TransAlta Corporation has announced:

that it is not proceeding with the previously announced transaction pursuant to which all the currently outstanding first preferred shares in the capital of the Corporation would be exchanged for shares in a single new series of cumulative redeemable minimum rate reset first preferred shares in the capital of the Corporation. In light of the decision to terminate such transaction, the special meetings of preferred shareholders of the Corporation scheduled for February 16, 2017 have been cancelled.

This is wonderful news – it was a horrible plan, at least so far as investors were concerned; it was only good for the company and bank employees hoping to earn sleaze fees for a favourable vote.

This follows previous posts on this topic:

- TA Proposes Sleazy Exchange Offer

- TransAlta plays the Grinch with its preferred share holders

- TransAlta Nudges TA.PR.D Offer; Hopes To Pay Sleaze Fees To Banks

- TransAlta pref shareholders not happy with consolidation plan

- TransAlta Corp takes to the airwaves to spread the advantages of its pref share consolidation

Affected issues are TA.PR.D, TA.PR.E, TA.PR.F, TA.PR.H and TA.PR.J.

There was high volume but little price change today after the announcement:

| Market Movement in TA Issues 2017-2-10 |

||||

| Ticker | Bid 2017-2-9 |

Bid 2017-2-10 |

Change | Volume |

| TA.PR.D | 12.89 | 13.00 | +0.85% | 785,355 |

| TA.PR.E | 13.09 | 12.70 | -2.98% | 121,800 |

| TA.PR.F | 16.95 | 16.88 | -0.30% | 320,371 |

| TA.PR.H | 18.88 | 18.70 | -0.95% | 393,853 |

| TA.PR.J | 19.89 | 19.80 | -0.45% | 120,022 |

TransAlta cancels a planned preferred share swap because of investor push back

Barry Critchley was kind enough to quote me in his piece TransAlta cancels a planned preferred share swap because of investor push back:

“It is a good day for shareholders. We don’t always do what the banks tell us to do,” said James Hymas, portfolio manager at Hymas Investment Management and the publisher of the PrefBlog. CIBC World Markets was TransAlta’s financial adviser while PWC provided a fairness opinion.

When TransAlta announced the plan in late December, Hymas said on the blog: “This is a rotten deal for the preferred shareholders, so rotten that we may call it a sleazy attempt by the company to pull the wool over the eyes of unsophisticated retail investors.”

Reached Friday, Hymas reiterated that it “was a bad deal. I suspect the early returns by shareholders combined with comments made to their investor relations department convinced them that it was not going to pass. Rather than be embarrassed, my guess is that they decided to cancel the deal.”

Hymas offered TransAlta, whose common share holders received a major dividend cut one year back, some advice: Get to work on improving the credit rating and spend less time on financial engineering. Last March DBRS changed the trends of all TransAlta’s long-term debt ratings – as well as on its preferred share ratings – to negative from stable.

There are also some amusing quotes from a portfolio manager who liked the deal so much, he’s willing to hide under his bed with the light turned off and say so anonymously:

The manager had little time for the view that holders were being “compromised” because they were not being offered full value, or $25 per share.

“That’s a fiction. They are perpetual securities and worth what they are worth. It’s not like a piece of debt where eventually they owe you the principal,” he added.

I hadn’t actually heard anybody say the holders were being compromised because they were not being offered full value. Perhaps the fact that all this guy has is a straw-man argument explains his anonymity..

This follows previous posts on this topic:

- TA Proposes Sleazy Exchange Offer

- TransAlta plays the Grinch with its preferred share holders

- TransAlta Nudges TA.PR.D Offer; Hopes To Pay Sleaze Fees To Banks

- TransAlta pref shareholders not happy with consolidation plan

- TransAlta Corp takes to the airwaves to spread the advantages of its pref share consolidation

- TA Withdraws Plan of Arrangement

Affected issues are TA.PR.D, TA.PR.E, TA.PR.F, TA.PR.H and TA.PR.J.

February 10, 2017

Data released Friday show a labor market that’s finally beginning to create new jobs, while at the same time offering little evidence that’s translating into higher incomes for workers as wage growth and hours worked slump.

…

Still, wage data showed underlying weakness that may complicate matters for Bank of Canada policy makers. Average hourly wages for permanent employees increased 1 percent in January from a year earlier, the slowest pace of growth since at least 2003. Hours worked also fell 0.8 percent from a year earlier.

…

Most of the gains came from two categories — a 20,500 increase in finance, insurance, real estate and leasing and another 16,400 in business, building and other support services — and for men aged 25 to 54, with the increase of about 30,000 the largest in more than two years.It was split between 32,400 part-time positions and 15,800 full-time jobs.

There’s a fascinating story about Nav Sarao, the Flash Crash scapegoat, that shows once again that trading and investment management are two completely different things:

After four months of dead ends, his legal team struck a deal with the authorities: If the U.S. Justice Department and the Commodity Futures Trading Commission agreed not to oppose a reduction in bail to 50,000 pounds, the firm would act as a bounty hunter, taking on responsibility for tracking down the missing millions on the condition that its fees be paid if it did.

