“It doesn’t matter whether a cat is white or black, as long as it throws financial guys in jail after a crash“:

China’s brokerages tumbled after Citic Securities Co. executives were detained and people familiar with the matter said the industry was told to contribute another 100 billion yuan ($15.7 billion) to a market rescue fund.

Four executives of Citic including managing directors Xu Gang and Liu Wei, admitted alleged insider trading, the state-run Xinhua News Agency said. The nation’s largest brokerage fell as much as 8.6 percent in Shanghai and slid to the lowest since May 2014 in Hong Kong. A Citic press officer declined to comment.

The China Securities Regulatory Commission ordered the rescue-fund contributions at a meeting with 50 brokerages on Saturday that was attended by CSRC Chairman Xiao Gang, said the people, who asked not to be identified because the meeting hasn’t been made public. The regulator encouraged listed brokerages to buy back shares worth as much as 10 percent of their total market value, the people said.

Central bankers are feeling some angst:

Mario Draghi may have skipped the Federal Reserve’s Jackson Hole symposium this year, but he can’t dodge its conclusion: central banks can’t steer inflation as well as they thought.

Less than six months into a stimulus program that the European Central Bank president promised would revive consumer-price growth, the euro area is facing renewed disinflationary pressure as China’s economy slows and commodity prices slump. Inflation failed to pick up this month, data showed on Monday, and Draghi may have to downgrade the institution’s forecasts on Thursday.

The newest risk to prices highlights how in the 19-nation currency bloc — as in the U.S., the U.K. and other industrialized nations — headline inflation is still far below target even as the economy recovers.

…

At Jackson Hole, academics effectively delivered a beating to central banks’ confidence in their ability to predict and manage their key variable, by pointing out wide gaps in knowledge about how inflation works.Harvard University’s Gita Gopinath argued that the relationship between prices and exchange rates isn’t well understood. Boston University’s Simon Gilchrist said that strict inflation targeting can worsen economic outcomes.

Worse still, trying to influence inflation while not understanding it is a “recipe for disaster,” according to MIT Sloan School of Management professor Athanasios Orphanides, himself a former ECB Governing Council member.

I knew American universities were venal, but I didn’t know just how venal they could be:

Bank of America’s relationship with the university extends well beyond marketing at sports events. The bank has an $8.4 million, seven-year contract with Michigan State giving it access to students’ names and addresses and use of the university’s logo. The more students who take the banks’ credit cards, the more money the university gets. Under certain circumstances, Michigan State even stands to receive more money if students carry a balance on these cards.

…

The relationships are reminiscent of those uncovered two years ago between student loan companies and universities. In those, some lenders offered universities an incentive to steer potential borrowers their way.

In Friday’s post I mentioned some interesting things that are happening with barcodes and smartphones … these were interesting enough that I did some poking around.

The Global Food Safety Resource published an interesting article titled Food Regulatory Trends in 2015, which included the interesting note:

In December 2014, Guangdong province piloted an e-traceability system for baby formula. Consumers can use a mobile app and scan a barcode to get information about the product including it’s provenance. But it’s unique to Guangdong and doesn’t translate nationally.

The Grower, a specialty newsletter billing itself as ‘Canada’s Premier Horticultural Publication’, published an article titled How a celery swizzle stick meets its bar code in the field, which contains a bit of insight into Canada’s laws regarding food traceability and how this is implemented at the farm level.

GS1 Canada (the worldwide GS1 organization is mentioned in the Reuters article that got me interested) issued a statement titled Update On Loblaw And Wal-Mart GS1 DataBar™ Pilots (the GS1 Databar was used in one of the examples in the article) that stated:

In June 2006, Loblaw Companies Limited (Loblaw) and Wal-Mart Stores inc. (Wal-Mart) selected several suppliers to pilot the GS1 DataBar™ … on apples and bananas …

To date, Loblaw and Wal-Mart have attributed the following business benefits to their DataBar pilots:

•Decreased out-of-stocks

•Improved shrink control

•Enhanced product replenishment

•Increased customer satisfaction at self-checkouts

So on Saturday evening I visited my local Loblaws and looked at the apples and bananas and lo and behold! They all had GS1 Databars on them!

