It’s nice to see a little high-level push-back against civil forfeiture:

Q: What reforms would help fix the flaws in the law?

A: I’m working to draft bipartisan reforms to fix these flaws. For starters, the direct quid pro quo between asset forfeiture and funding should be eliminated. Law enforcement shouldn’t be relying on funds obtained from forfeiting the particular assets that they have seized or shift crime-fighting priorities based on financial considerations. In addition, real procedural reforms must be enacted for people whose assets are seized, including prompt timelines for government action and the ability to challenge the seizure promptly before a judge. And, individuals who cannot afford a lawyer to guide them through the system should be provided one. Part of addressing this problem lies in reversing the Supreme Court’s recent decision that allows the government to prevent people from showing that they need access to their seized funds to hire a lawyer. We also need to codify changes in the use of civil asset forfeiture in structuring cases, where small business owners like Iowa’s Carole Hinders get unfairly caught up in forfeiture for depositing money in a bank without any indication of any underlying crime. The government’s burden of proof for forfeiting assets needs to be raised.

It’s clear the current process isn’t working as Congress intended. It is time to end seizure for suspicion’s sake and enact reforms that will help restore the proper mission of asset forfeiture laws and rebuild credibility in our law enforcement agencies.

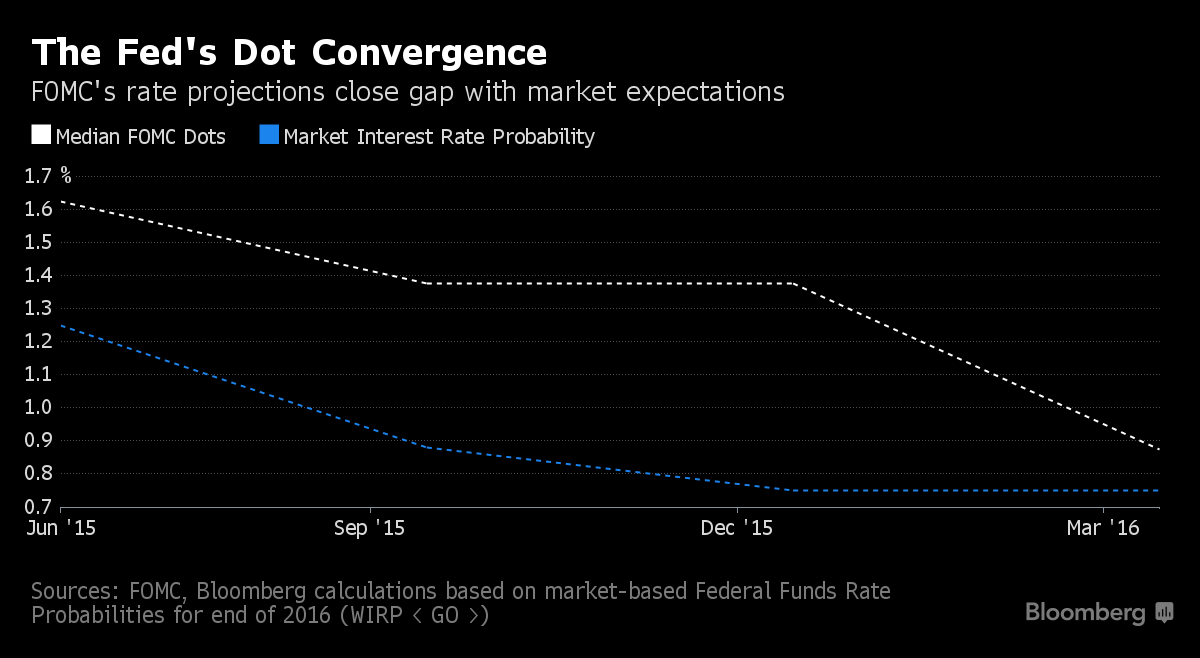

Market and Fed policy rate expectations are converging:

The Federal Reserve looks to have outsourced monetary policy to the financial markets — and that may not necessarily be bad.

Fed Chair Janet Yellen told the Economic Club of New York on Tuesday that policy makers had scaled back the number of interest rate increases they expect to carry out this year after investors did the same.

