We are approaching the end-game of the US Money Market Fund re-regulation:

With a seismic overhaul of the $2.6 trillion money-market industry weeks away from kicking in, money managers are bracing for a last-minute exodus of as much as $300 billion from funds in regulators’ cross hairs.

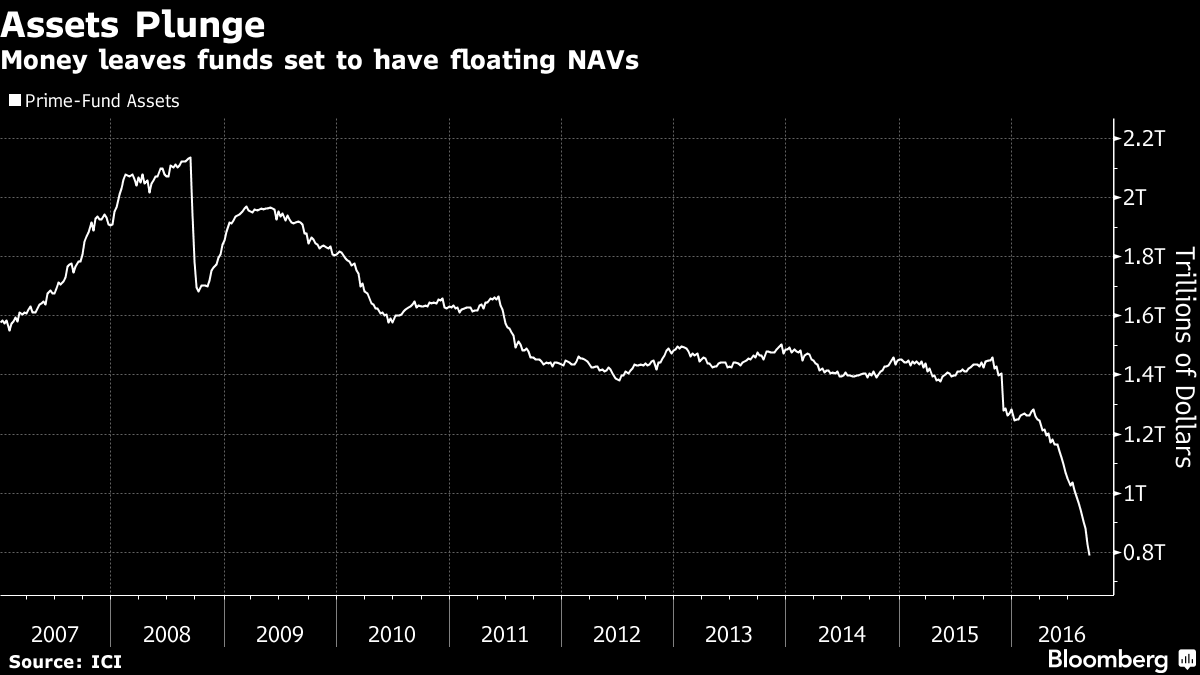

Prime funds, which seek higher yields by buying securities like commercial paper, are at the center of the upheaval. Their assets have already plunged by almost $700 billion since the start of 2015, to $789 billion, Investment Company Institute data show. The outflow has rippled across financial markets, shattering demand for banks’ and other companies’ short-term debt and raising their funding costs.

The transformation of the money-fund industry, where investors turn to park cash, is a result of regulators’ efforts to make the financial system safer in the aftermath of the credit crisis. The key date is Oct. 14, when rules take effect mandating that institutional prime and tax-exempt funds end an over-30-year tradition of fixing shares at $1. Funds that hold only government debt will be able to maintain that level. Companies such as Federated Investors Inc. and Fidelity Investments, which have already reduced or altered prime offerings, are preparing in case investors yank more money as the new era approaches.

…

A major repercussion of the flight from prime funds is that there’s less money flowing into commercial paper and certificates of deposit, which banks depend on for funding. As a result, banks’ unsecured lending rates, such as the dollar London interbank offered rate, have soared. Three-month Libor reached about 0.86 percent Tuesday, the highest since 2009.

