It will be recalled that BNS.PR.Y will reset to 1.82% effective April 26 and that BRF.PR.A will reset to 3.355% effective April 30.

Holders of both securities have the option to convert to FloatingResets, which will pay 3-month bills plus 100bp and plus 262bp, respectively. Deadlines for notifying the company of the intent to convert are April 13 and April 15, respectively; note that these are company deadlines and that brokers will generally set their deadlines a day or two in advance, so there’s not much time to lose if you’re planning to convert! Also, I realize that Monday will be the last day to notify BNS of intent to convert and that brokerage deadlines will have passed; but the brokerage deadline is just the date they want to know their answers. They’ll probably do it on a ‘best efforts’ basis when notified on the last day, if you grovel in a sufficiently entertaining fashion.

The most logical way to analyze the question of whether or not to convert is through the theory of Preferred Pairs, for which a calculator is available. Briefly, a Strong Pair is defined as a pair of securities that can be interconverted in the future (e.g., BNS.PR.Y and the FloatingReset that will exist if enough holders convert). Since they will be interconvertible on this future date, it may be assumed that they will be priced identically on this date (if they aren’t then holders will simply convert en masse to the higher-priced issue). And since they will be priced identically on a given date in the future, any current difference in price must be offset by expectations of an equal and opposite value of dividends to be received in the interim. And since the dividend rate on one element of the pair is both fixed and known, the implied average rate of the other, floating rate, instrument can be determined. Finally, we say, we may compare these average rates and take a view regarding the actual future course of that rate relative to the implied rate, which will provide us with guidance on which element of the pair is likely to outperform the other until the next interconversion date, at which time the process will be repeated.

To this end, we may construct a table showing similar pairs currently trading:

| Fixed Reset |

Fixed Rate |

Floating Reset |

Spread over Bills |

Bid Price

Fixed Reset |

Bid Price

Floating Reset |

Break-Even 3-Month Bill Rate |

| Investment Grade |

| BNS.PR.P |

3.35% |

BNS.PR.A |

205 |

25.12 |

25.35 |

0.19% |

| TD.PR.S |

3.371% |

TD.PR.T |

160 |

25.07 |

23.96 |

0.28% |

| BMO.PR.M |

3.39% |

BMO.PR.R |

165 |

25.17 |

24.12 |

0.36% |

| BNS.PR.Q |

3.61% |

BNS.PR.B |

170 |

25.25 |

23.91 |

0.21% |

| TD.PR.Y |

3.5595% |

TD.PR.Z |

168 |

25.30 |

23.95 |

0.17% |

| BNS.PR.R |

3.83% |

BNS.PR.C |

188 |

25.37 |

24.05 |

0.36 |

| RY.PR.I |

3.52% |

RY.PR.K |

193 |

25.41 |

24.25 |

0.23% |

| TRP.PR.A |

3.266% |

TRP.PR.F |

192 |

18.90 |

19.01 |

1.46% |

| Junk |

| DC.PR.B |

5.688% |

DC.PR.D |

410 |

23.71 |

20.50 |

-2.05% |

| AZP.PR.B |

5.57% |

AZP.PR.C |

418 |

13.70 |

13.26 |

0.84% |

| FFH.PR.C |

4.578% |

FFH.PR.D |

315 |

21.13 |

20.02 |

0.25% |

| AIM.PR.A |

4.50% |

AIM.PR.B |

375 |

19.41 |

19.55 |

0.89% |

| FFH.PR.E |

2.91% |

FFH.PR.F |

216 |

15.32 |

14.70 |

0.13% |

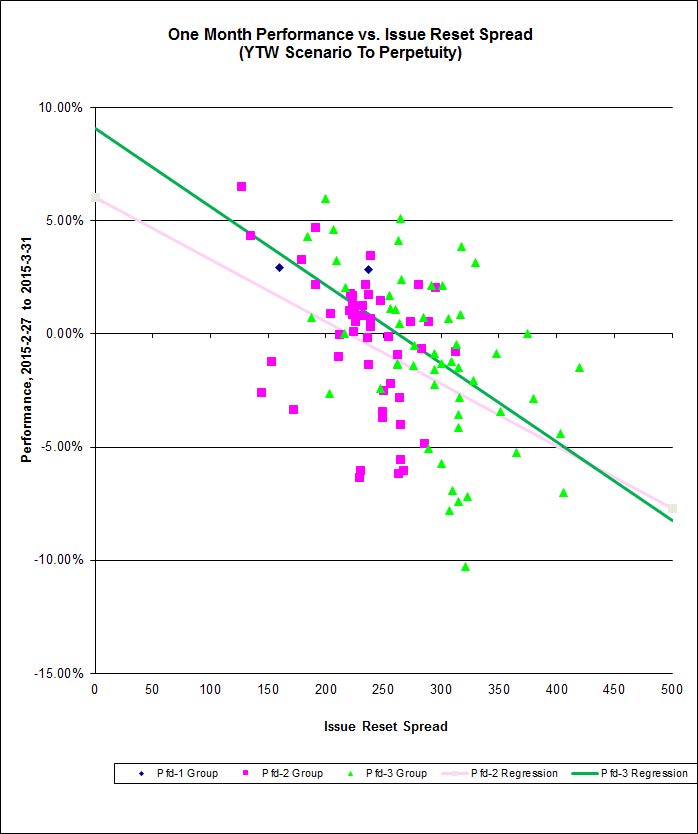

We can show this graphically by plotting the implied average 3-month bill rate against the next Exchange Date (which is the date to which the average will be calculated).

Click for Big

Click for BigThe market appears to have a distaste at the moment for floating rate product; the implied rates until the next interconversion are all (except one!) lower than the current 3-month bill rate and one is significantly negative! Whatever might be the result of the next few Bank of Canada overnight rate decisions, I suggest that it is unlikely that the average rate over the next five years will be lower than current – but if you disagree, of course, you may interpret the data any way you like.

Since credit quality of each element of the pair is equal to the other element, it should not make any difference whether the pair examined is investment-grade or junk, although we might expect greater variation of implied rates between junk issues on grounds of lower liquidity. The average in the table above for the junk issues (except DC.PR.B / DC.PR.D) is about +0.53%; for the investment grade issues (except TRP.PR.A / TRP.PR.F) it is about 0.26%. There will be more on these exceptions later, but if we plug in these implied yields and the current bid prices of the FixedResets, we may construct the following table showing consistent prices for the two pairs under consideration:

| Estimate of FloatingReset Trading Price In Current Conditionss |

| |

Assumed FloatingReset

Price if Implied Bill

is equal to |

| FixedReset |

Bid Price |

Spread |

+0.26% |

+0.53% |

| BNS.PR.Y |

21.70 |

100bp |

21.06 |

21.37 |

| BRF.PR.A |

18.01 |

262bp |

17.52 |

17.80 |

Based on current market conditions, I suggest that the FloatingResets that may result from conversion of BNS.PR.Y and BRF.PR.A will be cheap and trading a little below the price of the continuing FixedResets. Therefore, I recommend that holders of BNS.PR.Y and BRF.PR.A continue to hold these issues and not to convert. I will note that, given the apparent cheapness of the FloatingResets, it may be a good trade to swap the FixedReset for the FloatingReset in the market once both elements of each pair are trading. But that, of course, will depend on the prices at that time.

Now, about those two exceptions.

The first exception, TRP.PR.A / TRP.PR.F, is problematical. It is notable that the break-even rate has moved dramatically upwards in the course of the last week – on April 2, this pair was an outlier to the downside; which is equivalent to saying that the FloatingReset, TRP.PR.F, has significantly outperformed the FixedReset, TRP.PR.A, during this week’s downdraft. It is tempting to write off the difference as a mere fluctuation, but on the other hand this pair is unique in another way: it is the only investment-grade pair that is not an NVCC non-compliant issue from a bank; which is to say that it is the only investment-grade pair not subject to a DeemedMaturity; which is to say it is the only investment-grade pair for which it is (deemed!) possible to exist to perpetuity, which is in fact the YTW scenario for each pair.

It is possible that the market is trading these issues such that the bank FixedResets with DeemedMaturities have these DeemedMaturities recognized and therefore, quite rightly, have outperformed their FixedResets considered likely to be extant in perpetuity during the week’s downdraft. And it is possible that this DeemedMaturity is being ignored for the FloatingResets. And that the market is ignoring the “Strong Pair” relationship between the pairs for banks, but paying attention to it for the TRP issues (or vice versa!).

This doesn’t make any sense; the Strong Pair theory demands only that the prices be equal on the next exchange date; whatever happens afterwards is irrelevant. But this is the preferred share market, which often doesn’t make sense.

It might be that the TRP pair is predicting the actual implied bill rate better than the bank pairs as far as discounted investment grade pairs are concerned, but fortunately BNS.PR.Y is, like the other bank issues, subject to a DeemedMaturity, so it is reasonable to assume that it and its future pair (if issued) will trade like the other banks.

The other exception is DC.PR.B / DC.PR.C. I don’t understand why there is such an enormous price difference. Sorry!