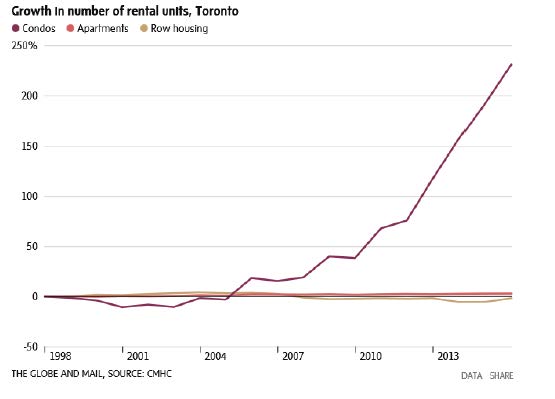

There were two charts I found particularly interesting in a Globe “Explainer” regarding Ontario’s proposed housing legislation.

The first provides a historical count of rental units by type:

Click for Big

That’s as good an explanation as any of the benefits that rent control brings.

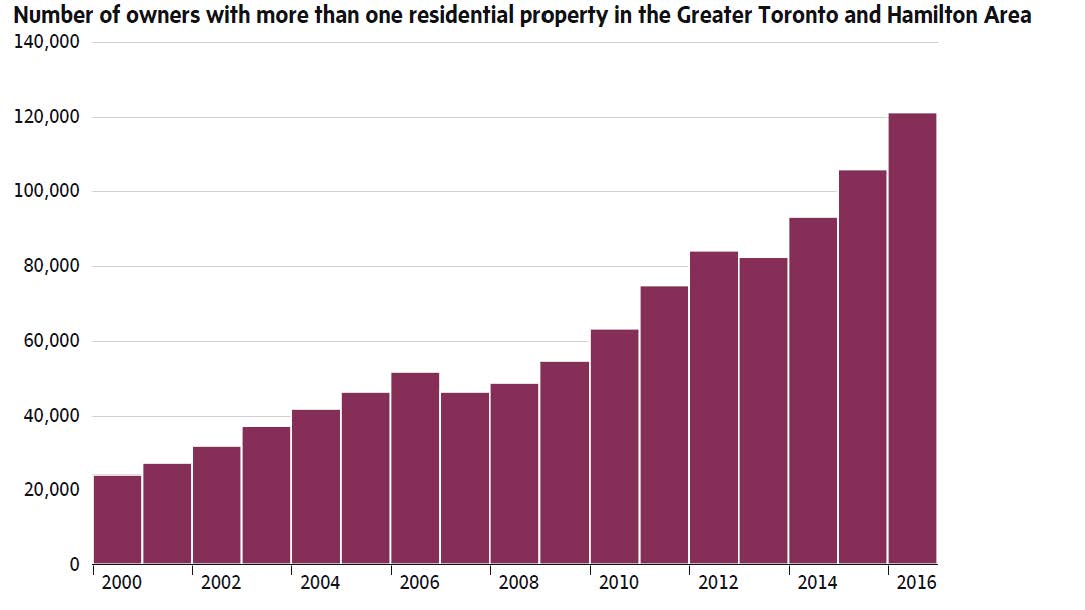

The second is a historical accounting of individuals owning multiple properties in the region:

Click for big

That’s as good an explanation as any of the effect of poor stock market returns on the housing market; an effect which is exacerbated by low interest rates.

Meanwhile, it was a pretty nasty day for preferred shares. There was no major change in bond yields today, so I suppose we’ll just have to put this one down as a delayed reaction. TXPR was rebalancing today; it is obvious that this might lead to high volume, but an influence on direction is less clear.

The TXPR Total Return Index is now slightly negative for the month. The smoothness of today’s decline makes me suspect the day’s action was due to selling from one big player … but that is merely speculation!

Click for Big

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.8226 % | 2,108.1 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.8226 % | 3,868.3 |

| Floater | 3.62 % | 3.70 % | 44,543 | 18.07 | 4 | -1.8226 % | 2,229.3 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0718 % | 3,021.5 |

| SplitShare | 4.94 % | 4.16 % | 53,625 | 0.62 | 6 | -0.0718 % | 3,608.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0718 % | 2,815.4 |

| Perpetual-Premium | 5.32 % | -4.52 % | 76,129 | 0.09 | 23 | -0.4174 % | 2,775.7 |

| Perpetual-Discount | 5.14 % | 5.15 % | 109,947 | 15.24 | 13 | -1.1773 % | 2,962.1 |

| FixedReset | 4.42 % | 3.98 % | 233,655 | 6.59 | 94 | -0.7985 % | 2,341.9 |

| Deemed-Retractible | 5.03 % | 0.99 % | 144,964 | 0.09 | 31 | -0.6241 % | 2,874.4 |

