Assiduous Reader Prefhound can always be relied upon for detailed analysis and he has not disappointed in his comment on the February 2 Market Report:

For the Jan 23 FTS series, the lowest reset spread was said to be “cheap”, but its return would only be higher than a higher reset spread if long run GOC-5 rose to an equilibrium around 3%. Current price and reset spreads made sense if the long run equilibrium GOC-5 yield were in the 1-1.5% range (vs 0.85% at the time). Only if the long run equilibrium GOC-5 Yield were 0-0.50% would the original rich/cheap analysis produce substantially different long run returns. This suggested to me that rich/cheap was fairly sensitive to long run GOC-5, so arbitrage returns would depend on changes in (and perception of) that benchmark. As you often note, perception can differ enormously from reality, so fixed reset arbitrage appears to have a substantial element of added GOC-5 risk.

It will be recalled that in my original essay on Implied Volatility for FixedResets I made the point that both the “Pure” price (that is, the price of a non-callable annuity) with any given spread would approach par as GOC-5 increased, while the option value would approach zero; thus, we may conclude that an increase in GOC-5 will cause all issues to move closer to their par value (and contrariwise!) regardless of whether they are at a premium or a discount.

As Prefhound has focussed on the January 23 analysis of the FTS FixedResets, I will show their data for that day to make it easier for Assiduous Readers to replicate and extend the analysis. My findings are at variance with Prefhound‘s conclusions, but I’m sure a bit more methodological detail will sort out a difference in assumptions:

| FTS FixedResets: Characteristics | ||||

| Ticker | Current Dividend |

Issue Reset Spread |

Next Exchange Date |

Bid Price 2015-1-23 |

| FTS.PR.G | 0.9708 | +213 | 2018-9-1 | 24.70 |

| FTS.PR.H | 1.0625 | +145 | 2015-6-1 | 18.28 |

| FTS.PR.K | 1.00 | +205 | 2019-3-1 | 25.15 |

| FTS.PR.M | 1.025 | +248 | 2019-12-1 | 25.58 |

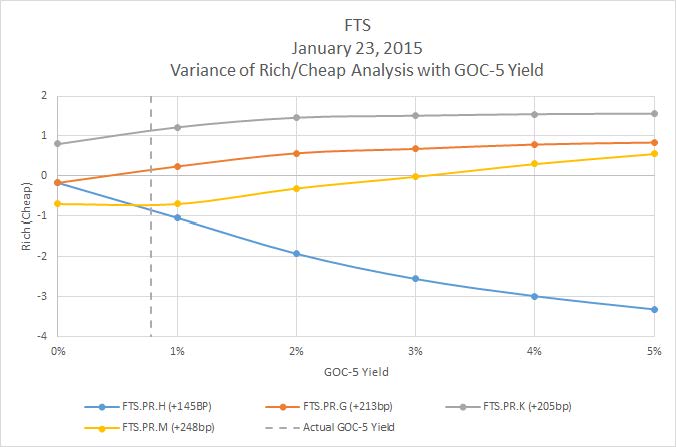

So first we will perform a series of computations using the January 23 bids, but varying GOC-5; we come up with the following table:

| Rich / (Cheap) | ||||||

| GOC5 | ImpVol | Spread | FTS.PR.H | FTS.PR.G | FTS.PR.K | FTS.PR.M |

| 5% | 1% | 247 | -3.31 | 0.84 | 1.56 | 0.55 |

| 4% | 1% | 241 | -2.98 | 0.79 | 1.55 | 0.3 |

| 3% | 3% | 234 | -2.55 | 0.68 | 1.51 | -0.02 |

| 2% | 4% | 227 | -1.92 | 0.57 | 1.46 | -0.31 |

| 1% | 5% | 217 | -1.04 | 0.24 | 1.22 | -0.7 |

| 0% | 11% | 196 | -0.17 | -0.17 | 0.8 | -0.7 |

… which may be graphed as:

