I noticed last night that I was running short of milk and paper towels, so trotted up to Blah-blahs this afternoon to replenish my supply. Holy Smokes, the place was a madhouse! It was jammed with people wheeling around carts full to the brim … I suppose I might have seen it busier on occasion, like on a Saturday before it closes for two days at Christmas, but I can’t remember such a sight!

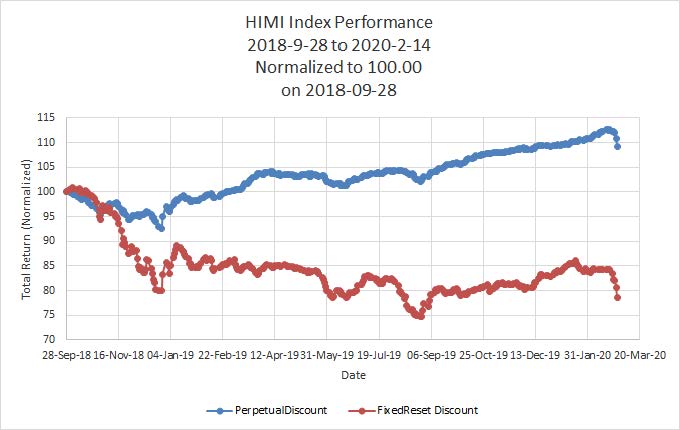

The Total Return version of TXPR closed today at 1208.11. The value of this index on June 29, 2007, the first month-end following the launch date, was 1217.73, so total return has been negative over the past TWELVE YEARS AND EIGHT MONTHS and a little bit, which we can round off to “forever”. That’s before fees and expenses. Remember those charts I published in the post MAPF Performance : August 2019 illustrating the downturn to date, comparing it to the Credit Crunch and remarking that there had been zero total return for seven years and four months? Well, those charts are now out of date.

And my own preferred share reporting shows massive volume, huge moves and so many candidates for the “Bad Quote Hall of Shame” that I’m not going to check any of them. Interestingly, the “Bank FixedReset NVCC non-compliant” subindex, comprised of the three remaining bank issues which may reasonably be expected to be redeemed in the near future, underperformed discount FixedResets. Which is a little odd; have we reached the point of maximum panic?