She argued that the downgrading of rate expectations in the market had led to lower bond yields, providing the economy with needed support in the face of weaker growth overseas. The Fed then followed suit this month by reducing its anticipated rate hikes in 2016 to two from four quarter-percentage point moves projected in December.

Click for Big

PerpetualDiscounts now yield 5.63%, equivalent to 7.32% interest at the standard conversion factor of 1.3x. Long corporates now yield about 4.1%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 320bp, unchanged from the figure reported March 23.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.00 % | 6.08 % | 11,039 | 16.60 | 1 | 1.8854 % | 1,571.9 |

| FixedFloater | 6.86 % | 6.03 % | 24,847 | 16.26 | 1 | 1.0949 % | 2,898.4 |

| Floater | 4.63 % | 4.76 % | 62,625 | 15.93 | 4 | -1.3050 % | 1,672.7 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2997 % | 2,791.1 |

| SplitShare | 4.75 % | 5.27 % | 88,709 | 1.61 | 6 | 0.2997 % | 3,266.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2997 % | 2,548.3 |

| Perpetual-Premium | 5.79 % | -4.49 % | 89,184 | 0.08 | 6 | -0.2039 % | 2,560.5 |

| Perpetual-Discount | 5.61 % | 5.63 % | 94,587 | 14.39 | 33 | 0.1798 % | 2,592.5 |

| FixedReset | 5.31 % | 4.81 % | 184,776 | 13.94 | 87 | -0.3188 % | 1,921.6 |

| Deemed-Retractible | 5.20 % | 5.55 % | 130,740 | 5.08 | 34 | 0.1698 % | 2,617.8 |

| FloatingReset | 3.04 % | 5.04 % | 37,342 | 5.39 | 16 | -0.1836 % | 2,018.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.I | FloatingReset | -4.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 11.00 Evaluated at bid price : 11.00 Bid-YTW : 4.49 % |

| TD.PR.S | FixedReset | -3.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.61 Bid-YTW : 4.78 % |

| TRP.PR.G | FixedReset | -3.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 18.61 Evaluated at bid price : 18.61 Bid-YTW : 5.02 % |

| HSE.PR.A | FixedReset | -2.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 10.35 Evaluated at bid price : 10.35 Bid-YTW : 5.93 % |

| TRP.PR.B | FixedReset | -2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 10.99 Evaluated at bid price : 10.99 Bid-YTW : 4.62 % |

| BAM.PR.T | FixedReset | -1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 15.45 Evaluated at bid price : 15.45 Bid-YTW : 5.02 % |

| HSE.PR.E | FixedReset | -1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 18.41 Evaluated at bid price : 18.41 Bid-YTW : 5.91 % |

| TRP.PR.D | FixedReset | -1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 16.96 Evaluated at bid price : 16.96 Bid-YTW : 4.76 % |

| TRP.PR.C | FixedReset | -1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 11.61 Evaluated at bid price : 11.61 Bid-YTW : 4.84 % |

| CIU.PR.C | FixedReset | -1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 11.06 Evaluated at bid price : 11.06 Bid-YTW : 4.71 % |

| TRP.PR.A | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 15.05 Evaluated at bid price : 15.05 Bid-YTW : 4.59 % |

| BAM.PR.X | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 14.00 Evaluated at bid price : 14.00 Bid-YTW : 4.73 % |

| IAG.PR.G | FixedReset | -1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.85 Bid-YTW : 7.56 % |

| BNS.PR.Q | FixedReset | -1.56 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.67 Bid-YTW : 4.92 % |

| BAM.PR.K | Floater | -1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 9.90 Evaluated at bid price : 9.90 Bid-YTW : 4.78 % |

| BAM.PR.B | Floater | -1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 9.94 Evaluated at bid price : 9.94 Bid-YTW : 4.76 % |

| GWO.PR.N | FixedReset | -1.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.35 Bid-YTW : 10.29 % |

| RY.PR.I | FixedReset | -1.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.26 Bid-YTW : 4.54 % |

| TRP.PR.E | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 17.75 Evaluated at bid price : 17.75 Bid-YTW : 4.62 % |