Click for Big

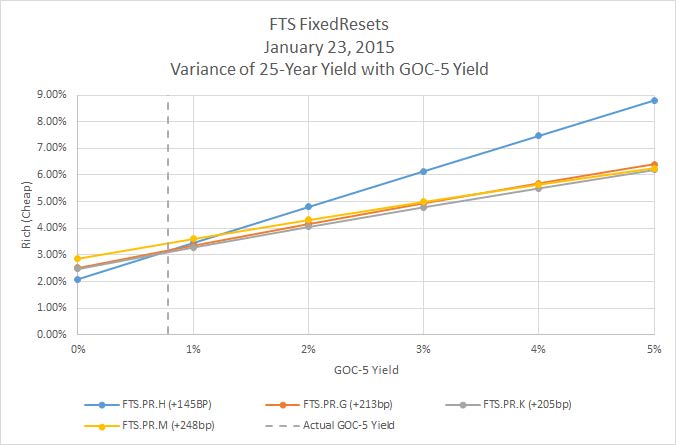

Further, we can use the Yield Calculator for Resets, which was given a thorough explanation in early December to determine the 25-year yield expected for each of the GOC-5 levels – note that no prior call is assumed in any of these calculations and that the end-price is set equal to current price. We derive the following table (nb: incorrect figures from the original post have been struck out and replaced with corrected figures 2015-2-4).

| GOC5 | FTS.PR.H | FTS.PR.G | FTS.PR.K | FTS.PR.M |

| 5% | 8.80% | 6.41% | 6.19% | |

| 4% | 7.47% | 5.69% | 5.50% | |

| 3% | 6.14% | 4.94% | 4.79% | |

| 2% | 4.80% | 4.16% | 4.05% | |

| 1% | 3.45% | 3.35% | 3.28% | |

| 0% | 2.09% | 2.51% | 2.47% |

… and plotted as:

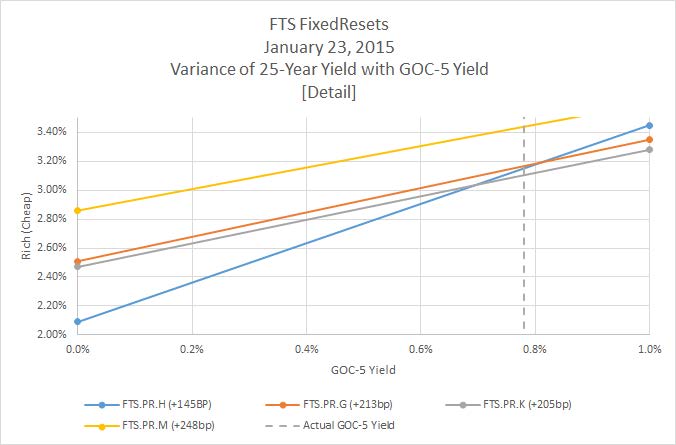

Click for Big

Corrected 2015-2-4

What makes this chart particularly fascinating is that the minimal difference between the four calculated yields is found at a value for GOC-5 that is very close to the actual GOC-5 rate of 0.78% at the close of that day:

Click for Big

Corrected 2015-2-4

This bears investigating … one might almost wonder if there isn’t some market making going on that has the effect of grouping these yields together …

