The low dollar is attracting some notice:

On Tuesday, the Canadian dollar, commonly known as the loonie, broke below 70 U.S. cents for the first time since May 1, 2003.

For America’s northern neighbor, which imports about 80 percent of the fresh fruits and vegetables its citizens consume, this entails a sharp rise in prices for these goods. With lower-income households tending to spend a larger portion of income on food, this side effect of a soft currency brings them the most acute stress.

…

From coast-to-coast-to-coast, Canadians have taken to social media to express displeasure with soaring produce prices:

Bombardier is desperately reinventing its business model:

Bombardier Inc. scrapped $1.75 billion of business-aircraft orders, saying it anticipates making more money by reselling them directly to customers.

The Canadian planemaker also said it was ending a four-decade relationship with distributor TAG Aeronautics as part of a change in its sales strategy. Bombardier will book a $278 million pretax charge in the fourth quarter due to its moves to cut out the middleman standing between itself and aircraft buyers.

Bombardier is revamping its business-jet sales effort as the company’s finances have been strained by its $5.4 billion program for C Series commercial planes. The development of its largest-ever model is more than two years late and at least $2 billion over budget, and Bombardier has been seeking more government aid to right itself.

If it doesn’t work, they can always get another government cheque!

I’m not sure whether it’s a genuine attempt to track down laundered money or the misuse of government powers to follow a populist agenda, but I am sure we’ll hear calls for this in Canada!

Concerned about illicit money flowing into luxury real estate, the Treasury Department said Wednesday that it would begin identifying and tracking secret buyers of high-end properties.

The initiative will start in two of the nation’s major destinations for global wealth: Manhattan and Miami-Dade County. It will shine a light on the darkest corner of the real estate market: all-cash purchases made by shell companies that often shield purchasers’ identities.

It is the first time the federal government has required real estate companies to disclose names behind all-cash transactions, and it is likely to send shudders through the real estate industry, which has benefited enormously in recent years from a building boom increasingly dependent on wealthy, secretive buyers.

The initiative is part of a broader federal effort to increase the focus on money laundering in real estate. Treasury and federal law enforcement officials said they were putting greater resources into investigating luxury real estate sales that involve shell companies like limited liability companies, often known as L.L.C.s; partnerships; and other entities.

There will be ceaseless debate over the next twelve months regarding the advisability of Fed hikes … Larry Summers has fired the opening volley:

Policy makers need to heed the message from global commodity and stock markets that “risks are substantially tilted to the downside,” former U.S. Treasury Secretary Lawrence Summers said Wednesday.

Given the weakness in prices and growth, it’ll be hard for the world to take in stride four interest-rate increases that forecasters are penciling in from the Federal Reserve this year, Summers said in a Bloomberg TV interview.

“I would be surprised if the world economy could comfortably withstand four hikes, and I think that basically the markets agree with me,” he said, adding that’s why it’s important to prepare for a range of possibilities. “Really, what policy makers need to think about is, it is insurance against the more negative scenarios.”

It was another crummy day for equities:

U.S. stocks tumbled, with the Dow Jones Industrial Average plunging more than 370 points and small caps entering a bear market, as oil’s failure to maintain a 4 percent rally rekindled a flight from risk assets. Treasuries surged amid signs that demand for the relative safety of bonds is rising.

The Standard & Poor’s 500 Index fell past 1,900, a level it’s closed below only five times in the past 14 months. The Nasdaq 100 Index had its worst day since Aug. 24, as selling was heaviest in technology and consumer shares. The Russell 2000 Index capped a 22 percent slide from its June record. Brent crude dipped below $30 for the first time since 2004. The yield on the 10-year Treasury note fell to 2.04 percent, after an auction of $21 billion of 10-year notes was deemed ‘outstanding.’ Gold traded above $1,090 an ounce.

…

Treasuries rallied after investors flocked to a $21 billion auction of 10-year notes at the lowest yields since October amid concern that global growth is slowing. A class of investors that includes foreign central banks and mutual funds bought 71 percent of the sale, the second-highest amount on record.

Meanwhile, at time of writing, Chinese equities have bounced back a little … but nobody knows how much of that is manipulation:

The Shanghai Composite Index gained 2 percent to 3,007.65 at the close, reversing a loss of as much as 2.8 percent and sending a gauge of volatility to the highest levels since September. The ChiNext small-caps index surged the most in two months after 28 listed companies vowed to take action to stabilize the market, with some pledging not to sell shares over the next six months. State funds may have entered to buy stocks after the Shanghai index fell below the lowest levels reached in last year’s rout, according to Galaxy Securities Co.

…

The Shanghai gauge earlier dropped below the low of 2,927.29 set in August, when a summer rout wiped out $5 trillion and spurred the government to impose emergency rescue measures. The index, the worst performer among 93 global benchmark measures tracked by Bloomberg this year, fell as much as 20 percent from the December high before paring losses.

The question of trailer fees and the regulatory banishment thereof has been discussed many times on PrefBlog – a CSA request for comment was mentioned on December 13, 2012, for instance, which was clarified on December 18, 2012, with more discussion December 27, 2012. Assiduous Readers with good memories will remember that I have argued that the only problem with the Platonic ideals espoused by regulatory dreamers is that they won’t work in the real world (much like the regulatory dreamers themselves): Joe Lunchbucket does not want to pay a fee to his advisor unless the advisor trades a lot; this goes double if he’s just lost money in the market. So instead of buying an equity mutual fund like he should, he’ll go down to the bank and put his money into a GIC and every step in the process will be approved by the bank’s compliance department, stuffed to the gills with ex-regulators on fat salaries.

I was only one of many holding this view:

From now on, financial advisers will have to charge upfront fees to their customers rather than receive commission from companies supplying financial products. The move by the Financial Services Authority under its retail distribution review (RDR) includes pensions, Isas and unit trusts, and is designed to be more transparent and to reduce the risk of mis-selling.

It means that consumers will see clearly the cost of financial advice which may previously have appeared to be free since the charges were part of the commission payments made to the adviser. But some analysts believe that spelling out the costs, even though these can be spread over a number of years, could put many customers off seeking advice.

A recent survey by Rostrum Research found that nine out of 10 consumers would only pay up to £25 for an hour’s financial advice, compared with the mooted £50-£250 an hour fee range expected in the review.

I have been criticized for this view, but it appears that two years after banning producer payments to intermediaries, it is becoming clear that Joe Lunchbucket does not want to pay for advice:

An influential panel of experts appointed by the Government as part of the Financial Advice Market Review is considering radical reforms to regulation which would roll back key aspects of the RDR to boost access to advice, Money Marketing understands.