They were going down a rabbit hole. A review of Sarao’s investments from 2005 to the present day, based on dozens of interviews and thousands of pages of documents, reveals another twist in an already remarkable story. Navinder Sarao, the trading savant accused of sabotaging the world’s financial markets from his bedroom, may himself have been the naïve victim of what his lawyers portray as a series of cons that stripped him of almost every cent he earned.

Sarao declined to comment for this article. His lawyer, Roger Burlingame of Kobre & Kim in London, told a U.S. judge in November that all of the defendant’s assets “have been stolen.” Sarao invested in ventures from which he, the law firm and the CFTC had been unable to recover the funds, Burlingame said. “Basically, he has some extraordinary abilities with respect to pattern recognition and certain sorts of mathematical abilities, but he has some fairly severe social limitations.”

The story also illustrates the regulatory penchant for going after the easy marks for trivial infringements of arbitrary rules while ignoring the real crooks in the industry.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1603 % | 1,997.2 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1603 % | 3,664.7 |

| Floater | 3.78 % | 3.96 % | 47,260 | 17.47 | 4 | 0.1603 % | 2,112.0 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1079 % | 2,970.2 |

| SplitShare | 4.70 % | 4.51 % | 56,174 | 4.15 | 4 | 0.1079 % | 3,547.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1079 % | 2,767.6 |

| Perpetual-Premium | 5.44 % | -1.70 % | 77,668 | 0.09 | 16 | 0.0245 % | 2,727.3 |

| Perpetual-Discount | 5.16 % | 5.18 % | 107,437 | 15.10 | 22 | 0.2978 % | 2,913.1 |

| FixedReset | 4.49 % | 4.16 % | 223,928 | 6.74 | 97 | -0.1447 % | 2,289.5 |

| Deemed-Retractible | 5.03 % | 0.13 % | 131,640 | 0.14 | 31 | 0.1980 % | 2,842.2 |

| FloatingReset | 2.50 % | 3.16 % | 47,455 | 4.69 | 9 | 0.1837 % | 2,445.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| IFC.PR.C | FixedReset | -1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.43 Bid-YTW : 5.84 % |

| TRP.PR.E | FixedReset | -1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-10 Maturity Price : 21.37 Evaluated at bid price : 21.37 Bid-YTW : 4.18 % |

| PWF.PR.P | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-10 Maturity Price : 15.51 Evaluated at bid price : 15.51 Bid-YTW : 4.24 % |

| CU.PR.I | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-01 Maturity Price : 25.00 Evaluated at bid price : 26.30 Bid-YTW : 2.99 % |

| BNS.PR.Z | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.19 Bid-YTW : 4.72 % |

| SLF.PR.D | Deemed-Retractible | 1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.29 Bid-YTW : 6.32 % |

| CU.PR.C | FixedReset | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-10 Maturity Price : 21.51 Evaluated at bid price : 21.51 Bid-YTW : 4.07 % |

| MFC.PR.O | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-06-19 Maturity Price : 25.00 Evaluated at bid price : 27.08 Bid-YTW : 3.75 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BAM.PF.F | FixedReset | 46,385 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-10 Maturity Price : 22.81 Evaluated at bid price : 23.56 Bid-YTW : 4.27 % |

| TRP.PR.K | FixedReset | 36,821 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-05-31 Maturity Price : 25.00 Evaluated at bid price : 25.76 Bid-YTW : 4.24 % |

| RY.PR.J | FixedReset | 36,300 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-10 Maturity Price : 22.35 Evaluated at bid price : 22.91 Bid-YTW : 4.11 % |

| RY.PR.Z | FixedReset | 35,585 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-10 Maturity Price : 21.06 Evaluated at bid price : 21.06 Bid-YTW : 4.02 % |

| BIP.PR.D | FixedReset | 34,166 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-10 Maturity Price : 23.20 Evaluated at bid price : 25.13 Bid-YTW : 4.90 % |

| TRP.PR.E | FixedReset | 32,587 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-10 Maturity Price : 21.37 Evaluated at bid price : 21.37 Bid-YTW : 4.18 % |

| There were 34 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| VNR.PR.A | FixedReset | Quote: 21.00 – 21.50 Spot Rate : 0.5000 Average : 0.3742 YTW SCENARIO |

| IFC.PR.C | FixedReset | Quote: 21.43 – 21.75 Spot Rate : 0.3200 Average : 0.1989 YTW SCENARIO |

| HSE.PR.A | FixedReset | Quote: 14.94 – 15.35 Spot Rate : 0.4100 Average : 0.2983 YTW SCENARIO |

| BAM.PR.T | FixedReset | Quote: 18.80 – 19.10 Spot Rate : 0.3000 Average : 0.2005 YTW SCENARIO |

| CU.PR.I | FixedReset | Quote: 26.30 – 26.67 Spot Rate : 0.3700 Average : 0.2763 YTW SCENARIO |

| CU.PR.C | FixedReset | Quote: 21.51 – 22.00 Spot Rate : 0.4900 Average : 0.4030 YTW SCENARIO |

