Turnover declined slightly to about 7% in November.

There is extreme segmentation in the marketplace, with OSFI’s NVCC rule changes in February 2011 having had the effect of splitting the formerly relatively homogeneous Straight Perpetual class of preferreds into three parts:

- Unaffected Straight Perpetuals

- DeemedRetractibles explicitly subject to the rules (banks)

- DeemedRetractibles considered by me, but not (yet!) by the market, to be likely to be explicitly subject to the rules in the future (insurers and insurance holding companies)

This segmentation, and the extreme valuation differences between the segments, has cut down markedly on the opportunities for trading.

To make this more clear, it used to be that there were 70-odd Straight Perpetuals and I was more or less indifferent as to which ones I owned (subject, of course, to issuer concentration concerns and other risk management factors). Thus, if any one of these 70 were to go down in price by – say – $0.25, I would quite often have something in inventory that I’d be willing to swap for it. The segmentation means that I am no longer indifferent; in addition to checking the valuation of a potential buy to other Straights, I also have to check its peer group. This cuts down on the potential for trading.

And, of course, the same segmentation has the same effect on trading opportunities between FixedReset issues.

There is no real hope that this situation will be corrected in the near-term. OSFI has indicated that the long-promised “Draft Definition of Capital” for insurers will not be issued “for public consultation in late 2012 or early 2013”, as they fear that it might encourage speculation in the marketplace. It is not clear why OSFI is so afraid of informed speculation, since the constant speculation in the marketplace is currently less informed than it would be with a little bit of regulatory clarity. While the framework has been updated, the modifications focus on the amount of capital required, not the required characteristics of that capital. However, OSFI has recently indicated that it would support a mechanism similar to the NVCC rule for banks, so we may see some developments as the IAIS deliberations regarding insurance capital continue.

As a result of this delay, I have extended the Deemed Maturity date for insurers and insurance holding companies by three years (to 2025-1-31), in the expectation that when OSFI finally does provide clarity, they will allow the same degree of lead-in time for these companies as they did for banks. This had a major effect on the durations of preferred shares subject to the change but, fortunately, not much on their calculated yields as most of these issues were either trading near par when the change was made or were trading at sufficient premium that a par call was expected on economic grounds. However, with the declines in the market over the past nine months, the expected capital gain on redemption of the insurance-issued DeemedRetractibles has become an important component of the calculated yield.

Due to the footdragging by OSFI, I will be extending the DeemedMaturity date for insurance issues by another few years in the near future.

Sectoral distribution of the MAPF portfolio on November 30 was as follows:

| MAPF Sectoral Analysis 2017-11-30 | |||

| HIMI Indices Sector | Weighting | YTW | ModDur |

| Ratchet | 0% | N/A | N/A |

| FixFloat | 0% | N/A | N/A |

| Floater | 0% | N/A | N/A |

| OpRet | 0% | N/A | N/A |

| SplitShare | 8.3% | 4.60% | 5.42 |

| Interest Rearing | 0% | N/A | N/A |

| PerpetualPremium | 0% | N/A | N/A |

| PerpetualDiscount | 11.5% | 5.24% | 15.05 |

| Fixed-Reset | 59.5% | 5.99% | 8.24 |

| Deemed-Retractible | 2.1% | 5.71% | 5.91 |

| FloatingReset | 7.9% | 7.85% | 6.39 |

| Scraps (Various) | 9.7% | 6.13% | 12.44 |

| Cash | +0.9% | 0.00% | 0.00 |

| Total | 100% | 5.89% | 8.92 |

| Totals and changes will not add precisely due to rounding. Cash is included in totals with duration and yield both equal to zero. | |||

| DeemedRetractibles are comprised of all Straight Perpetuals (both PerpetualDiscount and PerpetualPremium) issued by BMO, BNS, CM, ELF, GWO, HSB, IAG, MFC, NA, RY, SLF and TD, which are not exchangable into common at the option of the company. These issues are analyzed as if their prospectuses included a requirement to redeem at par on or prior to 2022-1-31 (banks) or 2025-1-3 (insurers and insurance holding companies), in addition to the call schedule explicitly defined. See OSFI Does Not Grandfather Extant Tier 1 Capital, CM.PR.D, CM.PR.E, CM.PR.G: NVCC Status Confirmed and the January, February, March and June, 2011, editions of PrefLetter for the rationale behind this analysis.