The FAMR, jointly led by the Treasury and the FCA, is assessing barriers to the provision of financial advice following the pensions overhaul introduced last April. In particular, the review is looking to tackle the advice gap for people with smaller pots to invest.

…

Sources close to the panel say a number of radical ideas have been seriously discussed during the three sessions held in the second half of last year. These include creating a new basic tier of advice with a lower qualification requirement for simple accumulation products, developing a new charging structure similar to commission and banning regulated advisers from selling unregulated products.

…A separate source says allowing firms to receive commission on simple accumulation product sales is also under consideration.

The source says: “The panel have discussed putting forward an alternative commercial model for advice that would allow a fee to be built into the product. So today you might pay 1 per cent and it is normally paid by selling units in funds but it has to be agreed as part of your service agreement with the adviser. What is being discussed is more like commission.

“So you could invest in an Isa or a pension and the adviser receives a fee on completion of the transaction direct from the provider.”

Panel members have also discussed the possibility of banning regulated advisers from selling unregulated products.

No agreement has been reached on taking these proposals to the Government.

However, the very fact they are being discussed suggests the FAMR could fundamentally redraw the advice landscape yet again.

Shaw Communications, proud issuer of SJR.PR.A, will finance the acquisition of Wind Mobile by selling media assets to the related Corus Entertainment:

Corus Entertainment Inc. has agreed to pay $2.65-billion to acquire Shaw Media Inc. from Shaw Communications Inc., bulking up to compete in a shifting television landscape.

The price will be paid through a combination of $1.85-billion in cash and 71 million Corus class B shares at $11.21 per share. Both companies are ultimately controlled by the Shaw family of Alberta, but are separately listed on the Toronto Stock Exchange.

…

It also removes any doubt about how Shaw will pay for its $1.6-billion acquisition of Wind Mobile Corp., which it announced in December. There had been some speculation that it could sell its U.S. data centre business ViaWest or issue equity.Instead, Shaw made it clear it intends to use the cash from the sale of Shaw Media to fund the Wind purchase.

Shaw expects its acquisition of Wind to close in the third quarter of its fiscal year, which is the three-month period ending May 31, and said Wednesday if that transaction closes earlier, it will rely on bridge financing to fund the deal.

Following the divestiture, DBRS notes that the loss of Shaw Media’s operating income and substantial cash generating capacity, in conjunction with the inclusion of the negative free cash flow wireless and existing business infrastructure services segments, will result in free cash flow (after cash dividend payments) turning negative until F2018. This signals a meaningful, albeit temporary, loss in financial flexibility and places greater reliance on growth in operating income to achieve stated financial leverage targets.

In its review, DBRS will focus on (1) assessing the business risk profile of the new entity, including organic growth prospects in the remaining segments and risks associated with integration of WIND; (2) the Company’s longer-term business strategy; (3) financial management intentions of the new entity going forward and its free cash flow trajectory profile; and (4) the Company’s liquidity profile over the near to medium term.

The proposed asset sale and the WIND acquisition are proceeding through customary regulatory, concurrently, and are both expected to close by Q3 F2016. As previously announced, the Company has secured a $1.7 billion bridge facility, which would allow it to complete the WIND acquisition in the event of a delay in completing the proposed divestiture. The Company would then repay the bridge upon receipt of proceeds from the Shaw Media divestiture.

The previously instated Under Review with Negative Implications rating action will be resolved once DBRS becomes confident that the proposed transaction will close under the current terms, at which point DBRS will likely downgrade Shaw’s ratings by one notch, to the BBB (low) rating category.

This follows prior news that SJR: Credit Agencies Nervous About Wind Acquisition.

GMP, proud issuer of GMP.PR.B, has swallowed hard and acknowledged hard times:

GMP Capital Inc.’s radical restructuring, which involves shutting down its United Kingdom and Australian operations as well as eliminating its dividend, is also hitting senior staff at home.

In total, seventy-three jobs are being axed in a new round of cuts announced Wednesday, affecting investment bankers, research analysts and employees in sales and trading. Twenty-nine positions are being eliminated in Canada, 22 in the U.K., 12 in Australia and 10 in the U.S. GMP said 97 positions – a quarter of its work force – have now been eliminated since the end of the third quarter.

…

GMP has lost money in three of the past four quarters. In the third quarter of 2015, revenue from the company’s energy sector investment banking cratered 87 per cent from a year ago.The brokerage was founded in 1995 and went public in December, 2003. GMP was immensely profitable during the great bull run in resources and some of its proprietary traders, such as Michael Wekerle, were among the best paid people on Bay Street. In mid-2006, GMP’s share price peaked at $28. It closed Tuesday at $3.92 – not far from an all-time low.

I have not seen any reaction from the Credit Rating Agencies yet.

I came across the following on the Internet … I think it might be a book about Canadian preferred shares …

Click for Big

It was another horrible day for the Canadian preferred share market, with PerpetualDiscounts down 44bp, FixedResets losing 133bp and DeemedRetractibles off 29bp. The Performance Highlights table is as lengthy as one might expect, but on the bright side there were a few winners today! Volume was well below average.

It was a big day for DC.PR.C, which Assiduous Readers will remember is the target of an abusive Exchange Offer via a Plan of Arrangement which has been the subject of widespread interest. The issue traded 732,460 shares today in a range of 16.70-00, including a monster-block of 555,600, crossed by GMP shortly before the close at 17.00. When one considers that there are only 6-million shares out, one gets even more impressed! The stock was up sharply on the day. If we assume this is an actual arm’s-length cross (and not an internal cross between two accounts of the same manager), then it looks like somebody has started to feel good about the deal … all the more so since the record date to vote on the Plan of Arrangement has long since passed.

PerpetualDiscounts now yield 5.93%, equivalent to 7.71% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 4.15%, so the pre-tax interest-equivalent spread is now about 355bp, a stunning increase from the 330bp that I should have reported last week. This is an incredible number, surpassed only for a month or so during the credit crunch … and this is happening without any significant credit worries!

