Looks like we may be looking at a Tobin Tax:

Chinese securities regulators are preparing some of the world’s strictest regulations on a trading practice at the heart of the global debate over high-speed computerized markets.

The draft rules are designed to prevent traders from flooding exchanges with orders they don’t fill by charging market participants fees for habitual cancellations. The proposal, which could come into force next year, echoes a plan by U.S. presidential hopeful Hillary Clinton to discourage high-speed trading strategies that she says could destabilize markets.

As regulators around the world grapple with the most effective ways to police computer-driven markets, they have focused on how to stop traders from using bogus orders to unfairly move prices in their favor. Critics contend that the tactic makes markets less fair and enables some traders to engage in a manipulative practice known as spoofing. Opponents of the proposed taxes on canceled orders say they would harm legitimate market makers and raise costs for the average investor.

…

China’s proposals on algorithmic trading, revealed around the same time in October as Clinton’s, state that “frequently placing and withdrawing orders where the ratio of trades concluded is abnormally low” would be prohibited, according to a translation by law firm Linklaters LLP. Traders who cancel more than 40 percent of their submitted orders in any given day would be charged a fee of 2 yuan (31 cents) per transaction.

…

Other measures suggested by the CSRC include forcing traders who use automated orders to provide a detailed description of their strategies to regulators and wait for a review before they’re allowed to execute trades. That proposal has raised concern among some international investors who don’t want to disclose their proprietary trading algorithms, according to Calvin Tai, the head of global clearing at Hong Kong’s stock exchange.Clinton, the front-runner to win the Democratic nomination for president, called for a fee on canceled orders in October and explicitly linked the idea to curbing high-frequency traders. Her plan is designed to target “harmful” high-frequency trading that makes markets “less stable and less fair,” Clinton’s campaign said at the time.

There is nothing intrinsically wrong with an exchange fee for cancelled orders. A 96% cancellation rate will obviously strain the system more than will a lower rate and require increased investment by all serious participants, in bandwidth and a ticker-plant. However, when charges such as China’s $0.31/transaction become exorbitant it becomes clear that this is just a revenue grab that will lead to migration of the markets to more trader-friendly nations, as well as having all the usual effects of ‘stamp charges’ on market liquidity. Compare the $0.31/transaction fee to the Toronto Stock Exchange’s Maker-Taker fees, which net out to $0.0004 / share. [I’ll save you the trouble: that means the Exchange would charge as much for a cancelled order as for an execution of 775 shares].

As I stated on April 3, 2014:

However, it is quite apparent that Tobin taxes harm market quality. One possibility where the AR PL and I might have a meeting of minds is the potential for an exchange to impose a fee for the placement of an order – generally, once you’re permitted to place orders on the exchange, the only fees remaining are charged for executed transactions.

Schwab is upset about the number of orders:

High-frequency trading pumped out over 300,000 trade inquiries each second last year, up from just 50,000 only seven years earlier. Yet actual trade volume on the exchanges has remained relatively flat over that period. It’s an explosion of head-fake ephemeral orders – not to lock in real trades, but to skim pennies off the public markets by the billions.

…

Added systems burdens, costs and distortions of rapid-fire quote activity: Ephemeral quotes, also called “quote stuffing,” that are cancelled and reposted in milliseconds distort the tape and present risk to the resiliency and integrity of critical market data and trading infrastructure. The tremendous added costs associated with the expanded capacity and bandwidth necessary to support this added data traffic is ultimately borne in part by individual investors.There are solutions. Today there is no restriction to pumping out millions of orders in a matter of seconds, only to reverse the majority of them. It’s the life-blood of high-frequency trading. A simple solution would be to establish cancellation fees to discourage the practice of quote stuffing. The SEC and CFTC floated the idea last year. It has great merit. Make the fees high enough and they will eliminate high-frequency trading entirely.

However, I would support a charge for order entry (or simply order cancellation, assuming that executed orders get charged by other means) only to the extent that it is imposed by the exchanges to recover costs or as a source of competitive advantage. If, once you count amortization of all the required infrastructure, it costs $1 to process 1,000,000 orders, then by all means, charge $0.000001 to process an order. If you want to make a profit and the market will bear it, then by all means, charge $0.000002 to process an order. If your customers complain that they have to process all these orders too, then by all means offer them a kiddie feed at reduced price, transmitting orders only when they have been extant for 10 milliseconds.

But don’t start imposing fees with grandiose visions of Better Living Through Higher Taxation. We all know where that ends up.

Fortis Inc., proud issuer of FTS.PR.E, FTS.PR.F, FTS.PR.G, FTS.PR.H, FTS.PR.I, FTS.PR.J, FTS.PR.K and FTS.PR.M, was confirmed at Pfd-2(low) by DBRS:

DBRS Limited (DBRS) has today confirmed the A (low) Issuer Rating, A (low) Unsecured Debentures rating and Pfd-2 (low) Preferred Shares rating of Fortis Inc. (Fortis, the Parent or the Company) with Stable trends. This action is based on DBRS’s view of the Company’s financial performance to date in 2015 (YTD 2015). The confirmations reflect Fortis’ improved business risk profile following the completion of the Waneta Expansion hydro generation project (Waneta Expansion), no material changes in its regulated subsidiaries and its reasonable consolidated and non-consolidated financial profiles.

…

Fortis maintained reasonable consolidated and non-consolidated ratios in YTD 2015 and remained consistent with the current rating. These ratios are expected to improve by the end of 2015 and in the medium term since (i) $230 million non-consolidated debt was reduced after September 30, 2015, with proceeds from the sale of Fortis Properties; (ii) all regulated utilities are expected to maintain their leverage in line with the regulatory capital structure in their respective jurisdictions; and (iii) Fortis’ equity injection to its utilities is expected to be modest and manageable over the next few years.

