The New York Fed has released a paper by Andreas Fuster and James Vickery titled Regulation and Risk Shuffling in Bank Securities Portfolios:

Bank capital requirements are based on a mix of market values and book values. We investigate the effects of a policy change that ties regulatory capital to the market value of the “available-for-sale” investment securities portfolio for some banking organizations. Our analysis is based on security-level data on individual bank portfolios matched to bond characteristics. We find little clear evidence that banks respond by reducing the riskiness of their securities portfolios, although there is some evidence of a greater use of derivatives to hedge securities exposures. Instead, banks respond by reclassifying securities to mitigate the effects of the policy change. This shift is most pronounced for securities with high levels of interest rate risk.

…

Quantitatively more importantly, we found evidence that treated banks respond by actively reshuffling their portfolios, and in particular classifying risky securities as “held to maturity” (HTM) rather than available for sale (AFS). The use of detailed security-level data allow us to control in a precise way for security characteristics – most finely by including both BHC fixed effects and a vector of CUSIP-by-calendar quarter fixed effects in our specifications. This is an important feature of our analysis, since it allows us to isolate the effects of the accounting classification decision for a given security from changes in the composition in investment securities portfolios which was occurring during this period. In these specifications, our preferred point estimates suggest that a security is 20 percentage points more likely to be classified as HTM rather than AFS if owned by a BHC subject to the AOCI rule (measured on a fully phased-in basis), or 38 percentage points measured on a weighted basis. For both agency MBS and Treasury securities, we find that these effects are concentrated among bonds with higher duration.

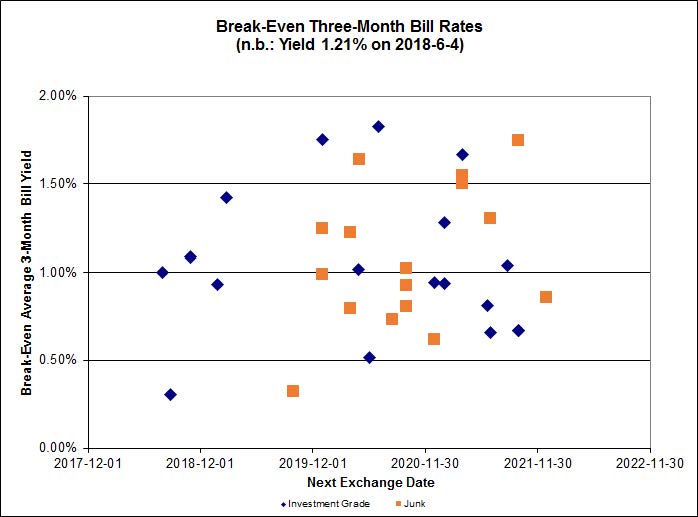

It’s a common fallacy – you will often find people arguing vociferously that a five year GIC is less risky than a five year bond because the reported price doesn’t change and the holder doesn’t intend to sell it anyway. Crazy.

In another paper released today, Richard Crump, Domenico Giannone, and Sean Hundtofte claim that volatility has meaning in a paper titled Changing Risk-Return Profiles:

We show that realized volatility, especially the realized volatility of financial sector stock returns, has strong predictive content for the future distribution of market returns. This is a robust feature of the last century of U.S. data and, most importantly, can be exploited in real time. Current realized volatility has the most information content on the uncertainty of future returns, whereas it has only limited content about the location of the future return distribution. When volatility is low, the predicted distribution of returns is less dispersed and probabilistic forecasts are sharper. Given this finding on the importance of financial sector volatility not just to financial equity return uncertainty but to the broader market, we test for changes in the realized volatility of banks over a $50 billion threshold associated with more stringent Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank) requirements. We find that the equity volatility of these large banks is differentially lower by 9 percentage points after Dodd-Frank compared to pre-crisis levels, controlling for changes over the same period for all banks and all large firms.

…

Our paper is most closely related to Cenesizoglu and Timmermann (2008) who study whether economic and financial variables can help improve prediction of the quantiles of the return distribution. Cenesizoglu and Timmermann (2008) also find evidence of predictive power especially in the upper tail of the return distribution. Our paper is also related to Massacci (2015) who evaluates the accuracy of density forecasts but restricts the economic and financial variables to predict the location of the distribution only. Durham and Geweke (2014) predict higher-frequency, daily returns allowing for realized intraday volatility and option-implied volatility but restrict these variables to predict the scale of the distribution only.Our paper is also related to those papers that investigate interactions between financial crises (high periods of market volatility) and equity returns. For example, Baron and Xiong (2017) ex-amine changes in skew of bank equity returns in response to changes in economic leverage (bank credit/GDP). Moreira and Muir (2017) look at the returns of a market portfolio managed by lagged volatility, finding investors are not compensated for risk in periods of lagged high volatility. Similarly, when we examine the distribution of aggregate returns conditional on realized volatility we find no predictability in the average return, but do find predictability in the risk to holding the

market portfolio (either in terms of variance at short horizon, or skew at longer horizons), indicating a breakdown in a risk-return tradeoff. Adrian et al. (2017b) document a strongly nonlinear dependence of stock and bond returns on past equity market volatility as measured by the VIX with expected stock returns increasing for stocks when volatility increases from moderate to high levels.

