Click for Big

The big news today was the US unemployment numbers:

In the last four weeks, the number of unemployment claims has reached 22 million — roughly the net number of jobs created in a nine-and-a-half-year stretch that began after the last recession and ended with the pandemic’s arrival.

…

The emergency relief enacted by Congress expanded benefits and eligibility to plug holes in an unemployment program that differs from state to state. The act extended jobless benefits to freelancers, part-timers, recent hires and other workers usually ineligible, added a $600 weekly supplement and offered an extra 13 weeks of benefits. But the surge in applicants has tested the ability of state agencies to keep up with claims and payments.According to the Labor Department, 33 states are now able to pay out the additional $600. One is Washington, where the volume of jobless claims last week was seven times the record pace set in the last recession, said Nick Demerice, public affairs director for the state’s Employment Security Department. A 2017 software upgrade helped avoid the backlogs that have plagued other states, he said.

…

In Rhode Island, another state where the $600 payment is now available, technology remains a sticking point, said Scott R. Jensen, director of the state’s Department of Labor and Training. Its system is capable of handling a few thousand people daily who call or log in online. On Sunday, the department expects 90,000 people to try to access the system.

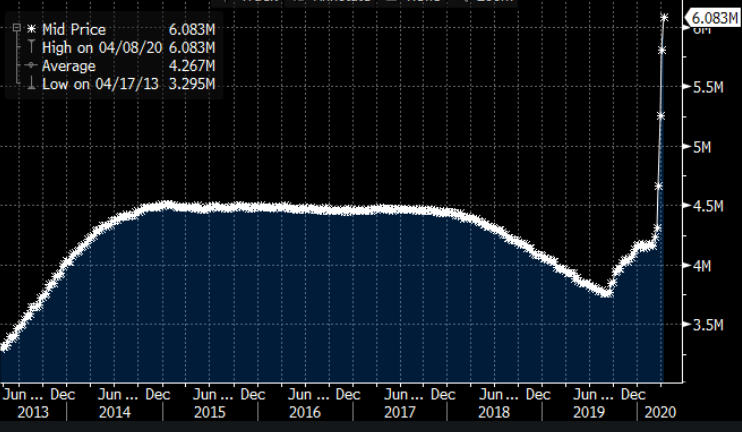

TXPR closed at 497.04, down 0.59% on the day, which was about 47bp higher than the day’s low, with a late recovery echoing yesterday’s. Volume today was 2.97-million, low in the context of the past thirty days.

CPD closed at 9.91, down 0.60% on the day. Volume was 152,770, near the median of the past 30 trading days.

ZPR closed at 7.66, down 0.78% on the day. Volume of 230,234 was second-lowest of the past 30 trading days, ahead of only April 15.

Five-year Canada yields were down 2bp to 0.43% today.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -2.8803 % | 1,345.6 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -2.8803 % | 2,469.2 |

| Floater | 5.71 % | 5.93 % | 41,073 | 14.01 | 4 | -2.8803 % | 1,423.0 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0119 % | 3,274.2 |

| SplitShare | 5.07 % | 6.28 % | 82,508 | 3.94 | 7 | -0.0119 % | 3,910.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0119 % | 3,050.8 |

| Perpetual-Premium | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2549 % | 2,761.1 |

| Perpetual-Discount | 6.07 % | 6.34 % | 89,700 | 13.47 | 35 | -0.2549 % | 2,961.5 |

| FixedReset Disc | 6.77 % | 5.69 % | 205,739 | 14.08 | 83 | -0.4785 % | 1,675.9 |

| Deemed-Retractible | 5.82 % | 6.16 % | 101,415 | 13.48 | 27 | -0.2439 % | 2,905.0 |

| FloatingReset | 3.33 % | 4.91 % | 29,732 | 13.99 | 4 | -0.7196 % | 1,695.3 |

| FixedReset Prem | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.4785 % | 2,317.7 |

