges, including Chicago, Duke, Dartmouth, and Columbia, have offered extensions of once-sacrosanct January admissions deadlines. The University of Pennsylvania, Vanderbilt, and Bates are among schools whose admissions deans said they were doing so for the first time, aside from individual hardship cases or such emergencies as storms and major website failures.

…

These universities are hardly hurting for customers. More than 30,000 hopefuls are applying to Chicago this year. In the last go-round, the school rejected 92 percent—the most ever—making it one of the most selective schools in the U.S. Advisers and high school seniors say they suspect schools are just burnishing reputations for selectivity. More applications mean more rejections, which heightens a college’s prestige in the world of higher education.

… while I cannot help but wonder what Gloria Steinem would think of keeping women in the seraglio (for their own safety, of course):

Sorority women at the University of Virginia were ordered to stay home on the biggest party night of the year to protect their “safety and well-being” — and they are furious about it.

Members of the National Panhellenic Conference told 16 UVA sorority chapters last week not to participate in Boys’ Bid Night fraternity parties on Saturday. The revelry has led to allegations of sexual assault and excessive drinking in the past. Women who break the prohibition may face sanctions.

“They are treating us like children and punishing us for being women,” said Whitney Rosser, a senior from Lynchburg, Virginia, and a member of Alpha Phi. “We’re angry because we are being told we are not allowed to go out instead of addressing the deeper issue of why sexual assault happens.”

Meanwhile…:

Click for Big

It was another explosively mixed day for the Canadian preferred share market, with PerpetualDiscounts gaining 3bp, FixedResets down 83bp (!) and DeemedRetractibles off 7bp. The Performance Highlights table is suitably enormous. Volume was slightly below average.

PerpetualDiscounts now yield 4.84%, equivalent to 6.29% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 3.71% so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 260bp, a slight (and perhaps spurious) narrowing from the 260bp reported January 21