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| HSE.PR.C |

FixedReset Disc |

-19.46 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 10.06

Evaluated at bid price : 10.06

Bid-YTW : 10.34 % |

| HSE.PR.G |

FixedReset Disc |

-19.29 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 10.25

Evaluated at bid price : 10.25

Bid-YTW : 10.05 % |

| HSE.PR.E |

FixedReset Disc |

-17.63 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 10.00

Evaluated at bid price : 10.00

Bid-YTW : 10.40 % |

| BNS.PR.Z |

FixedReset Bank Non |

-14.61 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.04

Bid-YTW : 14.50 % |

| CM.PR.R |

FixedReset Disc |

-14.04 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 14.94

Evaluated at bid price : 14.94

Bid-YTW : 6.69 % |

| SLF.PR.J |

FloatingReset |

-13.71 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 8.50

Evaluated at bid price : 8.50

Bid-YTW : 5.89 % |

| PWF.PR.A |

Floater |

-13.38 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 8.35

Evaluated at bid price : 8.35

Bid-YTW : 7.34 % |

| NA.PR.S |

FixedReset Disc |

-12.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.08

Evaluated at bid price : 12.08

Bid-YTW : 6.64 % |

| PWF.PR.P |

FixedReset Disc |

-12.37 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 9.00

Evaluated at bid price : 9.00

Bid-YTW : 5.82 % |

| BIP.PR.C |

FixedReset Prem |

-12.21 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 19.85

Evaluated at bid price : 19.85

Bid-YTW : 6.77 % |

| CM.PR.T |

FixedReset Disc |

-12.12 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 16.39

Evaluated at bid price : 16.39

Bid-YTW : 6.42 % |

| PWF.PR.Q |

FloatingReset |

-11.90 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 8.81

Evaluated at bid price : 8.81

Bid-YTW : 6.31 % |

| PWF.PR.T |

FixedReset Disc |

-11.85 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.50

Evaluated at bid price : 12.50

Bid-YTW : 6.44 % |

| BAM.PR.K |

Floater |

-11.68 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 8.05

Evaluated at bid price : 8.05

Bid-YTW : 7.52 % |

| TD.PF.F |

Perpetual-Discount |

-10.99 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.50

Evaluated at bid price : 20.50

Bid-YTW : 6.07 % |

| BMO.PR.Y |

FixedReset Disc |

-10.87 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 13.61

Evaluated at bid price : 13.61

Bid-YTW : 5.89 % |

| BIP.PR.B |

FixedReset Prem |

-10.85 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.30

Evaluated at bid price : 20.30

Bid-YTW : 6.80 % |

| CM.PR.P |

FixedReset Disc |

-10.79 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 11.91

Evaluated at bid price : 11.91

Bid-YTW : 6.58 % |

| BAM.PR.M |

Perpetual-Discount |

-10.76 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 17.89

Evaluated at bid price : 17.89

Bid-YTW : 6.66 % |

| MFC.PR.F |

FixedReset Ins Non |

-10.76 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 7.80

Evaluated at bid price : 7.80

Bid-YTW : 6.07 % |

| CM.PR.Y |

FixedReset Disc |

-10.72 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 17.32

Evaluated at bid price : 17.32

Bid-YTW : 6.44 % |

| MFC.PR.R |

FixedReset Ins Non |

-10.66 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 16.84

Evaluated at bid price : 16.84

Bid-YTW : 6.50 % |

| BAM.PR.C |

Floater |

-10.54 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 8.01

Evaluated at bid price : 8.01

Bid-YTW : 7.56 % |

| NA.PR.C |

FixedReset Disc |

-10.46 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 15.50

Evaluated at bid price : 15.50

Bid-YTW : 6.51 % |

| BAM.PR.N |

Perpetual-Discount |

-10.18 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 17.90

Evaluated at bid price : 17.90

Bid-YTW : 6.66 % |

| BMO.PR.Q |

FixedReset Bank Non |

-9.96 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.71

Bid-YTW : 12.28 % |

| TD.PF.C |

FixedReset Disc |

-9.77 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.65

Evaluated at bid price : 12.65

Bid-YTW : 6.16 % |

| RY.PR.H |

FixedReset Disc |

-9.75 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.50

Evaluated at bid price : 12.50

Bid-YTW : 5.99 % |

| BAM.PR.B |

Floater |

-9.74 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 8.01

Evaluated at bid price : 8.01

Bid-YTW : 7.56 % |

| BIP.PR.A |

FixedReset Disc |

-9.68 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 14.00