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

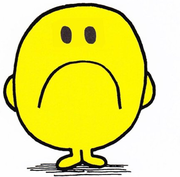

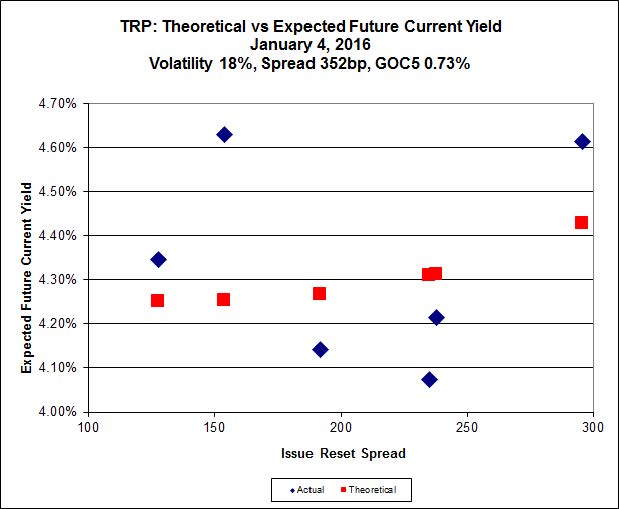

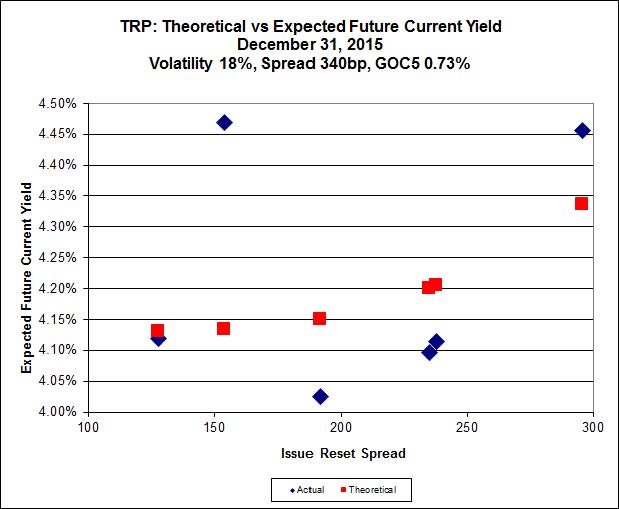

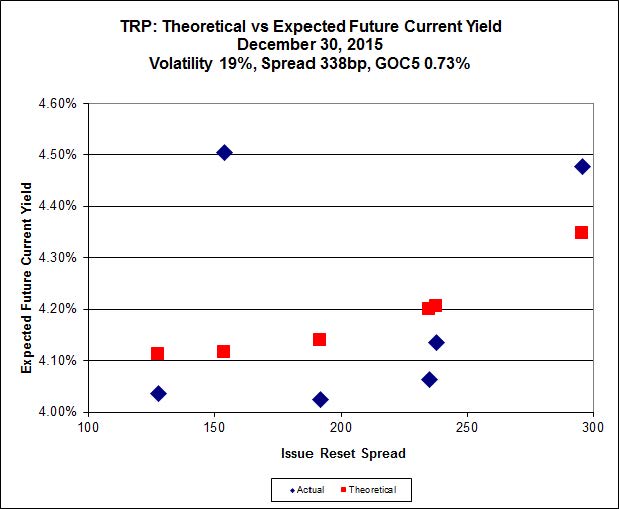

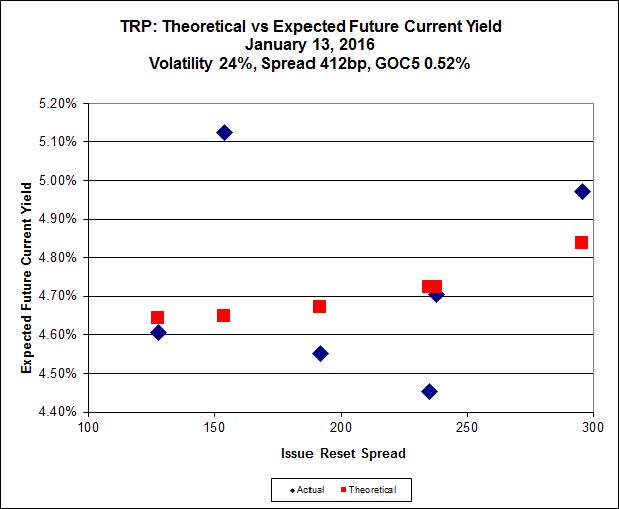

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 16.11 to be $0.91 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $1.03 cheap at its bid price of 10.05.