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

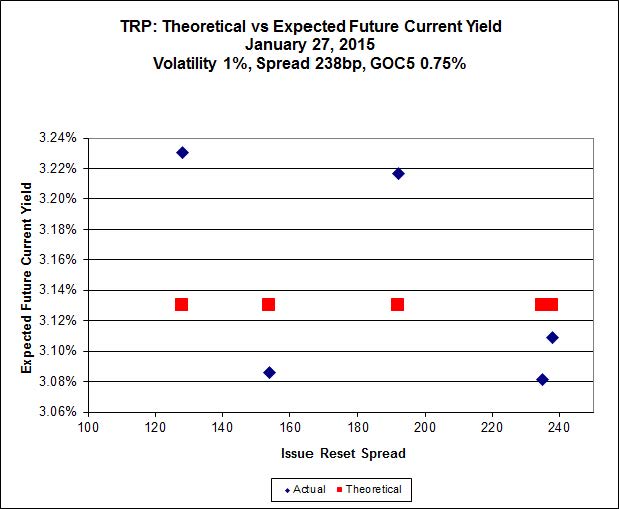

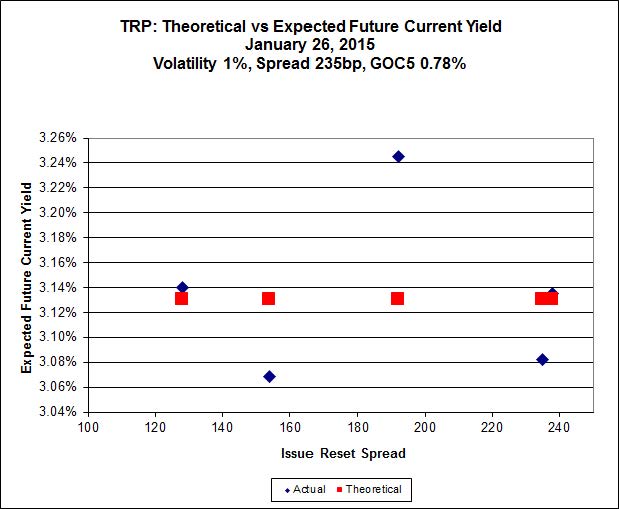

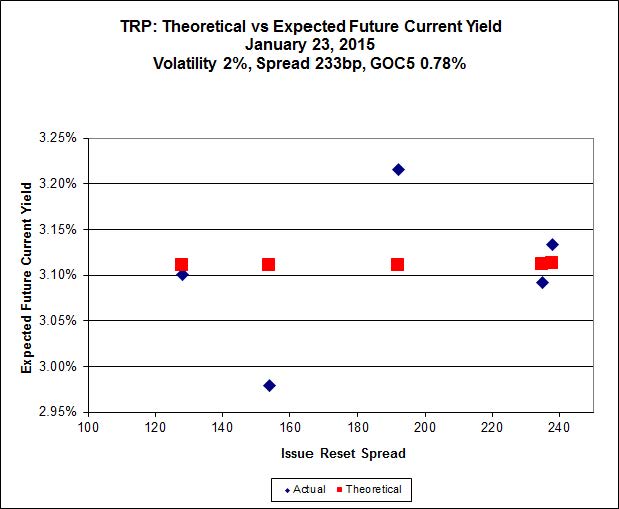

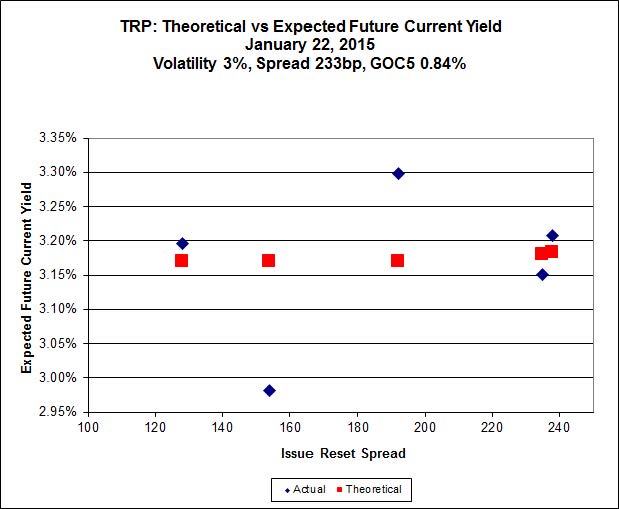

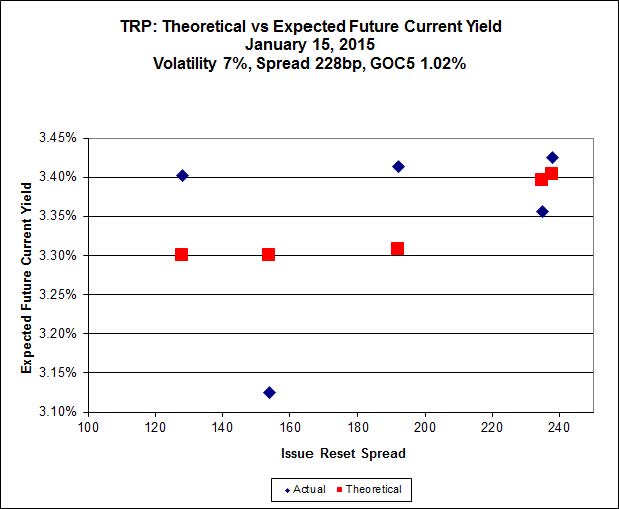

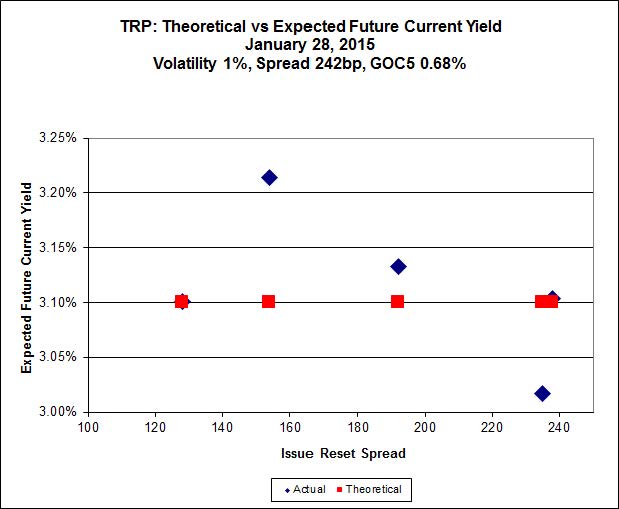

Here’s TRP:

Click for Big

So according to this, the cheapest issue is now TRP.PR.C, bid at 17.27 following its appalling recent performance; it is $0.63 cheap, and will reset 2016-1-30 at +154. TRP.PR.E, bid at 25.11 and resetting at +235bp on 2019-10-30 is $0.67 rich.