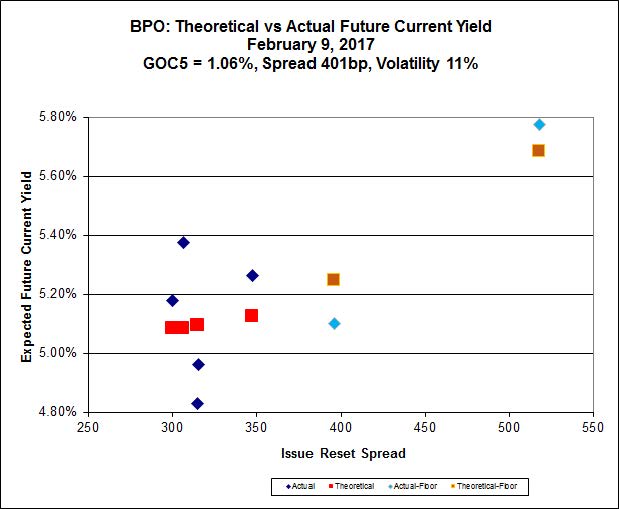

New Issue: BPO FixedReset, 5.10%+396M510

Brookfield Office Properties has announced (but not on their website yet, as far as I can tell given their idiotic, but ever-so-cool website design):

Brookfield Office Properties Inc., a subsidiary of Brookfield Property Partners L.P., announced today that it has agreed to issue to a syndicate of underwriters led by Scotiabank, CIBC Capital Markets, RBC Capital Markets and TD Securities Inc. for distribution to the public, eight million Cumulative Minimum Rate Reset Class AAA Preference Shares, Series EE (the “Preferred Shares, Series EE”). The Preferred Shares, Series EE will be issued at a price of C$25.00 per share, for aggregate proceeds of C$200 million. Holders of the Preferred Shares, Series EE will be entitled to receive a cumulative quarterly fixed dividend yielding 5.10% annually for the initial period ending March 31, 2022. Thereafter, the dividend rate will be reset every five years at a rate equal to the greater of (i) the five-year Government of Canada bond yield plus 3.96% and (ii) 5.10%.

Holders of Preferred Shares, Series EE will have the right, at their option, to convert their shares into Cumulative Floating Rate Class AAA Preference Shares, Series FF (the “Preferred Shares, Series FF”), subject to certain conditions, on March 31, 2022 and on March 31 every five years thereafter. Holders of Preferred Shares, Series FF will be entitled to receive cumulative quarterly floating dividends at a rate equal to the 90-day Government of Canada Treasury Bill yield plus 3.96%.

The Series EE Shares and Series FF Shares will be fully and unconditionally guaranteed, jointly and severally, as to: (i) the payment of dividends, as and when declared, (ii) the payment of amounts due on redemption, and (iii) the payment of amounts due on the liquidation, dissolution or winding-up of the Corporation, by the following entities: Brookfield Property Partners L.P., Brookfield Property L.P., Brookfield BPY Holdings Inc., Brookfield BPY Retail Holdings II Inc., BPY Bermuda Holdings Limited, BPY Bermuda Holdings II Limited, BPY Bermuda Holdings IV Limited and BPY Bermuda Holdings V Limited.

Brookfield Office Properties has granted the underwriters an option, exercisable in whole or in part anytime up to two business days prior to closing, to purchase an additional 2,000,000 Preferred Shares, Series EE at the same offering price. Should the option be fully exercised, the total gross proceeds of the financing will be C$250 million.

The Preferred Shares, Series EE will be offered in all provinces of Canada by way of a supplement to Brookfield Office Properties’ existing Canadian short form base shelf prospectus dated August 29, 2016.

The net proceeds of the issue will be used by Brookfield Office Properties for general corporate purposes which may include the redemption of existing preferred shares. The offering is expected to close on or about February 17, 2017.

They later announced:

Brookfield Office Properties Inc., a subsidiary of Brookfield Property Partners L.P., announced today that as a result of strong investor demand for its previously announced offering it has agreed to increase the size of the offering to eleven million Cumulative Minimum Rate Reset Class AAA Preference Shares, Series EE (the “Preferred Shares, Series EE”). The Preferred Shares, Series EE will be issued at a price of C$25.00 per share, for aggregate proceeds of C$275 million. There will not be an underwriters’ option. The Preferred Shares, Series EE are being offered on a bought deal basis by a syndicate of underwriters led by Scotiabank, CIBC Capital Markets, RBC Capital Markets and TD Securities Inc.

Holders of the Preferred Shares, Series EE will be entitled to receive a cumulative quarterly fixed dividend yielding 5.10% annually for the initial period ending March 31, 2022. Thereafter, the dividend rate will be reset every five years at a rate equal to the greater of (i) the five-year Government of Canada bond yield plus 3.96% and (ii) 5.10%.