So it may be concluded that all the data is in place for consumer access to provenance information for apples and bananas at Loblaws. All that is needed is a smartphone App that will read and interpret the information and possibly access to Loblaw’s database – I’m not sure how much, if any, of the data is proprietary.

So you can bet that as soon as Loblaws thinks they can make a dollar out the proposition this traceability will be available – at least as far as Loblaw’s apples and bananas are concerned.

However, I’m not holding my breath waiting for the roll-out. As the comments to the Globe’s republished article so convincingly demonstrate, Canadians as a group are both mentally deficient and terrified of anything developed after 1973. But maybe there’s an App Developer out there who might like to steal a march on the big boys …

I was hoping for some definitive news today on the all-but-certain extensions of NPI.PR.A, FFH.PR.G and ALA.PR.A, which reset 2015-9-30, but there’s nothing.

The Canadian preferred share market closed the month with a good strong day, with PerpetualDiscounts gaining 13bp, FixedResets winning 56bp and DeemedRetractibles up 21bp. There is still a lot of churn in the market, as is demonstrated by yet another lengthy Performance Highlights table. Volume was extremely low.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

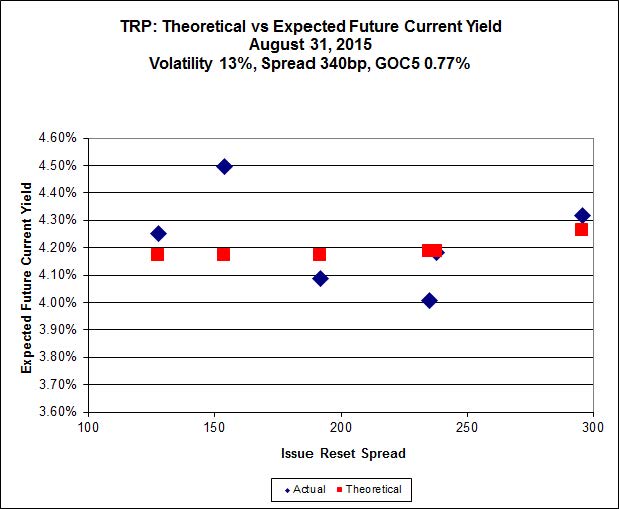

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.46 to be $0.82 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $1.00 cheap at its bid price of 12.85.

Click for Big

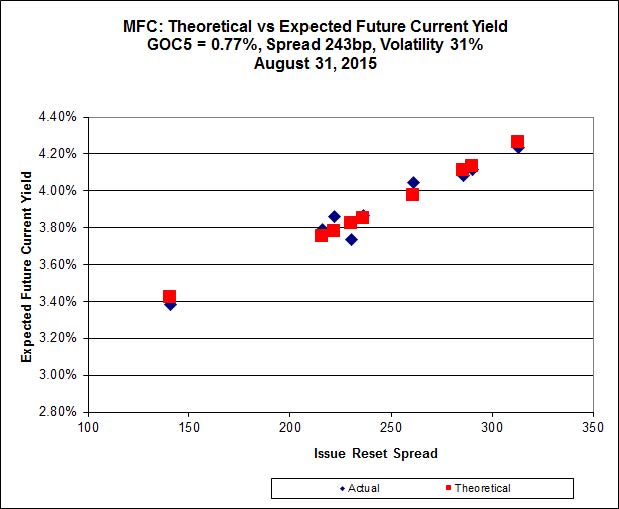

Another good fit today for MFC, with Implied Volatility dropping a bit again today.

Most expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 20.55 to be 0.48 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 19.37 to be 0.42 cheap.

Click for Big

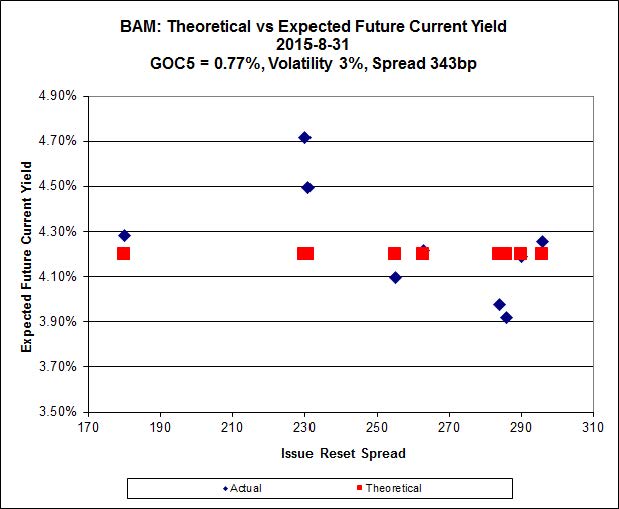

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.27 to be $2.00 cheap. BAM.PF.F, resetting at +286bp on 2019-9-30 is bid at 23.15 and appears to be $1.54 rich.

