Today the markets celebrated hopes of a great big bail-out:

Stocks soared on Tuesday on expectations that Congress was close to producing a stimulus bill to stabilize America’s faltering economy and offer lifelines to industries on the brink of collapse because of the coronavirus.

A plan to bail out companies and send checks of up to $1,200 to Americans had been stalled since Sunday over objections by Democrats. But on Tuesday, top Democrats and Trump administration officials said they were optimistic about finalizing an agreement on a roughly $2 trillion plan.

The S&P 500 had its biggest daily gain since 2008, rising more than 9 percent. Stocks in Europe climbed, led by Germany, where stocks rose more than 10 percent.

… and in Canada …:

Canada’s main stock market rallied on Tuesday, rebounding from an eight-year low the day before, as hopes rose that global stimulus measures will ease the economic impact of the coronavirus pandemic.

The Toronto Stock Exchange’s S&P/TSX composite index surged 11.96%, or 1,342.59 points, to 12,571.08, after hitting its lowest intraday level since October 2011 at 11,172.73 on Monday. Since peaking in February, the index has tumbled about 30%. Tuesday’s percentage gain for the Canadian index was its biggest since July 1979, based on Refinitiv Eikon data.

…

Suncor Energy Inc. cut its 2020 production outlook and suspended share repurchases for the year following the decline in crude oil prices and due to the economic impact of the virus outbreak. Still, its shares rallied 13%.

…

The Canadian dollar was little changed at about 1.45 to the U.S. dollar, or 68.97 U.S. cents. The currency, which last Thursday hit a four-year low at 1.4669, traded in a range of 1.4375 to 1.4532.Canadian government bond yields rose across the curve in sympathy with U.S. Treasuries. The 10-year was up 3.7 basis points at 0.855%.

As mentioned yesterday, the Fed has announced the Primary Market Corporate Credit Facility and the Secondary Market Corporate Support Facility. There are calls for the BoC to do the same:

The mad scramble for cash amid the coronavirus panic is putting enormous strain on the Canadian corporate bond market, which the country’s largest companies rely on for a steady source of financing.

While high-quality credit typically serves as a safe haven in the midst of an economic shock, corporate bonds have plummeted alongside stocks over the past few bewildering weeks.

The iShares Canadian Corporate Bond Index ETF (XCB) – the largest of its kind – fell by a staggering 23 per cent in just 11 trading days, before a market-wide bounce on Tuesday clawed back a portion of the fund’s losses.

…

To help restore order, the Bank of Canada may follow the U.S. Federal Reserve’s lead and intervene in the corporate credit market for the first time in its history.“To draw a line and support investment-grade debt, that’s the kind of bold move that can inspire confidence. That will create some semblance of rationality,” Mr. Mamdani said.

Last week, the Bank of Canada opened that door, giving itself the authority to buy and sell corporate and municipal debt, “for purposes of addressing a situation of financial system stress that could have material macroeconomic consequences,” according to a regulatory notice from March 18.

But in the real world:

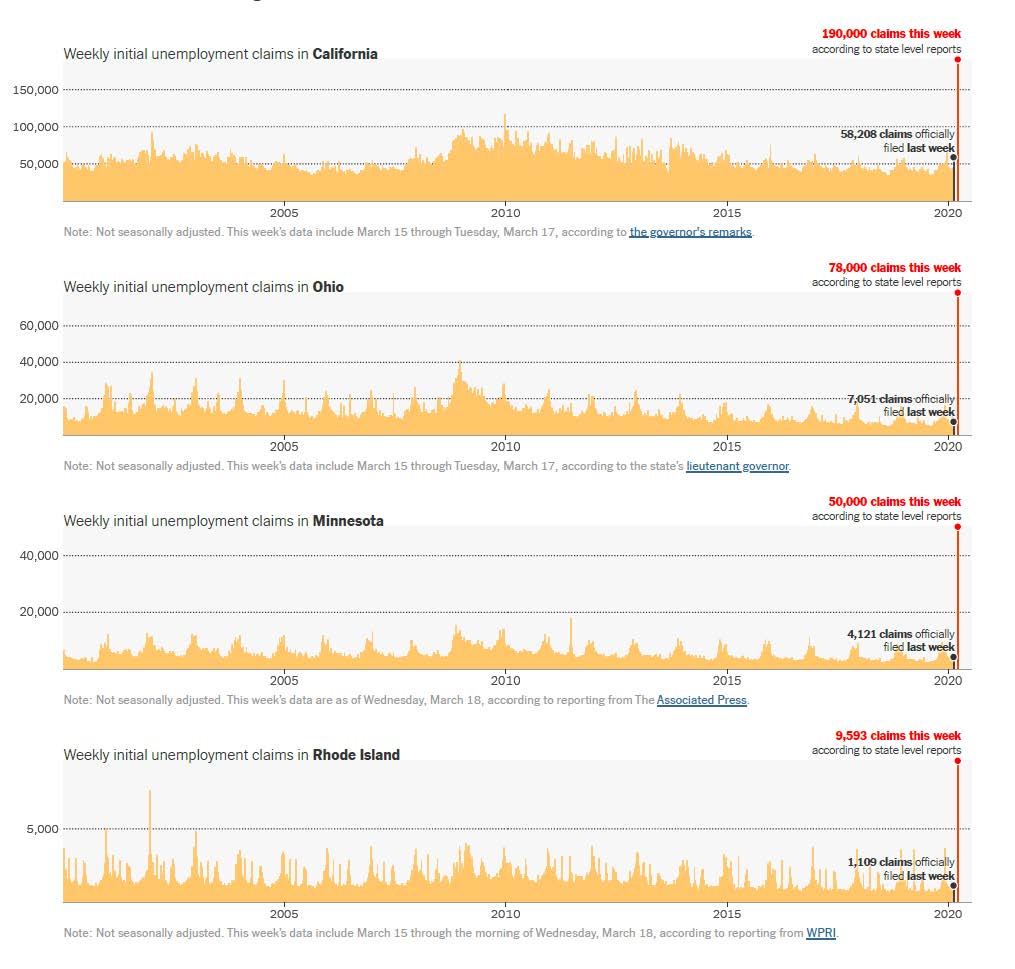

A source familiar with the data confirmed that the government received an estimated 929,000 Employment Insurance claims in the week of March 16-22 – a week in which a dramatic escalation of social-isolation requirements across the country forced many businesses to either sharply curtail their operations or shut down entirely.

Those EI filings represent roughly 5 per cent of all employees in the country – and imply that the national unemployment rate may have nearly doubled in just seven days.

The numbers of layoffs could surge again in the coming days, as the country’s two most populous provinces, Ontario and Quebec, will institute new rules requiring businesses deemed non-essential to close their doors as of midnight Tuesday night.

TXPR closed at 408.38, up 3.996% on the day. Volume today was 4.63-million – and this enormous figure is merely about average of the past two weeks.

CPD closed at 8.10, up 3.18% on the day. Volume of 325,281, above average but nothing special in the context of the past 30 trading days.

ZPR closed at 6.30, up 3.11% on the day. Volume of 500,507 was the lowest since March 6.

Five-year Canada yields were up 5bp to 0.76% today.

I’m not reviewing suspect quotes today, as has been the case for the past while. I’m saving my sarcasm for less turbulent times.

Update, 1:47am: A deal has been reached on the US stimulus package:

The legislation, which is expected to be enacted within days, is the biggest economic stimulus package in modern American history, aimed at delivering critical financial support to businesses forced to shut their doors and relief to American families and hospitals reeling from the rapid spread of the disease and the resulting economic disruption.

Struck shortly before 1 a.m., it was the product of a marathon set of negotiations among Senate Republicans, Democrats and President Trump’s team that nearly fell apart as Democrats insisted upon stronger worker protections and oversight over a new $500 billion fund to bail out distressed businesses.

The deal was struck after a furious final round of haggling between Senator Mitch McConnell, Republican of Kentucky, Steven Mnuchin, the Treasury secretary, and Senator Chuck Schumer, Democrat of New York, after Democrats twice blocked action on the measure as they insisted on concessions.

S&P overnight Futures are down 1.12% as of 1:34am; we’ll see what the next few updates look like!