Holders of Preferred Shares, Series EE will have the right, at their option, to convert their shares into Cumulative Floating Rate Class AAA Preference Shares, Series FF (the “Preferred Shares, Series FF”), subject to certain conditions, on March 31, 2022 and on March 31 every five years thereafter. Holders of Preferred Shares, Series FF will be entitled to receive cumulative quarterly floating dividends at a rate equal to the 90-day Government of Canada Treasury Bill yield plus 3.96%.

The Series EE Shares and Series FF Shares will be fully and unconditionally guaranteed, jointly and severally, as to: (i) the payment of dividends, as and when declared, (ii) the payment of amounts due on redemption, and (iii) the payment of amounts due on the liquidation, dissolution or winding-up of the Corporation, by the following entities: Brookfield Property Partners L.P., Brookfield Property L.P., Brookfield BPY Holdings Inc., Brookfield BPY Retail Holdings II Inc., BPY Bermuda Holdings Limited, BPY Bermuda Holdings II Limited, BPY Bermuda Holdings IV Limited and BPY Bermuda Holdings V Limited.

The Preferred Shares, Series EE will be offered in all provinces of Canada by way of a supplement to Brookfield Office Properties’ existing Canadian short form base shelf prospectus dated August 29, 2016.

The net proceeds of the issue will be used by Brookfield Office Properties for general corporate purposes which may include the redemption of existing preferred shares. The offering is expected to close on or about February 17, 2017.

Implied volatility analysis indicates:

Click for Big

So according to that, the new issue is a little expensive and should have had a coupon of more like 5.25%, but that depends on how much value you accord the minimum rate guarantee. I value it as zero!

February 9, 2017

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.5844 % | 1,994.0 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.5844 % | 3,658.9 |

| Floater | 3.79 % | 3.96 % | 47,497 | 17.47 | 4 | 0.5844 % | 2,108.6 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1861 % | 2,967.0 |

| SplitShare | 4.71 % | 4.65 % | 58,272 | 4.15 | 4 | -0.1861 % | 3,543.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1861 % | 2,764.6 |

| Perpetual-Premium | 5.44 % | -2.20 % | 80,135 | 0.09 | 16 | 0.1078 % | 2,726.6 |

| Perpetual-Discount | 5.17 % | 5.21 % | 104,418 | 15.04 | 22 | 0.0974 % | 2,904.4 |

| FixedReset | 4.49 % | 4.12 % | 226,318 | 6.74 | 97 | 0.0804 % | 2,292.8 |

| Deemed-Retractible | 5.04 % | -0.52 % | 132,112 | 0.14 | 31 | 0.1719 % | 2,836.6 |

| FloatingReset | 2.48 % | 3.16 % | 47,016 | 4.70 | 9 | 0.1895 % | 2,441.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| HSE.PR.A | FixedReset | -1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-09 Maturity Price : 14.86 Evaluated at bid price : 14.86 Bid-YTW : 4.63 % |

| MFC.PR.F | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.10 Bid-YTW : 9.60 % |

| TRP.PR.D | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-09 Maturity Price : 20.91 Evaluated at bid price : 20.91 Bid-YTW : 4.24 % |

| BAM.PR.K | Floater | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-09 Maturity Price : 12.04 Evaluated at bid price : 12.04 Bid-YTW : 3.96 % |

| BNS.PR.D | FloatingReset | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.35 Bid-YTW : 4.73 % |

| CU.PR.I | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-01 Maturity Price : 25.00 Evaluated at bid price : 26.60 Bid-YTW : 2.66 % |

| PWF.PR.T | FixedReset | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-09 Maturity Price : 21.76 Evaluated at bid price : 22.25 Bid-YTW : 3.94 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.H | FixedReset | 214,856 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.92 Bid-YTW : 4.07 % |

| IAG.PR.G | FixedReset | 97,106 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.11 Bid-YTW : 5.21 % |

| GWO.PR.S | Deemed-Retractible | 86,478 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.66 Bid-YTW : 4.96 % |

| BNS.PR.H | FixedReset | 56,600 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-01-26 Maturity Price : 25.00 Evaluated at bid price : 26.04 Bid-YTW : 3.98 % |

| TRP.PR.G | FixedReset | 51,400 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-09 Maturity Price : 22.21 Evaluated at bid price : 22.75 Bid-YTW : 4.36 % |

| BIP.PR.D | FixedReset | 43,891 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-09 Maturity Price : 23.20 Evaluated at bid price : 25.13 Bid-YTW : 4.90 % |

| There were 31 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TRP.PR.G | FixedReset | Quote: 22.75 – 23.20 Spot Rate : 0.4500 Average : 0.2932 YTW SCENARIO |

| BAM.PF.D | Perpetual-Discount | Quote: 23.31 – 23.57 Spot Rate : 0.2600 Average : 0.1715 YTW SCENARIO |

| MFC.PR.F | FixedReset | Quote: 15.10 – 15.37 Spot Rate : 0.2700 Average : 0.1888 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 20.89 – 21.20 Spot Rate : 0.3100 Average : 0.2362 YTW SCENARIO |

| CU.PR.C | FixedReset | Quote: 21.27 – 21.65 Spot Rate : 0.3800 Average : 0.3077 YTW SCENARIO |

| BAM.PF.F | FixedReset | Quote: 23.75 – 23.94 Spot Rate : 0.1900 Average : 0.1186 YTW SCENARIO |