The cessation of tax-loss selling pressure led to a superb day for the Canadian preferred share market, with PerpetualDiscounts up 94bp, FixedResets winning 121bp and DeemedRetractibles gaining 87bp. The Performance Highlights table is enormous, naturally enough, with only one loser. Volume was very extremely awfully low.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

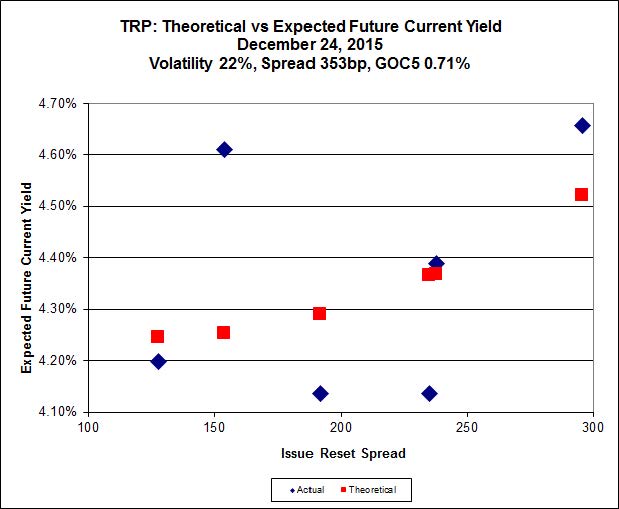

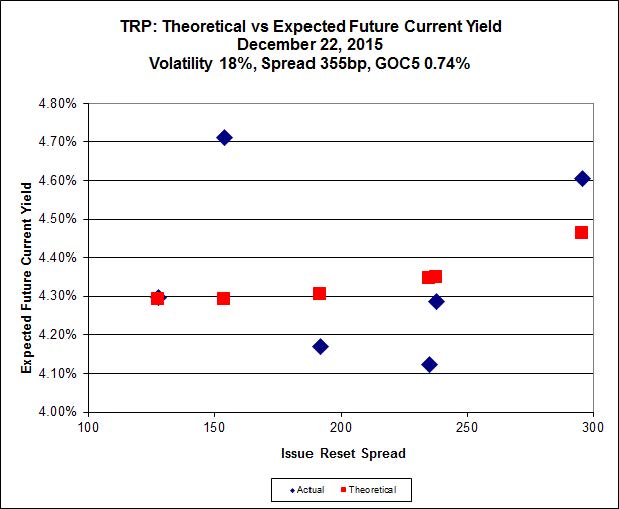

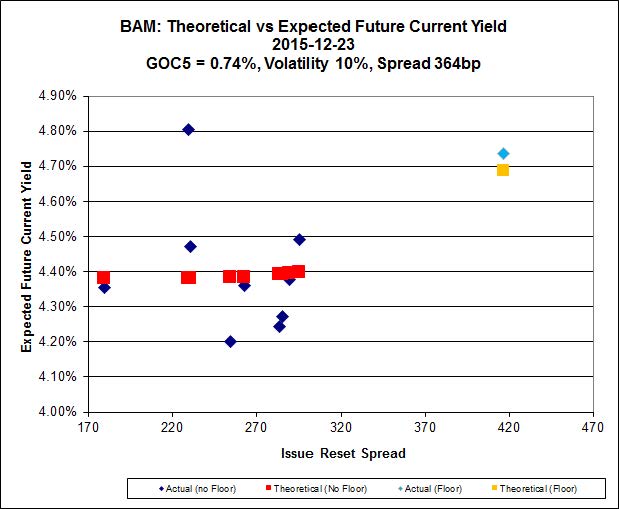

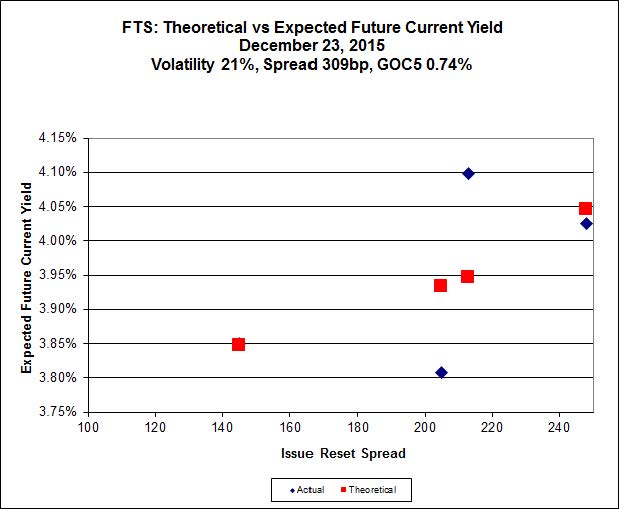

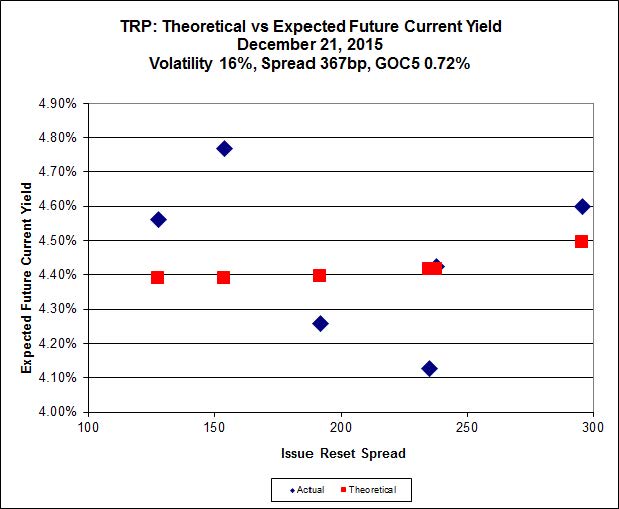

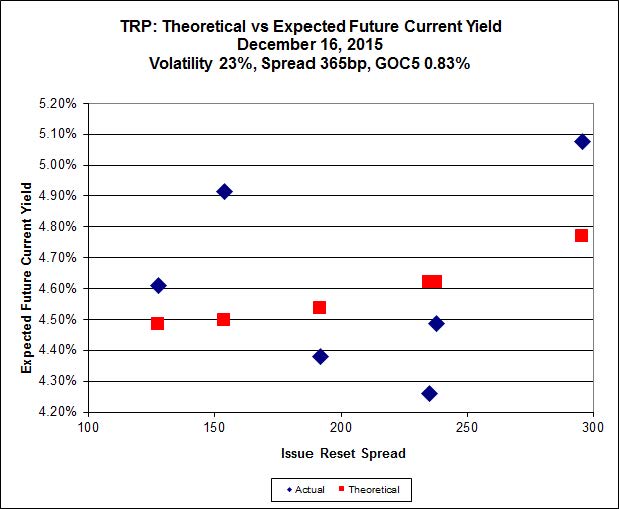

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 18.86 to be $0.91 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $1.19 cheap at its bid price of 12.30.

