Manulife Financial Corporation has announced:

that it has completed its offering of 16 million Non-cumulative Rate Reset Class 1 Shares Series 21 (the “Series 21 Preferred Shares”) at a price of $25 per share to raise gross proceeds of $400 million.

The offering was underwritten by a syndicate of investment dealers co-led by RBC Capital Markets, Scotia Capital Inc. and TD Securities Inc. The Series 21 Preferred Shares commence trading on the Toronto Stock Exchange today under the ticker symbol MFC.PR.O.

Manulife has granted the underwriters’ an option, exercisable in whole or in part, to purchase up to an additional 1 million Series 21 Preferred shares at the same offering price. The underwriters have 30 days from the closing of the preferred share offering to exercise the option.

The Series 21 Preferred Shares were issued under a prospectus supplement dated February 18, 2016 to Manulife’s short form base shelf prospectus dated December 17, 2015.

MFC.PR.O is a FixedReset, 5.60%+497, announced 2016-2-16. The issue will be tracked by HIMIPref™ and assigned to the FixedReset subindex.

As this issue is from an insurer and there is no provision for conversion into common shares at the option of the issuer, I consider this to be subject to my Deemed Retraction policy; accordingly I have placed a maturity entry dated 2025-1-31 at par in the call schedule of this instrument for analytical purposes. Note that this approach is due to analysis and there is no contractual provision in the terms of issue for any such maturity.

The issue traded 753,902 shares today (consolidated exchanges) in a range of 24.80-92 before closing at 24.86-89, 82×36. Since announcement date, the TXPL total return index has increased by 43bp since the announcement date, so ‘a little soft’ is an appropriate appraisal of its performance.

Vital statistics are:

| MFC.PR.O | FixedReset | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.86 Bid-YTW : 5.71 % |

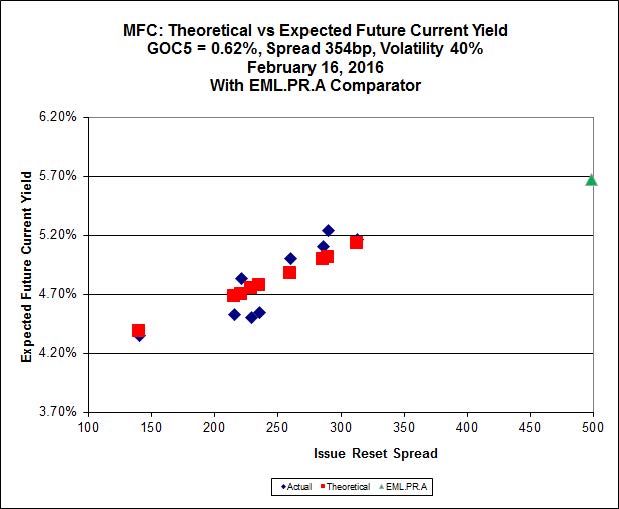

Implied volatility analysis indicates the issue is expensive at its current level:

Click for Big

According to this, the fair value for MFC.PR.O is 23.74 – and even at that, the slope of the theoretical line is clearly flattened by the influence of this issue. The issue is clearly well off the line defined by the lower-spread MFC issues.