February 8, 2017

PerpetualDiscounts now yield 5.22%, equivalent to 6.79% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 4.0%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 280bp, a significant widening from the 270bp reported January 25.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.7600 % | 1,982.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.7600 % | 3,637.6 |

| Floater | 3.81 % | 3.97 % | 46,934 | 17.45 | 4 | -0.7600 % | 2,096.4 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3045 % | 2,972.6 |

| SplitShare | 4.70 % | 4.48 % | 58,241 | 4.15 | 4 | 0.3045 % | 3,549.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3045 % | 2,769.7 |

| Perpetual-Premium | 5.44 % | -2.39 % | 75,050 | 0.09 | 16 | 0.1743 % | 2,723.6 |

| Perpetual-Discount | 5.18 % | 5.22 % | 92,935 | 15.04 | 22 | 0.3143 % | 2,901.6 |

| FixedReset | 4.49 % | 4.13 % | 228,123 | 6.74 | 97 | -0.1409 % | 2,291.0 |

| Deemed-Retractible | 5.05 % | 0.41 % | 131,833 | 0.14 | 31 | 0.1761 % | 2,831.7 |

| FloatingReset | 2.48 % | 3.14 % | 48,934 | 4.70 | 9 | -0.7469 % | 2,436.5 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.H | FloatingReset | -3.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-08 Maturity Price : 12.59 Evaluated at bid price : 12.59 Bid-YTW : 3.46 % |

| TRP.PR.F | FloatingReset | -2.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-08 Maturity Price : 16.45 Evaluated at bid price : 16.45 Bid-YTW : 3.63 % |

| BAM.PR.C | Floater | -2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-08 Maturity Price : 11.90 Evaluated at bid price : 11.90 Bid-YTW : 4.01 % |

| BAM.PR.K | Floater | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-08 Maturity Price : 11.91 Evaluated at bid price : 11.91 Bid-YTW : 4.00 % |

| BAM.PR.B | Floater | -1.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-08 Maturity Price : 12.01 Evaluated at bid price : 12.01 Bid-YTW : 3.97 % |

| BAM.PR.R | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-08 Maturity Price : 19.06 Evaluated at bid price : 19.06 Bid-YTW : 4.37 % |

| FTS.PR.K | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-08 Maturity Price : 19.78 Evaluated at bid price : 19.78 Bid-YTW : 4.15 % |

| TRP.PR.C | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-08 Maturity Price : 15.35 Evaluated at bid price : 15.35 Bid-YTW : 4.18 % |

| BNS.PR.D | FloatingReset | -1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.11 Bid-YTW : 4.97 % |

| FTS.PR.G | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-08 Maturity Price : 20.09 Evaluated at bid price : 20.09 Bid-YTW : 4.13 % |

| BAM.PR.N | Perpetual-Discount | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-08 Maturity Price : 22.76 Evaluated at bid price : 23.04 Bid-YTW : 5.21 % |

| PWF.PR.A | Floater | 1.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-08 Maturity Price : 13.80 Evaluated at bid price : 13.80 Bid-YTW : 3.42 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.B | FloatingReset | 108,100 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.78 Bid-YTW : 3.14 % |

| TD.PF.C | FixedReset | 101,102 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-08 Maturity Price : 20.88 Evaluated at bid price : 20.88 Bid-YTW : 4.09 % |

| TD.PF.A | FixedReset | 98,932 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-02-08 Maturity Price : 21.21 Evaluated at bid price : 21.21 Bid-YTW : 4.03 % |

| TD.PR.T | FloatingReset | 75,824 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.87 Bid-YTW : 2.95 % |

| TD.PR.Z | FloatingReset | 51,300 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.82 Bid-YTW : 3.08 % |

| BMO.PR.R | FloatingReset | 50,700 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.65 Bid-YTW : 3.20 % |

| There were 40 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.O | FixedReset | Quote: 26.77 – 27.04 Spot Rate : 0.2700 Average : 0.1857 YTW SCENARIO |

| PWF.PR.T | FixedReset | Quote: 21.96 – 22.34 Spot Rate : 0.3800 Average : 0.3198 YTW SCENARIO |

| PVS.PR.E | SplitShare | Quote: 26.19 – 26.39 Spot Rate : 0.2000 Average : 0.1441 YTW SCENARIO |

| HSB.PR.C | Deemed-Retractible | Quote: 25.31 – 25.48 Spot Rate : 0.1700 Average : 0.1178 YTW SCENARIO |

| TRP.PR.A | FixedReset | Quote: 17.87 – 18.11 Spot Rate : 0.2400 Average : 0.1895 YTW SCENARIO |

| IFC.PR.A | FixedReset | Quote: 18.29 – 18.58 Spot Rate : 0.2900 Average : 0.2411 YTW SCENARIO |

January 31, 2017

Another month draws to a close, with TXPR up 4.05% since year-end. That, together with the appalling January of 2016 dropping out of the trailing twelve months, means that TXPR has achieved a +24.23% total return over the past year … a pretty good recovery, but there’s still a ways to go! The five-year annualized total return is a miserable +0.42%, but at least it’s positive for the first time since August, 2015; the four-year figure is an abysmal -0.55%.

