On June 16, Bombardier announced (emphasis added):

In connection with the conversion privilege for holders of its Series 2 and Series 3 Preferred Shares, Bombardier Inc. (TSX: BBD.B) (TSX: BBD.A) (TSX: BBD.PR.B) (TSX:BBD.PR.D) today announced the basis for resetting the dividend rate on its Series 3 Preferred Shares in accordance with the terms applicable to those shares.

Holders of Bombardier Inc. Series 2 Preferred Shares have the right to convert all or part of their shares, effective on August 1, 2017, on a one for one basis into Series 3 Preferred Shares. Holders of Bombardier Inc. Series 3 Preferred Shares have the right to convert all or part of their shares, effective on August 1, 2017, on a one for one basis into Series 2 Preferred Shares. Holders who do not convert their shares will retain their Series 2 Preferred Shares or Series 3 Preferred Shares, as the case may be, unless automatically converted in accordance with the terms of the Series 2 or Series 3 Preferred Shares, as described below.

In the case of the Series 2 Preferred Shares, starting as of August 1, 2017, holders will continue to receive a monthly floating adjustable cash dividend, as and when declared by the Board of Directors of Bombardier Inc., based on a dividend rate equal to a percentage of the prime rate, subject to certain adjustments in accordance with the terms of such shares.

In the case of the Series 3 Preferred Shares, starting as of August 1, 2017, holders will receive a quarterly fixed cash dividend for the following five years, as and when declared by the Board of Directors of Bombardier Inc., based on a fixed rate equal to 265% of the yield on five-year non-callable Government of Canada bonds determined as at July 11, 2017, in accordance with the terms of such shares. The annual dividend rate applicable to the Series 3 Preferred Shares will be published on July 12, 2017 in select newspapers.

Any registered shareholder who wishes to convert his or her Series 2 and/ or Series 3 Preferred Shares must complete and sign the conversion panel contained on the back of the Series 2 or Series 3 Preferred Share certificate as the case may be, and deliver it, at the latest by 5:00 p.m. (Montréal time) on July 18, 2017, to Computershare Investor Services Inc.

Shareholders who are beneficial owners and who wish to exercise their right of conversion should communicate as soon as possible with their broker or other nominee and follow their instructions. In that case, it is important that they follow such instructions and act in the timeframe advised so as to provide enough time to their broker or other nominee to meet the July 18, 2017 deadline.

If, after July 18, 2017, Bombardier Inc. determines that there would be less than one million Series 2 Preferred Shares outstanding after the conversion date (being August 1, 2017), then all remaining Series 2 Preferred Shares will automatically be converted into Series 3 Preferred Shares on a one-for-one basis. However, if, after July 18, 2017, Bombardier Inc. determines that there would be less than one million Series 3 Preferred Shares outstanding after the conversion date (being August 1, 2017), then all remaining Series 3 Preferred Shares will automatically be converted into Series 2 Preferred Shares on a one-for-one basis. In either case, Bombardier Inc. shall give a written notice to that effect to holders of such remaining shares no later than July 25, 2017.

Subject to the conditions mentioned in the previous paragraph, on August 1, 2017, and every five years thereafter, holders of Series 2 Preferred Shares and holders of Series 3 Preferred Shares will have again the right to convert their shares into shares of the other series.

The Series 2 and Series 3 Preferred Shares are listed on the Toronto Stock Exchange under the ticker symbol BBD.PR.B and BBD.PR.D, respectively.

In my terminology, BBD.PR.B is a Ratchet Rate preferred, currently paying 100% of Prime, reset quarterly. BBD.PR.D is a FixedFloater currently paying $0.7835 p.a., or 3.134% of its $25 par value. The latter rate resets every Exchange Date; the next exchange date is imminent – 2017-8-1. Both issues have been relegated to the Scraps subindex since inception on credit concerns.

The company has further announced (emphasis added):

that as of August 1, 2017, its Series 3 Preferred Shares will pay, on a quarterly basis, as and when declared by the Board of Directors of Bombardier Inc., cash dividends for the following five years that will be based on a fixed rate equal to the product of (a) the average of the yield to maturity, designated on July 11, 2017 by National Bank Financial Inc. and Scotia Capital Inc., that would be carried by a Government of Canada bond with a five-year maturity, namely 1.503%, multiplied by (b) 265%, which multiplier was previously announced on June 16, 2017.

Accordingly, the annual dividend rate applicable to the Series 3 Preferred Shares for the period of five years beginning on August 1, 2017 will be 3.983%.

As a reminder, any registered shareholder who wishes to convert his or her Series 2 and/ or Series 3 Preferred Shares must complete and sign the conversion panel contained on the back of the Series 2 or Series 3 Preferred Share certificate as the case may be, and deliver it, at the latest by 5:00 p.m. (Montréal time) on July 18, 2017, to Computershare Investor Services Inc. Likewise, shareholders who are beneficial owners and who wish to exercise their right of conversion should communicate as soon as possible with their broker or other nominee and follow their instructions. In that case, it is important that they follow such instructions and act in the timeframe advised so as to provide enough time to their broker or other nominee to meet the July 18, 2017 deadline.

