The downside of the elimination of bankruptcy law as it relates to banks is becoming apparent:

But after studying the proposals, National Bank Financial analyst Peter Routledge found that, under the new rules, commmon shareholders should be much more concerned, because they are quickly treated as collateral damage under the new regime. Should a new crisis emerge, common shareholders could be quickly wiped out, and that could rewrite the survival playbook.

Employing standard banking assumptions about leverage ratios and balance sheet sizes, Mr. Routledge discovered that just a 6 per cent drop in asset values, possibly from writing down a loan book and securities portfolio, would deplete a bank’s common equity capital. Because the bank’s existing common shareholders would then be wiped out, the preferred shareholders and bondholders would have their securities converted into common shares – making them the bank’s new owners.

Under the old rules, governments tried their best to protect common shareholders by setting up bailout schemes such as the Troubled Asset Relief Program, which purchased preferred shares and took toxic debt off of bank balance sheets, but did not upend the common equity investor base.

Mr. Routledge worries too few people appreciate just how easy it is to wipe out the existing shareholders under the proposed rules. When people start to realize this, possibly during the next crisis, he fears it will have disastrous implications for troubled banks.

Debt reduction through austerity reduces spending and thus slows growth; slower growth reduces incoming revenues and thus limits the ability to reduce debt.

This is a factor in the stubborn lack of global capital investment that has been limiting economic expansion – and Canada is no exception.

Standard & Poor’s on Monday pointed a finger at consumer debt as it lowered its 2014 growth forecast for the Canadian economy to 2.3 per cent from 2.5 per cent.

“Consumers might still be postponing purchases, worried about the heavy debt burdens they built up in the past decade, and this could be short-circuiting the growth we normally see in recoveries,” said S&P global fixed income analyst Robert Palombi. Without that consumer pick-up, he said, businesses lack a key catalyst to invest in expansion, which in turn has stifled employment growth.

New OSFI honcho Jeremy Rudin gave a speech to the Economic Club of Canada but didn’t say anything of interest.

The ruble’s in trouble:

Prospects Russia is considering capital controls amid the worst performance in emerging markets for the nation’s bonds and currency sent the ruble tumbling past the level at which the central bank said it would step in.

The ruble temporarily slid beyond 44.40 against the Bank of Russia’s basket of dollars and euros after two officials said policy makers are considering temporary restrictions if net outflows rise significantly. It pared declines after the central bank said it isn’t considering limits on cross-border capital movements. The yield on 10-year bonds rose six basis points to 9.42 percent, bringing this quarter’s increase to 102 basis points. The Micex Index pared its first gain in four days.

Reimposing restrictions on the flow of money that were abandoned eight years ago threatens to worsen a selloff in Russian assets that has gained momentum as the U.S. and European Union expanded sanctions over the conflict in Ukraine. The ruble slid 14 percent versus the dollar this quarter, breaking record lows in the past three days.

“Capital outflows should sharply increase now,” Stanislav Kopylov, who helps manage 45 billion rubles ($1.14 billion) at UralSib Asset Management in Moscow, said by phone from Moscow. “When you’re threatened like that, you need to urgently pull out the cash.”

And so much for Putin’s grandiose dreams of having a reserve currency:

After proclaiming in 2007 that the ruble was poised to become a haven for global investors, the Russian leader has watched it fade, a victim of his nation’s stagnating economy since the land grab in Ukraine. Now so much money is leaving Russia that its central bank is considering temporary capital controls, according to two officials with direct knowledge of the discussions.

The ruble’s share of global trading dropped to 0.4 percent from 0.6 percent since 2012, falling five places to rank 18th most-traded in the world, while the yuan tripled to 1.5 percent, according to the Society for Worldwide Interbank Financial Telecommunication, or SWIFT. Even as protests in Hong Kong this week challenged China’s leadership, direct trading began between the yuan and the euro, capping a year in which trade with European Union nations grew 12 percent.

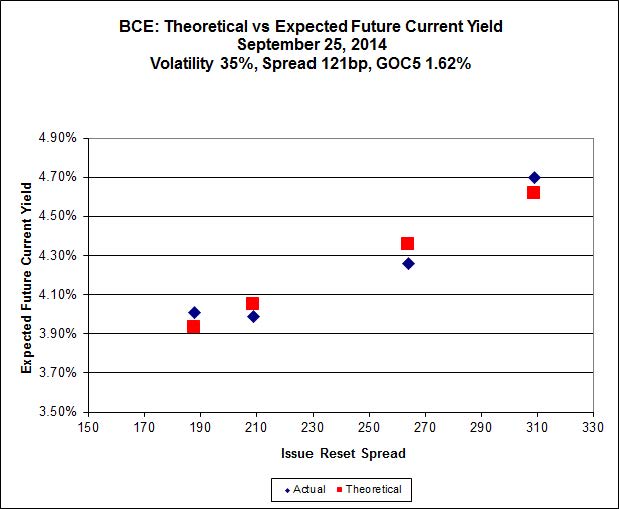

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts gaining 2bp, FixedResets up 8bp and DeemedRetractibles off 1bp. Volatility was low. Volume was low.

