Well, it was another day-and-a-half for equities:

Two things that have supported U.S. stocks in the past, dovish words from the Federal Reserve and improving economic data, triggered the biggest rally since 2011 and halted a plunge that erased $2.2 trillion from share values.

Technology companies led the gains with Apple Inc., Google Inc. and Intel Inc. rising at least 5.5 percent. Amazon.com Inc. surged 7.4 percent, and Netflix Inc. posted a two-day gain of 14 percent. JPMorgan Chase & Co. and Citigroup Inc. increased more than 4.8 percent. Cameron International Corp. soared 41 percent after agreeing to be bought by Schlumberger Ltd. in a $14.8 billion deal.

Gains in equities accelerated in the final hour as the Standard & Poor’s 500 Index climbed 3.9 percent to 1,940.51 at 4 p.m. in New York, halting a six-day slide that was its steepest in four years. The Dow Jones Industrial Average added 619.07 points, or 4 percent, to 16,285.51. The Nasdaq Composite Index rose 4.2 percent for its strongest increase since August 2011. About 10.7 billion shares traded hands on U.S. exchanges, 55 percent above the three-month average.

Dovish words from the Fed? Dudley pointed out that financial markets are important:

Global stock-market turmoil has weakened the case for raising interest rates in September, Federal Reserve Bank of New York President William C. Dudley said, cautioning it’s important not to overreact to short-term developments.

“From my perspective, at this moment, the decision to begin the normalization process at the September FOMC meeting seems less compelling to me than it was a few weeks ago,” Dudley told a news conference Wednesday at the New York Fed.

“Normalization could become more compelling by the time of the meeting as we get additional information on how the U.S. economy is performing, and more information on international and financial market developments.”

Treasuries suffered their biggest two-day tumble in six weeks as an unexpected jump in durable-goods orders and a recovery in stocks suppressed demand.

Losses deepened after an auction of five-year Treasuries drew the least interest since 2009, signaling that investors’ safe-haven appetite may have waned.

Debt found only temporary support after Federal Reserve Bank of New York President William Dudley said the case for increasing interest rates in September is less compelling because of worldwide market turmoil. Buyers demurred without evidence that the turbulence will slow the U.S. economy.

Real world effects of financial markets? There are fears that oil prices and currency turmoil are favouring ISIS:

Any currency crisis usually comes with dire consequences for a country, and the threat of one in Iraq shows how the impact can go beyond the economy and markets.

A foreign-exchange crunch because of a drop in oil prices could force a devaluation of the dinar and risk making the fight against Islamic State militants even tougher. The nation, currently OPEC’s biggest producer after Saudi Arabia, is dependent on oil revenue to fund its operations on the battlefield and quell growing unrest over the economy.

Dollar reserves tumbled about 20 percent to $59 billion as of July 23 since the fighting escalated a year before, and the losses are accelerating. In the first 25 days of August, the central bank sold $4.6 billion of currency to keep the dinar at a pegged rate, a daily outflow of about $184 million, data compiled by Bloomberg show.

…

Saudi Arabia’s central bank this week said it’s committed to the riyal’s dollar peg, the Saudi-owned Al Arabiya television reported, amid speculation the country would devalue its currency after the plunge in oil prices.

Canadian Utilities Limited, proud issuer of CU.PR.C, CU.PR.D, CU.PR.E, CU.PR.F, CU.PR.G and CU.PR.H, has been confirmed at Pfd-2(high) by DBRS:

DBRS Limited (DBRS) has today confirmed the Issuer Rating and Unsecured Debentures rating of Canadian Utilities Limited (CU or the Company) at “A,” the Commercial Paper rating at R-1 (low), and the Cum. Preferred Shares rating at Pfd-2 (high). All trends are Stable. The ratings of CU are supported by predictable earnings from its regulated subsidiaries, which are expected to account for approximately 80% of consolidated earnings over the next several years. However, the ratings assume that earnings contribution from the regulated business will gradually decrease to around 70% (but still higher than its historical weighting of 60%) of consolidated earnings over the long term with (1) the downshifting of Alberta’s economy and expected completion of the “big build” associated with electric transmission infrastructure over the next two years and (2) the Company’s focus on contracted, non-regulated business opportunities in Canada, Mexico and Australia. Although CU’s non-regulated segment provides a source of earnings growth and diversification benefits, it also entails higher business risk than that of the regulated utility business. CU’s non-regulated business is challenged by lower long-term earnings visibility and recontracting risk.