Evaluated at bid price : 14.00

Bid-YTW : 7.19 % |

| PVS.PR.H |

SplitShare |

-9.64 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2027-02-28

Maturity Price : 25.00

Evaluated at bid price : 22.50

Bid-YTW : 6.56 % |

| NA.PR.W |

FixedReset Disc |

-9.61 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 11.76

Evaluated at bid price : 11.76

Bid-YTW : 6.58 % |

| MFC.PR.H |

FixedReset Ins Non |

-9.58 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 14.06

Evaluated at bid price : 14.06

Bid-YTW : 6.57 % |

| GWO.PR.F |

Deemed-Retractible |

-9.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 22.12

Evaluated at bid price : 22.40

Bid-YTW : 6.60 % |

| RY.PR.Z |

FixedReset Disc |

-9.29 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.50

Evaluated at bid price : 12.50

Bid-YTW : 5.91 % |

| IFC.PR.A |

FixedReset Ins Non |

-9.29 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 10.45

Evaluated at bid price : 10.45

Bid-YTW : 5.84 % |

| RY.PR.P |

Perpetual-Premium |

-9.24 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.75

Evaluated at bid price : 22.01

Bid-YTW : 6.01 % |

| BMO.PR.S |

FixedReset Disc |

-9.24 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.58

Evaluated at bid price : 12.58

Bid-YTW : 6.14 % |

| NA.PR.E |

FixedReset Disc |

-9.09 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 13.00

Evaluated at bid price : 13.00

Bid-YTW : 6.54 % |

| HSE.PR.A |

FixedReset Disc |

-9.09 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 6.00

Evaluated at bid price : 6.00

Bid-YTW : 9.46 % |

| MFC.PR.J |

FixedReset Ins Non |

-9.00 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 13.55

Evaluated at bid price : 13.55

Bid-YTW : 6.26 % |

| W.PR.M |

FixedReset Prem |

-8.98 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.99

Evaluated at bid price : 20.99

Bid-YTW : 6.31 % |

| TD.PF.B |

FixedReset Disc |

-8.95 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.61

Evaluated at bid price : 12.61

Bid-YTW : 6.00 % |

| MFC.PR.G |

FixedReset Ins Non |

-8.91 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 13.40

Evaluated at bid price : 13.40

Bid-YTW : 6.40 % |

| NA.PR.A |

FixedReset Prem |

-8.77 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.21

Evaluated at bid price : 21.21

Bid-YTW : 6.13 % |

| TD.PF.A |

FixedReset Disc |

-8.75 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.51

Evaluated at bid price : 12.51

Bid-YTW : 6.02 % |

| BAM.PF.D |

Perpetual-Discount |

-8.75 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 18.50

Evaluated at bid price : 18.50

Bid-YTW : 6.65 % |

| PWF.PR.Z |

Perpetual-Discount |

-8.70 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.16

Evaluated at bid price : 20.16

Bid-YTW : 6.49 % |

| BIP.PR.D |

FixedReset Disc |

-8.66 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 18.35

Evaluated at bid price : 18.35

Bid-YTW : 6.84 % |

| BMO.PR.B |

FixedReset Prem |

-8.58 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 19.38

Evaluated at bid price : 19.38

Bid-YTW : 5.93 % |

| CM.PR.O |

FixedReset Disc |

-8.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.01

Evaluated at bid price : 12.01

Bid-YTW : 6.45 % |

| BIP.PR.E |

FixedReset Disc |

-8.50 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 18.40

Evaluated at bid price : 18.40

Bid-YTW : 6.82 % |

| GWO.PR.G |

Deemed-Retractible |

-8.43 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.30

Evaluated at bid price : 20.30

Bid-YTW : 6.43 % |

| SLF.PR.A |

Deemed-Retractible |

-8.43 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 19.00

Evaluated at bid price : 19.00

Bid-YTW : 6.27 % |

| SLF.PR.G |

FixedReset Ins Non |

-8.43 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 9.02

Evaluated at bid price : 9.02

Bid-YTW : 5.17 % |

| BMO.PR.W |

FixedReset Disc |

-8.40 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.65

Evaluated at bid price : 12.65

Bid-YTW : 6.00 % |

| MFC.PR.I |

FixedReset Ins Non |

-8.36 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 13.49

Evaluated at bid price : 13.49

Bid-YTW : 6.48 % |

| GWO.PR.N |

FixedReset Ins Non |

-8.33 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 9.35

Evaluated at bid price : 9.35

Bid-YTW : 4.73 % |

| TRP.PR.K |

FixedReset Prem |

-8.26 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 19.88

