There are new indications of a September Fed hike:

Traders are seeing virtually even odds on a September interest-rate increase in the U.S., pushing a gauge of the dollar to a four-month high.

The greenback rallied versus most major peers Tuesday as Federal Reserve Bank of Atlanta President Dennis Lockhart said in an interview with the Wall Street Journal that the central bank is close to raising rates next month for the first time since 2006. A report Friday is forecast to show U.S. employers added more than 200,000 jobs again in July.

…

Traders are pricing in a 48 percent probability that the Fed will raise borrowing costs in September, based on the assumption that the effective fed funds rate will average 0.375 percent after the first increase.

So I don’t know how this fits in:

Investor demand for longer-maturity Treasuries means they’re willing to accept a smaller yield premium to get the securities. Fidelity Investments says the trend has further to go.

The extra yield on 10-year notes over two-year securities shrank to 147 basis points Tuesday, the narrowest spread in three months. Traders in the world’s biggest bond market call this a flattening of the yield curve. The figure is less than the average of almost 2 percentage points for the past five years.

…

The difference between one-year U.S. yields and those for similar-maturity Treasury Inflation Protected Securities, a gauge of trader expectations for consumer prices over the life of the debt, was negative 0.67 percent. It has been below zero for two weeks.

SEC Commissioner Daniel M. Gallagher gave an entertaining speech on Dodd-Frank:

Last month marked the fifth anniversary of the Dodd-Frank Act,[1] meaning that my entire tenure as a Commissioner has occurred in the midst of the first Five-Year Plan for our national economy. And, as is always the case with grandiose central plans, Dodd-Frank has backfired, strangling our economy, increasing the fragility of the financial system, and politicizing our independent financial regulators.

…

Prudential regulation is an important tool for bank regulators to use in supervising banks’ risk-taking activities, so as to ensure that risks are limited to an acceptable level and avoid posing an undue strain on the government insurance backstop — despite the moral hazard and expectations of “no losses” that the insurance itself creates. But in practice, “prudential” regulation can and has evolved into an opaque regulatory system in which the government’s invisible hand replaces the market’s, transcending rule enforcement and becoming the decision maker for ostensibly private enterprises.The attempts by our prudential regulators and their international counterparts to de-risk the U.S. capital markets and make them look like the banking markets are not just philosophically wrong — they are an attack on U.S. competitiveness. As I have stated before, piling more regulatory burdens on our capital markets will only cause more activity to move overseas, where up-and-coming jurisdictions in Asia and elsewhere would be more than happy to gain market share.[7] And it will stifle domestic economic activity, as companies will be forced to line up for bank loans made scarce by new bank regulations rather than pursuing capital formation opportunities in the market.

It was another rotten day for the Canadian preferred share market, with PerpetualDiscounts and FixedResets both down 27bp and DeemedRetractibles losing 39bp. TRP, ENB and SLF issues are notable on the bad side of the Performance Highlights table. Volume was average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

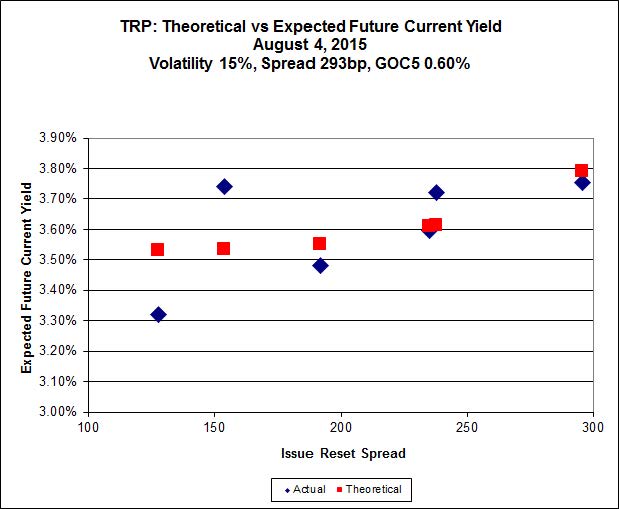

Here’s TRP:

Click for Big

TRP.PR.B, which resets 2020-6-30 at +128, is bid at 14.15 to be $0.84 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.85 cheap at its bid price of 14.30.

Click for Big

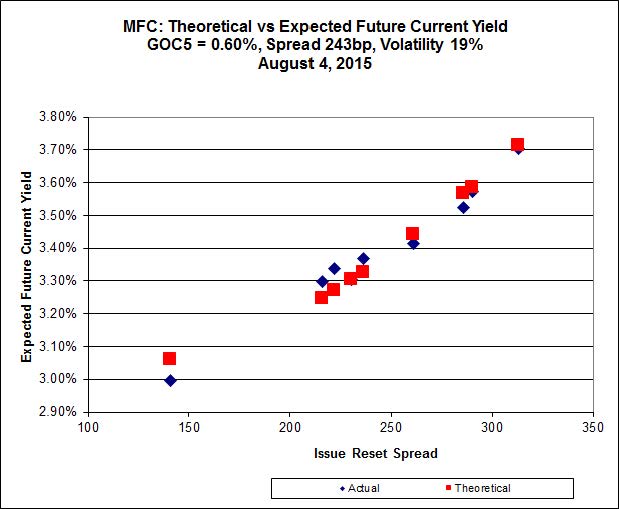

Another good fit today!