Click for Big

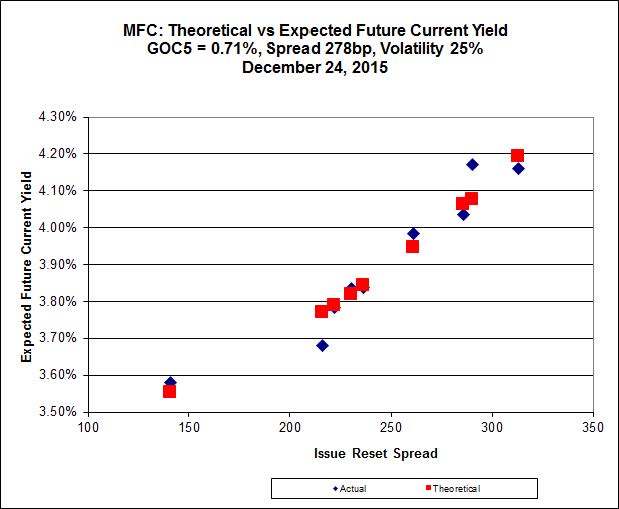

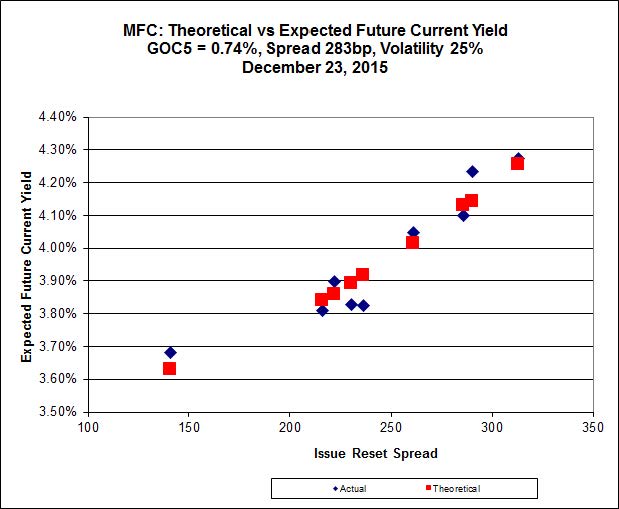

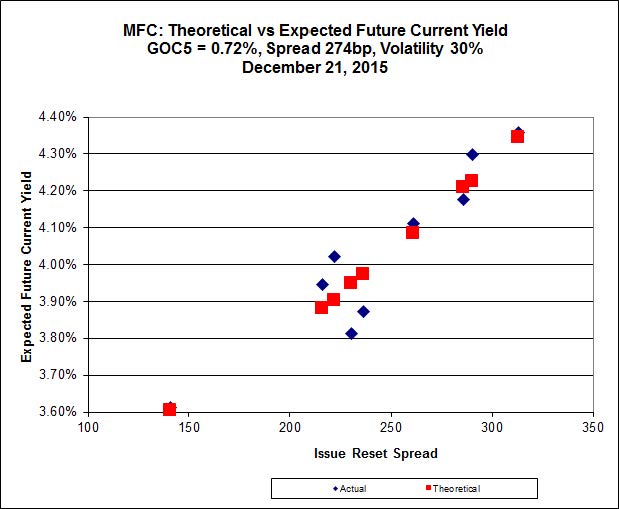

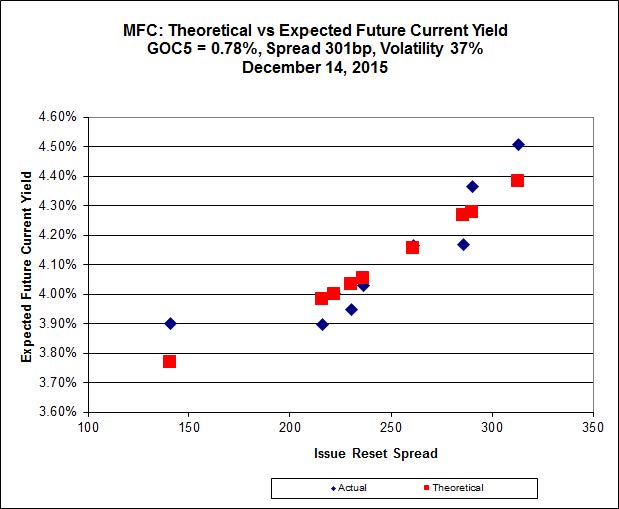

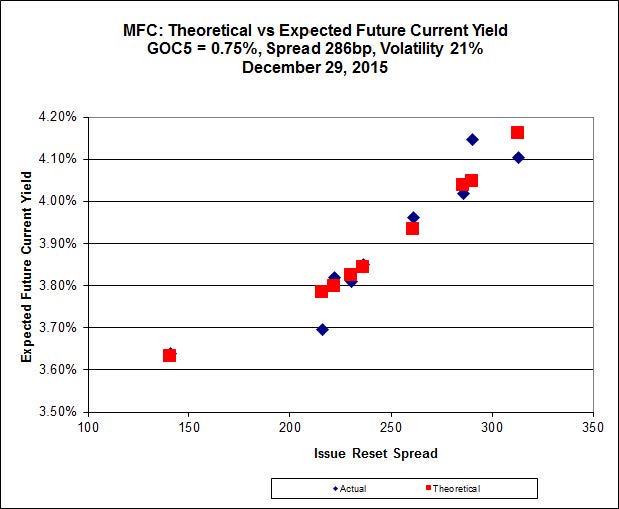

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 19.68 to be 0.45 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 22.00 to be 0.54 cheap.

