As expected, the FOMC hiked the US policy rate:

Information received since the Federal Open Market Committee met in May indicates that the labor market has continued to strengthen and that economic activity has been rising moderately so far this year. Job gains have moderated but have been solid, on average, since the beginning of the year, and the unemployment rate has declined. Household spending has picked up in recent months, and business fixed investment has continued to expand. On a 12-month basis, inflation has declined recently and, like the measure excluding food and energy prices, is running somewhat below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

…

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1 to 1-1/4 percent. The stance of monetary policy remains accommodative, thereby supporting some further strengthening in labor market conditions and a sustained return to 2 percent inflation.

The US market took it all in stride:

Treasuries rose, the dollar trimmed losses and U.S. stocks turned lower after Yellen suggested weak readings on inflation won’t persist amid a tightening labor market.

And, in fact, the Canada five-year reversed itself today, closing with a yield of 1.10%, down 5bp on the day.

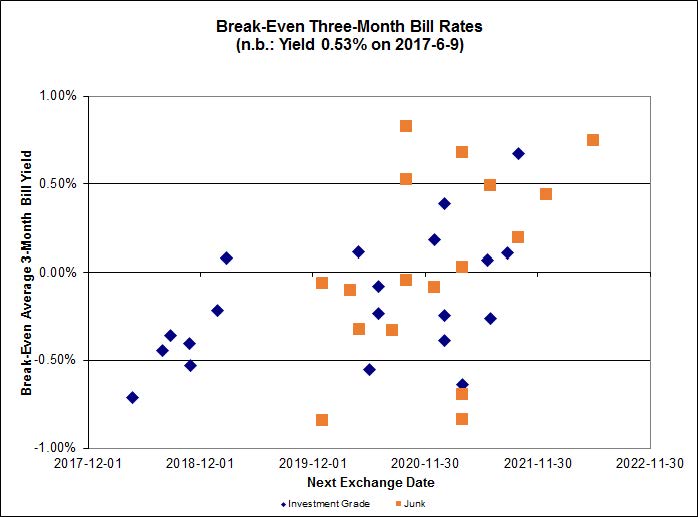

PerpetualDiscounts now yield 5.10%, equivalent to 6.63% interest at the standard equivalency factor of 1.3x. Long corporates now yield a little over 3.7%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 290bp, a narrowing from the 300bp reported June 7.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4144 % | 2,167.0 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4144 % | 3,976.3 |

| Floater | 3.66 % | 3.65 % | 80,052 | 18.20 | 3 | 0.4144 % | 2,291.6 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0785 % | 3,053.9 |

| SplitShare | 4.71 % | 4.33 % | 69,912 | 1.51 | 5 | -0.0785 % | 3,647.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0785 % | 2,845.5 |

| Perpetual-Premium | 5.28 % | 3.38 % | 72,370 | 0.09 | 25 | -0.1418 % | 2,795.6 |

| Perpetual-Discount | 5.10 % | 5.10 % | 93,387 | 15.24 | 12 | -0.3709 % | 3,005.5 |

| FixedReset | 4.44 % | 3.99 % | 200,150 | 6.56 | 96 | -0.4906 % | 2,337.7 |

| Deemed-Retractible | 4.98 % | 5.02 % | 118,645 | 6.25 | 30 | -0.2540 % | 2,902.8 |

| FloatingReset | 2.48 % | 3.00 % | 55,806 | 4.38 | 10 | -0.2860 % | 2,554.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.G | FixedReset | -2.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-06-14 Maturity Price : 22.64 Evaluated at bid price : 23.44 Bid-YTW : 4.13 % |

| HSE.PR.A | FixedReset | -1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-06-14 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 4.20 % |

| TRP.PR.B | FixedReset | -1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-06-14 Maturity Price : 14.55 Evaluated at bid price : 14.55 Bid-YTW : 3.83 % |

| MFC.PR.M | FixedReset | -1.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.94 Bid-YTW : 6.25 % |

| MFC.PR.L | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.34 Bid-YTW : 6.50 % |

| W.PR.K | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-01-15 Maturity Price : 25.00 Evaluated at bid price : 26.12 Bid-YTW : 4.18 % |

| CU.PR.I | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-01 Maturity Price : 25.00 Evaluated at bid price : 26.30 Bid-YTW : 2.97 % |

| MFC.PR.N | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.01 Bid-YTW : 6.14 % |

| MFC.PR.G | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.49 Bid-YTW : 4.85 % |

| VNR.PR.A | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-06-14 Maturity Price : 21.04 Evaluated at bid price : 21.04 Bid-YTW : 4.56 % |

| MFC.PR.O | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-06-19 Maturity Price : 25.00 Evaluated at bid price : 26.64 Bid-YTW : 3.83 % |

| MFC.PR.K | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.48 Bid-YTW : 6.33 % |

| BIP.PR.B | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.81 Bid-YTW : 4.46 % |

| TRP.PR.C | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-06-14 Maturity Price : 15.76 Evaluated at bid price : 15.76 Bid-YTW : 3.94 % |

| BMO.PR.S | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-06-14 Maturity Price : 21.45 Evaluated at bid price : 21.79 Bid-YTW : 3.85 % |

| BAM.PF.D | Perpetual-Discount | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-06-14 Maturity Price : 22.94 Evaluated at bid price : 23.33 Bid-YTW : 5.25 % |

| GWO.PR.N | FixedReset | 1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.25 Bid-YTW : 8.56 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| NA.PR.C | FixedReset | 143,066 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-06-14 Maturity Price : 23.09 Evaluated at bid price : 24.86 Bid-YTW : 4.34 % |

| CM.PR.R | FixedReset | 113,051 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-06-14 Maturity Price : 23.17 Evaluated at bid price : 25.04 Bid-YTW : 4.26 % |

| RY.PR.Z | FixedReset | 68,881 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-06-14 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 3.81 % |

| BAM.PF.A | FixedReset | 60,908 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-06-14 Maturity Price : 22.28 Evaluated at bid price : 22.69 Bid-YTW : 4.28 % |

| RY.PR.E | Deemed-Retractible | 56,816 | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-07-14 Maturity Price : 25.00 Evaluated at bid price : 25.28 Bid-YTW : -5.85 % |

| NA.PR.S | FixedReset | 42,550 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-06-14 Maturity Price : 21.52 Evaluated at bid price : 21.52 Bid-YTW : 4.03 % |

| There were 43 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PF.D | Perpetual-Discount | Quote: 23.33 – 23.76 Spot Rate : 0.4300 Average : 0.2828 YTW SCENARIO |

| CU.PR.G | Perpetual-Discount | Quote: 22.56 – 22.89 Spot Rate : 0.3300 Average : 0.1970 YTW SCENARIO |

| RY.PR.O | Perpetual-Premium | Quote: 25.43 – 25.74 Spot Rate : 0.3100 Average : 0.1984 YTW SCENARIO |

| GWO.PR.R | Deemed-Retractible | Quote: 23.90 – 24.20 Spot Rate : 0.3000 Average : 0.2055 YTW SCENARIO |

| MFC.PR.J | FixedReset | Quote: 22.55 – 22.78 Spot Rate : 0.2300 Average : 0.1365 YTW SCENARIO |

| MFC.PR.L | FixedReset | Quote: 20.34 – 20.59 Spot Rate : 0.2500 Average : 0.1594 YTW SCENARIO |