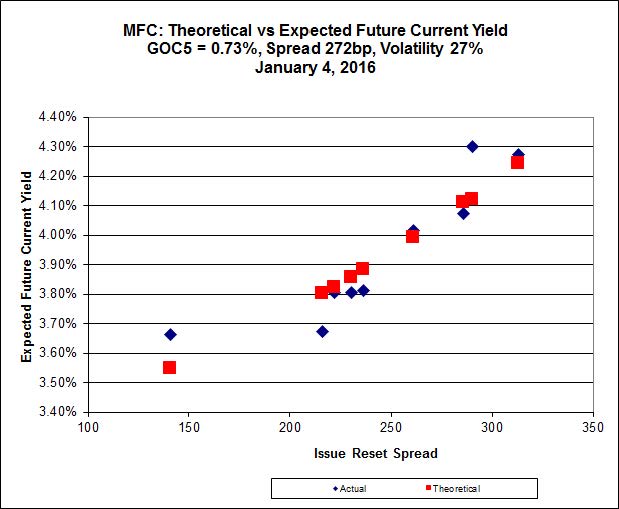

Click for Big

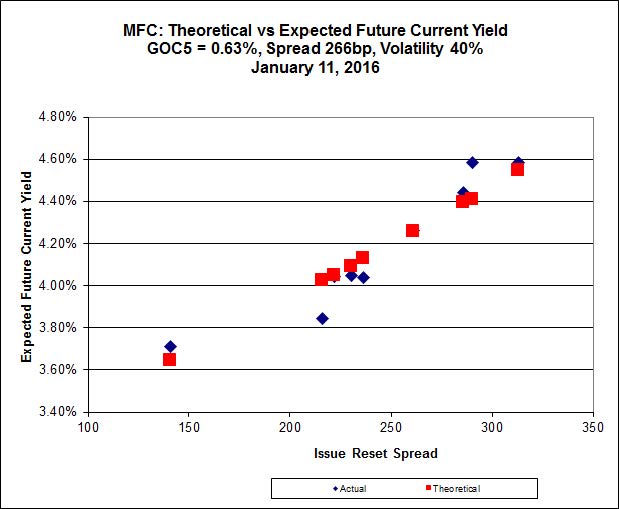

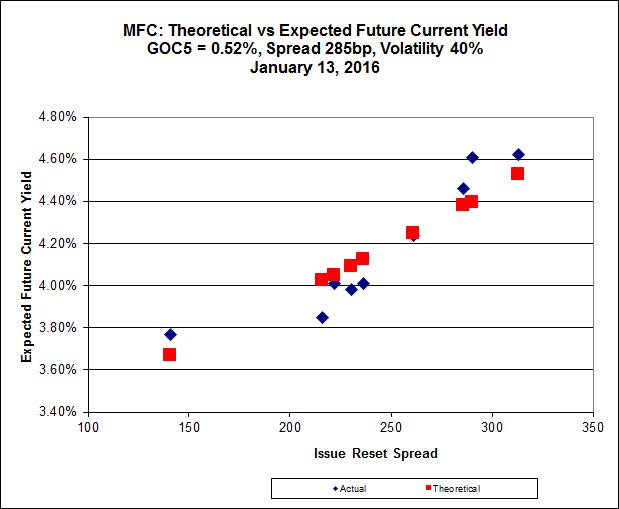

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 17.40 to be 0.75 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 18.55 to be 0.92 cheap.

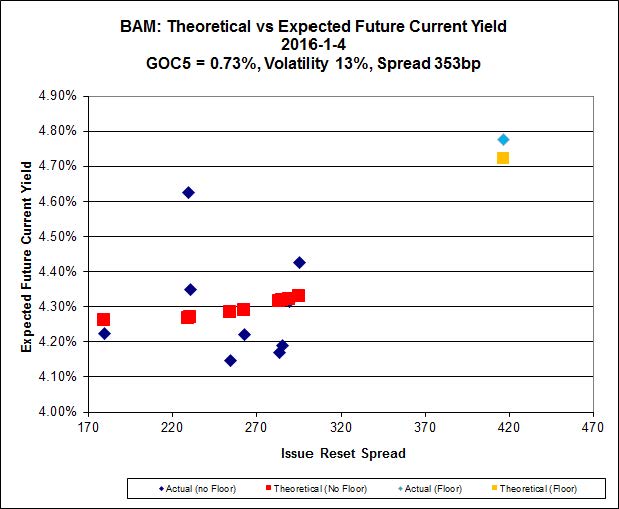

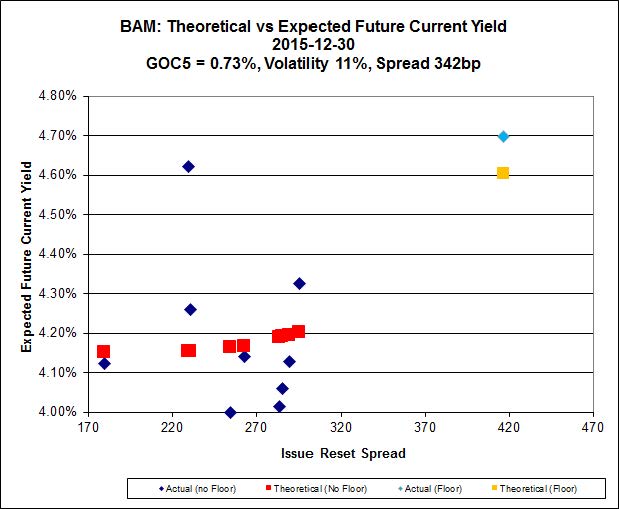

Click for Big

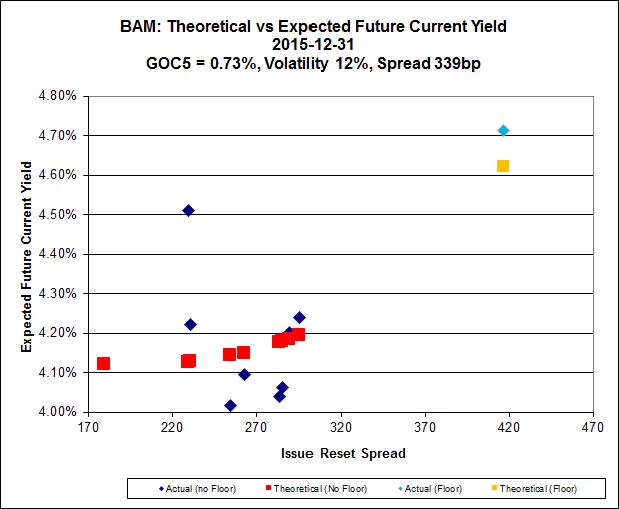

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 13.75 to be $1.09 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 16.83 and appears to be $0.67 rich.