Click for Big

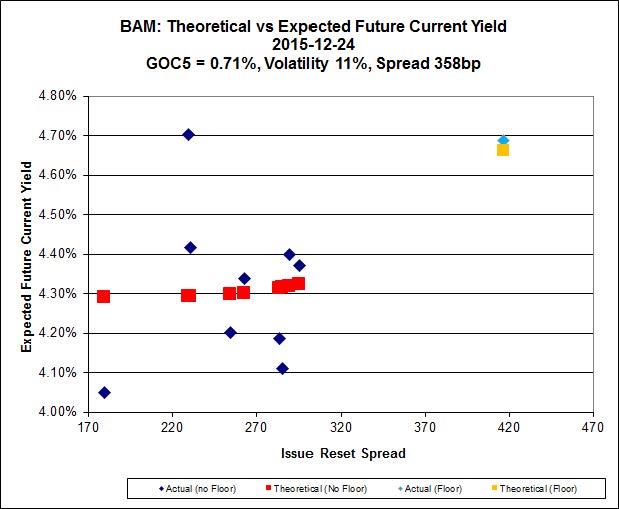

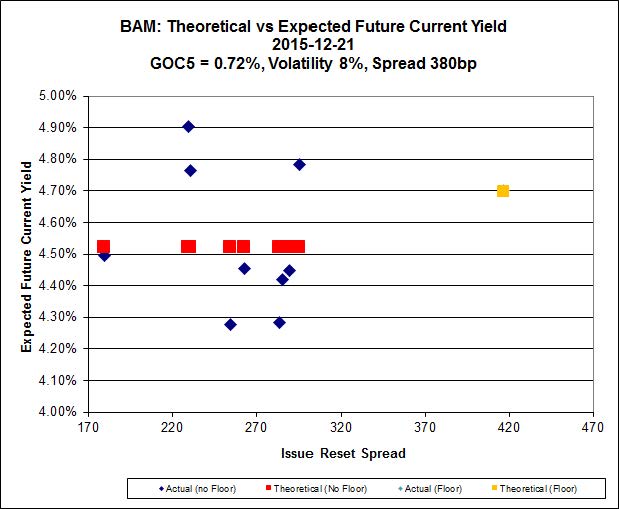

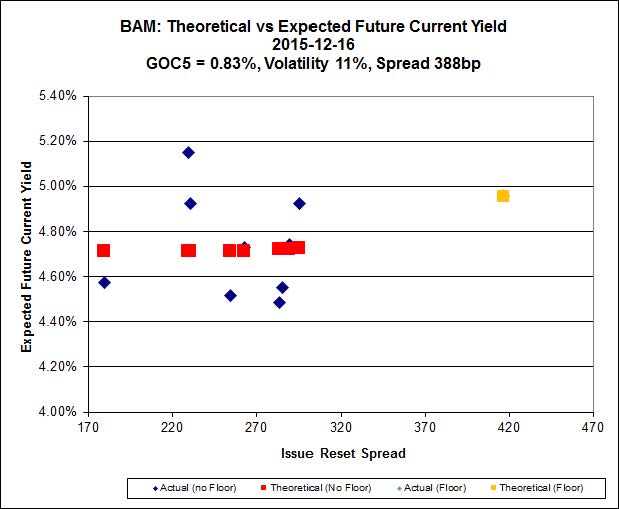

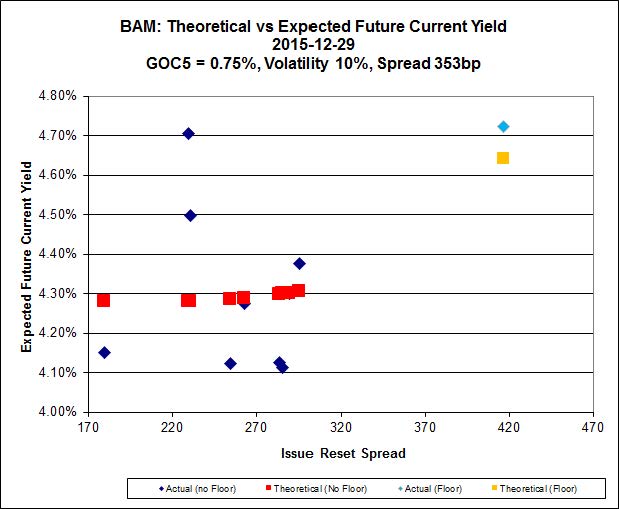

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.21 to be $1.60 cheap. BAM.PF.F, resetting at +286bp on 2019-9-30 is bid at 21.95 and appears to be $0.96 rich.

