BCE Inc. has announced (emphasis from original) that it:

will, on February 1, 2015, continue to have Cumulative Redeemable First Preferred Shares, Series AF (“Series AF Preferred Shares”) outstanding if, following the end of the conversion period on January 19, 2015, BCE Inc. determines that at least one million Series AF Preferred Shares would remain outstanding. In such a case, as of February 1, 2015, the Series AF Preferred Shares will pay, on a quarterly basis, as and when declared by the Board of Directors of BCE Inc., a fixed cash dividend for the following five years that will be based on a fixed rate equal to the product of: (a) the average of the yields to maturity compounded semi-annually, determined on January 12, 2015 by two investment dealers selected by BCE Inc., that would be carried by non-callable Government of Canada bonds with a 5-year maturity (the “Government of Canada Yield”), multiplied by (b) a percentage rate determined by BCE Inc. (the “Selected Percentage Rate”) for such period. The “Selected Percentage Rate” determined by BCE Inc. for such period is 259.4%. The “Government of Canada Yield” is 1.199% . Accordingly, the annual dividend rate applicable to the Series AF Preferred Shares for the period of five years beginning on February 1, 2015 will be 3.110%.

The rate was reset in 2010 to 4.541%, so this is a 32% cut to the dividend, which will no doubt cause much wailing and gnashing of teeth.

This is not much of a premium over the 3.00% (100% of Prime) paid by the RatchetRate issue, BCE.PR.E, and as it turns out the breakeven prime rate as determined by the pairs equivalency calculator is only 3.55% given today’s closing bids of 20.04 for BCE.PR.F and 20.50 for BCE.PR.E.

That is to say that IF BCE.PR.E continues to trade below par and therefore continues to pay 100% of prime, and if the average prime rate from now until the next interconversion date in 2020 exceeds 3.55%, THEN BCE.PR.E will have been the better choice.

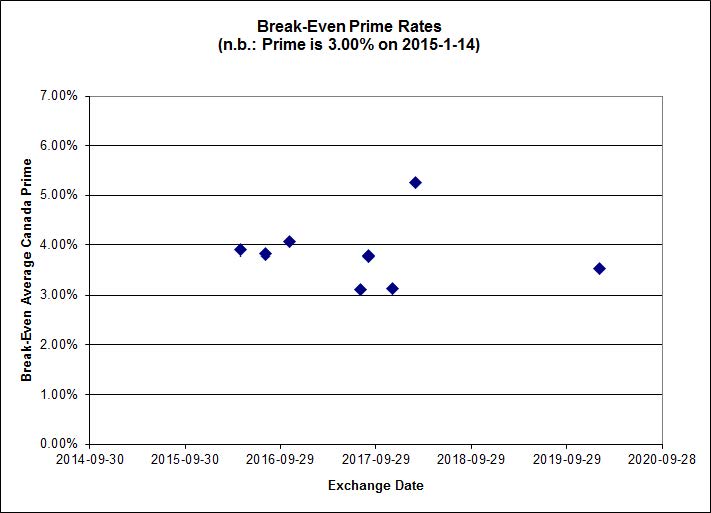

As one can see, this is a fairly modest hurdle, compared to that implied by other FixedFloater/RatchetRate Strong Pairs:

Click for Big

Given that there is a presumed immediate gain of $0.46 available by converting BCE.PR.F to BCE.PR.E and that the risk of this being reduced during the period between the decision date and the date that converters receive their replacement shares is small (since, all else being equal, a reduction in the price of BCE.PR.E implies a reduction in the Break-Even Prime Rate, which is already on the low side), I recommend that holders of BCE.PR.F convert to BCE.PR.E. Holders of BCE.PR.E should retain their shares.

Note that while the company requires notification of conversion prior to 5:00 p.m. (Eastern time) on January 19, 2015, brokerage houses will have deadlines a day or two in advance of the company deadline – so there’s not much time to waste!