Evaluated at bid price : 19.88

Bid-YTW : 6.23 % |

| TD.PF.J |

FixedReset Disc |

-8.25 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 14.90

Evaluated at bid price : 14.90

Bid-YTW : 5.88 % |

| BAM.PF.C |

Perpetual-Discount |

-8.18 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 18.30

Evaluated at bid price : 18.30

Bid-YTW : 6.65 % |

| TRP.PR.E |

FixedReset Disc |

-8.17 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 11.58

Evaluated at bid price : 11.58

Bid-YTW : 6.78 % |

| BMO.PR.T |

FixedReset Disc |

-8.09 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.50

Evaluated at bid price : 12.50

Bid-YTW : 5.94 % |

| IAF.PR.G |

FixedReset Ins Non |

-8.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 13.06

Evaluated at bid price : 13.06

Bid-YTW : 6.47 % |

| BIK.PR.A |

FixedReset Prem |

-7.84 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.42

Evaluated at bid price : 21.75

Bid-YTW : 6.74 % |

| BIP.PR.F |

FixedReset Disc |

-7.76 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 18.55

Evaluated at bid price : 18.55

Bid-YTW : 6.90 % |

| RY.PR.W |

Perpetual-Discount |

-7.74 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.10

Evaluated at bid price : 21.10

Bid-YTW : 5.87 % |

| BMO.PR.F |

FixedReset Disc |

-7.69 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 18.00

Evaluated at bid price : 18.00

Bid-YTW : 5.96 % |

| PWF.PR.R |

Perpetual-Premium |

-7.68 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.65

Evaluated at bid price : 21.65

Bid-YTW : 6.46 % |

| NA.PR.G |

FixedReset Disc |

-7.67 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 14.09

Evaluated at bid price : 14.09

Bid-YTW : 6.53 % |

| BMO.PR.E |

FixedReset Disc |

-7.62 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 14.67

Evaluated at bid price : 14.67

Bid-YTW : 6.06 % |

| MFC.PR.K |

FixedReset Ins Non |

-7.58 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.20

Evaluated at bid price : 12.20

Bid-YTW : 6.29 % |

| TD.PF.K |

FixedReset Disc |

-7.50 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 14.80

Evaluated at bid price : 14.80

Bid-YTW : 5.87 % |

| GWO.PR.Q |

Deemed-Retractible |

-7.40 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.65

Evaluated at bid price : 20.65

Bid-YTW : 6.26 % |

| GWO.PR.T |

Deemed-Retractible |

-7.37 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.61

Evaluated at bid price : 20.61

Bid-YTW : 6.27 % |

| W.PR.K |

FixedReset Prem |

-7.26 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.42

Evaluated at bid price : 21.73

Bid-YTW : 6.14 % |

| BMO.PR.C |

FixedReset Disc |

-7.22 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 16.70

Evaluated at bid price : 16.70

Bid-YTW : 5.86 % |

| BAM.PR.X |

FixedReset Disc |

-7.19 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 9.50

Evaluated at bid price : 9.50

Bid-YTW : 6.12 % |

| MFC.PR.L |

FixedReset Ins Non |

-7.17 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 11.53

Evaluated at bid price : 11.53

Bid-YTW : 6.37 % |

| TD.PF.L |

FixedReset Disc |

-7.15 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 17.91

Evaluated at bid price : 17.91

Bid-YTW : 5.80 % |

| MFC.PR.Q |

FixedReset Ins Non |

-7.15 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 13.38

Evaluated at bid price : 13.38

Bid-YTW : 6.29 % |

| BMO.PR.D |

FixedReset Disc |

-7.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 16.40

Evaluated at bid price : 16.40

Bid-YTW : 5.75 % |

| TRP.PR.G |

FixedReset Disc |

-6.86 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.90

Evaluated at bid price : 12.90

Bid-YTW : 6.73 % |

| BAM.PF.I |

FixedReset Prem |

-6.80 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.33

Evaluated at bid price : 21.63

Bid-YTW : 5.55 % |

| PWF.PR.E |

Perpetual-Premium |

-6.72 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.50

Evaluated at bid price : 21.50

Bid-YTW : 6.50 % |

| TD.PF.G |

FixedReset Prem |

-6.72 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.55

Evaluated at bid price : 21.92

Bid-YTW : 5.93 % |

| NA.PR.X |

FixedReset Prem |

-6.68 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.75

Evaluated at bid price : 22.21

Bid-YTW : 6.10 % |

| EML.PR.A |

FixedReset Ins Non |

-6.63 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2030-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.96