Click for Big

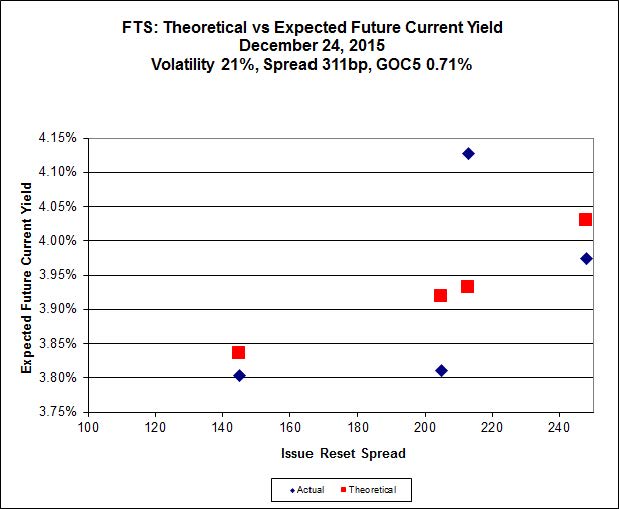

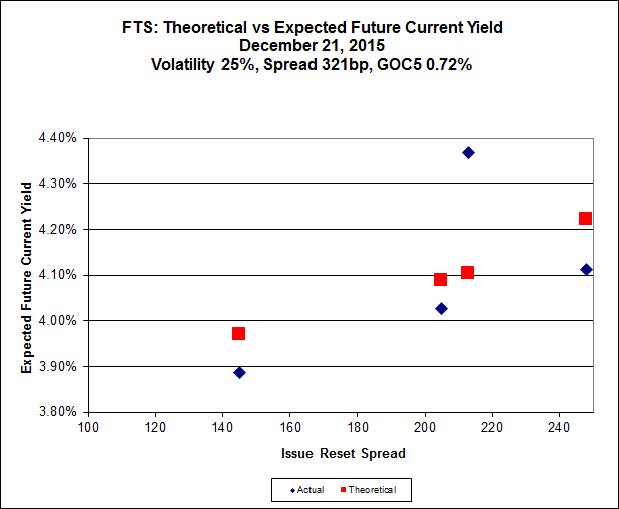

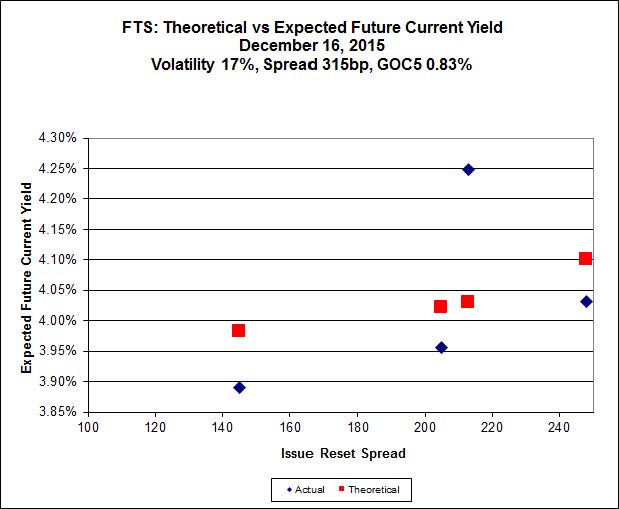

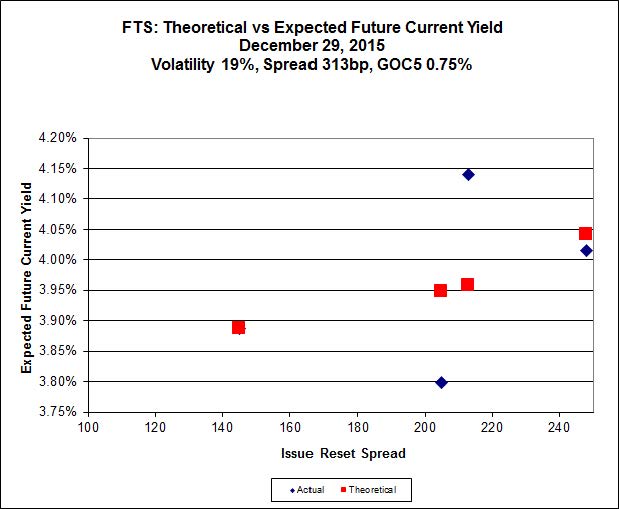

FTS.PR.K, with a spread of +205bp, and bid at 18.43, looks $0.70 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 17.39 and is $0.80 cheap.