The Canadian preferred share market had a bit of rebound today, with both PerpetualDiscounts and FixedResets gaining 10bp and DeemedRetractibles up 28bp. Floaters got hammered again though, so at least something is familiar! The Performance Highlights table continues to show a lot of churning, with 21 losers and 22 winners. Volume was on the low side of average.

PerpetualDiscounts now yield 5.57%, equivalent to 7.24% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 4.0%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 325bp, a sharp rise from the 310bp reported August 12.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

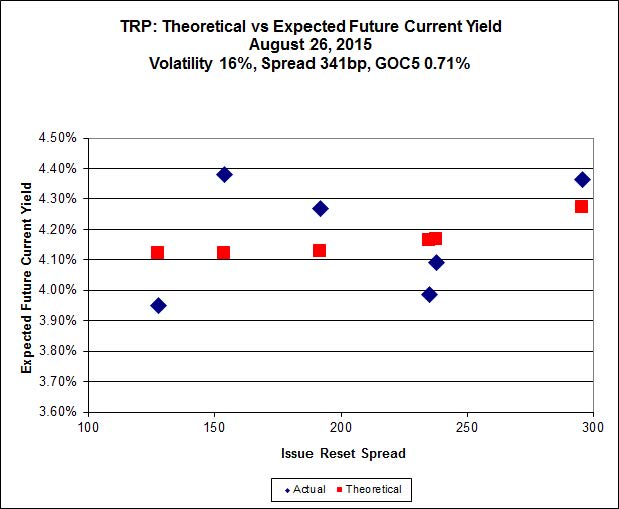

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.20 to be $0.82 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $0.81 cheap at its bid price of 12.84.

Click for Big

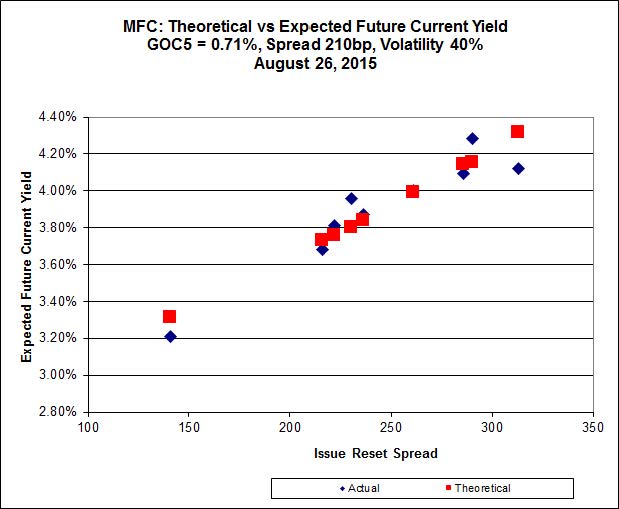

Another good fit today for MFC, while the series maintains its high level of Implied Volatility.

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 23.31 to be 1.07 rich, while MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 19.00 to be 0.81 cheap.