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2187 % | 1,227.2 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2187 % | 2,251.9 |

| Floater | 8.82 % | 8.92 % | 57,682 | 10.49 | 4 | -0.2187 % | 1,297.8 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 7.4768 % | 2,854.4 |

| SplitShare | 5.81 % | 9.75 % | 78,706 | 3.93 | 7 | 7.4768 % | 3,408.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 7.4768 % | 2,659.7 |

| Perpetual-Premium | 7.63 % | 8.08 % | 105,909 | 11.22 | 12 | 2.6740 % | 2,233.6 |

| Perpetual-Discount | 7.10 % | 7.15 % | 88,006 | 12.35 | 24 | 1.9898 % | 2,466.4 |

| FixedReset Disc | 8.89 % | 7.54 % | 209,786 | 11.48 | 64 | 3.4021 % | 1,355.4 |

| Deemed-Retractible | 7.06 % | 7.96 % | 98,671 | 11.45 | 27 | 3.4948 % | 2,393.8 |

| FloatingReset | 7.17 % | 7.35 % | 64,026 | 12.13 | 3 | 5.6312 % | 1,410.2 |

| FixedReset Prem | 7.20 % | 7.15 % | 194,211 | 12.28 | 22 | 4.7575 % | 1,883.0 |

| FixedReset Bank Non | 2.05 % | 8.14 % | 124,571 | 1.78 | 3 | 1.8638 % | 2,592.2 |

| FixedReset Ins Non | 8.92 % | 7.92 % | 118,838 | 11.16 | 22 | 5.6474 % | 1,321.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PWF.PR.P | FixedReset Disc | -6.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 7.22 Evaluated at bid price : 7.22 Bid-YTW : 7.91 % |

| TD.PF.I | FixedReset Disc | -2.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 12.82 Evaluated at bid price : 12.82 Bid-YTW : 7.58 % |

| EMA.PR.E | Perpetual-Discount | -2.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.10 Evaluated at bid price : 17.10 Bid-YTW : 6.67 % |

| BNS.PR.I | FixedReset Disc | -2.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 13.00 Evaluated at bid price : 13.00 Bid-YTW : 6.92 % |

| BAM.PR.B | Floater | -2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 6.75 Evaluated at bid price : 6.75 Bid-YTW : 9.01 % |

| RY.PR.J | FixedReset Disc | -2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 12.72 Evaluated at bid price : 12.72 Bid-YTW : 6.72 % |

| RY.PR.S | FixedReset Disc | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 13.90 Evaluated at bid price : 13.90 Bid-YTW : 6.29 % |

| POW.PR.B | Perpetual-Discount | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.23 Evaluated at bid price : 17.23 Bid-YTW : 7.97 % |

| PWF.PR.F | Perpetual-Discount | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.58 Evaluated at bid price : 16.58 Bid-YTW : 8.10 % |

| BAM.PF.E | FixedReset Disc | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.06 Evaluated at bid price : 10.06 Bid-YTW : 7.97 % |

| POW.PR.D | Perpetual-Discount | 1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.72 Evaluated at bid price : 16.72 Bid-YTW : 7.67 % |

| MFC.PR.J | FixedReset Ins Non | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.05 Evaluated at bid price : 11.05 Bid-YTW : 8.15 % |

| BIP.PR.D | FixedReset Disc | 1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.03 Evaluated at bid price : 16.03 Bid-YTW : 7.86 % |

| PWF.PR.R | Perpetual-Premium | 1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.41 Evaluated at bid price : 17.41 Bid-YTW : 8.08 % |

| PWF.PR.Z | Perpetual-Discount | 1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.48 Evaluated at bid price : 16.48 Bid-YTW : 7.99 % |

| CIU.PR.A | Perpetual-Discount | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.30 Evaluated at bid price : 16.30 Bid-YTW : 7.15 % |

| POW.PR.G | Perpetual-Premium | 1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.40 Evaluated at bid price : 17.40 Bid-YTW : 8.27 % |

| HSE.PR.C | FixedReset Disc | 1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 6.80 Evaluated at bid price : 6.80 Bid-YTW : 15.78 % |

| CM.PR.Q | FixedReset Disc | 1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.77 Evaluated at bid price : 10.77 Bid-YTW : 8.14 % |

| PWF.PR.T | FixedReset Disc | 1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.72 Evaluated at bid price : 10.72 Bid-YTW : 7.97 % |

| RY.PR.C | Deemed-Retractible | 1.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.31 Bid-YTW : 11.49 % |

| ELF.PR.H | Perpetual-Premium | 1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 19.35 Evaluated at bid price : 19.35 Bid-YTW : 7.28 % |

