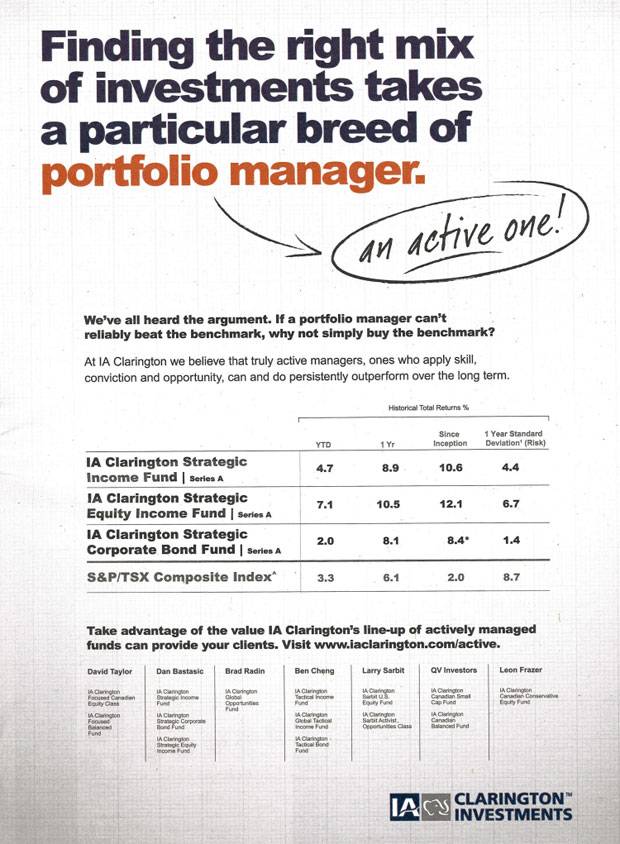

Credit where credit is due! The obnoxiously misleading advertisement for IA Clarington, which I discussed yesterday, has already been attacked by Dan Bortolotti in a post on Canadian Couch Potato dated 2013-11-11 and in a Moneysense post of the same date. Scooped!

Today’s FOMC statement made it clear that things are getting better, but only by Great Recession standards:

Information received since the Federal Open Market Committee met in March indicates that growth in economic activity has picked up recently, after having slowed sharply during the winter in part because of adverse weather conditions.

…

Beginning in May, the Committee will add to its holdings of agency mortgage-backed securities at a pace of $20 billion per month rather than $25 billion per month, and will add to its holdings of longer-term Treasury securities at a pace of $25 billion per month rather than $30 billion per month.

…

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that a highly accommodative stance of monetary policy remains appropriate. In determining how long to maintain the current 0 to 1/4 percent target range for the federal funds rate, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. The Committee continues to anticipate, based on its assessment of these factors, that it likely will be appropriate to maintain the current target range for the federal funds rate for a considerable time after the asset purchase program ends, especially if projected inflation continues to run below the Committee’s 2 percent longer-run goal, and provided that longer-term inflation expectations remain well anchored.When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

The Standard & Poor’s 500 Index increased 0.3 percent to 1,883.95 at 4 p.m. in New York, ending April with a 0.6 percent gain, its third straight monthly advance. The Dow climbed 45.47 points, or 0.3 percent, to 16,580.84, topping the previous closing record reached Dec. 31. The Nasdaq Composite Index added 0.3 percent, after an earlier drop of 0.8 percent. About 6.9 billion shares changed hands on U.S. exchanges, in line with the three-month average.

The war on markets is having an effect:

More than 30 traders from 11 firms have been fired, suspended, taken leaves of absence or retired since October, when regulators said they were investigating the market, according to data compiled by Bloomberg. London-based Barclays Plc (BARC) and Zurich-based UBS AG (UBSN) have been the worst-hit, each suspending at least half a dozen employees, the data show.

“That’s a considerable percentage of the workforce,” said Brad Bechtel, managing director at Faros Trading LLC in Stamford, Connecticut, who estimated the world’s largest banks have 80 to 160 voice traders for spot rates in the currencies market. “That explains the lack of liquidity in the market, and why what would normally be considered a small trade can actually push the market around more than normal.”

The US Treasury lost $11-billion on GM:

The U.S. Treasury’s bailout fund lost $11.2 billion on the rescue of General Motors Co. (GM) with the government’s exit of the largest U.S. automaker, a report said.

The total includes $826 million that the Treasury wrote off in March for its remaining claim in old GM, the special inspector general for the Troubled Asset Relief Program said in a report to Congress today. In December, the government had put the loss at about $10.5 billion on its $49.5 billion investment.

Fannie Mae will pay the Treasury Department $7.2 billion after posting an eighth straight quarterly profit, pushing total dividend payments above the $116.1 billion of aid it received after the financial crisis.

The mortgage-finance company, which is operating under federal conservatorship, had net income of $6.5 billion for the three months ended Dec. 31, Washington-based Fannie Mae (FNMA) said today in a regulatory filing. That brought earnings for 2013 to $84 billion, the highest ever for the 80-year-old firm.

Freddie Mac, the U.S.-owned mortgage financier, will return $10.4 billion to the Treasury Department next month, bringing total payments to about $10 billion above what it got in aid after the 2008 credit crisis.