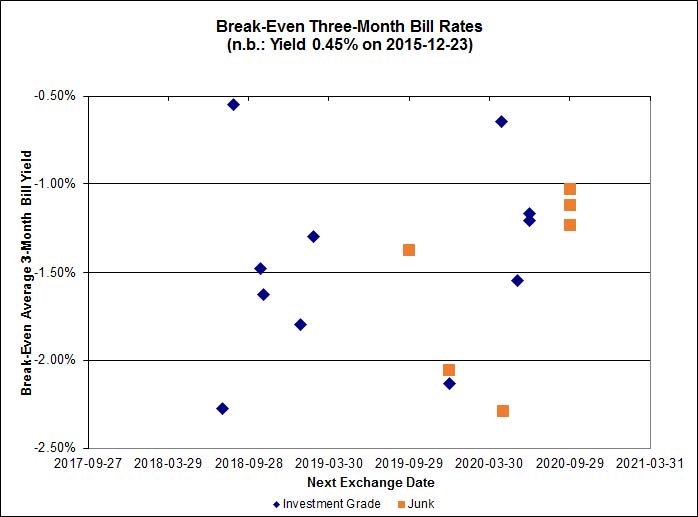

Click for Big

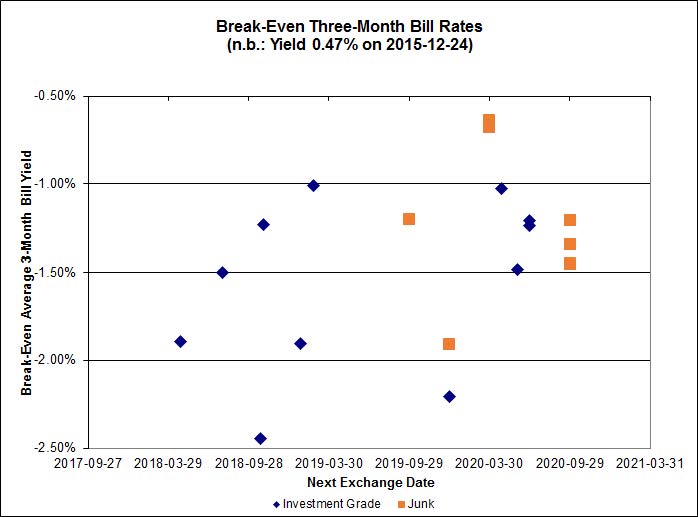

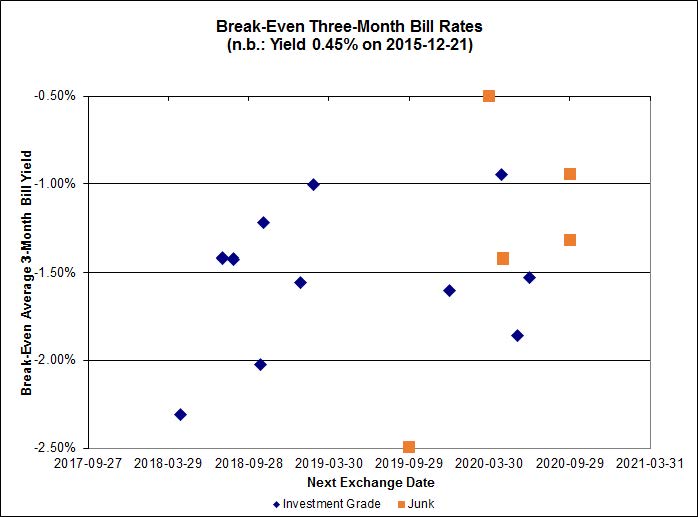

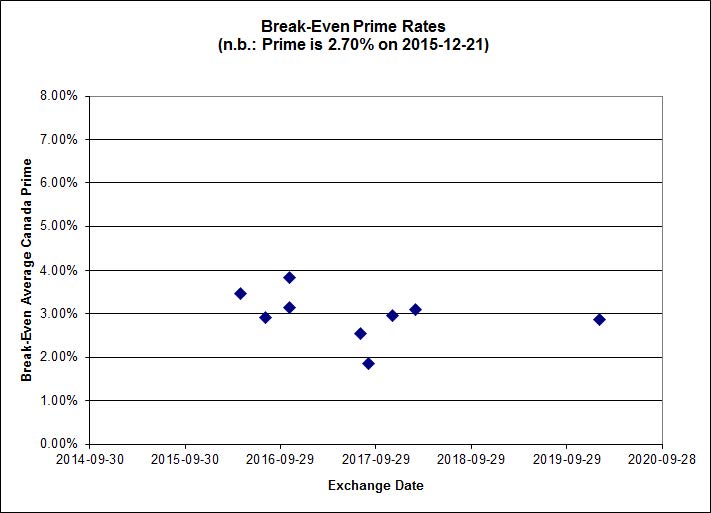

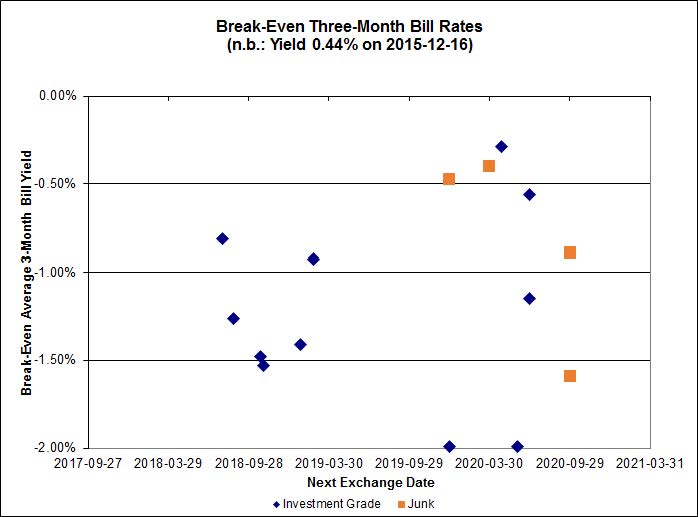

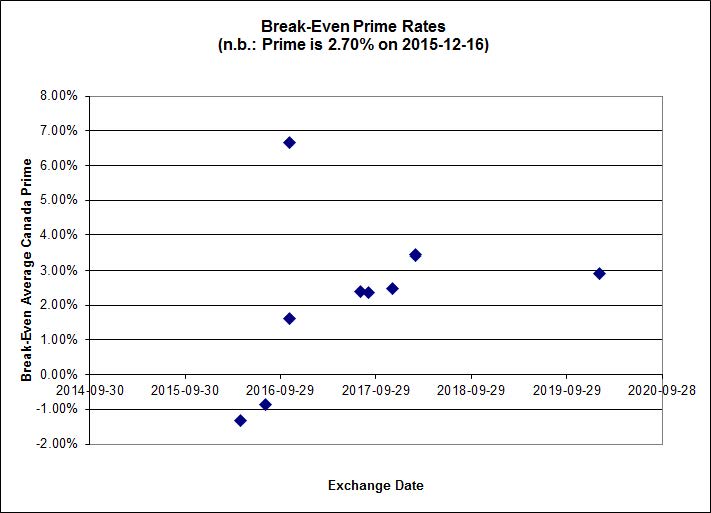

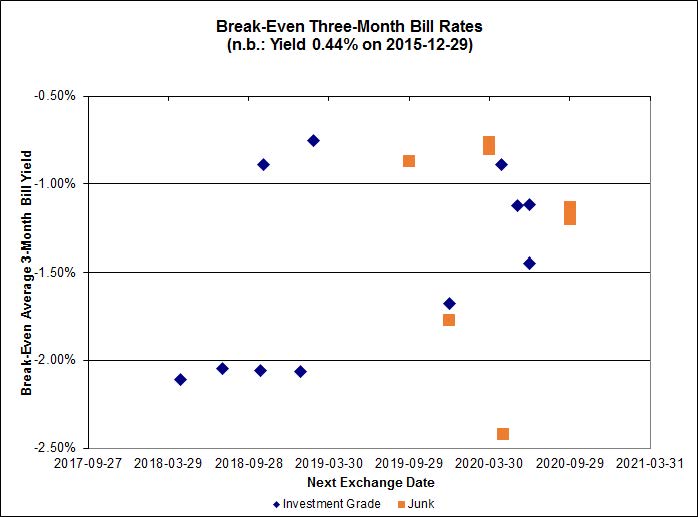

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.37%, with one outlier above -0.50%. There are two junk outliers above -0.50%.

Click for Big

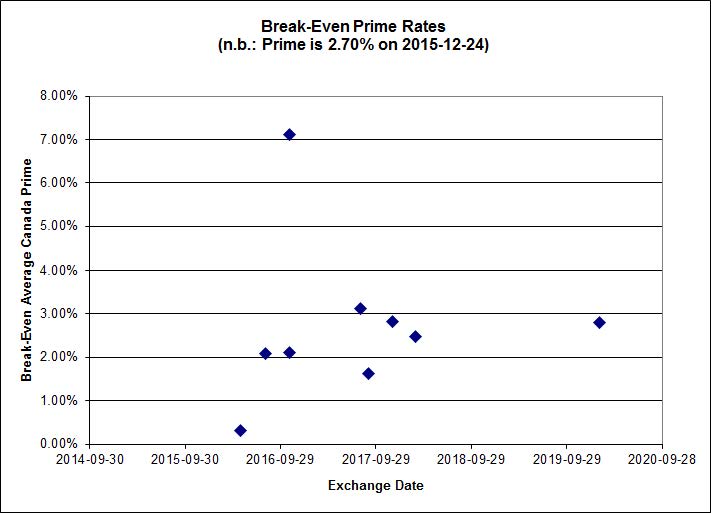

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.91 % | 5.95 % | 32,165 | 16.74 | 1 | 0.0180 % | 1,586.9 |

| FixedFloater | 7.10 % | 6.30 % | 39,441 | 15.85 | 1 | 1.1338 % | 2,748.6 |

| Floater | 4.28 % | 4.40 % | 82,517 | 16.61 | 4 | 2.8658 % | 1,785.1 |

| OpRet | 4.86 % | 4.15 % | 26,388 | 0.66 | 1 | 0.0794 % | 2,740.8 |

| SplitShare | 4.83 % | 5.42 % | 84,274 | 1.84 | 6 | 0.3027 % | 3,202.4 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3027 % | 2,498.6 |

| Perpetual-Premium | 5.79 % | 5.45 % | 91,663 | 2.58 | 7 | 0.8523 % | 2,518.1 |

| Perpetual-Discount | 5.69 % | 5.75 % | 105,325 | 14.27 | 33 | 0.9418 % | 2,523.3 |

| FixedReset | 5.07 % | 4.37 % | 270,601 | 14.85 | 81 | 1.2111 % | 2,040.7 |

| Deemed-Retractible | 5.17 % | 4.79 % | 134,552 | 5.27 | 33 | 0.8682 % | 2,594.6 |

| FloatingReset | 2.79 % | 4.12 % | 70,258 | 5.63 | 11 | 1.1263 % | 2,135.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| NA.PR.W | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 18.02 Evaluated at bid price : 18.02 Bid-YTW : 4.45 % |

| MFC.PR.M | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.20 Bid-YTW : 6.33 % |

| BAM.PR.Z | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 21.20 Evaluated at bid price : 21.20 Bid-YTW : 4.49 % |

| GWO.PR.S | Deemed-Retractible | 1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.75 Bid-YTW : 5.42 % |

| SLF.PR.A | Deemed-Retractible | 1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.72 Bid-YTW : 6.74 % |

| TD.PF.F | Perpetual-Discount | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 22.19 Evaluated at bid price : 22.55 Bid-YTW : 5.51 % |

| RY.PR.O | Perpetual-Discount | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 22.16 Evaluated at bid price : 22.52 Bid-YTW : 5.49 % |

| TD.PR.Z | FloatingReset | 1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.48 Bid-YTW : 4.02 % |