Most expensive is MFC.PR.F, resetting at +141bp on 2016-6-19, bid at 16.78 to be 0.36 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 21.12 to be $0.44 cheap.

Click for Big

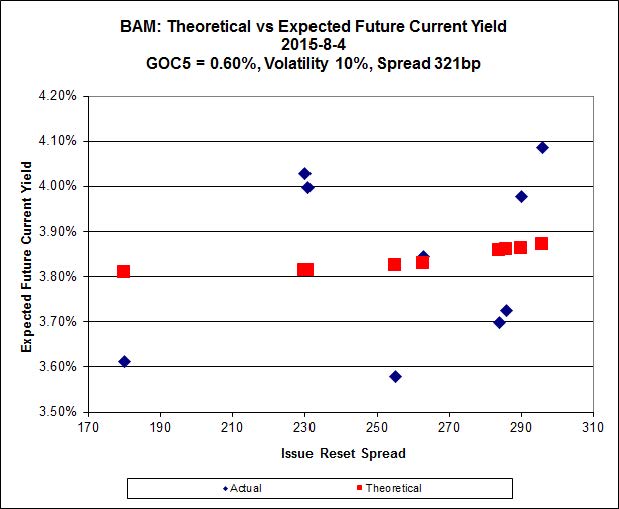

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.Z, resetting at +296bp on 2017-12-31, bid at 21.78 to be $1.21 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 23.25 and appears to be $0.95 rich.

Click for Big

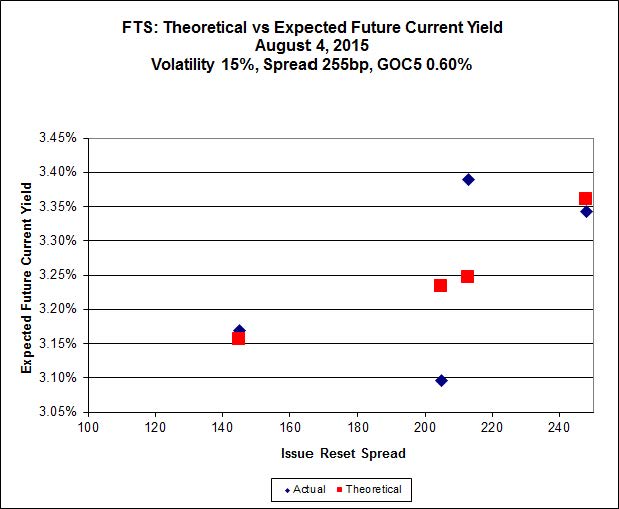

FTS.PR.K, with a spread of +205bp, and bid at 21.40, looks $0.91 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 20.14 and is $0.88 cheap.

Click for Big

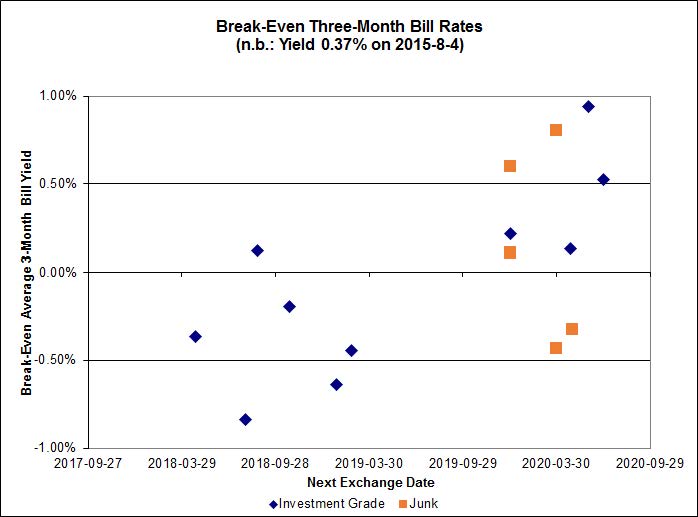

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of +0.03%, with one outlier above 1.00% and one below -1.00%. There is one junk outlier above +1.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.8774 % | 1,988.1 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.8774 % | 3,476.1 |

| Floater | 3.69 % | 3.73 % | 56,089 | 17.98 | 3 | -0.8774 % | 2,113.5 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0669 % | 2,774.8 |