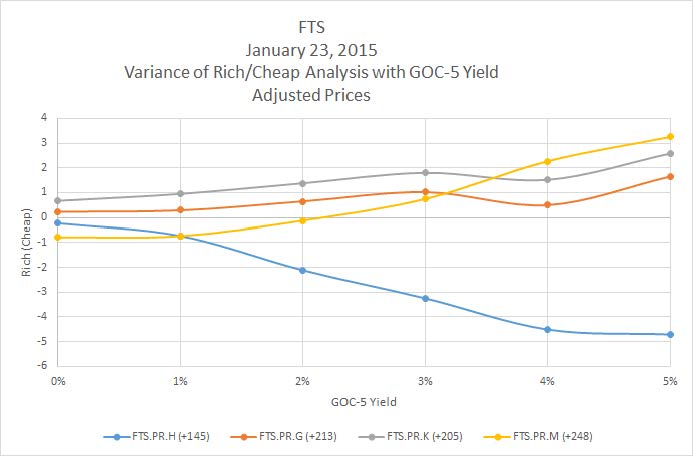

Update, 2015-02-04: Prefhound wants to see the prices for the Implied Volatility fitting adjusted to reflect the period until the next Exchange Date. OK, here goes!

| FTS.PR.H | FTS.PR.G | FTS.PR.K | FTS.PR.M | ||

| Spread | 145 | 213 | 205 | 248 | |

| Exchange Date |

2015-6-1 | 2018-9-1 | 2019-3-1 | 2019-12-1 | |

| Dividends Until Exchange Date |

2 | 15 | 17 | 20 | |

| Current Dividend |

1.0625 | 0.9708 | 1.00 | 1.025 | |

| Future Dividends | |||||

| GOC5 | 5% | 1.6125 | 1.7825 | 1.7625 | 1.87 |

| 4% | 1.3625 | 1.5325 | 1.5125 | 1.62 | |

| 3% | 1.1125 | 1.2825 | 1.2625 | 1.37 | |

| 2% | 0.8625 | 1.0325 | 1.0125 | 1.12 | |

| 1% | 0.6125 | 0.7825 | 0.7625 | 0.87 | |

| 0% | 0.3625 | 0.5325 | 0.5125 | 0.62 | |

| Price Adjustment | |||||

| GOC5 | 5% | -0.35 | -1.64 | -2.07 | -2.03 |

| 4% | 0.15 | 2.11 | 2.18 | 2.98 | |

| 3% | 0.03 | 1.17 | 1.12 | 1.73 | |

| 2% | -0.10 | 0.23 | 0.05 | 0.48% | |

| 1% | -0.23 | -0.71 | -1.01 | -0.78 | |

| 0% | -0.35 | -1.64 | -2.07 | -2.03 | |

| Effective Price | |||||

| GOC5 | 5% | 18.56 | 27.74 | 28.39 | 29.81 |

| 4% | 18.43 | 26.81 | 27.33 | 28.56 | |

| 3% | 18.31 | 25.87 | 26.27 | 27.31 | |

| 2% | 18.18 | 24.93 | 25.20 | 26.06 | |

| 1% | 18.06 | 23.99 | 24.14 | 24.81 | |

| 0% | 17.93 | 23.06 | 23.08 | 23.56 | |

And now we will perform a series of computations using the January 23 bids as adjusted in the above table, using the appropriate GOC-5:

| Rich / (Cheap) | ||||||

| GOC5 | ImpVol | Spread | FTS.PR.H | FTS.PR.G | FTS.PR.K | FTS.PR.M |

| 5% | 1% | 193 | -4.71 | 1.65 | 2.58 | 3.25 |

| 4% | 1% | 194 | -4.51 | 0.50 | 1.52 | 2.27 |

| 3% | 1% | 216 | -3.25 | 1.02 | 1.80 | 0.75 |

| 2% | 3% | 225 | -2.11 | 0.65 | 1.38 | -0.12 |

| 1% | 7% | 226 | -0.73 | 0.29 | 0.95 | -0.74 |

| 0% | 26% | 184 | -0.23 | 0.23 | 0.67 | -0.79 |

This allows the following chart to be drawn:

Click for Big

The price adjustments, of course, are very large, but it doesn’t make any difference to the fitting, which uses only prices. The Expected Future Current Yields are calculated only for display purposes. At any rate, while there are significant differences, the qualitative conclusions are the same – this chart looks pretty much the same as the one with unadjusted prices, although there’s a curious jog in the ‘Adjusted Price’ one.