Bid-YTW : 7.41 % |

| SLF.PR.I |

FixedReset Ins Non |

-6.56 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 13.25

Evaluated at bid price : 13.25

Bid-YTW : 6.15 % |

| GWO.PR.H |

Deemed-Retractible |

-6.49 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 19.75

Evaluated at bid price : 19.75

Bid-YTW : 6.16 % |

| GWO.PR.P |

Deemed-Retractible |

-6.48 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.51

Evaluated at bid price : 21.51

Bid-YTW : 6.30 % |

| POW.PR.B |

Perpetual-Discount |

-6.46 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.00

Evaluated at bid price : 21.00

Bid-YTW : 6.50 % |

| IAF.PR.I |

FixedReset Ins Non |

-6.42 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 13.85

Evaluated at bid price : 13.85

Bid-YTW : 6.35 % |

| PWF.PR.O |

Perpetual-Premium |

-6.41 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 22.21

Evaluated at bid price : 22.48

Bid-YTW : 6.54 % |

| PWF.PR.K |

Perpetual-Discount |

-6.32 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 19.87

Evaluated at bid price : 19.87

Bid-YTW : 6.33 % |

| RY.PR.S |

FixedReset Disc |

-6.31 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 15.00

Evaluated at bid price : 15.00

Bid-YTW : 5.53 % |

| TRP.PR.D |

FixedReset Disc |

-6.30 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.05

Evaluated at bid price : 12.05

Bid-YTW : 6.57 % |

| TRP.PR.J |

FixedReset Prem |

-6.28 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.35

Evaluated at bid price : 21.35

Bid-YTW : 6.51 % |

| TD.PF.I |

FixedReset Disc |

-6.25 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 15.75

Evaluated at bid price : 15.75

Bid-YTW : 5.85 % |

| PWF.PR.L |

Perpetual-Discount |

-6.21 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.40

Evaluated at bid price : 20.40

Bid-YTW : 6.35 % |

| BAM.PF.J |

FixedReset Prem |

-6.20 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.51

Evaluated at bid price : 21.51

Bid-YTW : 5.54 % |

| SLF.PR.H |

FixedReset Ins Non |

-6.17 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 11.70

Evaluated at bid price : 11.70

Bid-YTW : 5.66 % |

| ELF.PR.G |

Perpetual-Discount |

-6.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.10

Evaluated at bid price : 20.10

Bid-YTW : 6.02 % |

| GWO.PR.I |

Deemed-Retractible |

-6.02 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 18.26

Evaluated at bid price : 18.26

Bid-YTW : 6.18 % |

| BNS.PR.E |

FixedReset Prem |

-6.00 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.44

Evaluated at bid price : 21.77

Bid-YTW : 5.81 % |

| BNS.PR.H |

FixedReset Prem |

-5.98 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.61

Evaluated at bid price : 20.61

Bid-YTW : 5.75 % |

| CU.PR.E |

Perpetual-Discount |

-5.96 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.16

Evaluated at bid price : 21.16

Bid-YTW : 5.84 % |

| TRP.PR.F |

FloatingReset |

-5.92 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 9.70

Evaluated at bid price : 9.70

Bid-YTW : 6.48 % |

| POW.PR.C |

Perpetual-Premium |

-5.89 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 22.72

Evaluated at bid price : 23.01

Bid-YTW : 6.41 % |

| SLF.PR.C |

Deemed-Retractible |

-5.85 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 18.17

Evaluated at bid price : 18.17

Bid-YTW : 6.15 % |

| SLF.PR.E |

Deemed-Retractible |

-5.85 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 18.50

Evaluated at bid price : 18.50

Bid-YTW : 6.10 % |

| EMA.PR.E |

Perpetual-Discount |

-5.84 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.01