As near as I can make out, the Solactive Laddered Canadian Preferred Share Index is up 31.37% on the year (+4.76% on the month), but the four year annualized total return is still an awful -2.19%.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 3.93 % | 4.67 % | 17,971 | 18.29 | 1 | 0.4091 % | 1,984.0 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2411 % | 3,640.5 |

| Floater | 3.81 % | 3.92 % | 47,529 | 17.57 | 4 | -0.2411 % | 2,098.1 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0459 % | 2,962.9 |

| SplitShare | 4.78 % | 4.46 % | 64,683 | 4.17 | 6 | 0.0459 % | 3,538.4 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0459 % | 2,760.8 |

| Perpetual-Premium | 5.58 % | -5.29 % | 72,434 | 0.09 | 12 | 0.0033 % | 2,711.1 |

| Perpetual-Discount | 5.22 % | 5.26 % | 87,532 | 14.94 | 26 | 0.1296 % | 2,862.8 |

| FixedReset | 4.52 % | 4.23 % | 227,207 | 6.74 | 97 | -0.2471 % | 2,276.1 |

| Deemed-Retractible | 5.09 % | 5.17 % | 132,714 | 4.37 | 32 | 0.1577 % | 2,807.9 |

| FloatingReset | 2.43 % | 3.21 % | 44,584 | 4.71 | 11 | -0.0868 % | 2,445.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PWF.PR.P | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-31 Maturity Price : 15.35 Evaluated at bid price : 15.35 Bid-YTW : 4.33 % |

| CCS.PR.C | Deemed-Retractible | -1.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.21 Bid-YTW : 6.26 % |

| BAM.PR.X | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-31 Maturity Price : 15.95 Evaluated at bid price : 15.95 Bid-YTW : 4.69 % |

| VNR.PR.A | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-31 Maturity Price : 20.68 Evaluated at bid price : 20.68 Bid-YTW : 4.82 % |

| BAM.PR.T | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-31 Maturity Price : 18.42 Evaluated at bid price : 18.42 Bid-YTW : 4.72 % |

| PWF.PR.S | Perpetual-Discount | 1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-31 Maturity Price : 22.51 Evaluated at bid price : 22.83 Bid-YTW : 5.27 % |

| BMO.PR.Q | FixedReset | 1.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.47 Bid-YTW : 5.07 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.H | FixedReset | 257,827 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.86 Bid-YTW : 4.10 % |

| TRP.PR.K | FixedReset | 155,759 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-05-31 Maturity Price : 25.00 Evaluated at bid price : 25.45 Bid-YTW : 4.47 % |

| BAM.PR.K | Floater | 116,351 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-31 Maturity Price : 12.11 Evaluated at bid price : 12.11 Bid-YTW : 3.93 % |

| BIP.PR.D | FixedReset | 115,134 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-31 Maturity Price : 23.21 Evaluated at bid price : 25.18 Bid-YTW : 4.88 % |

| MFC.PR.R | FixedReset | 75,823 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-03-19 Maturity Price : 25.00 Evaluated at bid price : 25.65 Bid-YTW : 4.51 % |

| RY.PR.Z | FixedReset | 65,106 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-31 Maturity Price : 20.96 Evaluated at bid price : 20.96 Bid-YTW : 4.08 % |

| There were 42 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.A | Floater | Quote: 13.37 – 13.73 Spot Rate : 0.3600 Average : 0.2166 YTW SCENARIO |

| CCS.PR.C | Deemed-Retractible | Quote: 23.21 – 23.92 Spot Rate : 0.7100 Average : 0.5817 YTW SCENARIO |

| TRP.PR.G | FixedReset | Quote: 22.81 – 23.22 Spot Rate : 0.4100 Average : 0.3067 YTW SCENARIO |

| BAM.PR.T | FixedReset | Quote: 18.42 – 18.75 Spot Rate : 0.3300 Average : 0.2432 YTW SCENARIO |

| BAM.PF.H | FixedReset | Quote: 26.17 – 26.55 Spot Rate : 0.3800 Average : 0.2952 YTW SCENARIO |

| BAM.PR.R | FixedReset | Quote: 18.76 – 19.02 Spot Rate : 0.2600 Average : 0.1756 YTW SCENARIO |

