I have often railed against the useless of regulatory make-work schemes; clearly, one of the most ridiculous is the anti-money-laundering set of regulations. I’ve quoted John Allison’s observation before, but now I’ll quote it again:

And then there was the Patriot Act, which was supposed to catch terrorists. I’ve talked to many people in government and they all do this dancing act, but the fact is there has never been a single terrorist caught and convicted because of the Patriot Act. The Act cost the banking industry more than $5 billion annually, and I would argue that no one is going to be caught. If you are dumb enough to get caught under the Patriot Act, you are going to get caught anyway. The only significant conviction of the Patriot Act was Eliot Spitzer, the governor of New York, who was convicted of soliciting prostitutes under a law designed to catch terrorists.

Since he wrote that, the authorities also seem to have caught John Hastert, who needed lots of cash because he was being blackmailed as discussed on May 28, 2015; knowing that victims of blackmail can be caught and exposed more easily and righteously should certainly cause us all to sleep better at night. But the direct human effects – beyond the financial cost for this make-work – has now been written about in a Globe story about Canadian “politically exposed persons”:

Those regulations propose a vast reach: For 20 years after the politically exposed persons (PEPs) leave office, the financial institutions will need to keep their eyes on them, their family and associates. The financial institutions’ first job is to identify the PEPs; then to assess their risk; and then, if the institutions determine the PEPs are a high risk – there is little public explanation on how the banks are expected to do this – they will need to monitor the PEPs’ account activity. The institutions will need to report suspicious activity (anything they suspect is connected to terrorism or money laundering) to a federal intelligence agency known as Fintrac, which investigates and can turn over files to the Mounties or the Canada Revenue Agency.

…

Ontario sisters Catherine and Emilie Taman both said in interviews they received mysterious phone calls from their separate banks, asking intrusive questions. (Emilie Taman is running for the New Democratic Party in an Ottawa riding in the federal election.) Catherine’s banker eventually explained why: Her mother was a foreign PEP. The Taman sisters’ mother is Ms. Arbour, who apart from being a retired Supreme Court judge is also a former international war-crimes prosecutor and a former United Nations human rights commissioner. Catherine said when she refused to answer the questions (on her mother’s advice), her account was frozen, which she discovered when she tried to use her bank card in a restaurant. A letter she provided to The Globe showed her bank asking questions such as, “From whom/where are you getting money?” “How did you accumulate your wealth/net worth?”How the banks knew the Taman sisters were Ms. Arbour’s daughters was a mystery to all three women, but experts contacted by The Globe say a small group of private companies provide lists of foreign PEPs and their families, and banks run new customers through those computerized lists, for a fee. There are similar lists for domestic PEPs.

In a commentary published in Thursday’s Globe, Ms. Arbour calls the program a “useless bureaucratic nightmare,” and says that her children should be left alone by their bankers.

The highlight of the story is a quote from one of the piggies at the trough:

“I think corruption is growing by leaps and bounds,” Garry Clement, a former national director of the RCMP’s proceeds of crime program, said in an interview. “It’s far greater than people are willing to accept.”

I have a message for Garry Clement: I don’t give a rat’s ass what you think and neither does anybody else with half a brain. Let’s see some proof. Let’s see some proof, first that corruption is growing by leaps and bounds and second that it needs to be addressed (I don’t care about corruption in Libya, the Libyans aren’t paying me anything to look after them) and third that these regulations are the best way to fight it. Proof that can stand up in court and has been used to convict real bad guys, not pathetic victims like Spitzer and Hastert.

I mentioned the folly of UK central planners with respect to buy-to-let housing on October 1. The scheme has now attracted the ire of Institute of Chartered Accountants in England & Wales:

Britain’s leading professional accounting body, the Institute of Chartered Accountants in England & Wales, has attacked the Chancellor’s controversial new tax on buy-to-let tax as “unfair and unreasonable”.

It condemns the legislation as “unthought-through” and predicts it will cause “extreme confusion”, as well as forcing some landlords out of business, distorting the market – and even making life harder for first-time buyers.

The new tax, which was not consulted upon and which The Telegraph is campaigning against, is included within the Finance Bill currently progressing through Parliament.