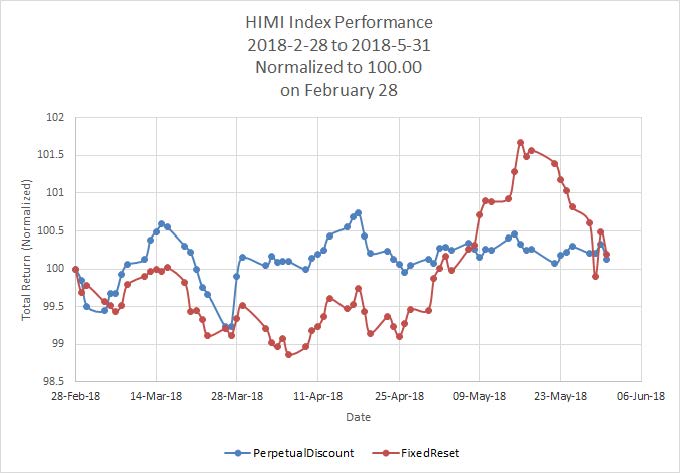

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1650 % | 3,024.7 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1650 % | 5,550.1 |

| Floater | 3.33 % | 3.52 % | 69,860 | 18.49 | 4 | -0.1650 % | 3,198.6 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1038 % | 3,162.0 |

| SplitShare | 4.65 % | 4.81 % | 77,123 | 5.00 | 5 | -0.1038 % | 3,776.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1038 % | 2,946.3 |

| Perpetual-Premium | 5.62 % | -7.38 % | 58,754 | 0.08 | 9 | 0.0131 % | 2,877.2 |

| Perpetual-Discount | 5.39 % | 5.54 % | 64,902 | 14.52 | 26 | 0.1779 % | 2,958.0 |

| FixedReset | 4.31 % | 4.71 % | 166,698 | 5.66 | 106 | -0.1117 % | 2,541.3 |

| Deemed-Retractible | 5.19 % | 5.78 % | 70,434 | 5.56 | 27 | 0.0535 % | 2,943.8 |

| FloatingReset | 3.13 % | 3.83 % | 35,795 | 3.45 | 9 | -0.0449 % | 2,796.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.X | FixedReset | -1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-06-15 Maturity Price : 18.36 Evaluated at bid price : 18.36 Bid-YTW : 5.02 % |

| BAM.PF.B | FixedReset | -1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-06-15 Maturity Price : 22.80 Evaluated at bid price : 23.42 Bid-YTW : 5.04 % |

| IFC.PR.A | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.55 Bid-YTW : 7.79 % |

| PWF.PR.T | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-06-15 Maturity Price : 23.59 Evaluated at bid price : 24.26 Bid-YTW : 4.65 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| EMA.PR.H | FixedReset | 97,100 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-06-15 Maturity Price : 23.19 Evaluated at bid price : 25.11 Bid-YTW : 4.80 % |

| NA.PR.G | FixedReset | 65,575 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-06-15 Maturity Price : 23.13 Evaluated at bid price : 24.97 Bid-YTW : 4.85 % |

| TD.PF.I | FixedReset | 55,300 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.20 Bid-YTW : 4.46 % |

| NA.PR.C | FixedReset | 41,570 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-11-15 Maturity Price : 25.00 Evaluated at bid price : 24.98 Bid-YTW : 4.59 % |

| BMO.PR.W | FixedReset | 31,300 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-06-15 Maturity Price : 22.60 Evaluated at bid price : 23.02 Bid-YTW : 4.70 % |

| RY.PR.Z | FixedReset | 30,177 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-06-15 Maturity Price : 22.93 Evaluated at bid price : 23.50 Bid-YTW : 4.62 % |

| There were 18 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PF.G | FixedReset | Quote: 24.05 – 24.57 Spot Rate : 0.5200 Average : 0.3215 YTW SCENARIO |

| BAM.PF.E | FixedReset | Quote: 23.25 – 23.68 Spot Rate : 0.4300 Average : 0.3025 YTW SCENARIO |

| GWO.PR.Q | Deemed-Retractible | Quote: 23.60 – 23.97 Spot Rate : 0.3700 Average : 0.2459 YTW SCENARIO |

| IFC.PR.A | FixedReset | Quote: 19.55 – 19.85 Spot Rate : 0.3000 Average : 0.1978 YTW SCENARIO |

| IFC.PR.F | Deemed-Retractible | Quote: 24.80 – 25.22 Spot Rate : 0.4200 Average : 0.3247 YTW SCENARIO |

| BAM.PF.F | FixedReset | Quote: 24.41 – 24.80 Spot Rate : 0.3900 Average : 0.2950 YTW SCENARIO |