| SplitShare | 4.59 % | 4.95 % | 60,699 | 3.15 | 3 | -0.0669 % | 3,251.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0669 % | 2,537.3 |

| Perpetual-Premium | 5.72 % | 4.49 % | 68,288 | 0.08 | 9 | -0.2817 % | 2,484.9 |

| Perpetual-Discount | 5.41 % | 5.46 % | 84,389 | 14.62 | 28 | -0.2738 % | 2,604.3 |

| FixedReset | 4.72 % | 3.87 % | 211,653 | 15.77 | 87 | -0.2673 % | 2,227.9 |

| Deemed-Retractible | 5.13 % | 5.19 % | 105,051 | 5.47 | 34 | -0.3934 % | 2,571.4 |

| FloatingReset | 2.33 % | 3.38 % | 47,702 | 6.02 | 9 | -0.5781 % | 2,253.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| ENB.PR.B | FixedReset | -3.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 15.41 Evaluated at bid price : 15.41 Bid-YTW : 5.09 % |

| TRP.PR.C | FixedReset | -3.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 14.30 Evaluated at bid price : 14.30 Bid-YTW : 3.76 % |

| TRP.PR.B | FixedReset | -2.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 14.15 Evaluated at bid price : 14.15 Bid-YTW : 3.43 % |

| TRP.PR.A | FixedReset | -2.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 18.09 Evaluated at bid price : 18.09 Bid-YTW : 3.72 % |

| ENB.PR.H | FixedReset | -2.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 15.45 Evaluated at bid price : 15.45 Bid-YTW : 4.81 % |

| TRP.PR.E | FixedReset | -2.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 3.92 % |

| CU.PR.F | Perpetual-Discount | -2.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 5.51 % |

| GWO.PR.P | Deemed-Retractible | -2.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.62 Bid-YTW : 5.72 % |

| TD.PR.Z | FloatingReset | -2.19 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.82 Bid-YTW : 3.50 % |

| ENB.PF.G | FixedReset | -2.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 18.25 Evaluated at bid price : 18.25 Bid-YTW : 4.99 % |

| FTS.PR.F | Perpetual-Discount | -2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 22.65 Evaluated at bid price : 22.91 Bid-YTW : 5.43 % |

| PWF.PR.L | Perpetual-Discount | -2.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 23.56 Evaluated at bid price : 23.81 Bid-YTW : 5.38 % |

| ELF.PR.H | Perpetual-Discount | -2.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 23.88 Evaluated at bid price : 24.35 Bid-YTW : 5.68 % |

| SLF.PR.D | Deemed-Retractible | -2.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.07 Bid-YTW : 6.82 % |

| ENB.PF.C | FixedReset | -1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 18.16 Evaluated at bid price : 18.16 Bid-YTW : 4.93 % |

| FTS.PR.H | FixedReset | -1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 16.17 Evaluated at bid price : 16.17 Bid-YTW : 3.29 % |

| PWF.PR.O | Perpetual-Premium | -1.51 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-10-31 Maturity Price : 25.25 Evaluated at bid price : 25.51 Bid-YTW : 5.31 % |

| HSE.PR.E | FixedReset | -1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 22.06 Evaluated at bid price : 22.60 Bid-YTW : 4.70 % |

| MFC.PR.I | FixedReset | -1.45 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.55 Bid-YTW : 3.98 % |

| SLF.PR.B | Deemed-Retractible | -1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.48 Bid-YTW : 6.33 % |

| SLF.PR.C | Deemed-Retractible | -1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.10 Bid-YTW : 6.80 % |

| MFC.PR.N | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.95 Bid-YTW : 5.08 % |

| SLF.PR.E | Deemed-Retractible | -1.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.36 Bid-YTW : 6.69 % |

| CU.PR.G | Perpetual-Discount | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 21.05 Evaluated at bid price : 21.05 Bid-YTW : 5.44 % |

| BIP.PR.A | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 21.53 Evaluated at bid price : 21.85 Bid-YTW : 4.88 % |

| CU.PR.C | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 23.14 Evaluated at bid price : 23.51 Bid-YTW : 3.27 % |

| POW.PR.G | Perpetual-Premium | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 24.49 Evaluated at bid price : 24.98 Bid-YTW : 5.64 % |

| BAM.PR.C | Floater | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 12.60 Evaluated at bid price : 12.60 Bid-YTW : 3.78 % |

| ENB.PR.F | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 16.80 Evaluated at bid price : 16.80 Bid-YTW : 4.89 % |

| ENB.PR.P | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 16.80 Evaluated at bid price : 16.80 Bid-YTW : 4.94 % |

| BAM.PR.K | Floater | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 12.76 Evaluated at bid price : 12.76 Bid-YTW : 3.73 % |