Note that the estimate for the time this will become effective for insurers and insurance holding companies was extended by three years in April 2013, due to the delays in OSFI’s providing clarity on the issue. |

|||

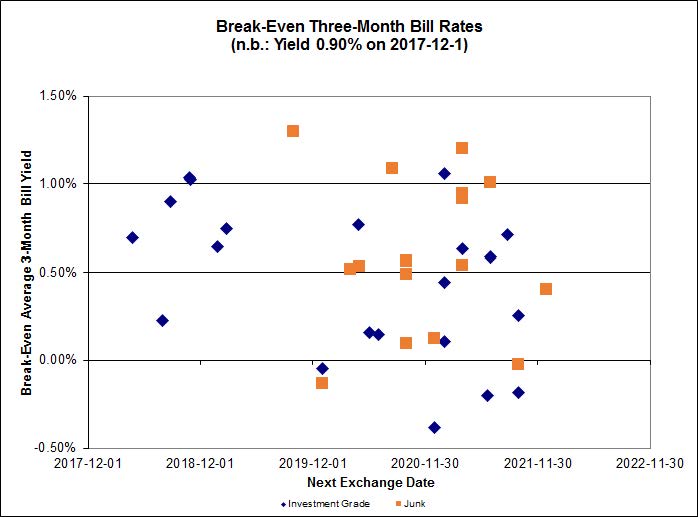

| Calculations of resettable instruments are performed assuming a constant GOC-5 rate of 1.62% and a constant 3-Month Bill rate of 0.87% | |||

The “total” reflects the un-leveraged total portfolio (i.e., cash is included in the portfolio calculations and is deemed to have a duration and yield of 0.00.). MAPF will often have relatively large cash balances, both credit and debit, to facilitate trading. Figures presented in the table have been rounded to the indicated precision.

Credit distribution is:

| MAPF Credit Analysis 2017-11-30 | ||

| DBRS Rating | Weighting | |

| Pfd-1 | 0 | |

| Pfd-1(low) | 0 | |

| Pfd-2(high) | 42.8% | |

| Pfd-2 | 31.4% | |

| Pfd-2(low) | 15.3% | |

| Pfd-3(high) | 2.0% | |

| Pfd-3 | 4.3% | |

| Pfd-3(low) | 2.8% | |

| Pfd-4(high) | 0% | |

| Pfd-4 | 0% | |

| Pfd-4(low) | 0% | |

| Pfd-5(high) | 0.6% | |

| Pfd-5 | 0.0% | |

| Cash | +0.9% | |

| Totals will not add precisely due to rounding. | ||

| The fund holds a position in AZP.PR.C, which is rated P-5(high) by S&P and is unrated by DBRS; it is included in the Pfd-5(high) total. | ||

| A position held in INE.PR.A is not rated by DBRS, but has been included as “Pfd-3” in the above table on the basis of its S&P rating of P-3. | ||

Liquidity Distribution is:

| MAPF Liquidity Analysis 2017-11-30 | |

| Average Daily Trading | Weighting |

| <$50,000 | 13.0% |

| $50,000 – $100,000 | 42.8% |

| $100,000 – $200,000 | 39.4% |

| $200,000 – $300,000 | 1.0% |

| >$300,000 | 3.6% |

| Cash | +0.2% |

| Totals will not add precisely due to rounding. | |

MAPF is, of course, Malachite Aggressive Preferred Fund, a “unit trust” managed by Hymas Investment Management Inc. Further information and links to performance, audited financials and subscription information are available the fund’s web page. The fund may be purchased either directly from Hymas Investment Management or through a brokerage account at Odlum Brown Limited. A “unit trust” is like a regular mutual fund, but is sold by offering memorandum rather than prospectus. This is cheaper, but means subscription is restricted to “accredited investors” (as defined by the Ontario Securities Commission). Fund past performances are not a guarantee of future performance. You can lose money investing in MAPF or any other fund.

A similar portfolio composition analysis has been performed on the Claymore Preferred Share ETF (symbol CPD) (and other funds) as of July 31, 2017, and published in the August, 2017, PrefLetter. It is fair to say:

- MAPF credit quality is much better

- MAPF liquidity is lower

- MAPF Yield is higher

- Weightings

- MAPF has similar exposure to Straight Perpetuals

- Much more exposed to PerpetualDiscounts

- Much less exposed to DeemedRetractibles

- A little less exposed to PerpetualPremiums

- Neither portfolio is exposed to Operating Retractibles (there aren’t too many of those any more!)

- MAPF is more exposed to SplitShares

- MAPF is a little less exposed to FixFloat / Floater / Ratchet

- MAPF is a little higher weighted in FixedResets, but has a greater emphasis on lower-spread issues

f

- MAPF has similar exposure to Straight Perpetuals