Click for Big

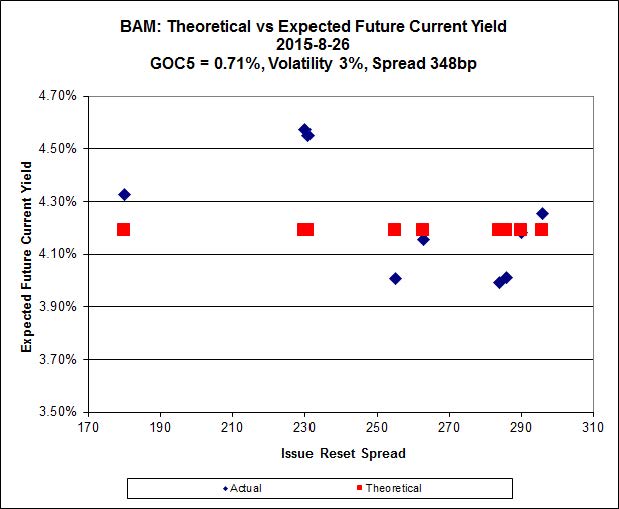

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.45 to be $1.51 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 22.23 and appears to be $1.05 rich.

Click for Big

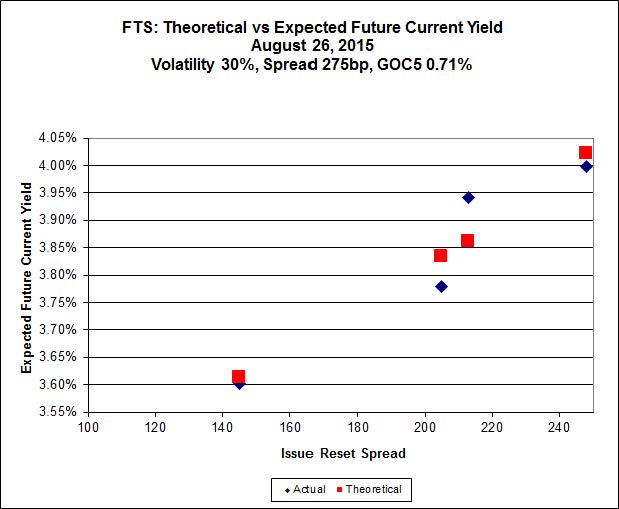

Implied Volatility jumped today and is unreasonably high.

FTS.PR.K, with a spread of +205bp, and bid at 18.26, looks $0.26 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.01 and is $0.37 cheap.

Click for Big

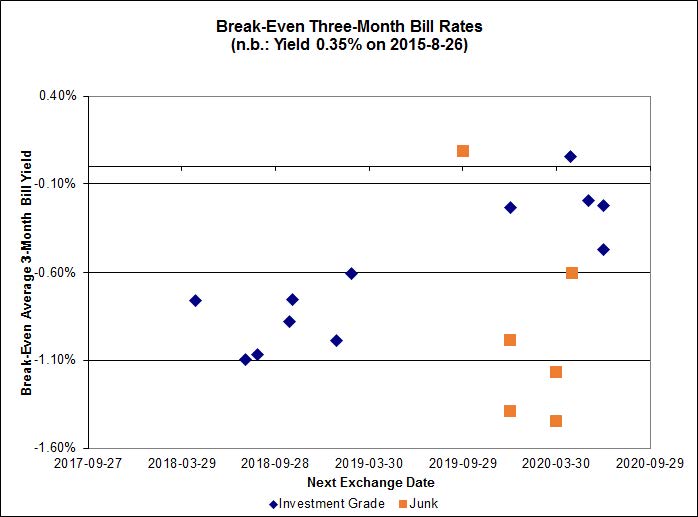

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.60%, with no outliers. Note that the distribution is bimodal, with NVCC non-compliant bank issues averaging -0.88% and the unregulated issues averaging -0.22%. There is one junk outlier below -1.60%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -2.4567 % | 1,603.0 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -2.4567 % | 2,802.8 |

| Floater | 4.58 % | 4.69 % | 58,355 | 15.99 | 3 | -2.4567 % | 1,704.1 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0272 % | 2,758.8 |

| SplitShare | 4.66 % | 5.26 % | 57,966 | 3.12 | 3 | 0.0272 % | 3,233.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0272 % | 2,522.6 |