The most logical way to analyze the question of whether or not to convert is through the theory of Preferred Pairs, for which a calculator is available. Briefly, a Strong Pair is defined as a pair of securities that can be interconverted in the future (e.g., BBD.PR.D and BBD.PR.B). Since they will be interconvertible on this future date, it may be assumed that they will be priced identically on this date (if they aren’t then holders will simply convert en masse to the higher-priced issue). And since they will be priced identically on a given date in the future, any current difference in price must be offset by expectations of an equal and opposite value of dividends to be received in the interim. And since the dividend rate on one element of the pair is both fixed and known, the implied average rate of the other, floating rate, instrument can be determined. Finally, we say, we may compare these average rates and take a view regarding the actual future course of that rate relative to the implied rate, which will provide us with guidance on which element of the pair is likely to outperform the other until the next interconversion date, at which time the process will be repeated.

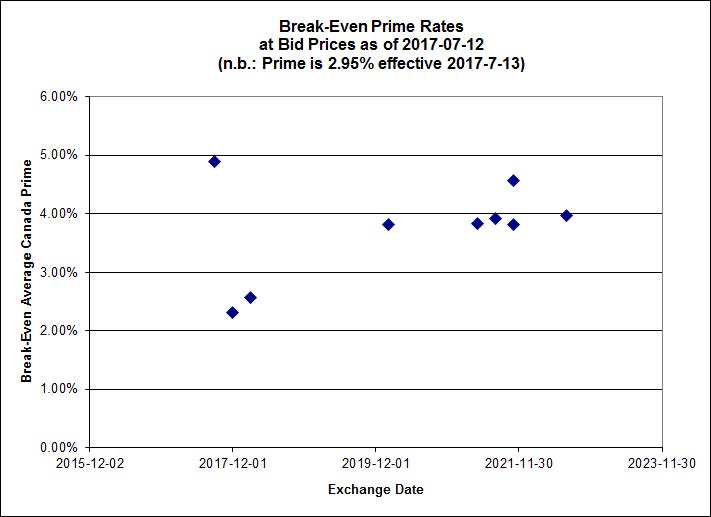

We can show the break-even rates for each FixedFloater / RatchetRate Strong Pair graphically by plotting the implied average Prime rate against the next Exchange Date (which is the date to which the average will be calculated).

Click for Big

Click for BigRecent tumult in the market resulting from the Bank of Canada’s hawkish signals (commencing on June 12, reinforced June 13 and piled on with a shovel on June 28) and the execution of a 25bp policy hike today has resulted in fine performance of RatchetRate preferreds, to the point where the average break-even Prime rate is now roughly 4.00% for issues with Exchange Dates in 2020 and afterwards.

Predictions are difficult, particularly when they are about the future! It will be remembered that Prime is currently at 2.95%; therefore, if we assume that future hikes are evenly sized and spaced, an average of 4.00% implies an end-value in five years of about 5.00%. I’m inclined to believe that it will turn out to be less than that, but if you disagree I won’t put up much of an argument!

Since credit quality of each element of the pair is equal to the other element, it should not make any difference whether the pair examined is investment-grade or junk, although we might expect greater variation of implied rates between junk issues on grounds of lower liquidity, and this is just what we see.

If we plug in the current bid price of the BBD.PR.D FixedFloater, we may construct the following table showing consistent prices for its soon-to-be-issued FloatingReset counterpart given a variety of Implied Breakeven yields consistent with issues currently trading:

| Estimate of BBD.PR.B (received in exchange for BBD.PR.D) Trading Price In Current Conditions |

| |

Assumed RatchetRate

Price if Implied Prime

is equal to |

| FixedFloater |

Bid Price |

Fixed Rate |

+3.50% |

4.00% |

4.50% |

| BBD.PR.D |

9.88 |

3.983% |

9.47 |

9.89 |

10.31 |

Based on current market conditions, I suggest that the BBD.PR.B will likely commence trading at close to the price of BBD.PR.D, its FixedFloater counterpart. Therefore, I make no recommendation regarding conversion into either one or the other. Those with strong convictions regarding future movements in Prime will, of course, have an equally strong preference for one of the two issues; other investors may wish to select which of the pair they wish to hold for the next five years based on their personal circumstances (e.g., if you’re hedging a prime-linked mortgage with this issue [not a wise move], you will want to hold BBD.PR.B).

I will note that the credit quality of these issues is lousy: S&P downgraded them to P-5(low) in 2016 and DBRS downgraded to Pfd-4(low) and discontinued coverage in 2013. With these issues, you’re making such a large bet on the future credit quality of the company that details regarding the next five years of dividends are a mere bagatelle.