The McLean, Virginia-based company had net income of $8.6 billion for the quarter ended Dec. 31 and a profit of $48.7 billion for all of 2013, according to a regulatory filing today, a profit largely driven by rising home prices. Freddie Mac, which was taken into federal conservatorship in 2008 along with larger rival Fannie Mae, earned $11 billion in 2012.

In fact, while Treasury realized a few scattered losses in investments in small firms, TARP has been a huge money-spinner for the US government … except for GM.

The Canadian preferred share market closed the month with a pop, as PerpetualDiscounts won 25bp, FixedResets were up 19bp and DeemedRetractibles gained 16bp. Volatility was average. Volume was high.

PerpetualDiscounts now yield 5.36%, equivalent to 6.97% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 4.5%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 245bp, a significant decline from the 255bp reported April 9.

And that’s it for another month – it’s been a good one!

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.6315 % | 2,403.9 |

| FixedFloater | 4.61 % | 3.85 % | 30,998 | 17.79 | 1 | 0.6351 % | 3,723.2 |

| Floater | 3.03 % | 3.15 % | 50,674 | 19.33 | 4 | -0.6315 % | 2,595.6 |

| OpRet | 4.35 % | -6.99 % | 34,165 | 0.09 | 2 | 0.0581 % | 2,698.9 |

| SplitShare | 4.79 % | 4.28 % | 66,781 | 4.20 | 5 | 0.1190 % | 3,096.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0581 % | 2,467.9 |

| Perpetual-Premium | 5.54 % | -7.99 % | 107,590 | 0.09 | 13 | 0.1148 % | 2,392.2 |

| Perpetual-Discount | 5.36 % | 5.36 % | 111,427 | 14.61 | 23 | 0.2502 % | 2,515.3 |

| FixedReset | 4.59 % | 3.54 % | 203,058 | 4.33 | 78 | 0.1861 % | 2,551.7 |

| Deemed-Retractible | 5.00 % | -3.88 % | 144,966 | 0.15 | 42 | 0.1632 % | 2,510.5 |

| FloatingReset | 2.66 % | 2.31 % | 193,398 | 4.08 | 5 | 0.3019 % | 2,493.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PWF.PR.A | Floater | -1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-04-30 Maturity Price : 19.21 Evaluated at bid price : 19.21 Bid-YTW : 2.72 % |

| TRP.PR.B | FixedReset | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-04-30 Maturity Price : 20.85 Evaluated at bid price : 20.85 Bid-YTW : 3.65 % |

| FTS.PR.J | Perpetual-Discount | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-04-30 Maturity Price : 23.82 Evaluated at bid price : 24.20 Bid-YTW : 4.97 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.Z | FixedReset | 196,624 | RBC crossed blocks of 100,000 and 46,900, both at 25.70. YTW SCENARIO Maturity Type : Call Maturity Date : 2019-05-24 Maturity Price : 25.00 Evaluated at bid price : 25.72 Bid-YTW : 3.33 % |

| TD.PR.K | FixedReset | 182,411 | TD crossed four blocks; 75,000 shares, 40,500 shares, 35,000 and 15,000, all at 25.30. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-07-31 Maturity Price : 25.00 Evaluated at bid price : 25.29 Bid-YTW : 1.65 % |

| BMO.PR.S | FixedReset | 173,726 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2019-05-25 Maturity Price : 25.00 Evaluated at bid price : 25.52 Bid-YTW : 3.58 % |

| TD.PR.Y | FixedReset | 129,863 | Nesbitt crossed 121,000 at 25.57. YTW SCENARIO Maturity Type : Call Maturity Date : 2018-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.57 Bid-YTW : 3.03 % |

| BNS.PR.M | Deemed-Retractible | 125,237 | Nesbitt crossed 119,500 at 25.92. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-05-30 Maturity Price : 25.75 Evaluated at bid price : 25.90 Bid-YTW : -2.69 % |

| NA.PR.S | FixedReset | 77,752 | Nesbitt crossed 46,900 at 25.78. YTW SCENARIO Maturity Type : Call Maturity Date : 2019-05-15 Maturity Price : 25.00 Evaluated at bid price : 25.66 Bid-YTW : 3.50 % |

| There were 47 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PF.A | FixedReset | Quote: 25.83 – 26.11 Spot Rate : 0.2800 Average : 0.1745 YTW SCENARIO |

| RY.PR.L | FixedReset | Quote: 26.33 – 26.64 Spot Rate : 0.3100 Average : 0.2060 YTW SCENARIO |

| GWO.PR.L | Deemed-Retractible | Quote: 25.96 – 26.24 Spot Rate : 0.2800 Average : 0.1872 YTW SCENARIO |

| RY.PR.C | Deemed-Retractible | Quote: 25.61 – 25.85 Spot Rate : 0.2400 Average : 0.1552 YTW SCENARIO |

| BAM.PF.B | FixedReset | Quote: 25.11 – 25.35 Spot Rate : 0.2400 Average : 0.1562 YTW SCENARIO |

| MFC.PR.A | OpRet | Quote: 25.73 – 25.94 Spot Rate : 0.2100 Average : 0.1300 YTW SCENARIO |