| Perpetual-Premium | 5.74 % | 5.71 % | 63,469 | 14.06 | 9 | 0.0754 % | 2,476.2 |

| Perpetual-Discount | 5.53 % | 5.57 % | 79,770 | 14.54 | 29 | 0.1050 % | 2,553.8 |

| FixedReset | 5.05 % | 4.30 % | 199,096 | 15.50 | 87 | 0.1005 % | 2,092.7 |

| Deemed-Retractible | 5.19 % | 5.29 % | 99,660 | 5.56 | 34 | 0.2804 % | 2,547.4 |

| FloatingReset | 2.38 % | 3.52 % | 47,501 | 5.96 | 9 | -0.3427 % | 2,181.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| MFC.PR.N | FixedReset | -4.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.00 Bid-YTW : 6.89 % |

| BAM.PR.K | Floater | -3.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 10.12 Evaluated at bid price : 10.12 Bid-YTW : 4.73 % |

| BAM.PR.C | Floater | -3.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 10.20 Evaluated at bid price : 10.20 Bid-YTW : 4.69 % |

| NA.PR.S | FixedReset | -2.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 20.30 Evaluated at bid price : 20.30 Bid-YTW : 3.98 % |

| TRP.PR.F | FloatingReset | -2.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 14.00 Evaluated at bid price : 14.00 Bid-YTW : 4.10 % |

| MFC.PR.K | FixedReset | -2.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.21 Bid-YTW : 6.51 % |

| FTS.PR.J | Perpetual-Discount | -2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 21.28 Evaluated at bid price : 21.55 Bid-YTW : 5.53 % |

| IAG.PR.G | FixedReset | -1.93 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.85 Bid-YTW : 4.34 % |

| BNS.PR.D | FloatingReset | -1.80 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.14 Bid-YTW : 4.89 % |

| RY.PR.H | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 20.73 Evaluated at bid price : 20.73 Bid-YTW : 3.72 % |

| BAM.PR.X | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 14.50 Evaluated at bid price : 14.50 Bid-YTW : 4.62 % |

| VNR.PR.A | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 4.58 % |

| BMO.PR.Y | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 22.59 Evaluated at bid price : 23.60 Bid-YTW : 3.62 % |

| NA.PR.W | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 20.05 Evaluated at bid price : 20.05 Bid-YTW : 3.88 % |

| BIP.PR.A | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 5.16 % |

| GWO.PR.N | FixedReset | -1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.00 Bid-YTW : 8.32 % |

| MFC.PR.G | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.07 Bid-YTW : 5.82 % |

| BAM.PF.E | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 20.33 Evaluated at bid price : 20.33 Bid-YTW : 4.34 % |

| MFC.PR.L | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.50 Bid-YTW : 6.42 % |

| POW.PR.B | Perpetual-Discount | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 23.21 Evaluated at bid price : 23.51 Bid-YTW : 5.76 % |

| MFC.PR.J | FixedReset | -1.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.74 Bid-YTW : 5.82 % |

| FTS.PR.M | FixedReset | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 19.95 Evaluated at bid price : 19.95 Bid-YTW : 4.17 % |

| HSE.PR.G | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 21.61 Evaluated at bid price : 21.95 Bid-YTW : 4.82 % |

| BAM.PR.M | Perpetual-Discount | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 20.38 Evaluated at bid price : 20.38 Bid-YTW : 5.93 % |

| BAM.PF.F | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 21.86 Evaluated at bid price : 22.25 Bid-YTW : 4.18 % |

| CM.PR.Q | FixedReset | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 21.85 Evaluated at bid price : 22.30 Bid-YTW : 3.87 % |

| IFC.PR.A | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.43 Bid-YTW : 8.42 % |

| HSE.PR.E | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 21.86 Evaluated at bid price : 22.30 Bid-YTW : 4.83 % |