| CU.PR.F | Perpetual-Discount | 1.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.30 Evaluated at bid price : 16.30 Bid-YTW : 7.00 % |

| GWO.PR.G | Deemed-Retractible | 1.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.08 Evaluated at bid price : 16.08 Bid-YTW : 8.15 % |

| MFC.PR.B | Deemed-Retractible | 1.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 15.39 Evaluated at bid price : 15.39 Bid-YTW : 7.63 % |

| BNS.PR.G | FixedReset Prem | 1.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 7.02 % |

| EMA.PR.C | FixedReset Disc | 2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 12.25 Evaluated at bid price : 12.25 Bid-YTW : 7.54 % |

| MFC.PR.C | Deemed-Retractible | 2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 14.28 Evaluated at bid price : 14.28 Bid-YTW : 7.96 % |

| TD.PF.C | FixedReset Disc | 2.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.63 Evaluated at bid price : 11.63 Bid-YTW : 7.05 % |

| RY.PR.P | Perpetual-Premium | 2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 20.51 Evaluated at bid price : 20.51 Bid-YTW : 6.49 % |

| PWF.PR.S | Perpetual-Discount | 2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 15.39 Evaluated at bid price : 15.39 Bid-YTW : 7.97 % |

| ELF.PR.G | Perpetual-Discount | 2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.75 Evaluated at bid price : 16.75 Bid-YTW : 7.26 % |

| BNS.PR.H | FixedReset Prem | 2.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.16 Evaluated at bid price : 17.16 Bid-YTW : 7.18 % |

| MFC.PR.O | FixedReset Ins Non | 2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.46 Evaluated at bid price : 17.46 Bid-YTW : 8.11 % |

| PWF.PR.A | Floater | 2.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 7.10 Evaluated at bid price : 7.10 Bid-YTW : 8.67 % |

| RY.PR.F | Deemed-Retractible | 2.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.22 Bid-YTW : 11.56 % |

| GWO.PR.F | Deemed-Retractible | 2.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 18.76 Evaluated at bid price : 18.76 Bid-YTW : 7.93 % |

| NA.PR.G | FixedReset Disc | 2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 12.27 Evaluated at bid price : 12.27 Bid-YTW : 7.91 % |

| RY.PR.A | Deemed-Retractible | 2.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.29 Bid-YTW : 11.37 % |

| PWF.PR.E | Perpetual-Premium | 2.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.40 Evaluated at bid price : 17.40 Bid-YTW : 8.08 % |

| CM.PR.S | FixedReset Disc | 2.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.51 Evaluated at bid price : 11.51 Bid-YTW : 7.54 % |

| TD.PF.H | FixedReset Prem | 2.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 7.15 % |

| BAM.PF.C | Perpetual-Discount | 2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.44 Evaluated at bid price : 16.44 Bid-YTW : 7.43 % |

| CU.PR.E | Perpetual-Discount | 2.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.65 Evaluated at bid price : 17.65 Bid-YTW : 7.04 % |

| MFC.PR.R | FixedReset Ins Non | 2.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 13.80 Evaluated at bid price : 13.80 Bid-YTW : 8.27 % |

| CU.PR.G | Perpetual-Discount | 2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.42 Evaluated at bid price : 16.42 Bid-YTW : 6.94 % |

| BMO.PR.S | FixedReset Disc | 2.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.78 Evaluated at bid price : 10.78 Bid-YTW : 7.58 % |

| GWO.PR.H | Deemed-Retractible | 2.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.07 Evaluated at bid price : 16.07 Bid-YTW : 7.60 % |

| POW.PR.A | Perpetual-Premium | 2.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.75 Evaluated at bid price : 17.75 Bid-YTW : 8.10 % |

| TD.PF.G | FixedReset Prem | 2.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 18.85 Evaluated at bid price : 18.85 Bid-YTW : 7.18 % |

| PVS.PR.D | SplitShare | 2.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 22.61 Bid-YTW : 11.66 % |

| BAM.PF.A | FixedReset Disc | 2.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 12.00 Evaluated at bid price : 12.00 Bid-YTW : 8.24 % |

| RY.PR.Q | FixedReset Prem | 2.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 18.65 Evaluated at bid price : 18.65 Bid-YTW : 7.06 % |

| PWF.PR.H | Perpetual-Premium | 2.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.78 Evaluated at bid price : 17.78 Bid-YTW : 8.27 % |