Evaluated at bid price : 20.01

Bid-YTW : 5.68 % |

| SLF.PR.D |

Deemed-Retractible |

-5.83 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 18.40

Evaluated at bid price : 18.40

Bid-YTW : 6.07 % |

| CCS.PR.C |

Deemed-Retractible |

-5.81 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.41

Evaluated at bid price : 21.41

Bid-YTW : 5.86 % |

| RY.PR.O |

Perpetual-Discount |

-5.79 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.49

Evaluated at bid price : 21.49

Bid-YTW : 5.76 % |

| PWF.PR.F |

Perpetual-Discount |

-5.69 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.06

Evaluated at bid price : 21.06

Bid-YTW : 6.33 % |

| BAM.PR.R |

FixedReset Disc |

-5.56 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 11.57

Evaluated at bid price : 11.57

Bid-YTW : 6.00 % |

| PWF.PR.I |

Perpetual-Premium |

-5.54 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 23.24

Evaluated at bid price : 23.54

Bid-YTW : 6.46 % |

| PVS.PR.F |

SplitShare |

-5.38 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2024-09-30

Maturity Price : 25.00

Evaluated at bid price : 23.75

Bid-YTW : 6.12 % |

| MFC.PR.C |

Deemed-Retractible |

-5.33 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 18.65

Evaluated at bid price : 18.65

Bid-YTW : 6.07 % |

| RY.PR.R |

FixedReset Prem |

-5.31 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 22.42

Evaluated at bid price : 22.82

Bid-YTW : 5.81 % |

| POW.PR.A |

Perpetual-Premium |

-5.13 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.76

Evaluated at bid price : 22.01

Bid-YTW : 6.47 % |

| TRP.PR.A |

FixedReset Disc |

-5.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 10.61

Evaluated at bid price : 10.61

Bid-YTW : 6.37 % |

| CM.PR.S |

FixedReset Disc |

-4.97 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 13.78

Evaluated at bid price : 13.78

Bid-YTW : 5.92 % |

| PWF.PR.H |

Perpetual-Premium |

-4.94 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 22.44

Evaluated at bid price : 22.70

Bid-YTW : 6.42 % |

| TD.PF.D |

FixedReset Disc |

-4.93 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 14.65

Evaluated at bid price : 14.65

Bid-YTW : 5.62 % |

| BAM.PR.T |

FixedReset Disc |

-4.89 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 11.50

Evaluated at bid price : 11.50

Bid-YTW : 6.21 % |

| CU.PR.C |

FixedReset Disc |

-4.86 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 14.50

Evaluated at bid price : 14.50

Bid-YTW : 5.07 % |

| GWO.PR.R |

Deemed-Retractible |

-4.81 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.00

Evaluated at bid price : 20.00

Bid-YTW : 6.02 % |

| BMO.PR.Z |

Perpetual-Discount |

-4.79 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 22.12

Evaluated at bid price : 22.47

Bid-YTW : 5.60 % |

| RY.PR.E |

Deemed-Retractible |

-4.66 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.75

Bid-YTW : 7.56 % |

| PWF.PR.G |

Perpetual-Premium |

-4.58 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 23.22

Evaluated at bid price : 23.52

Bid-YTW : 6.36 % |

| BAM.PF.B |

FixedReset Disc |

-4.49 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 14.04

Evaluated at bid price : 14.04

Bid-YTW : 6.10 % |

| MFC.PR.M |

FixedReset Ins Non |

-4.43 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.30

Evaluated at bid price : 12.30

Bid-YTW : 6.34 % |

| CU.PR.G |

Perpetual-Discount |

-4.43 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.08

Evaluated at bid price : 20.08

Bid-YTW : 5.65 % |

| TD.PF.M |

FixedReset Disc |

-4.37 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 18.60