Click for Big

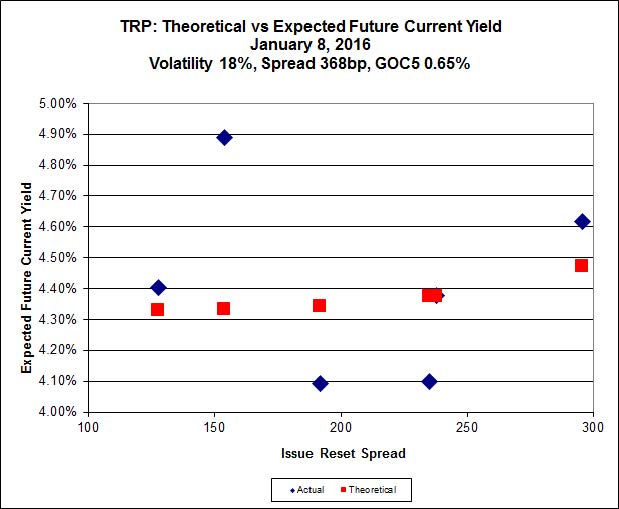

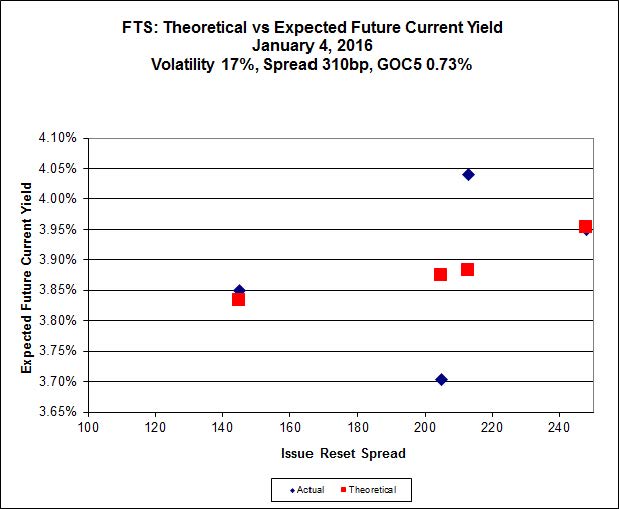

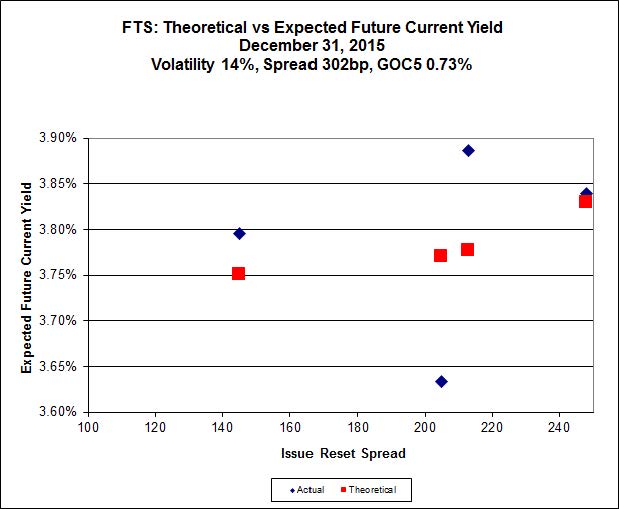

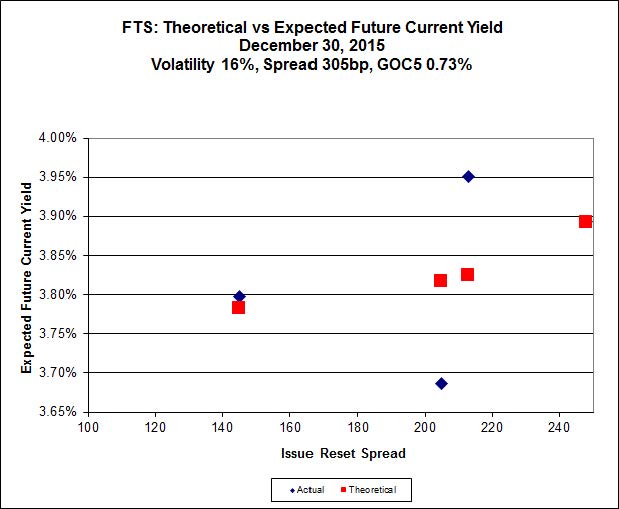

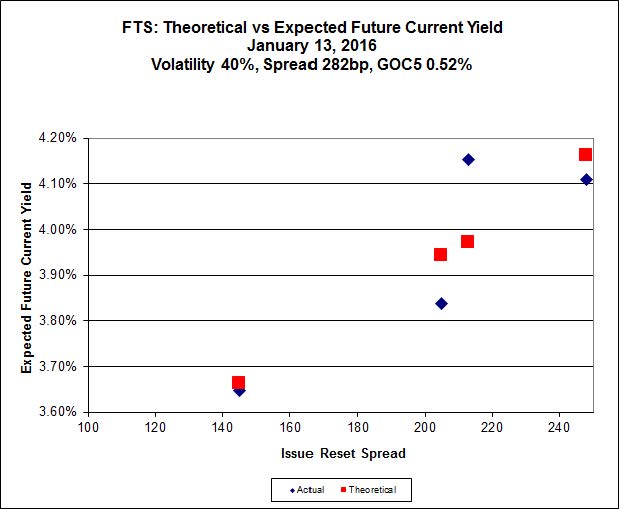

FTS.PR.K, with a spread of +205bp, and bid at 16.74, looks $0.45 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 15.95 and is $0.73 cheap.