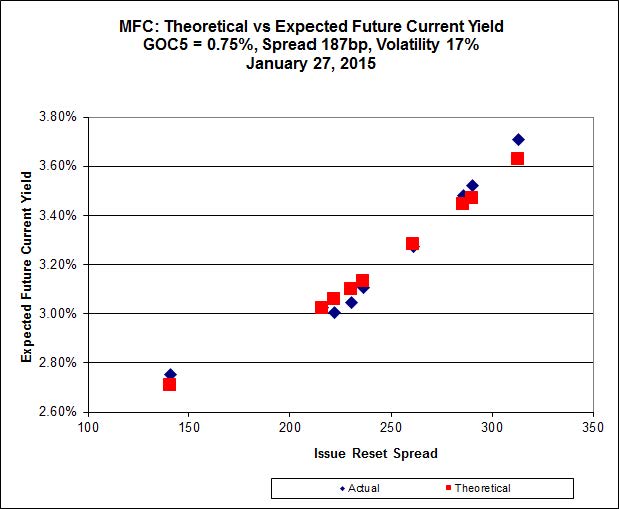

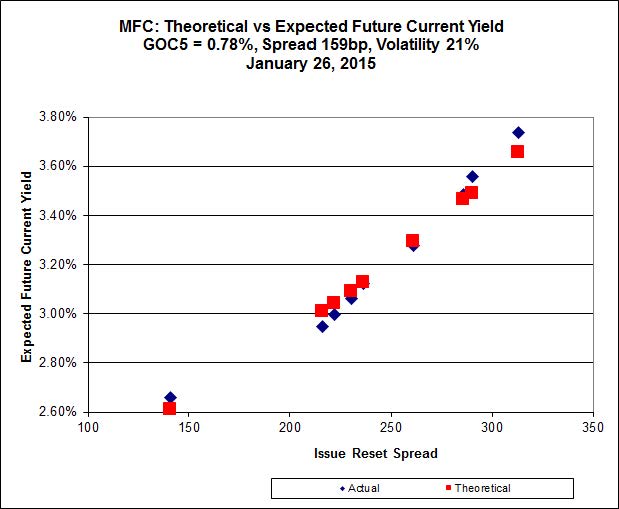

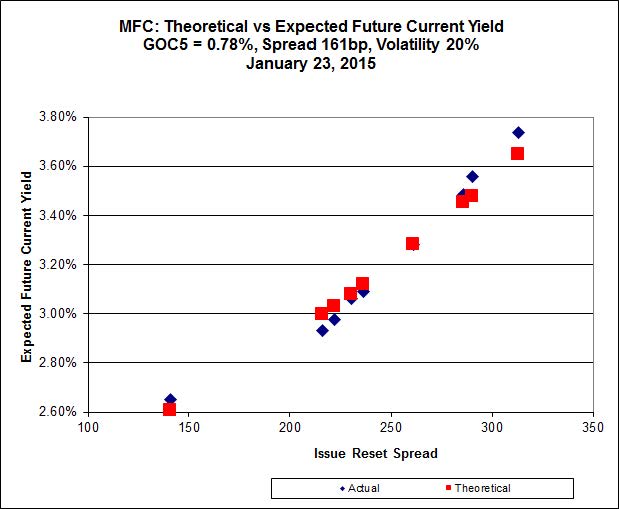

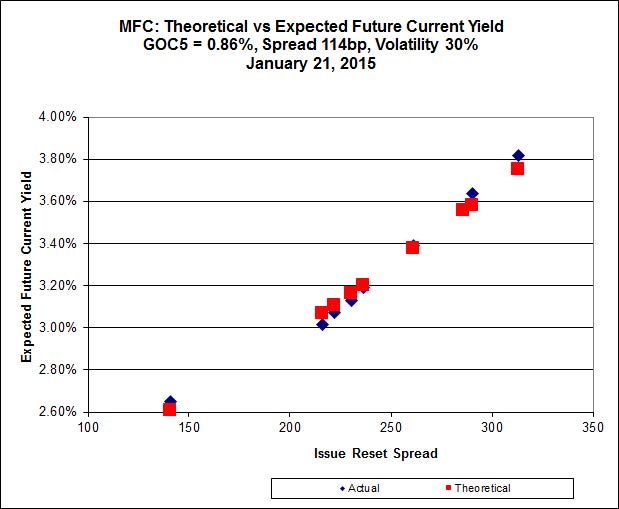

Click for Big

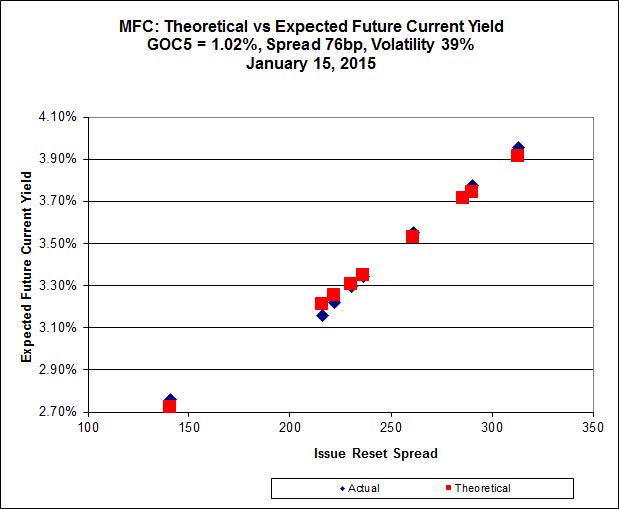

MFC.PR.F is now visibly above the line defined by its peers.

Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

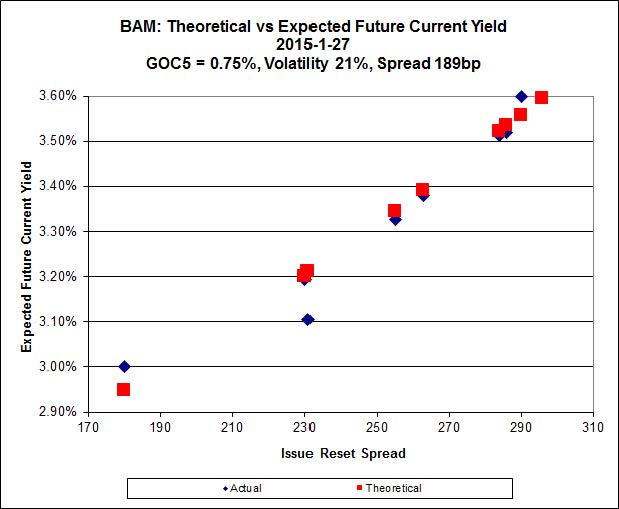

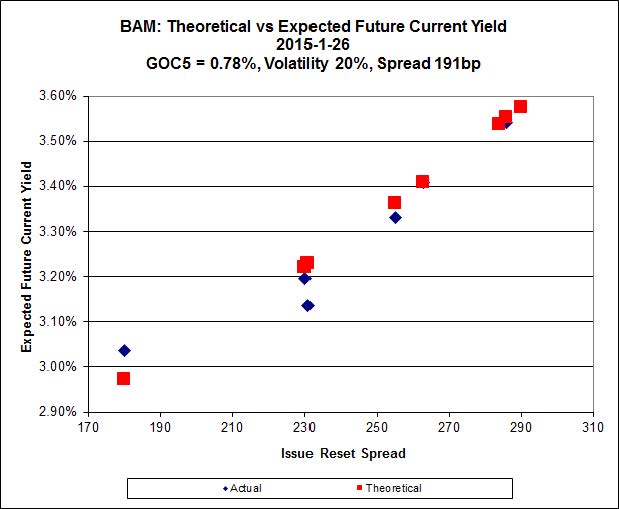

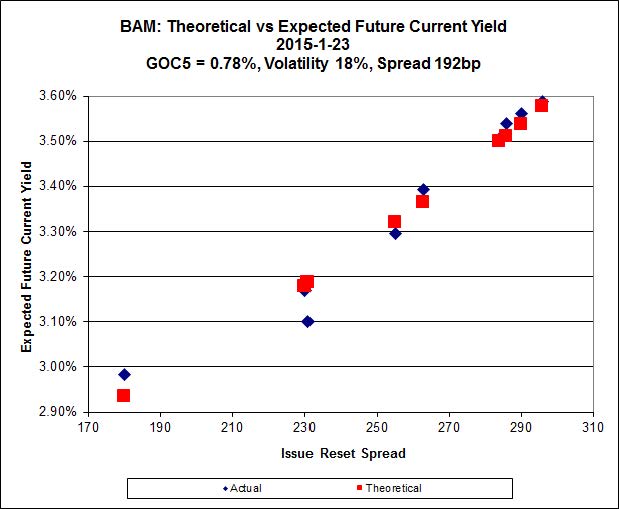

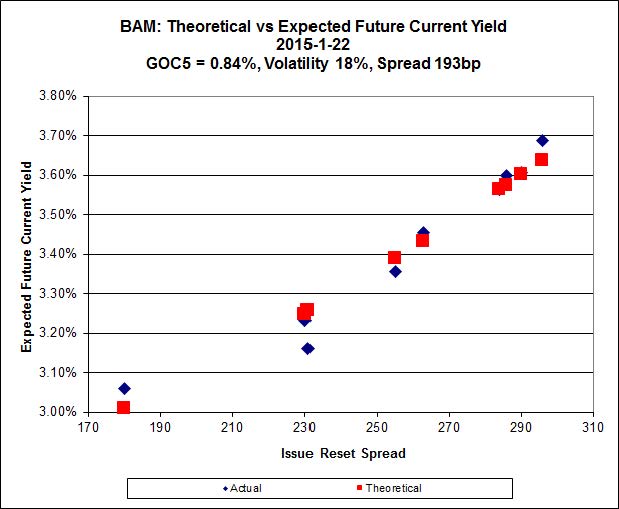

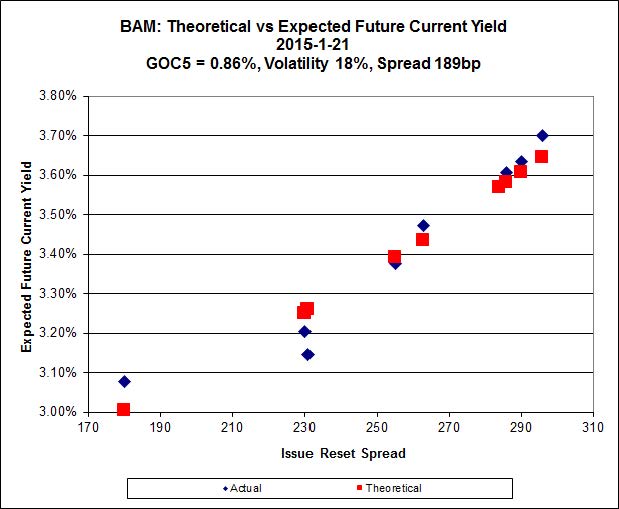

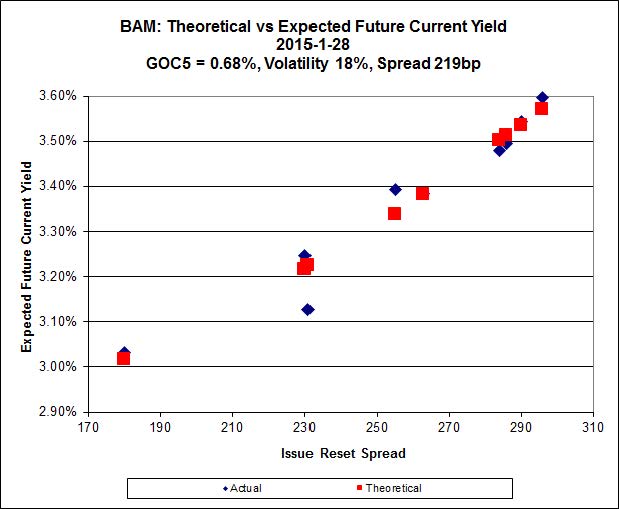

Click for Big

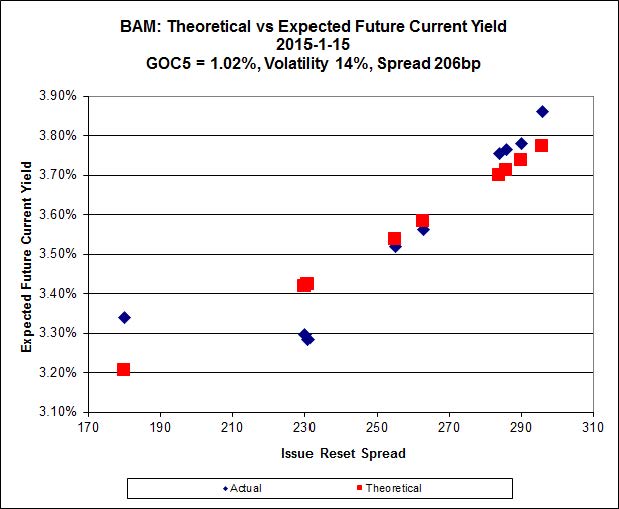

Changes in the market level, which have had the visible effect of reducing Implied Volatility, have resulted in the cheapest issue relative to