| FixedReset Bank Non | 1.97 % | 4.59 % | 112,750 | 1.75 | 3 | -0.0277 % | 2,702.1 |

| FixedReset Ins Non | 7.24 % | 5.98 % | 128,654 | 13.35 | 22 | -0.6846 % | 1,642.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.A | FixedReset Disc | -15.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 9.90 Evaluated at bid price : 9.90 Bid-YTW : 6.93 % |

| TRP.PR.G | FixedReset Disc | -14.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 12.45 Evaluated at bid price : 12.45 Bid-YTW : 7.05 % |

| HSE.PR.A | FixedReset Disc | -7.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 4.97 Evaluated at bid price : 4.97 Bid-YTW : 11.31 % |

| BAM.PR.X | FixedReset Disc | -6.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 9.10 Evaluated at bid price : 9.10 Bid-YTW : 6.46 % |

| MFC.PR.F | FixedReset Ins Non | -5.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 8.01 Evaluated at bid price : 8.01 Bid-YTW : 5.98 % |

| PWF.PR.A | Floater | -4.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 8.18 Evaluated at bid price : 8.18 Bid-YTW : 5.32 % |

| TRP.PR.B | FixedReset Disc | -4.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 7.99 Evaluated at bid price : 7.99 Bid-YTW : 5.50 % |

| GWO.PR.N | FixedReset Ins Non | -4.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 8.52 Evaluated at bid price : 8.52 Bid-YTW : 5.25 % |

| SLF.PR.G | FixedReset Ins Non | -4.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 8.46 Evaluated at bid price : 8.46 Bid-YTW : 5.58 % |

| TRP.PR.C | FixedReset Disc | -3.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 8.21 Evaluated at bid price : 8.21 Bid-YTW : 6.15 % |

| TD.PF.D | FixedReset Disc | -3.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 14.51 Evaluated at bid price : 14.51 Bid-YTW : 5.64 % |

| MFC.PR.I | FixedReset Ins Non | -3.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 14.06 Evaluated at bid price : 14.06 Bid-YTW : 6.27 % |

| CM.PR.R | FixedReset Disc | -3.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 16.20 Evaluated at bid price : 16.20 Bid-YTW : 6.09 % |

| SLF.PR.J | FloatingReset | -2.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 8.53 Evaluated at bid price : 8.53 Bid-YTW : 5.05 % |

| HSE.PR.E | FixedReset Disc | -2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 8.75 Evaluated at bid price : 8.75 Bid-YTW : 12.52 % |

| CU.PR.I | FixedReset Disc | -2.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 22.19 Evaluated at bid price : 22.90 Bid-YTW : 4.94 % |

| SLF.PR.I | FixedReset Ins Non | -2.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 13.42 Evaluated at bid price : 13.42 Bid-YTW : 6.13 % |

| BAM.PR.C | Floater | -2.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 7.30 Evaluated at bid price : 7.30 Bid-YTW : 5.93 % |

| RY.PR.Q | FixedReset Disc | -2.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 22.60 Evaluated at bid price : 23.10 Bid-YTW : 5.50 % |

| BIP.PR.A | FixedReset Disc | -2.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 13.35 Evaluated at bid price : 13.35 Bid-YTW : 7.63 % |

| NA.PR.E | FixedReset Disc | -2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 14.00 Evaluated at bid price : 14.00 Bid-YTW : 5.94 % |

| BAM.PR.K | Floater | -2.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 7.27 Evaluated at bid price : 7.27 Bid-YTW : 5.96 % |

| PVS.PR.G | SplitShare | -2.08 % | YTW SCENARIO Maturity Type : Option Certainty Maturity Date : 2026-02-28 Maturity Price : 25.00 Evaluated at bid price : 23.50 Bid-YTW : 6.28 % |

| RY.PR.J | FixedReset Disc | -1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 5.42 % |

| MFC.PR.N | FixedReset Ins Non | -1.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 12.76 Evaluated at bid price : 12.76 Bid-YTW : 6.01 % |