It will be phased in between 2017 and 2020, and effectively removes the ability of private landlords to offset the cost of their mortgage interest before arriving at a taxable profit.

…

While the proposed tax has found popularity among tenants, the ICAEW says it could exacerbate the property crisis and make it more difficult for first-time buyers.“The interest relief restriction will favour cash buyers who want to buy to let and may increase the competition even more at the lower end of the property market, thereby increasing prices and hindering first-time buyers.”

According to the Economist, Canadian housing is grossly overvalued, tied for most in the world (with Hong Kong) with respect to rents (89% rich) and highly ranked with respect to income (34% rich). Paul Matsiras of Moody’s claims:

“The risks are less around the rapid house price appreciation per se than the fact that, relative to incomes, homes in Toronto and Vancouver are increasingly becoming unaffordable either to own or to rent,” Moody’s economist Paul Matsiras said in his report.

“Canadian household debt has risen faster than disposable income since 2011, greatly increasing the debt burden for consumers and the risks of a pullback in spending as interest rates rise.”

He warned of difficulties as the key measure of household debt to disposable income rises, now standing at almost 165 per cent.

But fear not! In future photographs of G-7 meetings, Canada will display the best hair:

The country’s three major broadcasters — CTV, CBC and Global News — have projected a Liberal majority win. The Liberals won or were leading in 183 of the 338 House of Commons seats, with the Conservatives ahead in 98 and the New Democratic Party with 30, as of 10:36 p.m. Monday in Ottawa, according to preliminary results from Elections Canada. A party needs 170 seats for a majority.

…

The Canadian dollar fell after the networks called a Liberal victory, down 0.1 percent at 10 p.m. in Toronto to C$1.3040 per U.S. dollar, dropping for a third day. The currency has depreciated 10.9 percent against the U.S. dollar this year.

I’m very glad to see the end of the Bill C-51 boys, but I wish their replacements were led by somebody with a better claim to fame than being born. But we’ll see. Maybe we can stop obsessing about how other people dress, anyway.

Yee-haw!

Click for Big

Canadian preferred share investors were riding the bull today in the best day I can remember off the top of my head, with PerpetualDiscounts up 76bp, FixedResets winning an incredible 304bp and DeemedRetractibles gaining 35bp. The Performance Highlights table is much as you’d expect, with no less than a dozen issues – all FixedResets – gaining more than the 5% figure that usually indicates an absurdity of some kind. Volume was very high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

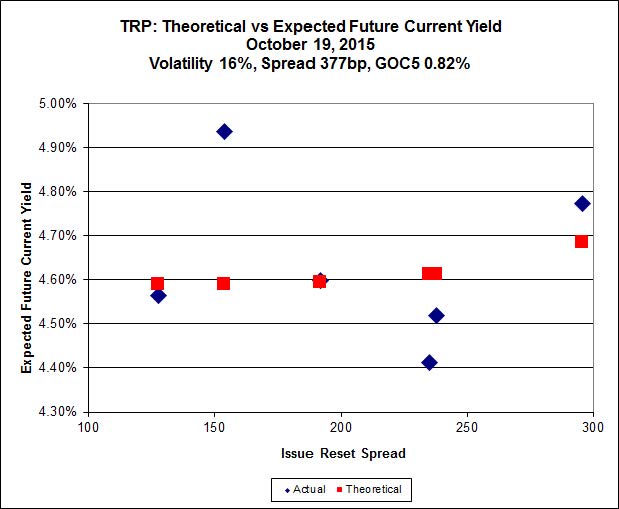

Here’s TRP:

Click for Big

Implied Volatility declined today but remains above what I consider reasonable.

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.96 to be $0.77 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.90 cheap at its bid price of 11.95.

Click for Big

There was some normalization from Friday‘s absurd results, but MFC.PR.F is still noticeably off the line defined by the other issues.

Most expensive is MFC.PR.F, resetting at +141bp on 2016-6-19, bid at 14.52 to be 0.85 rich, while MFC.PR.L resetting at +216bp on 2019-6-19, is bid at 17.09 to be 0.51 cheap.