Click for Big

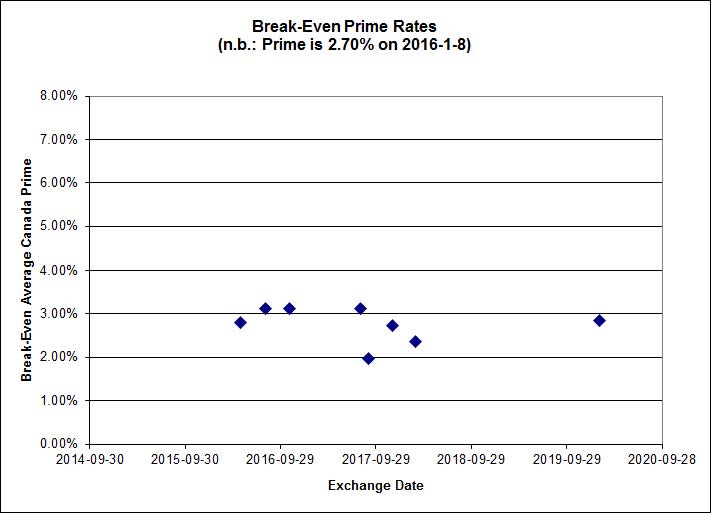

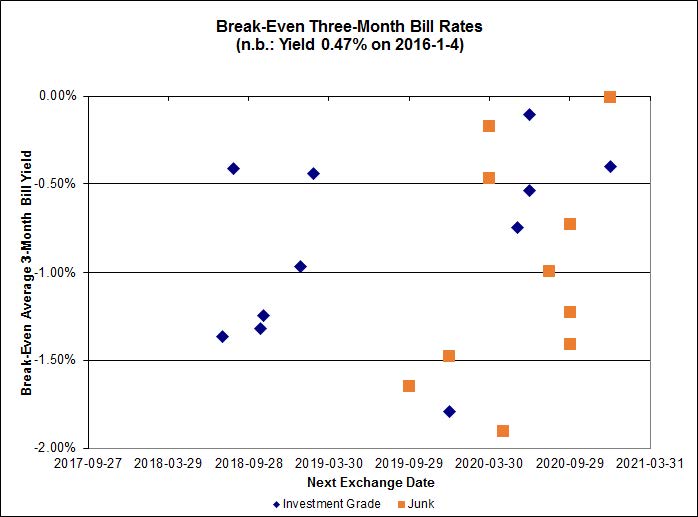

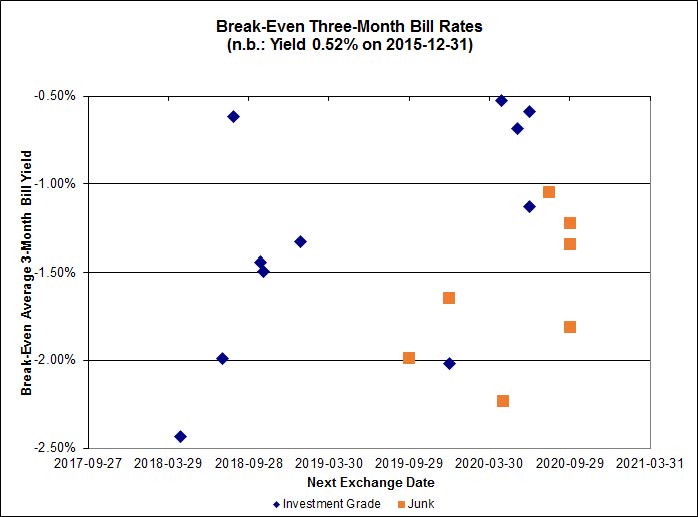

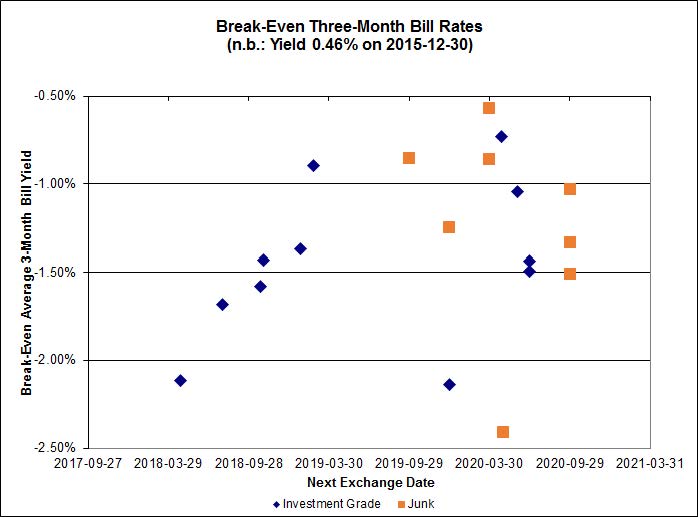

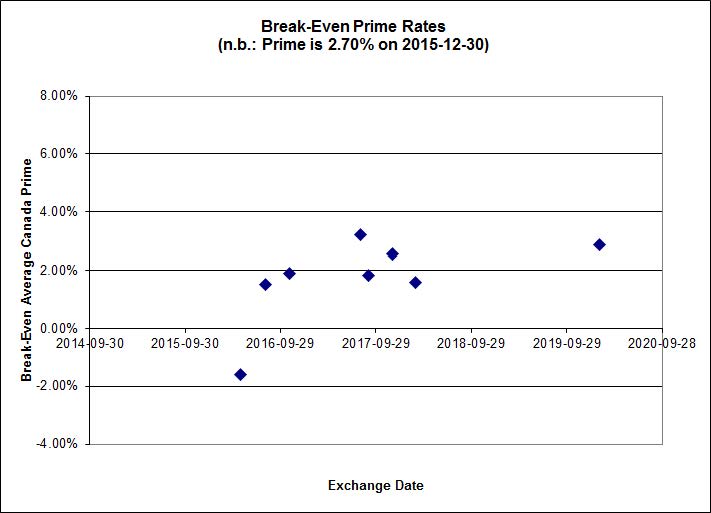

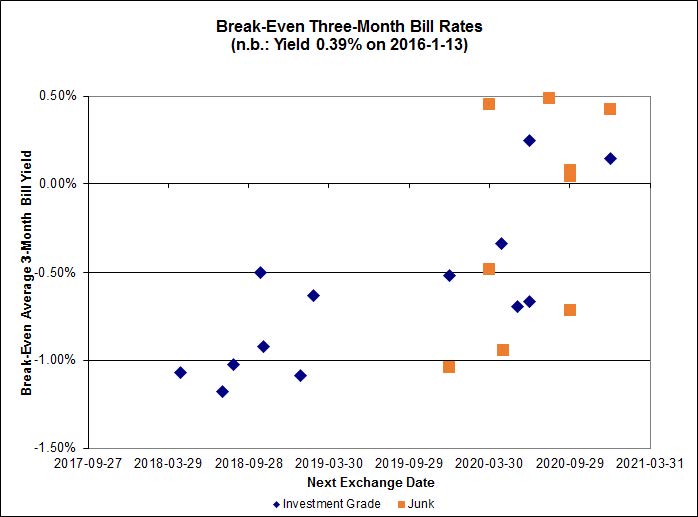

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.63%, with no outliers. There is one junk outlier below -1.50% and one above 0.50%.

Click for Big

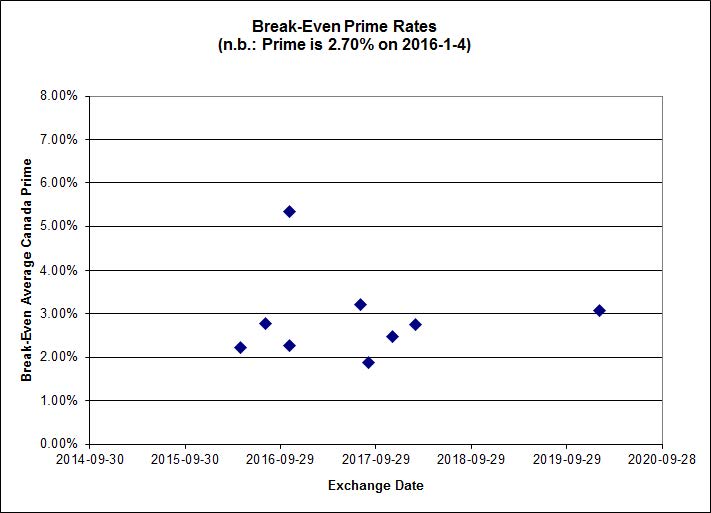

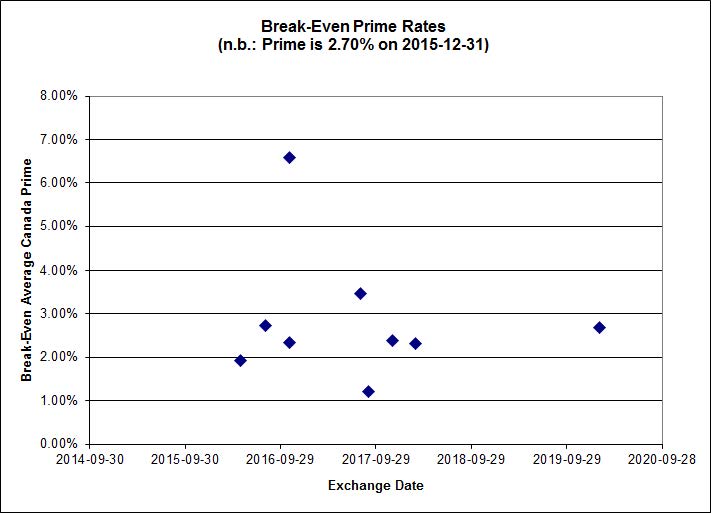

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.12 % | 6.23 % | 26,781 | 16.38 | 1 | -4.2630 % | 1,519.2 |