Now to figure out why PrefInfo isn’t working.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1783 % | 2,680.0 |

| FixedFloater | 4.20 % | 3.46 % | 24,464 | 18.41 | 1 | 0.0000 % | 4,127.3 |

| Floater | 2.89 % | 3.01 % | 63,851 | 19.70 | 4 | -0.1783 % | 2,771.4 |

| OpRet | 4.05 % | 2.18 % | 93,842 | 0.08 | 1 | 0.0000 % | 2,729.2 |

| SplitShare | 4.28 % | 3.63 % | 100,021 | 3.87 | 5 | 0.1978 % | 3,161.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,495.6 |

| Perpetual-Premium | 5.49 % | 2.53 % | 75,479 | 0.08 | 20 | -0.0650 % | 2,443.9 |

| Perpetual-Discount | 5.29 % | 5.17 % | 103,207 | 15.16 | 16 | 0.0190 % | 2,589.8 |

| FixedReset | 4.21 % | 3.75 % | 177,244 | 8.47 | 74 | 0.0813 % | 2,555.8 |

| Deemed-Retractible | 5.01 % | 2.21 % | 104,719 | 0.40 | 42 | -0.0105 % | 2,561.5 |

| FloatingReset | 2.56 % | -5.17 % | 79,595 | 0.08 | 6 | 0.1761 % | 2,541.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| CM.PR.D | Perpetual-Premium | -1.50 % | Called for redemption October 31 YTW SCENARIO Maturity Type : Call Maturity Date : 2014-10-30 Maturity Price : 25.00 Evaluated at bid price : 24.97 Bid-YTW : 1.47 % |

| PWF.PR.P | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-09-30 Maturity Price : 22.70 Evaluated at bid price : 23.15 Bid-YTW : 3.57 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BMO.PR.W | FixedReset | 117,600 | Desjardins crossed two blocks of 50,000 each, both at 25.13. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-09-30 Maturity Price : 23.18 Evaluated at bid price : 25.08 Bid-YTW : 3.72 % |

| BMO.PR.T | FixedReset | 63,200 | TD crossed 25,000 at 25.30. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-09-30 Maturity Price : 23.26 Evaluated at bid price : 25.30 Bid-YTW : 3.75 % |

| CM.PR.E | Perpetual-Premium | 57,899 | NVCC like CM.PR.D, which has been Called for redemption October 31 YTW SCENARIO Maturity Type : Call Maturity Date : 2014-10-30 Maturity Price : 25.00 Evaluated at bid price : 25.12 Bid-YTW : -5.75 % |

| TD.PR.O | Deemed-Retractible | 57,750 | Called for redemption October 31. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.27 Bid-YTW : 1.65 % |

| FTS.PR.M | FixedReset | 57,290 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2019-12-01 Maturity Price : 25.00 Evaluated at bid price : 25.25 Bid-YTW : 3.93 % |

| BNS.PR.Y | FixedReset | 54,870 | TD crossed 49,300 at 24.02. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.01 Bid-YTW : 3.44 % |

| There were 24 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| IAG.PR.A | Deemed-Retractible | Quote: 22.90 – 23.22 Spot Rate : 0.3200 Average : 0.2208 YTW SCENARIO |

| BNS.PR.N | Deemed-Retractible | Quote: 26.15 – 26.37 Spot Rate : 0.2200 Average : 0.1298 YTW SCENARIO |

| CU.PR.E | Perpetual-Discount | Quote: 24.20 – 24.45 Spot Rate : 0.2500 Average : 0.1667 YTW SCENARIO |

| IFC.PR.A | FixedReset | Quote: 23.70 – 24.00 Spot Rate : 0.3000 Average : 0.2182 YTW SCENARIO |

| GWO.PR.H | Deemed-Retractible | Quote: 23.60 – 23.90 Spot Rate : 0.3000 Average : 0.2260 YTW SCENARIO |

| IFC.PR.C | FixedReset | Quote: 25.49 – 25.72 Spot Rate : 0.2300 Average : 0.1560 YTW SCENARIO |