its peers being BAM.PF.E, resetting at +255bp on 2020-3-31, bid at 23.80 to be $0.40 cheap. BAM.PR.T, resetting at +231bp 2017-3-31 is bid at 23.90 and appears to be $0.72 rich.

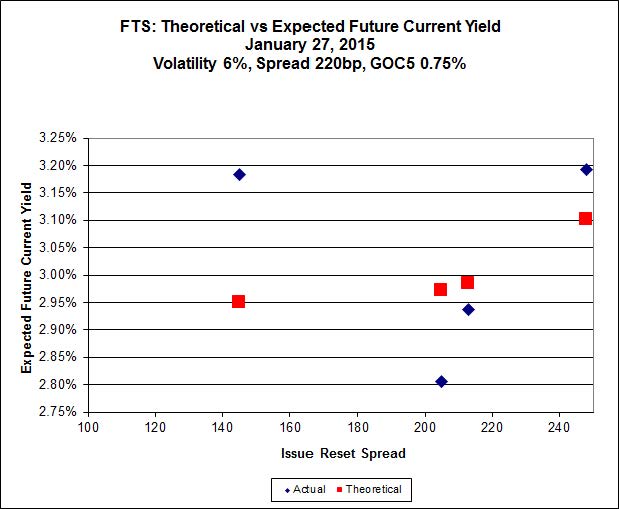

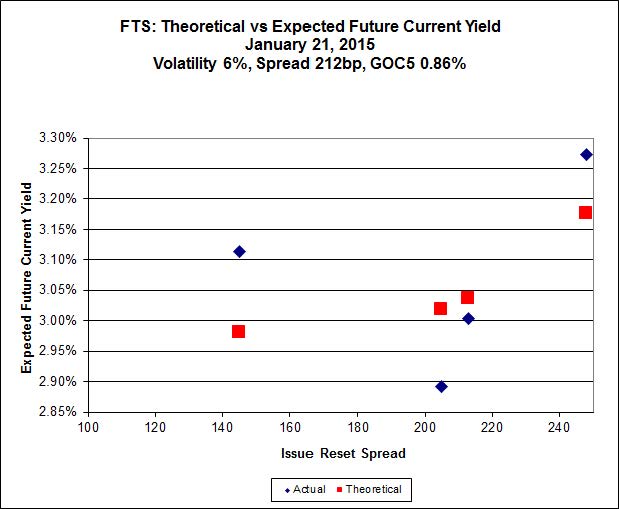

Click for Big

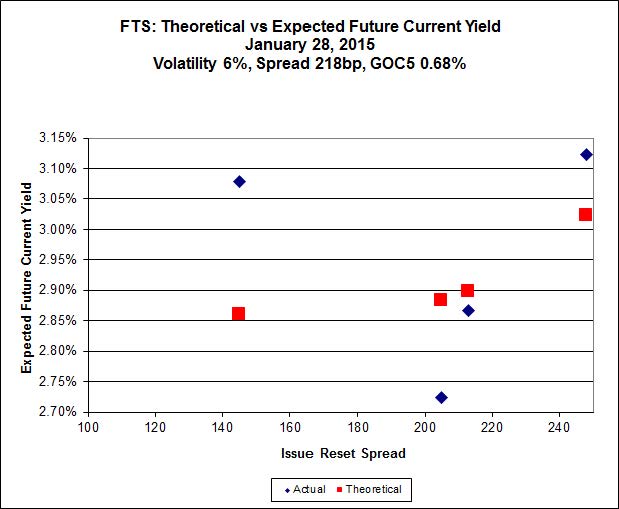

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 17.30, looks $1.32 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp, and bid at 25.05, looks $1.38 expensive and resets 2019-3-1.