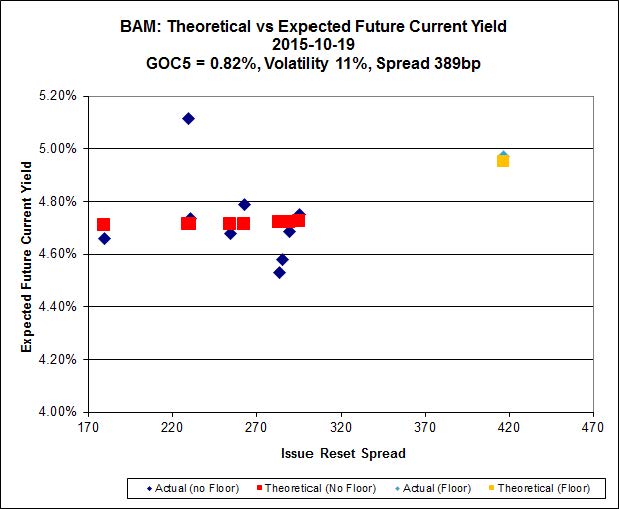

Click for Big

The fit on the BAM issues continues to be horrible!

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.25 to be $0.90 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 20.20 and appears to be $0.69 rich.

Click for Big

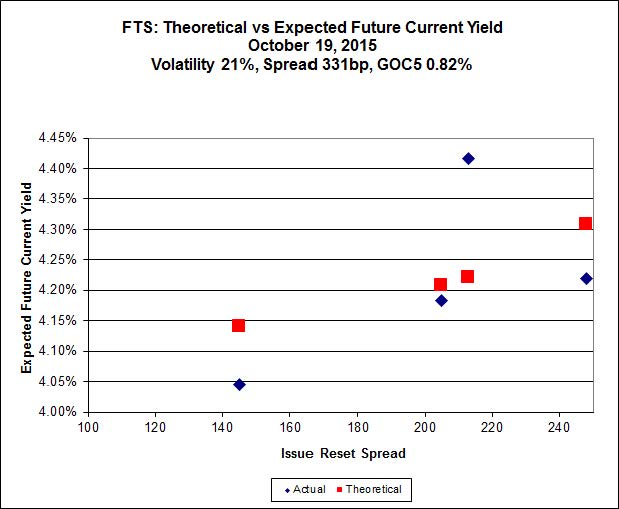

Implied Volatility declined substantially today but remains high.

FTS.PR.M, with a spread of +248bp, and bid at 19.55, looks $0.40 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 16.70 and is $0.78 cheap.