| RY.PR.K | FloatingReset | -1.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.85 Bid-YTW : 4.87 % |

| PWF.PR.A | Floater | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 11.10 Evaluated at bid price : 11.10 Bid-YTW : 4.30 % |

| BIP.PR.B | FixedReset | -1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 22.86 Evaluated at bid price : 24.15 Bid-YTW : 5.66 % |

| NA.PR.S | FixedReset | -1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 18.15 Evaluated at bid price : 18.15 Bid-YTW : 4.57 % |

| MFC.PR.I | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.83 Bid-YTW : 7.67 % |

| CU.PR.C | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 17.51 Evaluated at bid price : 17.51 Bid-YTW : 4.55 % |

| HSE.PR.G | FixedReset | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 18.44 Evaluated at bid price : 18.44 Bid-YTW : 5.89 % |

| BAM.PR.G | FixedFloater | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 25.00 Evaluated at bid price : 13.85 Bid-YTW : 6.03 % |

| RY.PR.F | Deemed-Retractible | 1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.67 Bid-YTW : 4.82 % |

| BAM.PF.G | FixedReset | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 19.65 Evaluated at bid price : 19.65 Bid-YTW : 4.81 % |

| PVS.PR.D | SplitShare | 1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 23.51 Bid-YTW : 5.87 % |

| PWF.PR.Q | FloatingReset | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 11.25 Evaluated at bid price : 11.25 Bid-YTW : 4.60 % |

| FTS.PR.H | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 12.79 Evaluated at bid price : 12.79 Bid-YTW : 4.40 % |

| W.PR.K | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 23.16 Evaluated at bid price : 24.95 Bid-YTW : 5.18 % |

| FTS.PR.I | FloatingReset | 1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 10.50 Evaluated at bid price : 10.50 Bid-YTW : 4.54 % |

| MFC.PR.F | FixedReset | 1.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.21 Bid-YTW : 10.47 % |

| BAM.PR.E | Ratchet | 1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 25.00 Evaluated at bid price : 13.51 Bid-YTW : 6.08 % |

| PWF.PR.T | FixedReset | 2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 4.22 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.R | FixedReset | 87,594 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-08-24 Maturity Price : 25.00 Evaluated at bid price : 25.96 Bid-YTW : 4.79 % |

| BNS.PR.N | Deemed-Retractible | 67,005 | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-01-27 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : 4.86 % |

| RY.PR.Z | FixedReset | 60,289 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-30 Maturity Price : 18.51 Evaluated at bid price : 18.51 Bid-YTW : 4.22 % |

| RY.PR.D | Deemed-Retractible | 59,461 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.90 Bid-YTW : 4.69 % |

| TD.PF.G | FixedReset | 56,716 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-30 Maturity Price : 25.00 Evaluated at bid price : 25.87 Bid-YTW : 5.01 % |

| BNS.PR.L | Deemed-Retractible | 39,093 | YTW SCENARIO Maturity Type : Call Maturity Date : 2016-05-27 Maturity Price : 25.00 Evaluated at bid price : 25.24 Bid-YTW : 3.14 % |

| There were 49 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| GWO.PR.O | FloatingReset | Quote: 12.01 – 14.25 Spot Rate : 2.2400 Average : 1.7176 YTW SCENARIO |

| TD.PR.S | FixedReset | Quote: 22.61 – 23.77 Spot Rate : 1.1600 Average : 0.8311 YTW SCENARIO |

| SLF.PR.J | FloatingReset | Quote: 12.30 – 13.00 Spot Rate : 0.7000 Average : 0.4251 YTW SCENARIO |

| TD.PR.Z | FloatingReset | Quote: 21.32 – 22.00 Spot Rate : 0.6800 Average : 0.5336 YTW SCENARIO |

| IAG.PR.G | FixedReset | Quote: 18.85 – 19.30 Spot Rate : 0.4500 Average : 0.3204 YTW SCENARIO |

| BAM.PR.G | FixedFloater | Quote: 13.85 – 14.24 Spot Rate : 0.3900 Average : 0.2611 YTW SCENARIO |