January 30, 2017

Here’s a video about using drones as part of lifeguarding. I understand that the St. Bernard Mountain Dog Union is very concerned about the potential of lost employment due to technology and has made a large donation to Mr. Trump.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 3.95 % | 4.69 % | 18,661 | 18.27 | 1 | 0.0000 % | 1,975.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.9736 % | 3,649.3 |

| Floater | 3.80 % | 3.90 % | 47,739 | 17.62 | 4 | 0.9736 % | 2,103.1 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1247 % | 2,961.6 |

| SplitShare | 4.79 % | 4.38 % | 65,653 | 4.18 | 6 | 0.1247 % | 3,536.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1247 % | 2,759.5 |

| Perpetual-Premium | 5.58 % | -6.40 % | 72,018 | 0.09 | 12 | -0.0033 % | 2,711.0 |

| Perpetual-Discount | 5.22 % | 5.27 % | 88,717 | 14.89 | 26 | 0.0879 % | 2,859.1 |

| FixedReset | 4.51 % | 4.23 % | 223,509 | 6.74 | 97 | 0.1907 % | 2,281.8 |

| Deemed-Retractible | 5.10 % | 5.17 % | 134,511 | 3.70 | 32 | 0.1540 % | 2,803.5 |

| FloatingReset | 2.42 % | 3.15 % | 45,449 | 4.72 | 11 | -0.0306 % | 2,448.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.H | FloatingReset | -2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-30 Maturity Price : 12.97 Evaluated at bid price : 12.97 Bid-YTW : 3.34 % |

| TRP.PR.G | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-30 Maturity Price : 22.36 Evaluated at bid price : 23.01 Bid-YTW : 4.40 % |

| TRP.PR.F | FloatingReset | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-30 Maturity Price : 16.85 Evaluated at bid price : 16.85 Bid-YTW : 3.53 % |

| TD.PF.F | Perpetual-Discount | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-30 Maturity Price : 24.59 Evaluated at bid price : 25.00 Bid-YTW : 4.91 % |

| BMO.PR.Q | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.15 Bid-YTW : 5.38 % |

| FTS.PR.K | FixedReset | 1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-30 Maturity Price : 19.62 Evaluated at bid price : 19.62 Bid-YTW : 4.24 % |

| BAM.PR.K | Floater | 1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-30 Maturity Price : 12.12 Evaluated at bid price : 12.12 Bid-YTW : 3.93 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BIP.PR.D | FixedReset | 325,007 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-03-31 Maturity Price : 25.00 Evaluated at bid price : 25.19 Bid-YTW : 4.87 % |

| TD.PF.H | FixedReset | 187,057 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.87 Bid-YTW : 4.09 % |

| FTS.PR.H | FixedReset | 151,900 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-30 Maturity Price : 15.15 Evaluated at bid price : 15.15 Bid-YTW : 4.30 % |

| TRP.PR.K | FixedReset | 140,024 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-05-31 Maturity Price : 25.00 Evaluated at bid price : 25.48 Bid-YTW : 4.44 % |

| RY.PR.H | FixedReset | 110,080 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-30 Maturity Price : 21.12 Evaluated at bid price : 21.12 Bid-YTW : 4.10 % |

| TD.PF.B | FixedReset | 99,929 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-01-30 Maturity Price : 20.93 Evaluated at bid price : 20.93 Bid-YTW : 4.14 % |

| There were 58 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.O | FixedReset | Quote: 26.77 – 27.15 Spot Rate : 0.3800 Average : 0.2588 YTW SCENARIO |

| BAM.PF.H | FixedReset | Quote: 26.40 – 26.70 Spot Rate : 0.3000 Average : 0.2022 YTW SCENARIO |

| POW.PR.B | Perpetual-Discount | Quote: 24.95 – 25.22 Spot Rate : 0.2700 Average : 0.1839 YTW SCENARIO |

| BAM.PR.Z | FixedReset | Quote: 22.20 – 22.46 Spot Rate : 0.2600 Average : 0.1792 YTW SCENARIO |

| CU.PR.G | Perpetual-Discount | Quote: 22.01 – 22.25 Spot Rate : 0.2400 Average : 0.1680 YTW SCENARIO |

| W.PR.J | Perpetual-Premium | Quote: 25.20 – 25.43 Spot Rate : 0.2300 Average : 0.1585 YTW SCENARIO |

DFN.PR.A Gets Bigger

On January 26, Dividend 15 Split Corp. announced:

it has filed a preliminary short form prospectus in each of the provinces of Canada with respect to an offering of Preferred Shares and Class A Shares of the Company. The offering will be co-led by National Bank Financial Inc., CIBC, RBC Capital Markets, Scotia Capital Inc., and will also include BMO Capital Markets, TD Securities Inc., GMP Securities L.P., Canaccord Genuity Corp., Raymond James, Desjardins Securities Inc., Echelon Wealth Partners, Mackie Research Capital Corporation and Manulife Securities Incorporated.. The Preferred Shares will be offered at a price of $10.00 per Preferred Share to yield 5.25% and the Class A Shares will be offered at a price of $10.95 per Class A Share to yield 10.96%. The closing price on the TSX of each of the Preferred Shares and the Class A Shares on January 25, 2017 was $10.41 and $11.20, respectively.