| TD.PF.K | FixedReset Disc | 2.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 12.75 Evaluated at bid price : 12.75 Bid-YTW : 7.21 % |

| CCS.PR.C | Deemed-Retractible | 2.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 6.99 % |

| CM.PR.P | FixedReset Disc | 2.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.65 Evaluated at bid price : 10.65 Bid-YTW : 7.77 % |

| SLF.PR.B | Deemed-Retractible | 2.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.21 Evaluated at bid price : 16.21 Bid-YTW : 7.46 % |

| GWO.PR.S | Deemed-Retractible | 2.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.37 Evaluated at bid price : 16.37 Bid-YTW : 8.08 % |

| RY.PR.E | Deemed-Retractible | 3.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.30 Bid-YTW : 11.40 % |

| MFC.PR.H | FixedReset Ins Non | 3.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.51 Evaluated at bid price : 11.51 Bid-YTW : 8.44 % |

| GWO.PR.I | Deemed-Retractible | 3.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 14.26 Evaluated at bid price : 14.26 Bid-YTW : 7.95 % |

| BMO.PR.T | FixedReset Disc | 3.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.54 Evaluated at bid price : 10.54 Bid-YTW : 7.46 % |

| SLF.PR.I | FixedReset Ins Non | 3.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.70 Evaluated at bid price : 10.70 Bid-YTW : 8.05 % |

| GWO.PR.L | Deemed-Retractible | 3.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.34 Evaluated at bid price : 17.34 Bid-YTW : 8.21 % |

| RY.PR.G | Deemed-Retractible | 3.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.30 Bid-YTW : 11.40 % |

| PWF.PR.K | Perpetual-Discount | 3.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.16 Evaluated at bid price : 16.16 Bid-YTW : 7.83 % |

| MFC.PR.F | FixedReset Ins Non | 3.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 7.26 Evaluated at bid price : 7.26 Bid-YTW : 7.13 % |

| TD.PF.B | FixedReset Disc | 3.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.31 Evaluated at bid price : 11.31 Bid-YTW : 7.06 % |

| IAF.PR.B | Deemed-Retractible | 3.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 15.51 Evaluated at bid price : 15.51 Bid-YTW : 7.47 % |

| BAM.PR.R | FixedReset Disc | 3.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 8.68 Evaluated at bid price : 8.68 Bid-YTW : 8.53 % |

| SLF.PR.C | Deemed-Retractible | 3.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 14.73 Evaluated at bid price : 14.73 Bid-YTW : 7.61 % |

| NA.PR.A | FixedReset Prem | 3.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.06 Evaluated at bid price : 17.06 Bid-YTW : 7.92 % |

| IFC.PR.G | FixedReset Ins Non | 3.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.75 Evaluated at bid price : 11.75 Bid-YTW : 7.66 % |

| NA.PR.S | FixedReset Disc | 3.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.71 Evaluated at bid price : 10.71 Bid-YTW : 7.91 % |

| PVS.PR.F | SplitShare | 3.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2024-09-30 Maturity Price : 25.00 Evaluated at bid price : 20.71 Bid-YTW : 9.69 % |

| PWF.PR.O | Perpetual-Premium | 3.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 8.24 % |

| RY.PR.H | FixedReset Disc | 3.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.50 Evaluated at bid price : 11.50 Bid-YTW : 6.86 % |

| BAM.PF.D | Perpetual-Discount | 3.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.70 Evaluated at bid price : 16.70 Bid-YTW : 7.39 % |

| PWF.PR.L | Perpetual-Discount | 3.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.40 Evaluated at bid price : 16.40 Bid-YTW : 7.95 % |

| TD.PF.E | FixedReset Disc | 3.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 12.50 Evaluated at bid price : 12.50 Bid-YTW : 7.16 % |

| TD.PF.M | FixedReset Disc | 3.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.08 Evaluated at bid price : 16.08 Bid-YTW : 7.07 % |

| NA.PR.E | FixedReset Disc | 3.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.62 Evaluated at bid price : 11.62 Bid-YTW : 7.73 % |

| BMO.PR.W | FixedReset Disc | 3.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.00 Evaluated at bid price : 11.00 Bid-YTW : 7.30 % |

| BNS.PR.E | FixedReset Prem | 3.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 18.40 Evaluated at bid price : 18.40 Bid-YTW : 7.17 % |