Click for Big

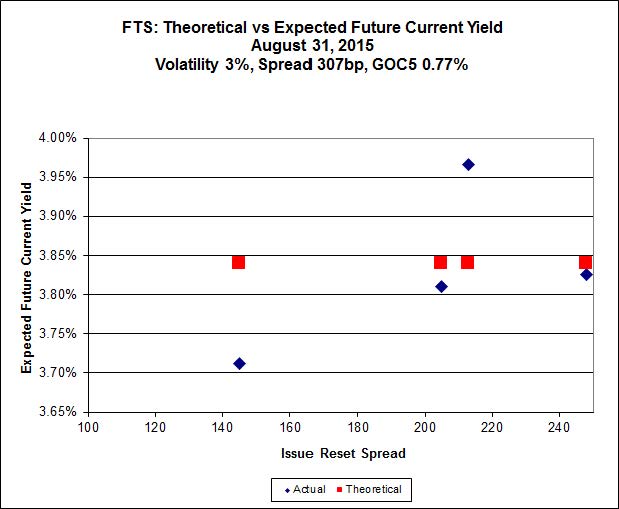

Implied Volatility declined precipitously today, illustrating the perils of relying too heavily on a four-point curve.

FTS.PR.H, with a spread of +145bp, and bid at 14.95, looks $0.50 expensive and resets 2020-6-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.28 and is $0.60 cheap.

Click for Big

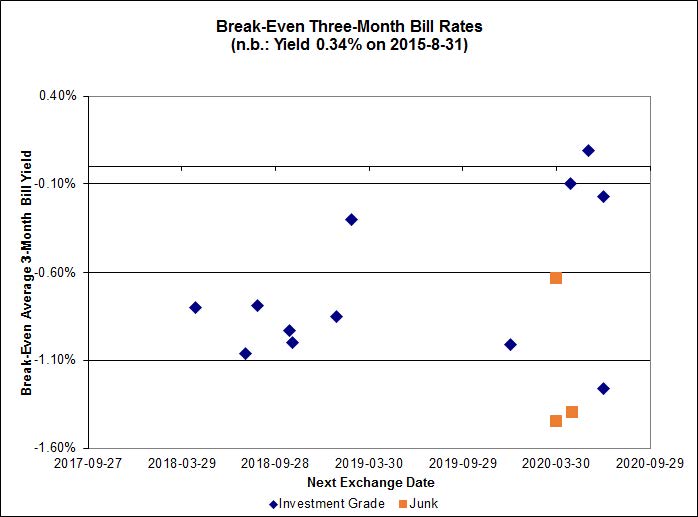

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.68%, with no outliers. Note that the distribution is bimodal, with NVCC non-compliant bank issues averaging -0.82% and the unregulated issues averaging -0.49%. There are two junk outliers below -1.60% and one two above +0.40%..

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.9201 % | 1,646.5 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.9201 % | 2,878.8 |

| Floater | 4.46 % | 4.53 % | 58,030 | 16.29 | 3 | 0.9201 % | 1,750.3 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3260 % | 2,774.9 |

| SplitShare | 4.64 % | 5.01 % | 58,636 | 3.11 | 3 | 0.3260 % | 3,252.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3260 % | 2,537.4 |

| Perpetual-Premium | 5.72 % | 5.67 % | 61,999 | 14.03 | 9 | 0.3319 % | 2,486.6 |

| Perpetual-Discount | 5.50 % | 5.57 % | 77,670 | 14.54 | 29 | 0.1270 % | 2,570.6 |

| FixedReset | 4.95 % | 4.35 % | 195,597 | 15.56 | 87 | 0.5555 % | 2,134.7 |

| Deemed-Retractible | 5.17 % | 5.26 % | 97,775 | 5.54 | 34 | 0.2128 % | 2,571.1 |