| BNS.PR.Q | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.67 Bid-YTW : 3.21 % |

| GWO.PR.S | Deemed-Retractible | -1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.80 Bid-YTW : 5.46 % |

| ENB.PR.N | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 17.20 Evaluated at bid price : 17.20 Bid-YTW : 4.98 % |

| ENB.PF.A | FixedReset | -1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 18.14 Evaluated at bid price : 18.14 Bid-YTW : 4.93 % |

| GWO.PR.Q | Deemed-Retractible | -1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.30 Bid-YTW : 5.64 % |

| BAM.PR.R | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 4.19 % |

| BNS.PR.A | FloatingReset | -1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.85 Bid-YTW : 3.14 % |

| ELF.PR.F | Perpetual-Discount | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 23.91 Evaluated at bid price : 24.15 Bid-YTW : 5.53 % |

| PWF.PR.K | Perpetual-Discount | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 22.86 Evaluated at bid price : 23.13 Bid-YTW : 5.37 % |

| MFC.PR.F | FixedReset | -1.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.78 Bid-YTW : 7.11 % |

| CU.PR.E | Perpetual-Discount | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 22.48 Evaluated at bid price : 22.77 Bid-YTW : 5.46 % |

| MFC.PR.L | FixedReset | 1.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.92 Bid-YTW : 5.59 % |

| BAM.PF.B | FixedReset | 1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 4.09 % |

| MFC.PR.K | FixedReset | 1.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.12 Bid-YTW : 5.35 % |

| BAM.PF.E | FixedReset | 1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 21.65 Evaluated at bid price : 22.00 Bid-YTW : 3.91 % |

| TD.PF.F | Perpetual-Discount | 1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 23.81 Evaluated at bid price : 24.15 Bid-YTW : 5.10 % |

| ENB.PR.Y | FixedReset | 1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 17.32 Evaluated at bid price : 17.32 Bid-YTW : 4.68 % |

| BAM.PR.Z | FixedReset | 1.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 21.44 Evaluated at bid price : 21.78 Bid-YTW : 4.28 % |

| HSE.PR.C | FixedReset | 2.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 22.01 Evaluated at bid price : 22.50 Bid-YTW : 4.34 % |

| BAM.PR.N | Perpetual-Discount | 2.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 21.40 Evaluated at bid price : 21.40 Bid-YTW : 5.62 % |

| BAM.PR.X | FixedReset | 2.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 16.61 Evaluated at bid price : 16.61 Bid-YTW : 3.93 % |

| FTS.PR.J | Perpetual-Discount | 3.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 22.35 Evaluated at bid price : 22.75 Bid-YTW : 5.29 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| CM.PR.P | FixedReset | 144,674 | Desjardins crossed 130,900 at 21.80. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 21.52 Evaluated at bid price : 21.81 Bid-YTW : 3.45 % |

| BMO.PR.T | FixedReset | 79,500 | Scotia crossed 74,000 at 22.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 21.98 Evaluated at bid price : 22.43 Bid-YTW : 3.33 % |

| BMO.PR.Y | FixedReset | 78,561 | Desjardins crossed 75,000 at 24.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 22.76 Evaluated at bid price : 23.96 Bid-YTW : 3.51 % |

| HSE.PR.G | FixedReset | 71,650 | Haywood (who?) crossed 70,000 at 22.83. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 22.15 Evaluated at bid price : 22.78 Bid-YTW : 4.66 % |

| CM.PR.O | FixedReset | 69,403 | Scotia crossed 56,000 at 22.65. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 22.12 Evaluated at bid price : 22.63 Bid-YTW : 3.39 % |

| BAM.PR.Z | FixedReset | 66,075 | Scotia crossed 56,000 at 21.83. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-04 Maturity Price : 21.44 Evaluated at bid price : 21.78 Bid-YTW : 4.28 % |

| There were 32 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TRP.PR.E | FixedReset | Quote: 20.50 – 21.27 Spot Rate : 0.7700 Average : 0.4808 YTW SCENARIO |

| ELF.PR.H | Perpetual-Discount | Quote: 24.35 – 24.90 Spot Rate : 0.5500 Average : 0.3375 YTW SCENARIO |

| MFC.PR.L | FixedReset | Quote: 20.92 – 21.50 Spot Rate : 0.5800 Average : 0.3781 YTW SCENARIO |

| GWO.PR.P | Deemed-Retractible | Quote: 24.62 – 25.12 Spot Rate : 0.5000 Average : 0.3204 YTW SCENARIO |

| MFC.PR.N | FixedReset | Quote: 21.95 – 22.50 Spot Rate : 0.5500 Average : 0.3959 YTW SCENARIO |

| PWF.PR.L | Perpetual-Discount | Quote: 23.81 – 24.24 Spot Rate : 0.4300 Average : 0.2860 YTW SCENARIO |