| BAM.PR.N | Perpetual-Discount | 3.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.20 Evaluated at bid price : 16.20 Bid-YTW : 7.38 % |

| BAM.PR.M | Perpetual-Discount | 3.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.35 Evaluated at bid price : 16.35 Bid-YTW : 7.32 % |

| RY.PR.N | Perpetual-Discount | 3.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 6.61 % |

| POW.PR.C | Perpetual-Premium | 3.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.92 Evaluated at bid price : 17.92 Bid-YTW : 8.31 % |

| MFC.PR.M | FixedReset Ins Non | 3.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.65 Evaluated at bid price : 10.65 Bid-YTW : 7.71 % |

| TD.PF.J | FixedReset Disc | 3.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 13.10 Evaluated at bid price : 13.10 Bid-YTW : 7.06 % |

| GWO.PR.P | Deemed-Retractible | 4.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.81 Evaluated at bid price : 16.81 Bid-YTW : 8.10 % |

| BIP.PR.C | FixedReset Prem | 4.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.35 Evaluated at bid price : 16.35 Bid-YTW : 8.25 % |

| IFC.PR.I | Perpetual-Premium | 4.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 7.32 % |

| SLF.PR.E | Deemed-Retractible | 4.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 14.96 Evaluated at bid price : 14.96 Bid-YTW : 7.58 % |

| W.PR.K | FixedReset Prem | 4.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.31 Evaluated at bid price : 17.31 Bid-YTW : 7.78 % |

| MFC.PR.I | FixedReset Ins Non | 4.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.11 Evaluated at bid price : 11.11 Bid-YTW : 8.30 % |

| NA.PR.X | FixedReset Prem | 4.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 7.83 % |

| PWF.PR.Q | FloatingReset | 4.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 7.04 Evaluated at bid price : 7.04 Bid-YTW : 7.65 % |

| CM.PR.Y | FixedReset Disc | 4.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 15.75 Evaluated at bid price : 15.75 Bid-YTW : 7.35 % |

| SLF.PR.A | Deemed-Retractible | 4.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.07 Evaluated at bid price : 16.07 Bid-YTW : 7.44 % |

| BAM.PF.B | FixedReset Disc | 4.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.00 Evaluated at bid price : 11.00 Bid-YTW : 8.25 % |

| BIP.PR.F | FixedReset Disc | 4.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 8.03 % |

| IAF.PR.G | FixedReset Ins Non | 4.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.22 Evaluated at bid price : 11.22 Bid-YTW : 7.92 % |

| BIP.PR.E | FixedReset Disc | 4.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.25 Evaluated at bid price : 16.25 Bid-YTW : 7.75 % |

| SLF.PR.J | FloatingReset | 4.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 7.16 Evaluated at bid price : 7.16 Bid-YTW : 6.73 % |

| CM.PR.O | FixedReset Disc | 4.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.58 Evaluated at bid price : 10.58 Bid-YTW : 7.72 % |

| HSE.PR.E | FixedReset Disc | 4.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 7.44 Evaluated at bid price : 7.44 Bid-YTW : 14.32 % |

| BAM.PR.Z | FixedReset Disc | 4.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.80 Evaluated at bid price : 11.80 Bid-YTW : 8.14 % |

| BAM.PR.T | FixedReset Disc | 4.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 9.06 Evaluated at bid price : 9.06 Bid-YTW : 8.40 % |

| CU.PR.C | FixedReset Disc | 5.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 12.60 Evaluated at bid price : 12.60 Bid-YTW : 6.19 % |

| GWO.PR.M | Deemed-Retractible | 5.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.99 Evaluated at bid price : 17.99 Bid-YTW : 8.13 % |

| SLF.PR.D | Deemed-Retractible | 5.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 14.81 Evaluated at bid price : 14.81 Bid-YTW : 7.57 % |

| CU.PR.I | FixedReset Prem | 5.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.94 Evaluated at bid price : 17.94 Bid-YTW : 6.35 % |

| PWF.PR.G | Perpetual-Premium | 5.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 18.60 Evaluated at bid price : 18.60 Bid-YTW : 8.11 % |

| PVS.PR.E | SplitShare | 5.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-10-31 Maturity Price : 25.00 Evaluated at bid price : 22.16 Bid-YTW : 10.80 % |

