DBRS has announced:

has today downgraded Enbridge Inc.’s (ENB) Issuer Rating and Medium-Term Notes & Unsecured Debentures rating to BBB (high) from A (low), Commercial Paper rating to R-2 (high) from R-1 (low) and Cumulative Redeemable Preferred Shares rating to Pfd-3 (high) from Pfd-2 (low). The trends are all Stable. ENB’s ratings were placed Under Review with Developing Implications on December 3, 2014, and changed to Under Review with Negative Implications on June 19, 2015 (please see DBRS press releases for details). The current action removes the ratings from Under Review with Negative Implications.

The ENB ratings downgrade is consistent with DBRS’s expectations as noted in the June 19, 2015, press release and follows today’s approval by the public shareholders of Enbridge Income Fund Holdings Inc. (EIFH) of the Transaction described below. For the rationale for the downgrade of ENB’s ratings, please see “Impact on ENB – Update”, below.

…

IMPACT ON ENB – UPDATE

Following its review of the EIFH Management Information Circular (MIC), DBRS continues to believe that the combination of the Transaction and the EECI Transfer have negatively impacted ENB’s credit risk profile. Please see the June 19, 2015, DBRS press release for the main factors leading to that conclusion.Prior to closing, EPA will issue a senior unsecured promissory note to ENB with a principal amount of approximately $4.1 billion (the Mirror Note), representing a portion of the required capitalization of EPA. Payments of principal and interest by EPA thereunder have been structured to mirror the payments of certain principal and interest required under certain Canadian MTNs issued by ENB.

While DBRS recognizes that the $4.1 billion Mirror Note provides ENB with a senior claim on EPA assets ranking ahead of EIF bond holder claims, this factor does not fully offset the increased structural subordination with respect to EPI’s assets and the loss of full access to EPA cash flows available prior to the Transaction.

Based on its review, DBRS has downgraded all of ENB’s ratings by one notch, with Stable trends following completion of the Transaction.

The two earlier warnings from DBRS were reported in PrefBlog in the posts Rating Agencies Unhappy With Enbridge and ENB Finalizes Dropdown; S&P Downgrades To P-2(low); DBRS Review-Negative.

Moody’s downgraded the ENB preferreds to junk in June, 2015.

Affected issues are: ENB.PF.A, ENB.PF.C, ENB.PF.E, ENB.PF.G, ENB.PR.A, ENB.PR.B, ENB.PR.D, ENB.PR.F, ENB.PR.H, ENB.PR.J, ENB.PR.N, ENB.PR.P, ENB.PR.T and ENB.PR.Y.

This is a major development: ENB issues comprise about 10% of the preferred share universe. If we look at the CPD credit quality breakdown, we find the sponsor indicates levels of 75.67% investment grade, 22.37% junk and 1.66% “other” (I confess I’m not sure what is meant by “other”). A shift of 10% between groups is significant!

I also note that the BMO-CM “50” index is 9.07% ENB issues.

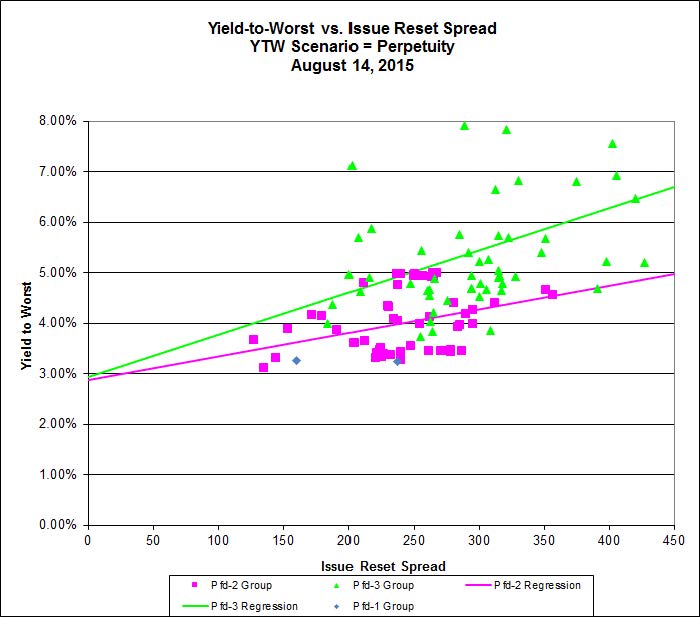

I do not expect significant price action as a result of this downgrade – it was well telegraphed in advance and Enbridge fans can comfort themselves with the thought that the issues remain investment-grade according to S&P. Additionally, we may examine Chart FR-29 from the August PrefLetter:

Click for Big

This chart shows the relationship between Issue Reset Spread and YTW for all FixedResets for which the YTW Scenario is extension until perpetuity. Correlations are fairly low, 10% for the “Pfd-2 Group” (issues rated Pfd-2(high), Pfd-2 and Pfd-2(low) by DBRS) and 15% for the Pfd-3 Group, but given that all information about each issue other than Issue Reset Spread, credit group, YTW and YTW-scenario has been thrown out, I’d say it’s close enough for government work!

The point is … see those purple boxes (Pfd-2 Group) that are right smack dab on top of the Pfd-3 Group regression line? That’s Enbridge. The downgrade has been anticipated by the market; we can construct the following table:

| ENB FixedResets – Predicted vs. Actual YTW August 14, 2015 |

||||

| Ticker | Issue Reset Spread |

Predicted YTW Pfd-2 |

Predicted YTW Pfd-3 |

Actual YTW |

| ENB.PF.A | 266 | 4.11% | 5.16% | 4.91% |

| ENB.PF.C | 264 | 4.10% | 5.14% | 4.90% |

| ENB.PF.E | 266 | 4.11% | 5.16% | 4.90% |

| ENF.PF.G | 268 | 4.12% | 5.18% | 4.98% |

| ENB.PR.B | 240 | 3.99% | 4.94% | 4.97% |

| ENB.PR.D | 237 | 3.97% | 4.92% | 4.97% |

| ENB.PR.F | 251 | 4.04% | 5.03% | 4.97% |

| ENB.PR.H | 212 | 3.85% | 4.71% | 4.78% |

| ENB.PR.J | 257 | 4.07% | 5.08% | 4.93% |

| ENB.PR.N | 265 | 4.10% | 5.15% | 4.98% |

| ENB.PR.P | 250 | 4.03% | 5.03% | 4.93% |

| ENB.PR.T | 250 | 4.03% | 5.03% | 4.95% |

| ENB.PR.Y | 238 | 3.98% | 4.92% | 4.75% |

Still, there will always be some investors who are surprised and others who were hoping a longshot affirmation would come through – so we’ll just see what the coming weeks bring by way of price movement!