| FloatingReset | 2.36 % | 3.51 % | 45,996 | 5.95 | 9 | 0.2358 % | 2,191.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PWF.PR.L | Perpetual-Discount | -2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 22.63 Evaluated at bid price : 22.88 Bid-YTW : 5.63 % |

| SLF.PR.I | FixedReset | -2.43 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.72 Bid-YTW : 5.37 % |

| BMO.PR.Y | FixedReset | -2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 22.39 Evaluated at bid price : 23.20 Bid-YTW : 3.81 % |

| MFC.PR.L | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.33 Bid-YTW : 6.63 % |

| IFC.PR.C | FixedReset | -1.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.15 Bid-YTW : 6.39 % |

| PWF.PR.S | Perpetual-Discount | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 21.88 Evaluated at bid price : 22.16 Bid-YTW : 5.47 % |

| FTS.PR.G | FixedReset | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 18.28 Evaluated at bid price : 18.28 Bid-YTW : 4.15 % |

| ELF.PR.H | Perpetual-Discount | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 23.57 Evaluated at bid price : 24.02 Bid-YTW : 5.79 % |

| BMO.PR.K | Deemed-Retractible | 1.02 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-09-30 Maturity Price : 25.50 Evaluated at bid price : 25.85 Bid-YTW : -10.17 % |

| TRP.PR.F | FloatingReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 14.35 Evaluated at bid price : 14.35 Bid-YTW : 3.93 % |

| BMO.PR.W | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 20.73 Evaluated at bid price : 20.73 Bid-YTW : 3.79 % |

| GWO.PR.L | Deemed-Retractible | 1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.95 Bid-YTW : 5.65 % |

| ENB.PF.C | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 17.65 Evaluated at bid price : 17.65 Bid-YTW : 5.17 % |

| ENB.PF.A | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 17.45 Evaluated at bid price : 17.45 Bid-YTW : 5.24 % |

| BAM.PR.N | Perpetual-Discount | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 5.82 % |

| PWF.PR.T | FixedReset | 1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 22.72 Evaluated at bid price : 23.59 Bid-YTW : 3.44 % |

| ENB.PR.J | FixedReset | 1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 5.11 % |

| TD.PF.A | FixedReset | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 3.75 % |

| W.PR.H | Perpetual-Discount | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 24.05 Evaluated at bid price : 24.30 Bid-YTW : 5.74 % |

| HSE.PR.C | FixedReset | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 21.02 Evaluated at bid price : 21.02 Bid-YTW : 4.78 % |

| W.PR.J | Perpetual-Discount | 1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 24.06 Evaluated at bid price : 24.32 Bid-YTW : 5.84 % |

| BAM.PR.B | Floater | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 10.80 Evaluated at bid price : 10.80 Bid-YTW : 4.43 % |

| PVS.PR.D | SplitShare | 1.42 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 24.35 Bid-YTW : 5.01 % |

| TD.PF.B | FixedReset | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 3.74 % |

| FTS.PR.F | Perpetual-Discount | 1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 22.33 Evaluated at bid price : 22.60 Bid-YTW : 5.44 % |

| TRP.PR.C | FixedReset | 1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 12.85 Evaluated at bid price : 12.85 Bid-YTW : 4.53 % |

| NA.PR.S | FixedReset | 1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 21.24 Evaluated at bid price : 21.24 Bid-YTW : 3.92 % |

| NA.PR.W | FixedReset | 1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 20.53 Evaluated at bid price : 20.53 Bid-YTW : 3.90 % |

| BMO.PR.T | FixedReset | 1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 21.45 Evaluated at bid price : 21.45 Bid-YTW : 3.69 % |

| BAM.PF.B | FixedReset | 1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 20.16 Evaluated at bid price : 20.16 Bid-YTW : 4.45 % |

| BAM.PR.X | FixedReset | 1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 4.66 % |

| RY.PR.K | FloatingReset | 2.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.33 Bid-YTW : 3.39 % |

| ENB.PR.P | FixedReset | 2.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 16.20 Evaluated at bid price : 16.20 Bid-YTW : 5.26 % |

