Fairfax Financial Holdings Limited has announced (emphasis added):

that the Toronto Stock Exchange (the “TSX”) accepted a notice filed by Fairfax of its intention to commence a Normal Course Issuer Bid for its Subordinate Voting Shares, Cumulative 5-Year Rate Reset Preferred Shares, Series C (“Series C Shares”), Cumulative Floating Rate Preferred Shares, Series D (“Series D Shares”), Cumulative 5-Year Rate Reset Preferred Shares, Series E (“Series E Shares”), Cumulative Floating Rate Preferred Shares, Series F (“Series F Shares”), Cumulative 5-Year Rate Reset Preferred Shares, Series G (“Series G Shares”), Cumulative 5-Year Rate Reset Preferred Shares, Series I (“Series I Shares”), Cumulative 5-Year Rate Reset Preferred Shares, Series K (“Series K Shares”) and Cumulative 5-Year Rate Reset Preferred Shares, Series M (“Series M Shares” and, together with the Series C Shares, Series D Shares, Series E Shares, Series F Shares, Series G Shares, Series I Shares and Series K Shares, the “Preferred Shares”) through the facilities of the TSX (or other alternative Canadian trading systems). Purchases will be made in accordance with the rules and policies of the TSX and Subordinate Voting Shares and Preferred Shares purchased will be cancelled.

The notice provides that Fairfax’s board of directors has approved the purchase on the TSX, during the period commencing September 28, 2015 and ending September 27, 2016, of up to 800,000 Subordinate Voting Shares, 601,538 Series C Shares, 398,361 Series D Shares, 405,134 Series E Shares, 357,204 Series F Shares, 1,000,000 Series G Shares, 1,200,000 Series I Shares, 950,000 Series K Shares and 920,000 Series M Shares, representing approximately 3.7% of the public float in respect of the Subordinate Voting Shares and 10% of the public float in respect of each series of Preferred Shares. As at September 21, 2015, Fairfax had outstanding 22,034,939 Subordinate Voting Shares, 6,016,384 Series C Shares, 3,983,616 Series D Shares, 4,051,346 Series E Shares, 3,572,044 Series F Shares, 10,000,000 Series G Shares, 12,000,000 Series I Shares, 9,500,000 Series K Shares and 9,200,000 Series M Shares. Under the bid, Fairfax may purchase up to 6,966 Subordinate Voting Shares, 1,881 Series C Shares, 1,426 Series D Shares, 1,908 Series E Shares, 1,151 Series F Shares, 2,695 Series G Shares, 3,394 Series I Shares, 2,919 Series K Shares and 5,713 Series M Shares on the TSX (or other alternative Canadian trading systems) during any trading day, each of which represents 25% of the average daily trading volume on the TSX calculated in accordance with the rules of the TSX. This limitation does not apply to purchases made pursuant to block purchase exemptions.

From time to time, when Fairfax does not possess material nonpublic information about itself or its securities, it may, in accordance with the requirements of applicable securities laws and the TSX, enter into a pre-defined plan with its broker to allow for the purchase of its Subordinate Voting Shares or Preferred Shares, as the case may be, under the bid at times when it ordinarily would not be active in the market due to its own internal trading blackout periods.

Fairfax is making this Normal Course Issuer Bid because it believes that in appropriate circumstances its Subordinate Voting Shares and Preferred Shares represent an attractive investment opportunity and that, with respect to the Subordinate Voting Shares, purchases under the bid will enhance the value of the Subordinate Voting Shares held by the remaining shareholders.

Pursuant to its existing normal course issuer bid for its Subordinate Voting Shares, Fairfax has purchased 127,309 of its Subordinate Voting Shares and 376,610 of its Series E Shares during the last twelve months at weighted average prices per share of Cdn.$671.76 and Cdn.$16.89, respectively.

Fairfax is a holding company which, through its subsidiaries, is engaged in property and casualty insurance and reinsurance and investment management.

It will be remembered that NCIBs, as a general rule, are public relations exercises by the announcing companies and are only rarely given effect. However, there was a real, if small, buy-back of BRF preferreds earlier this year and now it looks like there is another exception to the usual case.

FFH.PR.E was issued as a FixedReset FixedReset 4.75%+216, that commenced trading 2010-2-1 after being announced 2010-1-21. The dividend was reset to 2.91% effective 2015-3-31 and there was a 31% conversion to the FFH.PR.F FloatingReset, after which I reported:

there were 7,915,539 shares of FFH.PR.E outstanding relative to 3,572,044 shares of the FloatingReset FFH.PR.F.

This cannot be right since only eight million FFH.PR.E were originally issued! Oopsy.

TMXMoney now reports 4,074,543 shares of FFH.PR.E outstanding. compared to 3,572,044 of the FFH.PR.F; the total is 7,646,587, which although looking reasonable does not allow for the cancellation of the 376,610 shares of FFH.PR.E mentioned in the press release. So either there are some shares sitting in the FFH treasury that have not yet been cancelled, or there’s some kind of timing difference or (shock! horror!) the Toronto Stock Exchange has made a mistake, but I suppose these figures are close enough for government work.

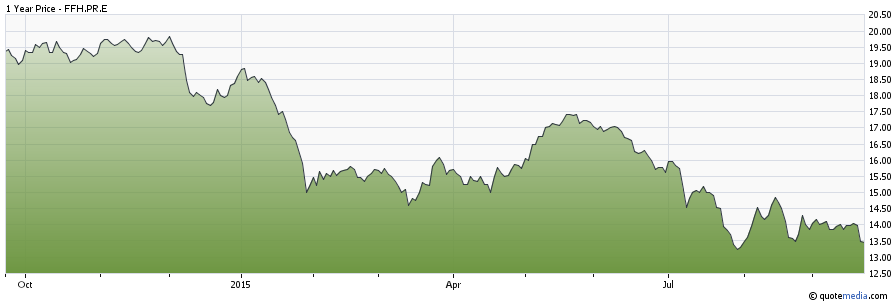

The pricing behaviour for the prior year, combined with the average reported price of $16.89, suggests that the bulk of the buying was done in 2015:

Click for Big

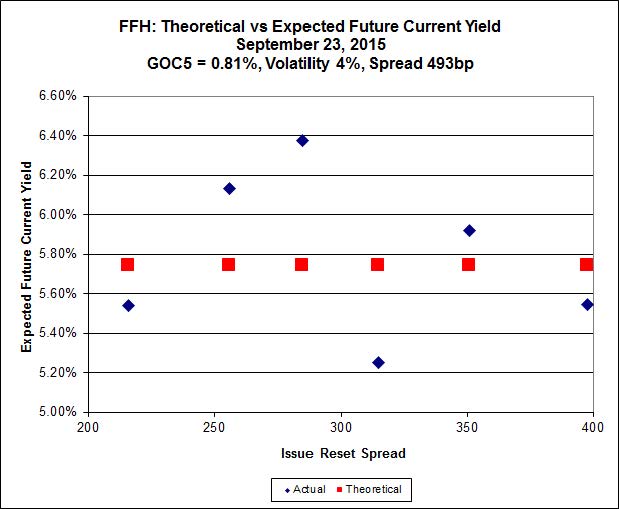

Click for BigIt is of interest to note that FFH.PR.E, resetting at +216bp over GOC-5, is the lowest-spread issue among the six FFH issues. The current comparison with other FFH FixedResets shows Implied Volatility is negligible:

Click for Big

Click for BigThe Implied Volatility of the FFH series has been quite low all year, implying that the lower-spread issues, as a group have been cheap relative to the higher-spread issues.