| BNS.PR.G | FixedReset Disc | -1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 23.34 Evaluated at bid price : 23.82 Bid-YTW : 5.46 % |

| GWO.PR.H | Deemed-Retractible | -1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 19.45 Evaluated at bid price : 19.45 Bid-YTW : 6.30 % |

| PWF.PR.P | FixedReset Disc | -1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 9.00 Evaluated at bid price : 9.00 Bid-YTW : 5.78 % |

| POW.PR.B | Perpetual-Discount | -1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 20.85 Evaluated at bid price : 20.85 Bid-YTW : 6.47 % |

| BMO.PR.D | FixedReset Disc | -1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 16.23 Evaluated at bid price : 16.23 Bid-YTW : 5.87 % |

| PWF.PR.S | Perpetual-Discount | -1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 19.11 Evaluated at bid price : 19.11 Bid-YTW : 6.31 % |

| POW.PR.G | Perpetual-Discount | -1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 21.45 Evaluated at bid price : 21.76 Bid-YTW : 6.47 % |

| BAM.PF.G | FixedReset Disc | -1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 13.35 Evaluated at bid price : 13.35 Bid-YTW : 6.25 % |

| BNS.PR.H | FixedReset Disc | -1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 21.26 Evaluated at bid price : 21.53 Bid-YTW : 5.43 % |

| GWO.PR.R | Deemed-Retractible | -1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 19.59 Evaluated at bid price : 19.59 Bid-YTW : 6.19 % |

| POW.PR.D | Perpetual-Discount | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 19.55 Evaluated at bid price : 19.55 Bid-YTW : 6.45 % |

| TRP.PR.F | FloatingReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 9.43 Evaluated at bid price : 9.43 Bid-YTW : 5.94 % |

| W.PR.M | FixedReset Disc | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 21.68 Evaluated at bid price : 22.12 Bid-YTW : 5.90 % |

| BAM.PR.R | FixedReset Disc | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 11.10 Evaluated at bid price : 11.10 Bid-YTW : 6.33 % |

| BAM.PR.B | Floater | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 7.26 Evaluated at bid price : 7.26 Bid-YTW : 5.96 % |

| BMO.PR.W | FixedReset Disc | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 13.60 Evaluated at bid price : 13.60 Bid-YTW : 5.61 % |

| IFC.PR.A | FixedReset Ins Non | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 10.32 Evaluated at bid price : 10.32 Bid-YTW : 5.82 % |

| SLF.PR.H | FixedReset Ins Non | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 11.37 Evaluated at bid price : 11.37 Bid-YTW : 5.88 % |

| CU.PR.H | Perpetual-Discount | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 21.74 Evaluated at bid price : 22.10 Bid-YTW : 6.02 % |

| RY.PR.H | FixedReset Disc | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 14.00 Evaluated at bid price : 14.00 Bid-YTW : 5.37 % |

| MFC.PR.B | Deemed-Retractible | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 18.92 Evaluated at bid price : 18.92 Bid-YTW : 6.23 % |

| IFC.PR.G | FixedReset Ins Non | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 14.40 Evaluated at bid price : 14.40 Bid-YTW : 5.93 % |

| BMO.PR.F | FixedReset Disc | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 19.45 Evaluated at bid price : 19.45 Bid-YTW : 5.55 % |

| NA.PR.G | FixedReset Disc | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 15.32 Evaluated at bid price : 15.32 Bid-YTW : 5.87 % |

| CCS.PR.C | Deemed-Retractible | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 20.94 Evaluated at bid price : 20.94 Bid-YTW : 6.03 % |

| BIP.PR.B | FixedReset Disc | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 21.20 Evaluated at bid price : 21.20 Bid-YTW : 6.56 % |

| BIP.PR.E | FixedReset Disc | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 6.84 % |

| PWF.PR.T | FixedReset Disc | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 13.05 Evaluated at bid price : 13.05 Bid-YTW : 6.10 % |