Click for Big

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.6155 % | 1,690.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.6155 % | 3,088.0 |

| Floater | 4.89 % | 4.61 % | 88,507 | 16.24 | 4 | 0.6155 % | 1,779.6 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1749 % | 2,873.0 |

| SplitShare | 5.07 % | 4.72 % | 73,931 | 2.19 | 5 | -0.1749 % | 3,431.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1749 % | 2,677.0 |

| Perpetual-Premium | 5.51 % | 4.64 % | 68,955 | 1.98 | 12 | -0.1530 % | 2,671.4 |

| Perpetual-Discount | 5.15 % | 5.17 % | 100,156 | 15.09 | 26 | -0.0359 % | 2,895.6 |

| FixedReset | 5.01 % | 4.50 % | 153,014 | 6.95 | 91 | -0.0695 % | 2,029.1 |

| Deemed-Retractible | 5.03 % | 4.04 % | 118,542 | 0.37 | 32 | -0.0673 % | 2,795.0 |

| FloatingReset | 2.83 % | 3.99 % | 26,983 | 5.02 | 12 | -0.0393 % | 2,203.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.F | FloatingReset | -2.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 13.38 Evaluated at bid price : 13.38 Bid-YTW : 4.56 % |

| CU.PR.C | FixedReset | -2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 18.07 Evaluated at bid price : 18.07 Bid-YTW : 4.37 % |

| PWF.PR.T | FixedReset | -1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 19.47 Evaluated at bid price : 19.47 Bid-YTW : 4.19 % |

| IFC.PR.C | FixedReset | -1.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.30 Bid-YTW : 8.62 % |

| MFC.PR.N | FixedReset | -1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.13 Bid-YTW : 7.97 % |

| VNR.PR.A | FixedReset | -1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 18.24 Evaluated at bid price : 18.24 Bid-YTW : 4.98 % |

| TRP.PR.G | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 20.07 Evaluated at bid price : 20.07 Bid-YTW : 4.64 % |

| GWO.PR.N | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.17 Bid-YTW : 9.82 % |

| BAM.PF.F | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 19.93 Evaluated at bid price : 19.93 Bid-YTW : 4.68 % |

| BAM.PF.G | FixedReset | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 20.29 Evaluated at bid price : 20.29 Bid-YTW : 4.62 % |

| BAM.PR.Z | FixedReset | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 19.15 Evaluated at bid price : 19.15 Bid-YTW : 4.93 % |

| BAM.PF.A | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 19.15 Evaluated at bid price : 19.15 Bid-YTW : 4.85 % |

| BAM.PR.K | Floater | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 10.29 Evaluated at bid price : 10.29 Bid-YTW : 4.59 % |

| BAM.PF.E | FixedReset | 1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 18.91 Evaluated at bid price : 18.91 Bid-YTW : 4.63 % |

| BAM.PF.B | FixedReset | 1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 17.94 Evaluated at bid price : 17.94 Bid-YTW : 4.85 % |

| BAM.PR.R | FixedReset | 1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 15.45 Evaluated at bid price : 15.45 Bid-YTW : 4.89 % |

| BAM.PR.X | FixedReset | 2.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 13.50 Evaluated at bid price : 13.50 Bid-YTW : 4.79 % |

| BAM.PR.T | FixedReset | 2.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 15.45 Evaluated at bid price : 15.45 Bid-YTW : 4.99 % |

| BAM.PR.S | FloatingReset | 3.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 14.70 Evaluated at bid price : 14.70 Bid-YTW : 4.80 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.H | FixedReset | 663,207 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.47 Bid-YTW : 4.51 % |

| BAM.PF.C | Perpetual-Discount | 166,291 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 22.58 Evaluated at bid price : 22.90 Bid-YTW : 5.29 % |

| FTS.PR.H | FixedReset | 132,900 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 13.75 Evaluated at bid price : 13.75 Bid-YTW : 4.07 % |

| TD.PF.G | FixedReset | 115,200 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-30 Maturity Price : 25.00 Evaluated at bid price : 26.75 Bid-YTW : 4.01 % |

| BMO.PR.Z | Perpetual-Premium | 84,833 | YTW SCENARIO Maturity Type : Call Maturity Date : 2024-08-25 Maturity Price : 25.00 Evaluated at bid price : 25.49 Bid-YTW : 4.77 % |

| TD.PF.A | FixedReset | 66,700 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-09-13 Maturity Price : 18.40 Evaluated at bid price : 18.40 Bid-YTW : 4.28 % |

| There were 46 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| IFC.PR.A | FixedReset | Quote: 15.24 – 15.75 Spot Rate : 0.5100 Average : 0.2929 YTW SCENARIO |

| TRP.PR.F | FloatingReset | Quote: 13.38 – 13.90 Spot Rate : 0.5200 Average : 0.3269 YTW SCENARIO |

| TRP.PR.H | FloatingReset | Quote: 10.45 – 10.95 Spot Rate : 0.5000 Average : 0.3902 YTW SCENARIO |

| PVS.PR.B | SplitShare | Quote: 24.78 – 25.09 Spot Rate : 0.3100 Average : 0.2153 YTW SCENARIO |

| MFC.PR.F | FixedReset | Quote: 13.32 – 13.59 Spot Rate : 0.2700 Average : 0.1876 YTW SCENARIO |

| POW.PR.B | Perpetual-Discount | Quote: 25.06 – 25.27 Spot Rate : 0.2100 Average : 0.1436 YTW SCENARIO |