TransAlta Corporation has announced:

it has completed its public offering (the “Offering”) of 6,600,000 Cumulative Redeemable Rate Reset First Preferred Shares, Series G (the “Series G Shares”) at a price of $25.00 per Series G Share.

The Offering, previously announced on August 6, 2014, includes the partial exercise of the underwriters’ option of an additional 600,000 Series G Shares for proceeds of an additional $15 million bringing the aggregate gross proceeds of the Offering to $165 million. The net proceeds of the Offering will be used for general corporate purposes in support of our business, to reduce short term indebtedness and to fund capital investments of the Corporation and its affiliates.

The Series G Shares were offered to the Canadian public through a syndicate of underwriters led by RBC Capital Markets, CIBC and Scotiabank by way of a prospectus supplement that was filed on August 8, 2014 with securities regulatory authorities in Canada under TransAlta’s short form base shelf prospectus dated December 9, 2013.

Holders of Series G Shares are entitled to receive a cumulative quarterly fixed dividend yielding 5.30% annually for the initial period ending September 30, 2019. Thereafter, the dividend rate will be reset every five years at a rate equal to the 5-year Government of Canada bond yield plus 3.80%. Holders of Series G Shares will have the right, at their option, to convert their Series G shares into Cumulative Redeemable Floating Rate First Preferred Shares, Series H (the “Series H Shares”), subject to certain conditions, on September 30, 2019 and on September 30 every five years thereafter. Holders of Series H Shares will be entitled to receive cumulative quarterly floating dividends at a rate equal to the three-month Government of Canada Treasury Bill yield plus 3.80%. The Series G Shares are listed on the Toronto Stock Exchange under the ticker symbol TA.PR.J.

TA.PR.J is a FixedReset, 5.30%+380, announced August 6. It will be tracked by HIMIPref™ and has been assigned to the Scraps index on credit concerns.

The issue traded 307,925 shares today (consolidated exchanges) in a range of 24.65-84 before closing at 24.72-75, 204×92. Vital statistics are:

| TA.PR.J | FixedReset | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-08-15 Maturity Price : 23.06 Evaluated at bid price : 24.72 Bid-YTW : 5.25 % |

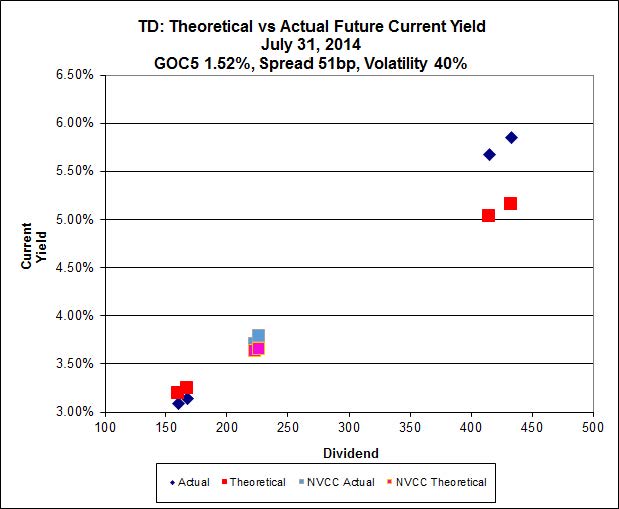

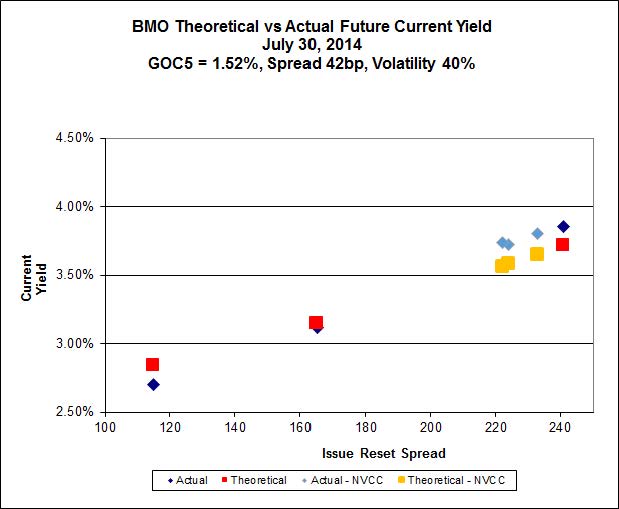

Implied Volatility theory suggests that this issue is about $0.50 expensive, being fairly priced at 24.22 compared to its closing bid of 24.72. TA.PR.F, on the other hand, is about $0.66 cheap, fairly priced at 22.36 compared to its closing bid of 21.70.

Click for Big