Click for Big

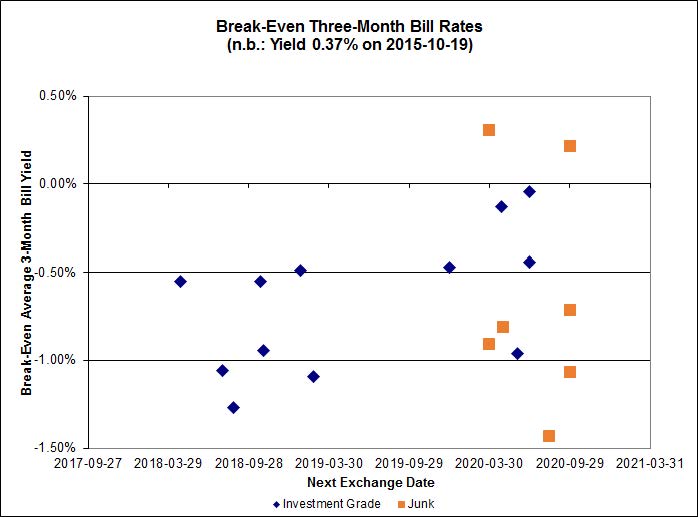

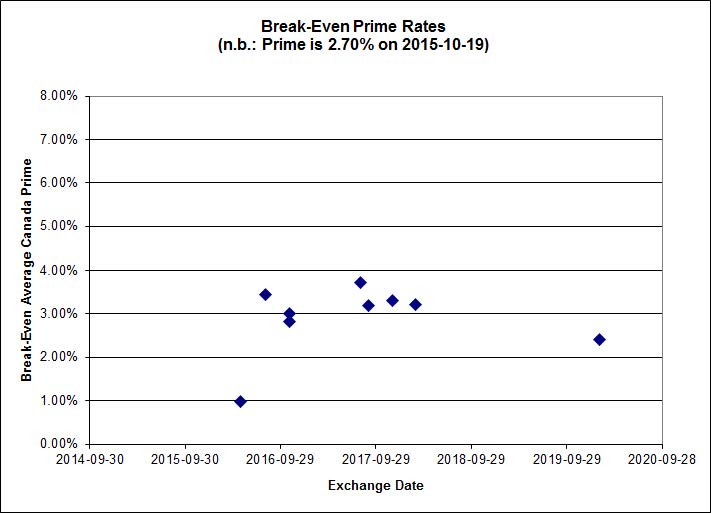

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.67%, with no outliers. The distribution is only slightly bimodal, with bank NVCC non-compliant pairs averaging -0.85% and other issues averaging -0.41%. There is one junk outlier above 0.50% and one below -1.50%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1924 % | 1,637.1 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1924 % | 2,862.4 |

| Floater | 4.54 % | 4.56 % | 62,422 | 16.32 | 3 | 0.1924 % | 1,740.3 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0648 % | 2,763.4 |

| SplitShare | 4.34 % | 5.16 % | 77,409 | 2.97 | 5 | 0.0648 % | 3,238.5 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0648 % | 2,526.8 |

| Perpetual-Premium | 5.92 % | 5.87 % | 67,825 | 13.99 | 5 | 0.9452 % | 2,458.4 |

| Perpetual-Discount | 5.74 % | 5.81 % | 79,938 | 14.16 | 33 | 0.7565 % | 2,484.8 |

| FixedReset | 5.22 % | 4.72 % | 202,387 | 15.41 | 76 | 3.0427 % | 1,954.6 |

| Deemed-Retractible | 5.26 % | 5.22 % | 103,649 | 5.45 | 33 | 0.3478 % | 2,532.2 |

| FloatingReset | 2.60 % | 4.51 % | 68,564 | 5.81 | 9 | 1.3760 % | 2,074.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.B | Floater | -1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 10.55 Evaluated at bid price : 10.55 Bid-YTW : 4.51 % |

| BAM.PR.C | Floater | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 10.24 Evaluated at bid price : 10.24 Bid-YTW : 4.65 % |

| PWF.PR.K | Perpetual-Discount | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 21.51 Evaluated at bid price : 21.77 Bid-YTW : 5.70 % |

| CU.PR.D | Perpetual-Discount | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 21.55 Evaluated at bid price : 21.55 Bid-YTW : 5.78 % |

| GWO.PR.I | Deemed-Retractible | 1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.59 Bid-YTW : 7.21 % |

| PWF.PR.L | Perpetual-Discount | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 22.06 Evaluated at bid price : 22.35 Bid-YTW : 5.71 % |

| BMO.PR.R | FloatingReset | 1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.90 Bid-YTW : 4.31 % |

| POW.PR.D | Perpetual-Discount | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 21.44 Evaluated at bid price : 21.70 Bid-YTW : 5.79 % |

| PWF.PR.F | Perpetual-Discount | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 22.24 Evaluated at bid price : 22.51 Bid-YTW : 5.84 % |

| TD.PF.F | Perpetual-Discount | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 22.07 Evaluated at bid price : 22.40 Bid-YTW : 5.47 % |

| BAM.PR.N | Perpetual-Discount | 1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 20.25 Evaluated at bid price : 20.25 Bid-YTW : 5.93 % |

| SLF.PR.B | Deemed-Retractible | 1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.43 Bid-YTW : 7.00 % |

| BMO.PR.Q | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.45 Bid-YTW : 6.77 % |

| PWF.PR.R | Perpetual-Discount | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 23.13 Evaluated at bid price : 23.51 Bid-YTW : 5.86 % |

| GWO.PR.N | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.09 Bid-YTW : 9.39 % |

| BNS.PR.Q | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.06 Bid-YTW : 4.51 % |

| SLF.PR.G | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.70 Bid-YTW : 8.92 % |

| BAM.PR.M | Perpetual-Discount | 1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 20.30 Evaluated at bid price : 20.30 Bid-YTW : 5.91 % |

| BNS.PR.B | FloatingReset | 1.66 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.40 Bid-YTW : 4.67 % |