| FixedFloater | 7.50 % | 6.54 % | 31,078 | 15.80 | 1 | 0.0581 % | 2,651.5 |

| Floater | 4.49 % | 4.69 % | 78,248 | 16.08 | 4 | 0.5017 % | 1,701.0 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0019 % | 2,722.1 |

| SplitShare | 4.85 % | 6.03 % | 67,583 | 2.76 | 6 | 0.0019 % | 3,185.4 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0019 % | 2,485.4 |

| Perpetual-Premium | 5.93 % | 5.82 % | 85,246 | 2.71 | 6 | -0.1684 % | 2,490.2 |

| Perpetual-Discount | 5.84 % | 5.93 % | 93,623 | 14.03 | 34 | -0.4432 % | 2,469.4 |

| FixedReset | 5.65 % | 5.08 % | 238,260 | 14.57 | 81 | -1.3328 % | 1,826.0 |

| Deemed-Retractible | 5.36 % | 5.59 % | 121,511 | 5.27 | 34 | -0.2872 % | 2,509.0 |

| FloatingReset | 2.92 % | 4.91 % | 63,358 | 5.59 | 13 | 0.3148 % | 2,021.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| VNR.PR.A | FixedReset | -7.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.17 Evaluated at bid price : 16.17 Bid-YTW : 5.52 % |

| HSE.PR.E | FixedReset | -5.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.38 Evaluated at bid price : 16.38 Bid-YTW : 6.63 % |

| MFC.PR.F | FixedReset | -5.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.80 Bid-YTW : 10.81 % |

| CU.PR.C | FixedReset | -4.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.27 Evaluated at bid price : 16.27 Bid-YTW : 4.87 % |

| BAM.PR.E | Ratchet | -4.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 25.00 Evaluated at bid price : 13.25 Bid-YTW : 6.23 % |

| FTS.PR.G | FixedReset | -4.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 15.95 Evaluated at bid price : 15.95 Bid-YTW : 4.67 % |

| FTS.PR.K | FixedReset | -3.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.74 Evaluated at bid price : 16.74 Bid-YTW : 4.42 % |

| MFC.PR.H | FixedReset | -3.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.74 Bid-YTW : 7.18 % |

| NA.PR.S | FixedReset | -3.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.73 Evaluated at bid price : 16.73 Bid-YTW : 4.84 % |

| TRP.PR.G | FixedReset | -2.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 5.31 % |

| IFC.PR.C | FixedReset | -2.79 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.72 Bid-YTW : 8.83 % |

| BAM.PR.T | FixedReset | -2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 14.00 Evaluated at bid price : 14.00 Bid-YTW : 5.52 % |

| CM.PR.P | FixedReset | -2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.10 Evaluated at bid price : 16.10 Bid-YTW : 4.81 % |

| NA.PR.W | FixedReset | -2.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.38 Evaluated at bid price : 16.38 Bid-YTW : 4.76 % |

| CM.PR.O | FixedReset | -2.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.85 Evaluated at bid price : 16.85 Bid-YTW : 4.70 % |

| TRP.PR.D | FixedReset | -2.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 15.41 Evaluated at bid price : 15.41 Bid-YTW : 5.22 % |

| BAM.PF.A | FixedReset | -2.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 17.79 Evaluated at bid price : 17.79 Bid-YTW : 5.24 % |

| BMO.PR.W | FixedReset | -2.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.63 Evaluated at bid price : 16.63 Bid-YTW : 4.68 % |

| TRP.PR.C | FixedReset | -2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 10.05 Evaluated at bid price : 10.05 Bid-YTW : 5.48 % |

| HSE.PR.C | FixedReset | -2.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.10 Evaluated at bid price : 16.10 Bid-YTW : 6.21 % |

| BAM.PR.X | FixedReset | -2.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 12.69 Evaluated at bid price : 12.69 Bid-YTW : 5.21 % |

| BMO.PR.S | FixedReset | -2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 4.65 % |

| TD.PF.E | FixedReset | -2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.70 % |

| TRP.PR.F | FloatingReset | -2.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 11.91 Evaluated at bid price : 11.91 Bid-YTW : 4.97 % |

| IFC.PR.A | FixedReset | -2.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.32 Bid-YTW : 10.29 % |

| CU.PR.I | FixedReset | -2.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 22.95 Evaluated at bid price : 24.40 Bid-YTW : 4.58 % |

| BAM.PF.D | Perpetual-Discount | -2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 19.64 Evaluated at bid price : 19.64 Bid-YTW : 6.30 % |

| HSE.PR.G | FixedReset | -2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.68 Evaluated at bid price : 16.68 Bid-YTW : 6.50 % |

| BAM.PF.F | FixedReset | -1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 18.45 Evaluated at bid price : 18.45 Bid-YTW : 5.08 % |

| TRP.PR.B | FixedReset | -1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 9.77 Evaluated at bid price : 9.77 Bid-YTW : 5.12 % |

| SLF.PR.G | FixedReset | -1.86 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.70 Bid-YTW : 9.90 % |

| RY.PR.H | FixedReset | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 17.03 Evaluated at bid price : 17.03 Bid-YTW : 4.63 % |

| BAM.PF.C | Perpetual-Discount | -1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 19.44 Evaluated at bid price : 19.44 Bid-YTW : 6.30 % |

| ELF.PR.H | Perpetual-Discount | -1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 22.36 Evaluated at bid price : 22.66 Bid-YTW : 6.09 % |

| BAM.PR.N | Perpetual-Discount | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 19.10 Evaluated at bid price : 19.10 Bid-YTW : 6.28 % |

| SLF.PR.I | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.31 Bid-YTW : 8.47 % |

| TD.PF.B | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.98 Evaluated at bid price : 16.98 Bid-YTW : 4.55 % |

| NA.PR.Q | FixedReset | -1.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.33 Bid-YTW : 4.54 % |