Since inception of the Company, the aggregate dividends declared on the Preferred Shares have been $6.76 per share and the aggregate dividends declared on the Class A Shares have been $18.90 per share (including five special distributions of $0.25 per share, one special distribution of $0.50 per share and one special stock dividend of $1.75 per share), for a combined total of $25.66 per unit. All distributions to date have been made in tax advantage eligible Canadian dividends or capital gains dividends. The net proceeds of the offering will be used by the Company to invest in an actively managed, high quality portfolio consisting of 15 dividend yielding Canadian companies as

follows:

Bank of Montreal Enbridge Inc. TELUS Corporation The Bank of Nova Scotia Manulife Financial Corp. Thomson-Reuters Corporation BCE Inc. National Bank of Canada The Toronto-Dominion Bank Canadian Imperial Bank of Commerce Royal Bank of Canada TransAlta Corporation CI Financial Corp. Sun Life Financial Inc. TransCanada Corporation The Company’s investment objectives are:

Preferred Shares:

i. to provide holders of the Preferred Shares with fixed, cumulative preferential monthly cash dividends in the amount of 5.25% annually; and

ii. on or about the termination date, currently December 1, 2019 (subject to further 5 year extensions thereafter), to pay the holders of the Preferred Shares $10.00 per Preferred Share.Class A Shares:

i. to provide holders of the Class A Shares with regular monthly cash dividends currently targeted to be $0.10 per share; and

ii. on or about the termination date, currently December 1, 2019 (subject to further 5 year extensions thereafter) to pay holders of Class A Shares at least the original issue price of those shares.The sales period of this overnight offering will end at 9:00 a.m. EST on January 27, 2017.

Today the company announced:

Dividend 15 Split Corp. (the “Company”) is pleased to announce it has completed the overnight marketing of up to 3,056,000 Preferred Shares and up to 3,056,000 Class A Shares of the Company. The total proceeds of the offering are expected to be approximately $64.0 million.

OSP.PR.A Gets Bigger

On January 26, Brompton Group announced (nb: slight change in table layout … JH):

Brompton Oil Split Corp. (the “Company”) is pleased to announce it is undertaking an overnight treasury offering of class A and preferred shares.

The class A shares will be offered at a price of $9.75 for a distribution rate of 12.3% on the issue price, and the preferred shares will be offered at a price of $10.00 for a yield to maturity of 5.2%. The closing price on the Toronto Stock Exchange (“TSX”) for each of the class A and preferred shares on January 25, 2017 was $10.10 and $10.16, respectively. The class A and preferred share offering prices were determined so as to be non-dilutive to the most recently calculated net asset value per unit of the Company, as adjusted for dividends and certain expenses to be accrued prior to or upon settlement of the offering.

The sales period of this overnight offering will end at 9:00 a.m. (ET) on January 27, 2017. The offering is expected to close on or about February 3, 2017 and is subject to certain closing conditions including approval by the TSX.

The syndicate of agents for the offering is being led by RBC Capital Markets, CIBC and Scotiabank.

The Company invests in a portfolio of equity securities of large capitalization North American oil and gas issuers, primarily focused on those with significant exposure to oil. All portfolio securities are S&P/TSX Composite Index or S&P 500 Index constituents which have a market capitalization of at least $2 billion and pay a dividend. Currently, the portfolio consists of common shares of the following companies:

Anadarko Petroleum Corporation Cimarex Energy Co. Whitecap Resources Inc. Pioneer Natural Resources Company Apache Corporation Crescent Point Energy Corporation PrairieSky Royalty Ltd. ARC Resources Ltd. Devon Energy Corporation Suncor Energy Inc. Canadian Natural Resources Limited EOG Resources Inc. Vermilion Energy Inc. Cenovus Energy Inc. Occidental Petroleum Corporation The investment objectives for the class A shares are to provide holders with regular monthly cash distributions targeted to be $0.10 per class A share and to provide the opportunity for growth in the net asset value per class A share.

The investment objectives for the preferred shares are to provide holders with fixed cumulative preferential quarterly cash distributions, currently in the amount of $0.1250 per preferred share, and to return the original issue price to holders of preferred shares on the Company’s maturity date (March 31, 2020).

Today they announced:

Brompton Oil Split Corp. (the “Company”) is pleased to announce the results of its overnight treasury offering of class A and preferred shares. Gross proceeds of the offering are expected to be approximately $11 million. The offering is expected to close on or about February 3, 2017 and is subject to customary closing conditions including approval from the Toronto Stock Exchange (the “TSX”).

Well, another $5-million-odd worth on the market won’t solve OSP.PR.A’s liquidity problems, but every little bit helps!

Update, 2017-2-3: Brompton Group has announced:

Brompton Oil Split Corp. (the “Company”) is pleased to announce that it has completed a treasury offering of 549,800 class A shares and 549,800 preferred shares for aggregate gross proceeds of approximately $11 million. The class A shares and preferred shares will trade on the Toronto Stock Exchange (the “TSX”) under the existing symbols OSP (class A shares) and OSP.PR.A (preferred shares).

The class A shares were offered at a price of $9.75 per class A share and the preferred shares were offered at a price of $10.00 per preferred share. The class A and preferred share offering prices were determined so as to be non-dilutive to the net asset value per unit of the Company as of the pricing date, as adjusted for dividends and certain expenses accrued prior to closing of the offering.