| GWO.PR.R | Deemed-Retractible | 1.67 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.90 Bid-YTW : 6.69 % |

| MFC.PR.B | Deemed-Retractible | 1.71 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.77 Bid-YTW : 7.29 % |

| PWF.PR.O | Perpetual-Premium | 1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 24.45 Evaluated at bid price : 24.75 Bid-YTW : 5.87 % |

| BMO.PR.Z | Perpetual-Discount | 1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 22.35 Evaluated at bid price : 22.65 Bid-YTW : 5.50 % |

| MFC.PR.J | FixedReset | 1.89 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.36 Bid-YTW : 7.04 % |

| PWF.PR.H | Perpetual-Premium | 1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 24.29 Evaluated at bid price : 24.60 Bid-YTW : 5.86 % |

| TRP.PR.C | FixedReset | 1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 11.95 Evaluated at bid price : 11.95 Bid-YTW : 4.99 % |

| GWO.PR.S | Deemed-Retractible | 1.98 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.75 Bid-YTW : 6.04 % |

| TRP.PR.D | FixedReset | 2.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 17.70 Evaluated at bid price : 17.70 Bid-YTW : 4.76 % |

| BMO.PR.Y | FixedReset | 2.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 20.66 Evaluated at bid price : 20.66 Bid-YTW : 4.49 % |

| FTS.PR.H | FixedReset | 2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 14.03 Evaluated at bid price : 14.03 Bid-YTW : 4.21 % |

| RY.PR.I | FixedReset | 2.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.50 Bid-YTW : 4.40 % |

| MFC.PR.H | FixedReset | 2.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.13 Bid-YTW : 5.76 % |

| TD.PF.E | FixedReset | 2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 20.25 Evaluated at bid price : 20.25 Bid-YTW : 4.58 % |

| CU.PR.C | FixedReset | 2.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 19.15 Evaluated at bid price : 19.15 Bid-YTW : 4.36 % |

| PWF.PR.P | FixedReset | 2.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 14.44 Evaluated at bid price : 14.44 Bid-YTW : 4.23 % |

| BAM.PR.R | FixedReset | 2.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 15.25 Evaluated at bid price : 15.25 Bid-YTW : 5.31 % |

| BMO.PR.M | FixedReset | 2.45 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.85 Bid-YTW : 3.84 % |

| MFC.PR.G | FixedReset | 2.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.85 Bid-YTW : 6.29 % |

| SLF.PR.C | Deemed-Retractible | 2.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.36 Bid-YTW : 7.31 % |

| TRP.PR.E | FixedReset | 2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 17.96 Evaluated at bid price : 17.96 Bid-YTW : 4.77 % |

| BNS.PR.P | FixedReset | 2.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.57 Bid-YTW : 4.12 % |

| NA.PR.Q | FixedReset | 2.72 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.15 Bid-YTW : 4.03 % |

| BMO.PR.T | FixedReset | 2.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 4.58 % |

| FTS.PR.G | FixedReset | 2.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 16.70 Evaluated at bid price : 16.70 Bid-YTW : 4.72 % |

| BAM.PF.E | FixedReset | 2.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 18.01 Evaluated at bid price : 18.01 Bid-YTW : 5.11 % |

| PWF.PR.S | Perpetual-Discount | 2.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 21.33 Evaluated at bid price : 21.62 Bid-YTW : 5.56 % |

| RY.PR.J | FixedReset | 3.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 19.23 Evaluated at bid price : 19.23 Bid-YTW : 4.72 % |

| IFC.PR.A | FixedReset | 3.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.10 Bid-YTW : 9.74 % |

| SLF.PR.H | FixedReset | 3.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.85 Bid-YTW : 8.26 % |

| BMO.PR.W | FixedReset | 3.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 17.55 Evaluated at bid price : 17.55 Bid-YTW : 4.66 % |

| TD.PF.B | FixedReset | 3.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 17.83 Evaluated at bid price : 17.83 Bid-YTW : 4.56 % |

| SLF.PR.I | FixedReset | 3.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.70 Bid-YTW : 6.87 % |

| HSE.PR.C | FixedReset | 3.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 4.80 % |

| IFC.PR.C | FixedReset | 3.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.55 Bid-YTW : 7.55 % |