| W.PR.M | FixedReset Prem | 5.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.75 Evaluated at bid price : 17.75 Bid-YTW : 7.51 % |

| CM.PR.R | FixedReset Disc | 5.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 13.09 Evaluated at bid price : 13.09 Bid-YTW : 7.98 % |

| GWO.PR.Q | Deemed-Retractible | 5.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.10 Evaluated at bid price : 16.10 Bid-YTW : 8.06 % |

| BIP.PR.B | FixedReset Prem | 5.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.90 Evaluated at bid price : 16.90 Bid-YTW : 8.20 % |

| IFC.PR.F | Deemed-Retractible | 5.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 7.42 % |

| BAM.PF.I | FixedReset Prem | 5.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.92 Evaluated at bid price : 17.92 Bid-YTW : 6.74 % |

| EIT.PR.A | SplitShare | 5.74 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2024-03-14 Maturity Price : 25.00 Evaluated at bid price : 20.25 Bid-YTW : 10.92 % |

| BAM.PF.H | FixedReset Prem | 5.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 19.05 Evaluated at bid price : 19.05 Bid-YTW : 6.60 % |

| BMO.PR.Q | FixedReset Bank Non | 5.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 9.07 % |

| BAM.PR.X | FixedReset Disc | 5.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 7.62 Evaluated at bid price : 7.62 Bid-YTW : 8.20 % |

| RY.PR.Z | FixedReset Disc | 6.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.56 Evaluated at bid price : 11.56 Bid-YTW : 6.74 % |

| TRP.PR.B | FixedReset Disc | 6.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 7.51 Evaluated at bid price : 7.51 Bid-YTW : 6.40 % |

| NA.PR.W | FixedReset Disc | 6.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.61 Evaluated at bid price : 10.61 Bid-YTW : 7.69 % |

| TRP.PR.C | FixedReset Disc | 6.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 7.45 Evaluated at bid price : 7.45 Bid-YTW : 7.46 % |

| EML.PR.A | FixedReset Ins Non | 6.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.05 Evaluated at bid price : 17.05 Bid-YTW : 8.29 % |

| EIT.PR.B | SplitShare | 6.84 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2025-03-14 Maturity Price : 25.00 Evaluated at bid price : 20.30 Bid-YTW : 9.75 % |

| MFC.PR.K | FixedReset Ins Non | 6.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.70 Evaluated at bid price : 10.70 Bid-YTW : 7.62 % |

| RY.PR.R | FixedReset Prem | 6.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 6.90 % |

| CU.PR.H | Perpetual-Discount | 7.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 6.93 % |

| EMA.PR.H | FixedReset Prem | 7.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 20.61 Evaluated at bid price : 20.61 Bid-YTW : 6.03 % |

| TD.PF.L | FixedReset Disc | 7.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 14.90 Evaluated at bid price : 14.90 Bid-YTW : 7.31 % |

| GWO.PR.R | Deemed-Retractible | 7.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 15.81 Evaluated at bid price : 15.81 Bid-YTW : 7.65 % |

| BAM.PF.J | FixedReset Prem | 7.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.71 Evaluated at bid price : 17.71 Bid-YTW : 6.75 % |

| TRP.PR.E | FixedReset Disc | 7.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.64 Evaluated at bid price : 10.64 Bid-YTW : 7.77 % |

| BIK.PR.A | FixedReset Prem | 7.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.82 Evaluated at bid price : 16.82 Bid-YTW : 8.77 % |

| MFC.PR.G | FixedReset Ins Non | 7.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.91 Evaluated at bid price : 10.91 Bid-YTW : 8.29 % |

| TRP.PR.F | FloatingReset | 7.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 8.31 Evaluated at bid price : 8.31 Bid-YTW : 7.35 % |

| IFC.PR.C | FixedReset Ins Non | 7.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.68 Evaluated at bid price : 10.68 Bid-YTW : 7.77 % |

| NA.PR.C | FixedReset Disc | 7.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 13.50 Evaluated at bid price : 13.50 Bid-YTW : 7.80 % |

| TRP.PR.J | FixedReset Prem | 7.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 20.40 Evaluated at bid price : 20.40 Bid-YTW : 6.84 % |

| TRP.PR.K | FixedReset Prem | 8.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.74 Evaluated at bid price : 17.74 Bid-YTW : 7.00 % |