Evaluated at bid price : 18.60

Bid-YTW : 5.87 % |

| TRP.PR.B |

FixedReset Disc |

-4.33 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 7.51

Evaluated at bid price : 7.51

Bid-YTW : 5.78 % |

| ELF.PR.H |

Perpetual-Premium |

-4.33 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 22.83

Evaluated at bid price : 23.20

Bid-YTW : 6.02 % |

| GWO.PR.L |

Deemed-Retractible |

-4.32 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 22.59

Evaluated at bid price : 22.84

Bid-YTW : 6.19 % |

| BAM.PF.H |

FixedReset Prem |

-4.27 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.80

Evaluated at bid price : 22.28

Bid-YTW : 5.60 % |

| BAM.PF.A |

FixedReset Disc |

-4.25 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 15.30

Evaluated at bid price : 15.30

Bid-YTW : 6.10 % |

| CU.PR.D |

Perpetual-Discount |

-4.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.50

Evaluated at bid price : 21.50

Bid-YTW : 5.75 % |

| IFC.PR.G |

FixedReset Ins Non |

-4.21 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 15.01

Evaluated at bid price : 15.01

Bid-YTW : 5.77 % |

| CU.PR.F |

Perpetual-Discount |

-4.17 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.20

Evaluated at bid price : 20.20

Bid-YTW : 5.62 % |

| IFC.PR.C |

FixedReset Ins Non |

-4.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 13.43

Evaluated at bid price : 13.43

Bid-YTW : 5.96 % |

| GWO.PR.M |

Deemed-Retractible |

-4.13 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 22.93

Evaluated at bid price : 23.20

Bid-YTW : 6.26 % |

| EMA.PR.F |

FixedReset Disc |

-4.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 15.20

Evaluated at bid price : 15.20

Bid-YTW : 5.66 % |

| RY.PR.G |

Deemed-Retractible |

-4.09 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.70

Bid-YTW : 7.68 % |

| GWO.PR.S |

Deemed-Retractible |

-4.05 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.30

Evaluated at bid price : 21.30

Bid-YTW : 6.18 % |

| BNS.PR.I |

FixedReset Disc |

-4.05 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 15.15

Evaluated at bid price : 15.15

Bid-YTW : 5.59 % |

| CIU.PR.A |

Perpetual-Discount |

-4.05 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.15

Evaluated at bid price : 20.15

Bid-YTW : 5.76 % |

| MFC.PR.N |

FixedReset Ins Non |

-4.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 12.14

Evaluated at bid price : 12.14

Bid-YTW : 5.70 % |

| RY.PR.A |

Deemed-Retractible |

-4.02 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.85

Bid-YTW : 7.26 % |

| EMA.PR.H |

FixedReset Prem |

-4.01 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 22.37

Evaluated at bid price : 22.96

Bid-YTW : 5.36 % |

| PWF.PR.S |

Perpetual-Discount |

-3.99 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 19.95

Evaluated at bid price : 19.95

Bid-YTW : 6.11 % |

| IFC.PR.E |

Deemed-Retractible |

-3.93 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.69

Evaluated at bid price : 22.00

Bid-YTW : 6.02 % |

| BAM.PR.Z |

FixedReset Disc |

-3.92 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 14.85

Evaluated at bid price : 14.85

Bid-YTW : 6.13 % |

| RY.PR.N |

Perpetual-Discount |

-3.90 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.61

Evaluated at bid price : 21.95

Bid-YTW : 5.62 % |

| RY.PR.C |

Deemed-Retractible |

-3.87 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.85

Bid-YTW : 7.42 % |

| IFC.PR.I |

Perpetual-Premium |

-3.86 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 22.07

Evaluated at bid price : 22.40

Bid-YTW : 6.08 % |

| EMA.PR.C |

FixedReset Disc |