| HSE.PR.A | FixedReset | 3.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 13.80 Evaluated at bid price : 13.80 Bid-YTW : 4.79 % |

| TRP.PR.A | FixedReset | 3.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 14.90 Evaluated at bid price : 14.90 Bid-YTW : 4.87 % |

| BMO.PR.S | FixedReset | 3.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 18.51 Evaluated at bid price : 18.51 Bid-YTW : 4.56 % |

| MFC.PR.K | FixedReset | 3.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.37 Bid-YTW : 8.17 % |

| BAM.PF.F | FixedReset | 3.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 20.09 Evaluated at bid price : 20.09 Bid-YTW : 4.85 % |

| MFC.PR.I | FixedReset | 3.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.76 Bid-YTW : 6.39 % |

| RY.PR.H | FixedReset | 3.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 18.06 Evaluated at bid price : 18.06 Bid-YTW : 4.58 % |

| BNS.PR.C | FloatingReset | 4.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.99 Bid-YTW : 4.38 % |

| TRP.PR.G | FixedReset | 4.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 19.80 Evaluated at bid price : 19.80 Bid-YTW : 4.86 % |

| TRP.PR.F | FloatingReset | 4.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 13.35 Evaluated at bid price : 13.35 Bid-YTW : 4.32 % |

| BNS.PR.R | FixedReset | 4.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.75 Bid-YTW : 4.23 % |

| TD.PF.D | FixedReset | 4.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 4.57 % |

| RY.PR.M | FixedReset | 4.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 4.60 % |

| RY.PR.Z | FixedReset | 4.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 18.08 Evaluated at bid price : 18.08 Bid-YTW : 4.53 % |

| FTS.PR.K | FixedReset | 4.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 17.15 Evaluated at bid price : 17.15 Bid-YTW : 4.56 % |

| CM.PR.Q | FixedReset | 4.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 20.56 Evaluated at bid price : 20.56 Bid-YTW : 4.41 % |

| VNR.PR.A | FixedReset | 4.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 19.88 Evaluated at bid price : 19.88 Bid-YTW : 4.70 % |

| BAM.PF.G | FixedReset | 4.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 4.85 % |

| CM.PR.P | FixedReset | 4.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 17.95 Evaluated at bid price : 17.95 Bid-YTW : 4.52 % |

| BAM.PF.B | FixedReset | 4.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 18.01 Evaluated at bid price : 18.01 Bid-YTW : 5.06 % |

| MFC.PR.L | FixedReset | 4.72 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.09 Bid-YTW : 8.50 % |

| TD.PF.A | FixedReset | 4.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 18.07 Evaluated at bid price : 18.07 Bid-YTW : 4.51 % |

| FTS.PR.M | FixedReset | 5.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 19.55 Evaluated at bid price : 19.55 Bid-YTW : 4.52 % |

| PWF.PR.T | FixedReset | 5.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 21.39 Evaluated at bid price : 21.39 Bid-YTW : 3.94 % |

| CM.PR.O | FixedReset | 5.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 18.39 Evaluated at bid price : 18.39 Bid-YTW : 4.52 % |

| TD.PF.C | FixedReset | 5.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 17.90 Evaluated at bid price : 17.90 Bid-YTW : 4.53 % |

| NA.PR.S | FixedReset | 5.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 18.16 Evaluated at bid price : 18.16 Bid-YTW : 4.68 % |

| BAM.PF.A | FixedReset | 5.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 4.90 % |

| MFC.PR.M | FixedReset | 5.66 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.29 Bid-YTW : 7.75 % |

| IAG.PR.G | FixedReset | 5.76 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.20 Bid-YTW : 6.68 % |

| MFC.PR.N | FixedReset | 5.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.00 Bid-YTW : 7.89 % |

| BIP.PR.A | FixedReset | 5.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 20.40 Evaluated at bid price : 20.40 Bid-YTW : 5.47 % |

| BAM.PR.T | FixedReset | 6.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 16.52 Evaluated at bid price : 16.52 Bid-YTW : 4.99 % |

| NA.PR.W | FixedReset | 6.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 17.90 Evaluated at bid price : 17.90 Bid-YTW : 4.57 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.B | FixedReset | 158,635 | Nesbitt crossed 19,300 at 17.30; RBC crossed 107,800 at 18.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 17.83 Evaluated at bid price : 17.83 Bid-YTW : 4.56 % |