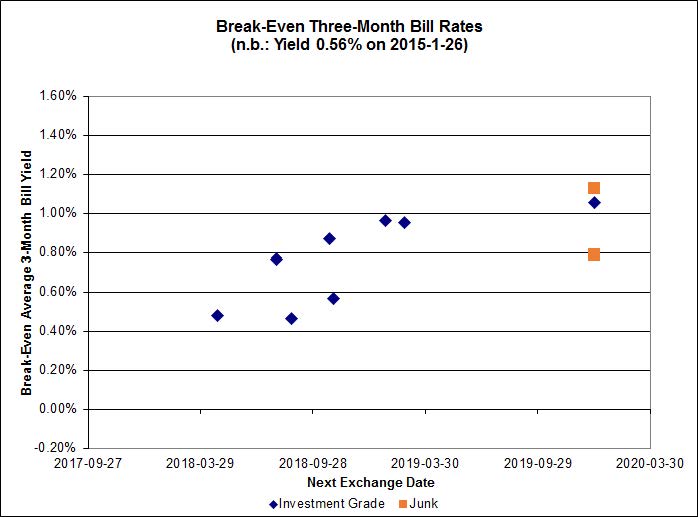

Click for Big

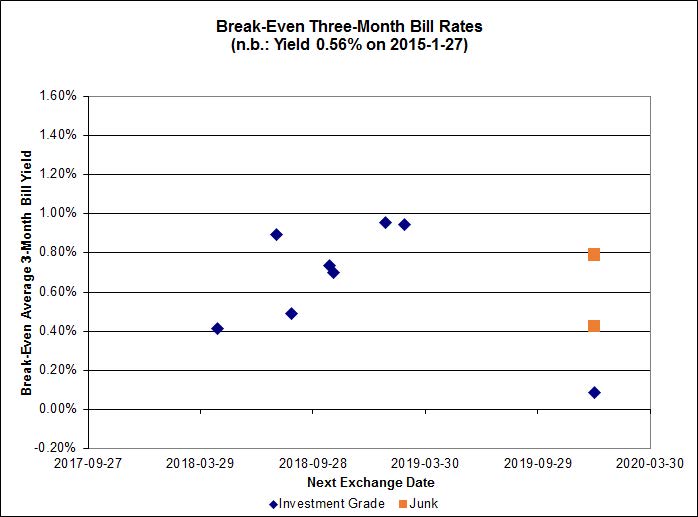

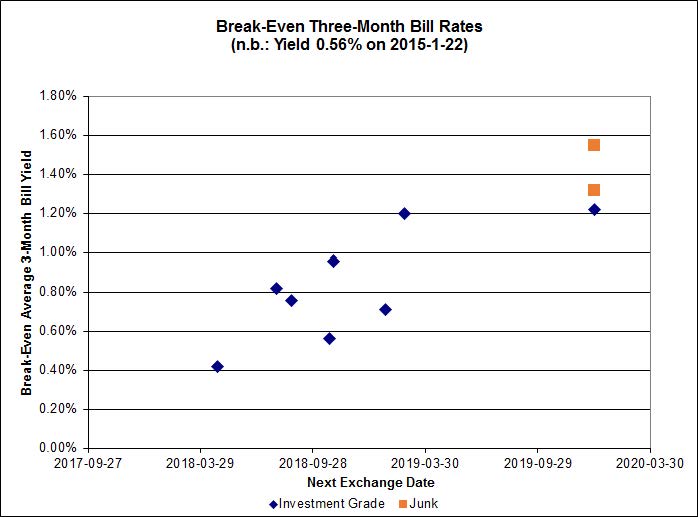

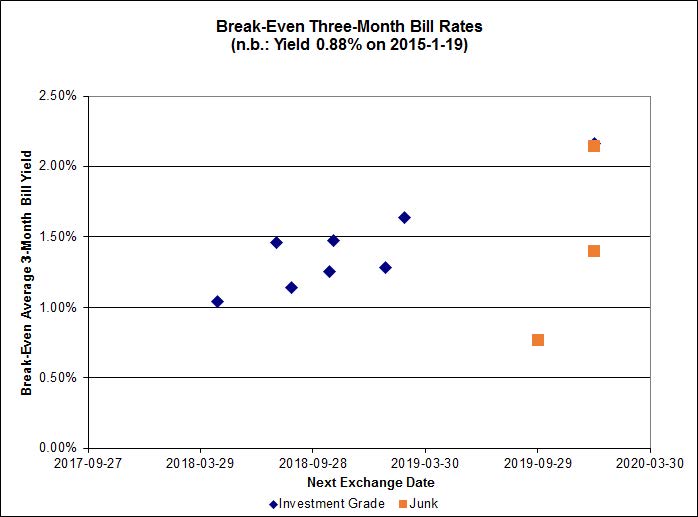

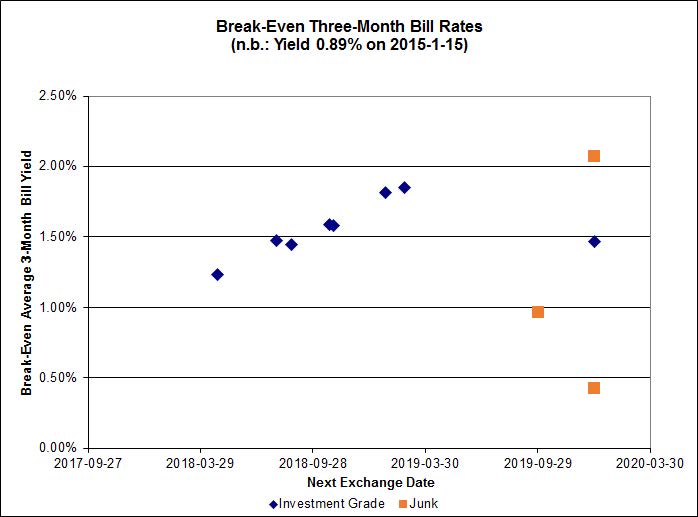

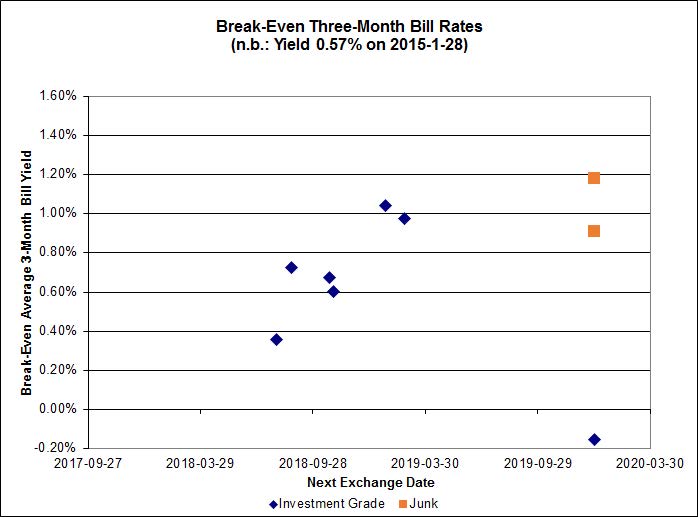

The point representing the DC.PR.B / DC.PR.D pair, interconvertible 2019-9-30, is not shown: it has an implied three-month bill yield of negative 1.27% – rather an extreme view for the market to take!

It is interesting to see that the TRP.PR.A / TRP.PR.F pair is now showing a breakeven three-month bill yield over the next five years of negative 0.16% … surprising to see this in an investment-grade pair, but when the market goes nuts, it doesn’t fool around!

Pairs equivalence is looking more rational, with the investment grade pairs (which are presumably more closely watched and easier to trade) do show a rising trend with increasing time to interconversion which, qualitatively speaking, is entirely reasonable, although the increase (over five years-odd) looks pretty substantial given the scale of the chart (two years-odd). The average break-even rate is way down from recent levels again today

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2155 % | 2,342.4 |

| FixedFloater | 4.33 % | 3.51 % | 20,137 | 18.42 | 1 | 0.4575 % | 4,085.6 |

| Floater | 3.08 % | 3.21 % | 54,521 | 19.20 | 4 | -0.2155 % | 2,490.1 |

| OpRet | 4.05 % | 1.99 % | 103,584 | 0.38 | 1 | 0.0791 % | 2,750.9 |

| SplitShare | 4.28 % | 4.12 % | 29,842 | 3.59 | 5 | 0.0317 % | 3,190.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0791 % | 2,515.4 |

| Perpetual-Premium | 5.42 % | -7.15 % | 56,355 | 0.08 | 19 | 0.0432 % | 2,508.1 |

| Perpetual-Discount | 5.02 % | 4.84 % | 108,158 | 14.98 | 16 | 0.0283 % | 2,760.1 |

| FixedReset | 4.33 % | 3.42 % | 204,899 | 17.23 | 77 | -0.8338 % | 2,472.7 |