| HSE.PR.G | FixedReset | 2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 22.14 Evaluated at bid price : 22.75 Bid-YTW : 4.73 % |

| FTS.PR.J | Perpetual-Discount | 2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 21.69 Evaluated at bid price : 22.00 Bid-YTW : 5.41 % |

| ENB.PR.H | FixedReset | 2.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 14.85 Evaluated at bid price : 14.85 Bid-YTW : 5.16 % |

| MFC.PR.G | FixedReset | 2.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.29 Bid-YTW : 5.21 % |

| TRP.PR.G | FixedReset | 2.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 21.33 Evaluated at bid price : 21.60 Bid-YTW : 4.31 % |

| GWO.PR.S | Deemed-Retractible | 2.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.85 Bid-YTW : 5.31 % |

| ENB.PR.Y | FixedReset | 2.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 15.91 Evaluated at bid price : 15.91 Bid-YTW : 5.24 % |

| FTS.PR.M | FixedReset | 2.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 21.24 Evaluated at bid price : 21.24 Bid-YTW : 4.02 % |

| TRP.PR.A | FixedReset | 2.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 16.45 Evaluated at bid price : 16.45 Bid-YTW : 4.25 % |

| ENB.PR.F | FixedReset | 2.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 15.99 Evaluated at bid price : 15.99 Bid-YTW : 5.29 % |

| ENB.PR.B | FixedReset | 3.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 15.10 Evaluated at bid price : 15.10 Bid-YTW : 5.36 % |

| BAM.PF.F | FixedReset | 3.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 22.42 Evaluated at bid price : 23.15 Bid-YTW : 4.09 % |

| MFC.PR.N | FixedReset | 3.74 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.55 Bid-YTW : 5.93 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| HSB.PR.D | Deemed-Retractible | 261,800 | Scotia crossed blocks of 50,000 and 210,700, both at 24.95. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.90 Bid-YTW : 5.26 % |

| TRP.PR.D | FixedReset | 26,010 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 18.83 Evaluated at bid price : 18.83 Bid-YTW : 4.40 % |

| TD.PF.C | FixedReset | 23,150 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 3.73 % |

| ENB.PR.N | FixedReset | 19,420 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 16.56 Evaluated at bid price : 16.56 Bid-YTW : 5.31 % |

| ENB.PF.C | FixedReset | 19,180 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 17.65 Evaluated at bid price : 17.65 Bid-YTW : 5.17 % |

| ENB.PR.J | FixedReset | 18,900 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-31 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 5.11 % |

| There were 14 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.M | FixedReset | Quote: 20.25 – 22.30 Spot Rate : 2.0500 Average : 1.2798 YTW SCENARIO |

| BAM.PF.G | FixedReset | Quote: 22.70 – 24.12 Spot Rate : 1.4200 Average : 0.8188 YTW SCENARIO |

| BAM.PF.E | FixedReset | Quote: 20.27 – 21.80 Spot Rate : 1.5300 Average : 1.0370 YTW SCENARIO |

| RY.PR.M | FixedReset | Quote: 22.40 – 23.85 Spot Rate : 1.4500 Average : 1.0600 YTW SCENARIO |

| TRP.PR.E | FixedReset | Quote: 19.46 – 20.25 Spot Rate : 0.7900 Average : 0.5126 YTW SCENARIO |

| PWF.PR.L | Perpetual-Discount | Quote: 22.88 – 23.65 Spot Rate : 0.7700 Average : 0.5216 YTW SCENARIO |

Hi James,

I note that one of my favorite preferreds, BAM.PR.G, does not appear in your performance highlights table. It had a nearly 10% jump today on high volume (10,000 shares). Did you not include it because it has recently been suffering from liquidity problems?

That’s correct. It’s a real shame that BAM.PR.G and BAM.PR.E are both currently trading with an average daily turnover (as calculated using HIMIPref™ methodology, which seeks to minimize the influence of the occasional block trade) of less than $25,000.

What with the poor volume on these two issues and the poor credit on BCE, it means that the RatchetRate and FixedFloater subindices are almost always empty.

However, the jump today of over 10% in the BAM.PR.G bid price illustrates why I keep low-volume instruments out of the indices in the first place: when they trade by appointment only, the quotations aren’t very reliable.