| TRP.PR.B | FixedReset | 139,492 | Scotia crossed 58,500 at 11.40 and another 50,000 at 11.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 11.50 Evaluated at bid price : 11.50 Bid-YTW : 4.65 % |

| BMO.PR.W | FixedReset | 137,345 | RBC crossed 110,400 at 17.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 17.55 Evaluated at bid price : 17.55 Bid-YTW : 4.66 % |

| TD.PF.A | FixedReset | 110,520 | TD crossed 23,500 at 17.41; RBC crossed 23,800 at 17.75. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 18.07 Evaluated at bid price : 18.07 Bid-YTW : 4.51 % |

| RY.PR.H | FixedReset | 73,588 | RBC crossed 30,000 at 17.86. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-19 Maturity Price : 18.06 Evaluated at bid price : 18.06 Bid-YTW : 4.58 % |

| MFC.PR.J | FixedReset | 72,700 | Nesbitt crossed 31,000 at 19.02 and 20,000 at 19.22. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.36 Bid-YTW : 7.04 % |

| There were 61 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TRP.PR.E | FixedReset | Quote: 17.96 – 20.00 Spot Rate : 2.0400 Average : 1.3076 YTW SCENARIO |

| HSE.PR.G | FixedReset | Quote: 22.75 – 23.54 Spot Rate : 0.7900 Average : 0.4964 YTW SCENARIO |

| RY.PR.N | Perpetual-Discount | Quote: 22.65 – 23.24 Spot Rate : 0.5900 Average : 0.3439 YTW SCENARIO |

| TRP.PR.D | FixedReset | Quote: 17.70 – 18.40 Spot Rate : 0.7000 Average : 0.4649 YTW SCENARIO |

| TD.PR.Z | FloatingReset | Quote: 21.31 – 22.00 Spot Rate : 0.6900 Average : 0.4746 YTW SCENARIO |

| TD.PF.E | FixedReset | Quote: 20.25 – 20.85 Spot Rate : 0.6000 Average : 0.3876 YTW SCENARIO |

Now this post hit a nerve.

A few years ago we decided to move back to TO and enter our Golden Years, so to speak. So, with that we set about to collect our eggs and nest them all in one tree called BMO.

Opening those accts. a few years ago I stated my occupation as “Retired”. It was and is true.

However a few months ago, I made a deposit into a Investor Line acct. and the a few days later. Presto, it was frozen. I called and they said I needed to visit a local branch and see the Investor Line Rep.

I met w/ the Rep the following morning and while sitting he made some inquiries inquiries and found out such a deposit for a person who was retired set off red flags and thus my acct. was frozen. And the local Investor Line rep proceeded to ask where I rec’d the funds from. He also explained the the US Gov has requirements for Cdn Banks w/r/t reporting funds rec’d.

I explained that I had sold a vehicle. He asked to see a rec’t. Nope was not going to happen.

We kicked my issue up the food chain a few times where I was told this was a simple mater of explaining where the money came from. And that they had no record of employment for me (direct deposits/pay history. “Such information would be helpful”.

I gave nothing. We eventually resolved the matter. The intrusion into my privacy was not appreciated. I am left w/ the question: Is my banking history my personal and private information? The answer is no.

The intrusion into my privacy was not appreciated. I am left w/ the question: Is my banking history my personal and private information? The answer is no.

Thanks for posting this.

I can only suggest that you pass this story on to your (new?) MP with a copy to the new Finance Minister and tell them you don’t like this kind of snooping. You might also wish to contact the British Columbia Civil Liberties Association, who made a presentation to the House of Commons committee studying the issue; you may also be interested in the committee’s final report.

You may also be interested in the 2013 Audit of FINTRAC by the Privacy Commissioner.

He also explained the the US Gov has requirements for Cdn Banks w/r/t reporting funds rec’d.

One thing I’ve learned in this business is that hardly anybody understands why they do things and information you get from front-line staff will almost always be incorrect. Company policy gets labelled as regulation, regulation gets labelled as law, law gets labelled as normal and every possible combination of these explanations is used, almost always in good faith.