| Deemed-Retractible | 4.92 % | 0.30 % | 101,576 | 0.17 | 39 | -0.0666 % | 2,640.7 |

| FloatingReset | 2.49 % | 2.63 % | 69,096 | 6.45 | 7 | -1.2258 % | 2,350.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.C | FixedReset | -6.90 % | Quite real enough, as all of the last twenty-five (small) trades of the day were executed at or below 17.50, with a low of 17.36. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 17.27 Evaluated at bid price : 17.27 Bid-YTW : 3.51 % |

| BNS.PR.A | FloatingReset | -5.21 % | Not real. One odd-lot traded at 23.84 to close the day, but the board-lot low on the day was 24.51. So this is just more of what us fiasco aficionados call a routine report from the Toronto Stock Exchange. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.46 Bid-YTW : 3.54 % |

| BAM.PF.E | FixedReset | -4.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 22.68 Evaluated at bid price : 23.80 Bid-YTW : 3.73 % |

| BAM.PR.R | FixedReset | -3.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 22.53 Evaluated at bid price : 22.95 Bid-YTW : 3.52 % |

| BAM.PR.X | FixedReset | -3.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 20.45 Evaluated at bid price : 20.45 Bid-YTW : 3.47 % |

| BAM.PR.K | Floater | -3.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 15.45 Evaluated at bid price : 15.45 Bid-YTW : 3.25 % |

| BAM.PR.T | FixedReset | -2.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 23.07 Evaluated at bid price : 23.90 Bid-YTW : 3.34 % |

| ENB.PR.P | FixedReset | -2.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 21.36 Evaluated at bid price : 21.66 Bid-YTW : 3.99 % |

| BAM.PR.C | Floater | -2.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 15.48 Evaluated at bid price : 15.48 Bid-YTW : 3.24 % |

| BAM.PR.B | Floater | -2.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 15.64 Evaluated at bid price : 15.64 Bid-YTW : 3.21 % |