| NA.PR.A | FixedReset Disc | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 21.81 Evaluated at bid price : 22.31 Bid-YTW : 5.74 % |

| W.PR.K | FixedReset Disc | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 21.61 Evaluated at bid price : 21.99 Bid-YTW : 5.99 % |

| BNS.PR.I | FixedReset Disc | 1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 16.44 Evaluated at bid price : 16.44 Bid-YTW : 5.04 % |

| BIP.PR.D | FixedReset Disc | 1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 19.31 Evaluated at bid price : 19.31 Bid-YTW : 6.55 % |

| BAM.PF.A | FixedReset Disc | 1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 15.25 Evaluated at bid price : 15.25 Bid-YTW : 6.17 % |

| HSE.PR.C | FixedReset Disc | 1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 8.60 Evaluated at bid price : 8.60 Bid-YTW : 12.02 % |

| CM.PR.Y | FixedReset Disc | 1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 19.75 Evaluated at bid price : 19.75 Bid-YTW : 5.54 % |

| PVS.PR.H | SplitShare | 1.94 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2027-02-28 Maturity Price : 25.00 Evaluated at bid price : 23.70 Bid-YTW : 5.75 % |

| MFC.PR.J | FixedReset Ins Non | 2.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 14.30 Evaluated at bid price : 14.30 Bid-YTW : 5.97 % |

| BIP.PR.F | FixedReset Disc | 2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 6.38 % |

| TRP.PR.K | FixedReset Disc | 3.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 22.38 Evaluated at bid price : 22.67 Bid-YTW : 5.47 % |

| MFC.PR.M | FixedReset Ins Non | 3.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 13.10 Evaluated at bid price : 13.10 Bid-YTW : 5.98 % |

| CU.PR.C | FixedReset Disc | 4.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 14.90 Evaluated at bid price : 14.90 Bid-YTW : 4.98 % |

| BIP.PR.C | FixedReset Disc | 4.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 21.05 Evaluated at bid price : 21.05 Bid-YTW : 6.42 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TRP.PR.H | FloatingReset | 263,247 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 8.11 Evaluated at bid price : 8.11 Bid-YTW : 4.91 % |

| RY.PR.J | FixedReset Disc | 154,673 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 5.42 % |

| MFC.PR.J | FixedReset Ins Non | 130,375 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 14.30 Evaluated at bid price : 14.30 Bid-YTW : 5.97 % |

| IAF.PR.I | FixedReset Ins Non | 120,625 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 14.26 Evaluated at bid price : 14.26 Bid-YTW : 6.21 % |

| CM.PR.R | FixedReset Disc | 98,095 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 16.20 Evaluated at bid price : 16.20 Bid-YTW : 6.09 % |

| IFC.PR.A | FixedReset Ins Non | 75,077 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-04-16 Maturity Price : 10.32 Evaluated at bid price : 10.32 Bid-YTW : 5.82 % |

| There were 42 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TD.PF.M | FixedReset Disc | Quote: 19.77 – 24.65 Spot Rate : 4.8800 Average : 4.1270 YTW SCENARIO |

| TRP.PR.A | FixedReset Disc | Quote: 9.90 – 12.01 Spot Rate : 2.1100 Average : 1.3898 YTW SCENARIO |

| BIP.PR.E | FixedReset Disc | Quote: 18.50 – 20.75 Spot Rate : 2.2500 Average : 1.7793 YTW SCENARIO |

| RY.PR.P | Perpetual-Discount | Quote: 23.76 – 24.99 Spot Rate : 1.2300 Average : 0.7674 YTW SCENARIO |

| CM.PR.T | FixedReset Disc | Quote: 17.98 – 19.00 Spot Rate : 1.0200 Average : 0.6260 YTW SCENARIO |

| TD.PF.D | FixedReset Disc | Quote: 14.51 – 15.70 Spot Rate : 1.1900 Average : 0.8172 YTW SCENARIO |