Brookfield Infrastructure has announced:

that it has agreed to issue 8,000,000 Cumulative Class A Preferred Limited Partnership Units, Series 9 (“Series 9 Preferred Units”) on a bought deal basis to a syndicate of underwriters led by CIBC Capital Markets, BMO Capital Markets, RBC Capital Markets, Scotiabank, and TD Securities Inc. The Series 9 Preferred Units will be issued at a price of $25.00 per unit, for gross proceeds of $200,000,000. Holders of the Series 9 Preferred Units will be entitled to receive a cumulative quarterly fixed distribution at a rate of 5.00% annually for the initial period ending March 31, 2023. Thereafter, the distribution rate will be reset every five years at a rate equal to the greater of: (i) the 5-year Government of Canada bond yield plus 3.00%, and (ii) 5.00%. The Series 9 Preferred Units are redeemable on or after March 31, 2023.

Holders of the Series 9 Preferred Units will have the right, at their option, to reclassify their Series 9 Preferred Units into Cumulative Class A Preferred Limited Partnership Units, Series 10 (“Series 10 Preferred Units”), subject to certain conditions, on March 31, 2023 and on March 31 every five years thereafter. Holders of Series 10 Preferred Units will be entitled to receive a cumulative quarterly floating distribution at a rate equal to the 90-day Canadian Treasury Bill yield plus 3.00%.

Brookfield Infrastructure has granted the underwriters an option, exercisable until 48 hours prior to closing, to purchase up to an additional 2,000,000 Series 9 Preferred Units which, if exercised, would increase the gross offering size to $250,000,000.

The Series 9 Preferred Units will be offered in all provinces and territories of Canada by way of a supplement to Brookfield Infrastructure’s existing short form base shelf prospectus.

Brookfield Infrastructure intends to use the net proceeds of the issue of the Series 9 Preferred Units to fund a growing backlog of committed organic growth capital expenditure projects and an active pipeline of new investment opportunities, and for general working capital purposes. The offering of Series 9 Preferred Units is expected to close on or about January 23, 2018.

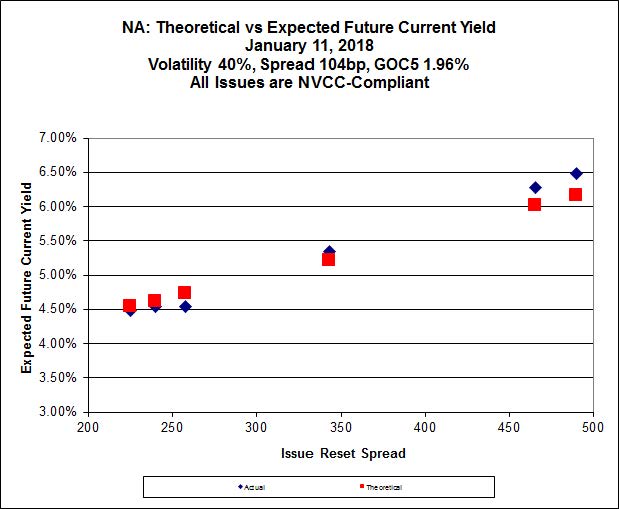

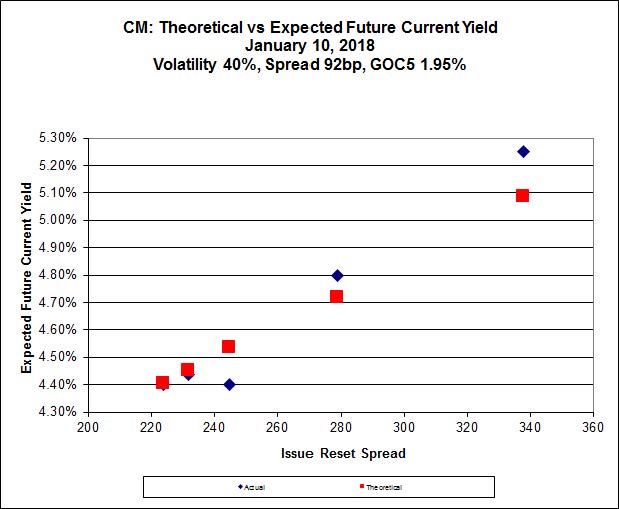

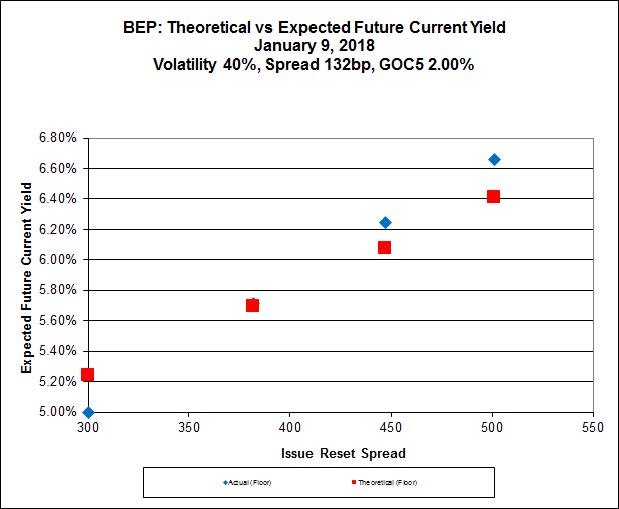

This issue looks quite expensive to me, according to Implied Volatility Analysis:

Click for Big

Well, it’s starting to get monotonous, but we see in this chart many of the same features we saw when reviewing last week’s BEP issue, the CM issue and NA issue:

- The curve is very steep, with Implied Volatility equal to 40% (a ridiculously large figure), and

- The extant issues are trading relatively near to, or well above par

The ludicrously high figure of Implied Volatility is something I take to mean that the underlying assumption of the Black-Scholes model, that of no directionality of prices, is not accepted by the market; the market seems to be taking the view that since things seem rosy now, they will always be rosy and everything will trade near par in the future.

I balk at ascribing a 100% probability to this outcome. There may still be a few old geezers amongst the Assiduous Readers of this blog who can still (faintly) remember the Great Bear Market of 2014-16, in which quite a few similar assumptions made earlier turned out to be slightly inaccurate.

For the long term, I suggest that any change in the slope of the curve will be a flattening, with a very high degree of confidence. This will imply that the higher-spread issues will outperform the lower-spread issues.

All told, though, I have no hesitation in slapping an ‘Expensive’ label on this issue – according to the Implied Volatility analysis shown above, the theoretical price of the new issue is 23.50. Mind you, the Implied Volatility cap rate of 40% is arbitrary; perhaps if I allowed 50% or so the new issue would sit on the curve … but in that case, Implied Volatility has become a completely arbitrary meaningless number.