| PWF.PR.P | FixedReset | 1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 15.79 Evaluated at bid price : 15.79 Bid-YTW : 3.58 % |

| ENB.PR.J | FixedReset | 1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 16.19 Evaluated at bid price : 16.19 Bid-YTW : 5.32 % |

| BAM.PF.A | FixedReset | 1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 21.29 Evaluated at bid price : 21.58 Bid-YTW : 4.30 % |

| ENB.PR.B | FixedReset | 1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 14.03 Evaluated at bid price : 14.03 Bid-YTW : 5.57 % |

| TRP.PR.A | FixedReset | 1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 15.40 Evaluated at bid price : 15.40 Bid-YTW : 4.47 % |

| ENB.PR.A | Perpetual-Discount | 1.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 24.25 Evaluated at bid price : 24.55 Bid-YTW : 5.62 % |

| BAM.PR.R | FixedReset | 2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 16.45 Evaluated at bid price : 16.45 Bid-YTW : 4.67 % |

| HSE.PR.A | FixedReset | 2.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 13.55 Evaluated at bid price : 13.55 Bid-YTW : 4.57 % |

| ENB.PR.Y | FixedReset | 2.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 15.06 Evaluated at bid price : 15.06 Bid-YTW : 5.38 % |

| ENB.PF.G | FixedReset | 3.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 5.33 % |

| ENB.PF.C | FixedReset | 3.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 5.40 % |

| SLF.PR.B | Deemed-Retractible | 3.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.70 Bid-YTW : 6.68 % |

| TD.PF.E | FixedReset | 3.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 22.69 Evaluated at bid price : 23.82 Bid-YTW : 3.65 % |

| PWF.PR.S | Perpetual-Discount | 4.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 22.16 Evaluated at bid price : 22.50 Bid-YTW : 5.37 % |

| FTS.PR.H | FixedReset | 5.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 14.99 Evaluated at bid price : 14.99 Bid-YTW : 3.62 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| NA.PR.M | Deemed-Retractible | 184,940 | Called for redemption. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-09-25 Maturity Price : 25.50 Evaluated at bid price : 25.77 Bid-YTW : -4.76 % |

| RY.PR.B | Deemed-Retractible | 168,722 | RBC crossed two blocks of 50,000 each and one of 49,900, all at 25.00. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.94 Bid-YTW : 4.77 % |

| RY.PR.J | FixedReset | 68,048 | RBC crossed 50,000 at 22.55. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 22.11 Evaluated at bid price : 22.70 Bid-YTW : 3.72 % |

| ENB.PF.E | FixedReset | 45,964 | TD crossed 18,000 at 16.25. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 16.40 Evaluated at bid price : 16.40 Bid-YTW : 5.49 % |

| ENB.PF.G | FixedReset | 35,530 | TD crossed 18,600 at 16.85. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 5.33 % |

| TRP.PR.B | FixedReset | 31,097 | Nesbitt crossed 25,000 at 12.70. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-26 Maturity Price : 12.60 Evaluated at bid price : 12.60 Bid-YTW : 3.93 % |

| There were 29 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.G | FixedReset | Quote: 21.07 – 21.99 Spot Rate : 0.9200 Average : 0.6245 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 19.50 – 20.35 Spot Rate : 0.8500 Average : 0.6013 YTW SCENARIO |

| BAM.PR.X | FixedReset | Quote: 14.50 – 14.95 Spot Rate : 0.4500 Average : 0.2670 YTW SCENARIO |

| MFC.PR.N | FixedReset | Quote: 19.00 – 19.80 Spot Rate : 0.8000 Average : 0.6283 YTW SCENARIO |

| POW.PR.B | Perpetual-Discount | Quote: 23.51 – 23.96 Spot Rate : 0.4500 Average : 0.2919 YTW SCENARIO |

| RY.PR.H | FixedReset | Quote: 20.73 – 21.30 Spot Rate : 0.5700 Average : 0.4125 YTW SCENARIO |