| ENB.PR.D | FixedReset | -2.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 21.48 Evaluated at bid price : 21.48 Bid-YTW : 3.88 % |

| PWF.PR.P | FixedReset | -2.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 20.16 Evaluated at bid price : 20.16 Bid-YTW : 3.07 % |

| HSE.PR.A | FixedReset | -2.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 3.47 % |

| ENB.PR.N | FixedReset | -2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 22.05 Evaluated at bid price : 22.51 Bid-YTW : 3.96 % |

| SLF.PR.G | FixedReset | -2.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.06 Bid-YTW : 6.05 % |

| ENB.PF.E | FixedReset | -2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 22.53 Evaluated at bid price : 23.50 Bid-YTW : 3.92 % |

| BAM.PF.B | FixedReset | -2.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 23.03 Evaluated at bid price : 24.45 Bid-YTW : 3.57 % |

| GWO.PR.N | FixedReset | -2.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.60 Bid-YTW : 5.66 % |

| TRP.PR.D | FixedReset | -2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 23.10 Evaluated at bid price : 24.65 Bid-YTW : 3.26 % |

| IFC.PR.C | FixedReset | -2.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.31 Bid-YTW : 3.97 % |

| ENB.PR.F | FixedReset | -1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 21.76 Evaluated at bid price : 22.05 Bid-YTW : 3.90 % |

| ENB.PR.H | FixedReset | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 20.45 Evaluated at bid price : 20.45 Bid-YTW : 3.85 % |

| GWO.PR.P | Deemed-Retractible | -1.62 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-03-31 Maturity Price : 25.25 Evaluated at bid price : 26.10 Bid-YTW : 4.73 % |

| ENB.PR.B | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 21.20 Evaluated at bid price : 21.20 Bid-YTW : 3.92 % |

| BMO.PR.Q | FixedReset | -1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.25 Bid-YTW : 3.65 % |

| GWO.PR.I | Deemed-Retractible | -1.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.67 Bid-YTW : 5.26 % |

| ENB.PR.T | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 21.39 Evaluated at bid price : 21.70 Bid-YTW : 4.00 % |

| TD.PR.T | FloatingReset | -1.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.04 Bid-YTW : 2.70 % |

| TRP.PR.F | FloatingReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 3.26 % |

| BNS.PR.Z | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.05 Bid-YTW : 3.64 % |

| BAM.PF.F | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 23.29 Evaluated at bid price : 25.33 Bid-YTW : 3.67 % |

| ENB.PF.G | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 22.68 Evaluated at bid price : 23.86 Bid-YTW : 3.87 % |

| MFC.PR.M | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.72 Bid-YTW : 3.74 % |

| MFC.PR.H | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-03-19 Maturity Price : 25.00 Evaluated at bid price : 25.87 Bid-YTW : 3.16 % |

| BNS.PR.Y | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.26 Bid-YTW : 3.64 % |

| BMO.PR.M | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.20 Bid-YTW : 2.91 % |

| IAG.PR.A | Deemed-Retractible | 1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.00 Bid-YTW : 4.67 % |

| IFC.PR.A | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.75 Bid-YTW : 5.33 % |

| MFC.PR.L | FixedReset | 2.45 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.65 Bid-YTW : 3.62 % |

| PWF.PR.A | Floater | 7.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 18.25 Evaluated at bid price : 18.25 Bid-YTW : 2.72 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| HSB.PR.D | Deemed-Retractible | 53,600 | Desjardins crossed 48,800 at 25.20. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-02-27 Maturity Price : 25.00 Evaluated at bid price : 25.23 Bid-YTW : -1.52 % |

| BMO.PR.R | FloatingReset | 41,100 | Desjardins crossed 40,000 at 24.40. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.39 Bid-YTW : 2.61 % |

| ENB.PF.E | FixedReset | 34,400 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 22.53 Evaluated at bid price : 23.50 Bid-YTW : 3.92 % |

| TD.PF.B | FixedReset | 34,071 | RBC crossed 25,800 at 24.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 23.17 Evaluated at bid price : 24.92 Bid-YTW : 3.08 % |

| SLF.PR.G | FixedReset | 27,418 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.06 Bid-YTW : 6.05 % |

| ENB.PR.H | FixedReset | 25,510 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-28 Maturity Price : 20.45 Evaluated at bid price : 20.45 Bid-YTW : 3.85 % |

| There were 28 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BNS.PR.A | FloatingReset | Quote: 23.46 – 24.80 Spot Rate : 1.3400 Average : 0.7555 YTW SCENARIO |

| BAM.PF.E | FixedReset | Quote: 23.80 – 24.80 Spot Rate : 1.0000 Average : 0.6821 YTW SCENARIO |

| BAM.PR.X | FixedReset | Quote: 20.45 – 21.11 Spot Rate : 0.6600 Average : 0.4161 YTW SCENARIO |

| IFC.PR.C | FixedReset | Quote: 24.31 – 24.85 Spot Rate : 0.5400 Average : 0.3497 YTW SCENARIO |

| GWO.PR.P | Deemed-Retractible | Quote: 26.10 – 26.68 Spot Rate : 0.5800 Average : 0.4214 YTW SCENARIO |

| BAM.PF.B | FixedReset | Quote: 24.45 – 24.95 Spot Rate : 0.5000 Average : 0.3541 YTW SCENARIO |