| SLF.PR.D | Deemed-Retractible | -1.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.20 Bid-YTW : 8.20 % |

| BIP.PR.A | FixedReset | -1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 18.22 Evaluated at bid price : 18.22 Bid-YTW : 5.94 % |

| MFC.PR.M | FixedReset | -1.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.95 Bid-YTW : 7.96 % |

| RY.PR.J | FixedReset | -1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 4.85 % |

| IAG.PR.A | Deemed-Retractible | -1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.06 Bid-YTW : 7.75 % |

| RY.PR.M | FixedReset | -1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 17.75 Evaluated at bid price : 17.75 Bid-YTW : 4.80 % |

| BAM.PR.Z | FixedReset | -1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 5.40 % |

| MFC.PR.N | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.70 Bid-YTW : 8.09 % |

| RY.PR.Z | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 17.11 Evaluated at bid price : 17.11 Bid-YTW : 4.55 % |

| SLF.PR.C | Deemed-Retractible | -1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.35 Bid-YTW : 8.09 % |

| FTS.PR.M | FixedReset | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 18.25 Evaluated at bid price : 18.25 Bid-YTW : 4.63 % |

| BAM.PR.M | Perpetual-Discount | -1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 19.10 Evaluated at bid price : 19.10 Bid-YTW : 6.28 % |

| IAG.PR.G | FixedReset | -1.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.60 Bid-YTW : 7.68 % |

| TRP.PR.A | FixedReset | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 13.40 Evaluated at bid price : 13.40 Bid-YTW : 5.13 % |

| MFC.PR.I | FixedReset | -1.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.95 Bid-YTW : 7.52 % |

| BAM.PF.B | FixedReset | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.73 Evaluated at bid price : 16.73 Bid-YTW : 5.20 % |

| MFC.PR.J | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.46 Bid-YTW : 7.59 % |

| MFC.PR.K | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.08 Bid-YTW : 8.32 % |

| CU.PR.D | Perpetual-Discount | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 20.77 Evaluated at bid price : 20.77 Bid-YTW : 5.99 % |

| W.PR.H | Perpetual-Discount | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 22.27 Evaluated at bid price : 22.54 Bid-YTW : 6.13 % |

| SLF.PR.E | Deemed-Retractible | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.43 Bid-YTW : 8.09 % |

| PWF.PR.T | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 20.25 Evaluated at bid price : 20.25 Bid-YTW : 3.96 % |

| TRP.PR.E | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.11 Evaluated at bid price : 16.11 Bid-YTW : 5.08 % |

| TD.PF.D | FixedReset | -1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 18.29 Evaluated at bid price : 18.29 Bid-YTW : 4.77 % |

| BAM.PF.G | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 18.15 Evaluated at bid price : 18.15 Bid-YTW : 5.20 % |

| BAM.PR.R | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 13.75 Evaluated at bid price : 13.75 Bid-YTW : 5.49 % |

| BMO.PR.Y | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 18.81 Evaluated at bid price : 18.81 Bid-YTW : 4.68 % |

| MFC.PR.B | Deemed-Retractible | -1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.97 Bid-YTW : 7.90 % |

| TD.PF.A | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 17.12 Evaluated at bid price : 17.12 Bid-YTW : 4.53 % |

| CM.PR.Q | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 18.37 Evaluated at bid price : 18.37 Bid-YTW : 4.75 % |

| BAM.PF.E | FixedReset | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.83 Evaluated at bid price : 16.83 Bid-YTW : 5.22 % |

| TD.PR.Y | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.02 Bid-YTW : 4.42 % |

| RY.PR.K | FloatingReset | 1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.65 Bid-YTW : 4.96 % |

| POW.PR.C | Perpetual-Premium | 1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 24.30 Evaluated at bid price : 24.61 Bid-YTW : 5.92 % |

| BAM.PF.H | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 23.20 Evaluated at bid price : 25.10 Bid-YTW : 4.91 % |

| BNS.PR.Q | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.81 Bid-YTW : 4.63 % |

| PWF.PR.P | FixedReset | 1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 12.00 Evaluated at bid price : 12.00 Bid-YTW : 4.71 % |

| MFC.PR.G | FixedReset | 1.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.55 Bid-YTW : 7.74 % |

| BAM.PR.K | Floater | 2.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 10.15 Evaluated at bid price : 10.15 Bid-YTW : 4.69 % |

| BNS.PR.R | FixedReset | 2.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.57 Bid-YTW : 4.28 % |

| CCS.PR.C | Deemed-Retractible | 2.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.28 Bid-YTW : 7.35 % |

| BNS.PR.D | FloatingReset | 3.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.08 Bid-YTW : 7.08 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.Q | FixedReset | 288,467 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 23.28 Evaluated at bid price : 25.46 Bid-YTW : 5.11 % |

| BNS.PR.E | FixedReset | 158,036 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 23.29 Evaluated at bid price : 25.47 Bid-YTW : 5.10 % |

| NA.PR.S | FixedReset | 108,125 | TD crossed 98,800 at 16.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-13 Maturity Price : 16.73 Evaluated at bid price : 16.73 Bid-YTW : 4.84 % |

| TD.PR.T | FloatingReset | 65,152 | Scotia crossed 63,200 at 21.65. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.58 Bid-YTW : 4.56 % |

| RY.PR.I | FixedReset | 43,400 | Nesbitt crossed 35,000 at 23.21. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.20 Bid-YTW : 4.57 % |

| BNS.PR.L | Deemed-Retractible | 39,064 | RBC crossed 35,300 at 24.48. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.48 Bid-YTW : 4.88 % |

| There were 20 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| GWO.PR.O | FloatingReset | Quote: 11.95 – 13.75 Spot Rate : 1.8000 Average : 1.4048 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 16.17 – 17.11 Spot Rate : 0.9400 Average : 0.7033 YTW SCENARIO |

| FTS.PR.M | FixedReset | Quote: 18.25 – 18.87 Spot Rate : 0.6200 Average : 0.4595 YTW SCENARIO |

| FTS.PR.H | FixedReset | Quote: 13.50 – 13.99 Spot Rate : 0.4900 Average : 0.3545 YTW SCENARIO |

| HSE.PR.G | FixedReset | Quote: 16.68 – 17.29 Spot Rate : 0.6100 Average : 0.4813 YTW SCENARIO |

| GWO.PR.L | Deemed-Retractible | Quote: 23.90 – 24.36 Spot Rate : 0.4600 Average : 0.3511 YTW SCENARIO |