-3.82 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 15.34

Evaluated at bid price : 15.34

Bid-YTW : 5.66 % |

| RY.PR.Q |

FixedReset Prem |

-3.80 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.78

Evaluated at bid price : 22.25

Bid-YTW : 5.67 % |

| IFC.PR.F |

Deemed-Retractible |

-3.80 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.68

Evaluated at bid price : 22.00

Bid-YTW : 6.14 % |

| TD.PF.E |

FixedReset Disc |

-3.77 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 15.06

Evaluated at bid price : 15.06

Bid-YTW : 5.61 % |

| BNS.PR.G |

FixedReset Prem |

-3.76 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.94

Evaluated at bid price : 22.51

Bid-YTW : 5.83 % |

| IAF.PR.B |

Deemed-Retractible |

-3.71 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.25

Evaluated at bid price : 20.25

Bid-YTW : 5.70 % |

| BNS.PR.Y |

FixedReset Bank Non |

-3.63 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.66

Bid-YTW : 4.55 % |

| SLF.PR.B |

Deemed-Retractible |

-3.61 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.00

Evaluated at bid price : 20.00

Bid-YTW : 6.02 % |

| MFC.PR.B |

Deemed-Retractible |

-3.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 19.41

Evaluated at bid price : 19.41

Bid-YTW : 6.02 % |

| MFC.PR.O |

FixedReset Ins Non |

-3.43 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.58

Evaluated at bid price : 21.97

Bid-YTW : 6.20 % |

| RY.PR.F |

Deemed-Retractible |

-3.01 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.85

Bid-YTW : 7.26 % |

| CU.PR.H |

Perpetual-Discount |

-2.92 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 22.55

Evaluated at bid price : 22.90

Bid-YTW : 5.76 % |

| POW.PR.G |

Perpetual-Premium |

-2.87 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.94

Evaluated at bid price : 22.30

Bid-YTW : 6.38 % |

| CU.PR.I |

FixedReset Prem |

-2.81 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 22.85

Evaluated at bid price : 23.50

Bid-YTW : 4.78 % |

| BAM.PF.F |

FixedReset Disc |

-2.65 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 14.35

Evaluated at bid price : 14.35

Bid-YTW : 6.13 % |

| EIT.PR.A |

SplitShare |

-2.30 % |

YTW SCENARIO

Maturity Type : Soft Maturity

Maturity Date : 2024-03-14

Maturity Price : 25.00

Evaluated at bid price : 24.67

Bid-YTW : 5.19 % |

| CM.PR.Q |

FixedReset Disc |

-2.24 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 13.10

Evaluated at bid price : 13.10

Bid-YTW : 6.31 % |

| BAM.PF.E |

FixedReset Disc |

-2.21 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 13.24

Evaluated at bid price : 13.24

Bid-YTW : 5.69 % |

| TD.PF.H |

FixedReset Prem |

-2.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 21.00

Evaluated at bid price : 21.00

Bid-YTW : 5.55 % |

| TRP.PR.C |

FixedReset Disc |

-1.78 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 8.26

Evaluated at bid price : 8.26

Bid-YTW : 6.16 % |

| PVS.PR.D |

SplitShare |

-1.74 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2021-10-08

Maturity Price : 25.00

Evaluated at bid price : 24.35

Bid-YTW : 6.33 % |

| POW.PR.D |

Perpetual-Discount |

-1.65 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 20.85

Evaluated at bid price : 20.85

Bid-YTW : 6.11 % |

| PVS.PR.E |

SplitShare |

-1.57 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-10-31

Maturity Price : 25.00

Evaluated at bid price : 25.01

Bid-YTW : 5.55 % |

| BAM.PF.G |

FixedReset Disc |

-1.22 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2050-03-12

Maturity Price : 14.14

Evaluated at bid price : 14.14

Bid-YTW : 5.84 % |