| FloatingReset | 2.57 % | 3.13 % | 56,874 | 4.51 | 9 | -0.7209 % | 2,522.5 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.F | FloatingReset | -5.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 18.13 Evaluated at bid price : 18.13 Bid-YTW : 3.47 % |

| BAM.PR.K | Floater | -3.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 12.61 Evaluated at bid price : 12.61 Bid-YTW : 3.77 % |

| HSE.PR.A | FixedReset | -2.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 15.71 Evaluated at bid price : 15.71 Bid-YTW : 4.33 % |

| IAG.PR.G | FixedReset | -2.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.40 Bid-YTW : 5.62 % |

| MFC.PR.J | FixedReset | -2.81 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.46 Bid-YTW : 5.39 % |

| MFC.PR.G | FixedReset | -2.71 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.99 Bid-YTW : 5.26 % |

| PWF.PR.S | Perpetual-Discount | -2.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 22.93 Evaluated at bid price : 23.33 Bid-YTW : 5.14 % |

| BAM.PR.M | Perpetual-Discount | -2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 22.34 Evaluated at bid price : 22.61 Bid-YTW : 5.29 % |

| MFC.PR.N | FixedReset | -2.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.50 Bid-YTW : 5.87 % |

| BAM.PF.C | Perpetual-Discount | -2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 22.49 Evaluated at bid price : 22.82 Bid-YTW : 5.35 % |

| BAM.PR.N | Perpetual-Discount | -2.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 22.30 Evaluated at bid price : 22.57 Bid-YTW : 5.30 % |

| MFC.PR.K | FixedReset | -2.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.86 Bid-YTW : 6.15 % |

| VNR.PR.A | FixedReset | -2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 21.23 Evaluated at bid price : 21.23 Bid-YTW : 4.57 % |

| BAM.PR.C | Floater | -2.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 12.66 Evaluated at bid price : 12.66 Bid-YTW : 3.76 % |

| SLF.PR.D | Deemed-Retractible | -2.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.17 Bid-YTW : 6.39 % |

| BAM.PF.D | Perpetual-Discount | -2.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 22.96 Evaluated at bid price : 23.35 Bid-YTW : 5.28 % |

| PWF.PR.L | Perpetual-Premium | -2.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 24.26 Evaluated at bid price : 24.56 Bid-YTW : 5.20 % |

| POW.PR.D | Perpetual-Discount | -2.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 24.15 Evaluated at bid price : 24.40 Bid-YTW : 5.15 % |

| SLF.PR.C | Deemed-Retractible | -1.99 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.21 Bid-YTW : 6.36 % |

| MFC.PR.F | FixedReset | -1.98 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.38 Bid-YTW : 9.44 % |

| BAM.PR.R | FixedReset | -1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 19.41 Evaluated at bid price : 19.41 Bid-YTW : 4.25 % |

| SLF.PR.A | Deemed-Retractible | -1.96 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.50 Bid-YTW : 5.79 % |

| BAM.PR.Z | FixedReset | -1.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 22.55 Evaluated at bid price : 23.17 Bid-YTW : 4.34 % |

| SLF.PR.I | FixedReset | -1.91 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.10 Bid-YTW : 5.04 % |

| BAM.PF.B | FixedReset | -1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 22.09 Evaluated at bid price : 22.38 Bid-YTW : 4.17 % |

| MFC.PR.L | FixedReset | -1.88 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.85 Bid-YTW : 6.22 % |

| BAM.PR.T | FixedReset | -1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 19.63 Evaluated at bid price : 19.63 Bid-YTW : 4.35 % |

| MFC.PR.H | FixedReset | -1.85 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.47 Bid-YTW : 4.58 % |

| MFC.PR.I | FixedReset | -1.81 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.84 Bid-YTW : 5.38 % |

| SLF.PR.E | Deemed-Retractible | -1.80 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.32 Bid-YTW : 6.34 % |

| SLF.PR.H | FixedReset | -1.72 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.40 Bid-YTW : 6.79 % |

| TD.PF.B | FixedReset | -1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 21.40 Evaluated at bid price : 21.73 Bid-YTW : 3.86 % |

| NA.PR.S | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 21.61 Evaluated at bid price : 22.03 Bid-YTW : 3.95 % |

| MFC.PR.B | Deemed-Retractible | -1.65 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.25 Bid-YTW : 5.88 % |

| BAM.PF.A | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 22.83 Evaluated at bid price : 23.27 Bid-YTW : 4.28 % |