| TD.PF.A | FixedReset Disc | 8.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.50 Evaluated at bid price : 11.50 Bid-YTW : 6.90 % |

| SLF.PR.H | FixedReset Ins Non | 8.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 9.23 Evaluated at bid price : 9.23 Bid-YTW : 7.65 % |

| MFC.PR.N | FixedReset Ins Non | 8.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.00 Evaluated at bid price : 10.00 Bid-YTW : 7.40 % |

| HSE.PR.A | FixedReset Disc | 8.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 4.77 Evaluated at bid price : 4.77 Bid-YTW : 12.55 % |

| CM.PR.T | FixedReset Disc | 8.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 15.18 Evaluated at bid price : 15.18 Bid-YTW : 7.22 % |

| TRP.PR.G | FixedReset Disc | 9.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 12.26 Evaluated at bid price : 12.26 Bid-YTW : 7.46 % |

| IFC.PR.E | Deemed-Retractible | 9.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 7.48 % |

| MFC.PR.Q | FixedReset Ins Non | 10.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.00 Evaluated at bid price : 11.00 Bid-YTW : 8.13 % |

| TRP.PR.D | FixedReset Disc | 10.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.38 Evaluated at bid price : 11.38 Bid-YTW : 7.32 % |

| IFC.PR.A | FixedReset Ins Non | 11.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 8.93 Evaluated at bid price : 8.93 Bid-YTW : 7.17 % |

| MFC.PR.L | FixedReset Ins Non | 11.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 10.16 Evaluated at bid price : 10.16 Bid-YTW : 7.66 % |

| SLF.PR.G | FixedReset Ins Non | 13.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 7.24 Evaluated at bid price : 7.24 Bid-YTW : 7.10 % |

| GWO.PR.N | FixedReset Ins Non | 13.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 8.61 Evaluated at bid price : 8.61 Bid-YTW : 5.66 % |

| BIP.PR.A | FixedReset Disc | 14.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 12.00 Evaluated at bid price : 12.00 Bid-YTW : 8.81 % |

| TRP.PR.A | FixedReset Disc | 15.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 9.64 Evaluated at bid price : 9.64 Bid-YTW : 7.43 % |

| PVS.PR.G | SplitShare | 35.41 % | YTW SCENARIO Maturity Type : Option Certainty Maturity Date : 2026-02-28 Maturity Price : 25.00 Evaluated at bid price : 20.65 Bid-YTW : 8.83 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| SLF.PR.B | Deemed-Retractible | 527,750 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 16.21 Evaluated at bid price : 16.21 Bid-YTW : 7.46 % |

| TD.PF.A | FixedReset Disc | 431,800 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 11.50 Evaluated at bid price : 11.50 Bid-YTW : 6.90 % |

| TD.PF.H | FixedReset Prem | 169,358 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 7.15 % |

| TD.PF.K | FixedReset Disc | 54,905 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 12.75 Evaluated at bid price : 12.75 Bid-YTW : 7.21 % |

| MFC.PR.O | FixedReset Ins Non | 45,900 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 17.46 Evaluated at bid price : 17.46 Bid-YTW : 8.11 % |

| TRP.PR.J | FixedReset Prem | 36,300 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-24 Maturity Price : 20.40 Evaluated at bid price : 20.40 Bid-YTW : 6.84 % |

| There were 93 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.I | FixedReset Ins Non | Quote: 11.11 – 19.90 Spot Rate : 8.7900 Average : 5.0421 YTW SCENARIO |

| PWF.PR.T | FixedReset Disc | Quote: 10.72 – 17.75 Spot Rate : 7.0300 Average : 4.0528 YTW SCENARIO |

| NA.PR.A | FixedReset Prem | Quote: 17.06 – 23.90 Spot Rate : 6.8400 Average : 3.9887 YTW SCENARIO |

| MFC.PR.G | FixedReset Ins Non | Quote: 10.91 – 18.18 Spot Rate : 7.2700 Average : 4.5998 YTW SCENARIO |

| MFC.PR.N | FixedReset Ins Non | Quote: 10.00 – 15.88 Spot Rate : 5.8800 Average : 3.3816 YTW SCENARIO |

| CM.PR.Q | FixedReset Disc | Quote: 10.77 – 15.00 Spot Rate : 4.2300 Average : 2.5856 YTW SCENARIO |