| BAM.PF.E | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 21.95 Evaluated at bid price : 22.26 Bid-YTW : 4.18 % |

| W.PR.M | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-15 Maturity Price : 25.00 Evaluated at bid price : 26.00 Bid-YTW : 4.26 % |

| NA.PR.W | FixedReset | -1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 21.45 Evaluated at bid price : 21.45 Bid-YTW : 3.94 % |

| BAM.PF.G | FixedReset | -1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 22.74 Evaluated at bid price : 23.57 Bid-YTW : 4.20 % |

| SLF.PR.J | FloatingReset | -1.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.55 Bid-YTW : 8.84 % |

| IFC.PR.A | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.11 Bid-YTW : 7.72 % |

| TD.PF.C | FixedReset | -1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 21.31 Evaluated at bid price : 21.61 Bid-YTW : 3.87 % |

| PWF.PR.K | Perpetual-Discount | -1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 23.83 Evaluated at bid price : 24.08 Bid-YTW : 5.15 % |

| GWO.PR.I | Deemed-Retractible | -1.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.50 Bid-YTW : 6.21 % |

| PWF.PR.P | FixedReset | -1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 16.10 Evaluated at bid price : 16.10 Bid-YTW : 4.01 % |

| MFC.PR.C | Deemed-Retractible | -1.45 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.40 Bid-YTW : 6.31 % |

| MFC.PR.M | FixedReset | -1.41 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.67 Bid-YTW : 5.82 % |

| BAM.PR.B | Floater | -1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 12.85 Evaluated at bid price : 12.85 Bid-YTW : 3.70 % |

| IFC.PR.C | FixedReset | -1.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.56 Bid-YTW : 5.75 % |

| SLF.PR.B | Deemed-Retractible | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.85 Bid-YTW : 5.61 % |

| GWO.PR.R | Deemed-Retractible | -1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.76 Bid-YTW : 5.67 % |

| BMO.PR.T | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 21.46 Evaluated at bid price : 21.81 Bid-YTW : 3.87 % |

| PWF.PR.T | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 22.50 Evaluated at bid price : 22.85 Bid-YTW : 3.80 % |

| TD.PF.A | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 21.48 Evaluated at bid price : 21.84 Bid-YTW : 3.84 % |

| PWF.PR.R | Perpetual-Premium | -1.16 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-30 Maturity Price : 25.00 Evaluated at bid price : 25.55 Bid-YTW : 4.88 % |

| CM.PR.P | FixedReset | -1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 21.32 Evaluated at bid price : 21.62 Bid-YTW : 3.86 % |

| NA.PR.X | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-15 Maturity Price : 25.00 Evaluated at bid price : 26.85 Bid-YTW : 3.55 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.A | FloatingReset | 174,600 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.29 Bid-YTW : 3.27 % |

| GWO.PR.M | Deemed-Retractible | 130,105 | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-05-21 Maturity Price : 25.50 Evaluated at bid price : 26.05 Bid-YTW : -15.87 % |

| BAM.PR.R | FixedReset | 101,701 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 19.41 Evaluated at bid price : 19.41 Bid-YTW : 4.25 % |

| BMO.PR.C | FixedReset | 93,355 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-05-25 Maturity Price : 25.00 Evaluated at bid price : 25.75 Bid-YTW : 3.98 % |

| CM.PR.Q | FixedReset | 85,000 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-21 Maturity Price : 22.51 Evaluated at bid price : 23.18 Bid-YTW : 4.05 % |

| MFC.PR.R | FixedReset | 83,516 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-03-19 Maturity Price : 25.00 Evaluated at bid price : 25.95 Bid-YTW : 4.11 % |

| There were 79 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TRP.PR.F | FloatingReset | Quote: 18.13 – 19.07 Spot Rate : 0.9400 Average : 0.5473 YTW SCENARIO |

| SLF.PR.I | FixedReset | Quote: 23.10 – 23.79 Spot Rate : 0.6900 Average : 0.4179 YTW SCENARIO |

| PWF.PR.S | Perpetual-Discount | Quote: 23.33 – 24.00 Spot Rate : 0.6700 Average : 0.4240 YTW SCENARIO |

| PWF.PR.L | Perpetual-Premium | Quote: 24.56 – 25.12 Spot Rate : 0.5600 Average : 0.3347 YTW SCENARIO |

| PWF.PR.F | Perpetual-Premium | Quote: 25.03 – 25.58 Spot Rate : 0.5500 Average : 0.3279 YTW SCENARIO |

| BAM.PF.A | FixedReset | Quote: 23.27 – 23.80 Spot Rate : 0.5300 Average : 0.3149 YTW SCENARIO |