| BAM.PF.F | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 21.66 Evaluated at bid price : 21.95 Bid-YTW : 4.27 % |

| PWF.PR.O | Perpetual-Premium | 1.08 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2018-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.34 Bid-YTW : 5.67 % |

| FTS.PR.G | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 17.39 Evaluated at bid price : 17.39 Bid-YTW : 4.34 % |

| BAM.PR.G | FixedFloater | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 25.00 Evaluated at bid price : 13.38 Bid-YTW : 6.30 % |

| TD.PF.D | FixedReset | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 4.36 % |

| POW.PR.B | Perpetual-Discount | 1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 22.93 Evaluated at bid price : 23.20 Bid-YTW : 5.77 % |

| BNS.PR.P | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.95 Bid-YTW : 3.14 % |

| HSE.PR.A | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 12.15 Evaluated at bid price : 12.15 Bid-YTW : 5.07 % |

| PVS.PR.B | SplitShare | 1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2019-01-10 Maturity Price : 25.00 Evaluated at bid price : 24.00 Bid-YTW : 5.94 % |

| IGM.PR.B | Perpetual-Premium | 1.27 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2018-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.20 Bid-YTW : 5.45 % |

| BAM.PR.K | Floater | 1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 10.30 Evaluated at bid price : 10.30 Bid-YTW : 4.59 % |

| RY.PR.H | FixedReset | 1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 18.99 Evaluated at bid price : 18.99 Bid-YTW : 4.19 % |

| FTS.PR.F | Perpetual-Discount | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 22.35 Evaluated at bid price : 22.62 Bid-YTW : 5.46 % |

| VNR.PR.A | FixedReset | 1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 19.35 Evaluated at bid price : 19.35 Bid-YTW : 4.75 % |

| BAM.PR.R | FixedReset | 1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 16.21 Evaluated at bid price : 16.21 Bid-YTW : 4.74 % |

| TD.PR.S | FixedReset | 1.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.52 Bid-YTW : 3.24 % |

| SLF.PR.D | Deemed-Retractible | 1.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.41 Bid-YTW : 7.28 % |

| TD.PF.B | FixedReset | 1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 18.86 Evaluated at bid price : 18.86 Bid-YTW : 4.22 % |

| ELF.PR.G | Perpetual-Discount | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 20.78 Evaluated at bid price : 20.78 Bid-YTW : 5.84 % |

| PWF.PR.H | Perpetual-Premium | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 24.69 Evaluated at bid price : 25.01 Bid-YTW : 5.84 % |

| SLF.PR.J | FloatingReset | 1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.20 Bid-YTW : 9.86 % |

| ELF.PR.F | Perpetual-Discount | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 22.47 Evaluated at bid price : 22.73 Bid-YTW : 5.94 % |

| TRP.PR.A | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 16.12 Evaluated at bid price : 16.12 Bid-YTW : 4.31 % |

| BMO.PR.Z | Perpetual-Discount | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 23.01 Evaluated at bid price : 23.43 Bid-YTW : 5.38 % |

| BNS.PR.B | FloatingReset | 1.43 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.01 Bid-YTW : 4.42 % |

| GWO.PR.G | Deemed-Retractible | 1.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.24 Bid-YTW : 6.26 % |

| BMO.PR.S | FixedReset | 1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 19.26 Evaluated at bid price : 19.26 Bid-YTW : 4.21 % |

| SLF.PR.B | Deemed-Retractible | 1.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.80 Bid-YTW : 6.74 % |

| MFC.PR.I | FixedReset | 1.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.46 Bid-YTW : 5.20 % |

| W.PR.K | FixedReset | 1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 23.09 Evaluated at bid price : 24.79 Bid-YTW : 5.25 % |

| TD.PF.C | FixedReset | 1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 4.23 % |

| GWO.PR.H | Deemed-Retractible | 1.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.88 Bid-YTW : 6.74 % |

| GWO.PR.Q | Deemed-Retractible | 1.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.10 Bid-YTW : 6.30 % |

| SLF.PR.C | Deemed-Retractible | 1.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.60 Bid-YTW : 7.15 % |

| BMO.PR.W | FixedReset | 1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 18.60 Evaluated at bid price : 18.60 Bid-YTW : 4.22 % |

| HSE.PR.G | FixedReset | 1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 18.55 Evaluated at bid price : 18.55 Bid-YTW : 5.87 % |

| SLF.PR.E | Deemed-Retractible | 1.66 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.79 Bid-YTW : 7.08 % |

| FTS.PR.J | Perpetual-Discount | 1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 21.70 Evaluated at bid price : 22.00 Bid-YTW : 5.44 % |

| SLF.PR.H | FixedReset | 1.69 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.01 Bid-YTW : 7.24 % |

| MFC.PR.G | FixedReset | 1.71 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 5.43 % |

| BMO.PR.Y | FixedReset | 1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 20.65 Evaluated at bid price : 20.65 Bid-YTW : 4.30 % |

| FTS.PR.K | FixedReset | 1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 18.43 Evaluated at bid price : 18.43 Bid-YTW : 4.06 % |

| GWO.PR.I | Deemed-Retractible | 1.81 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.84 Bid-YTW : 7.04 % |

| MFC.PR.J | FixedReset | 1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.21 Bid-YTW : 5.71 % |

| BNS.PR.D | FloatingReset | 1.83 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.91 Bid-YTW : 6.35 % |

| IAG.PR.G | FixedReset | 1.89 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.55 Bid-YTW : 5.68 % |

| NA.PR.Q | FixedReset | 1.92 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-11-15 Maturity Price : 25.00 Evaluated at bid price : 25.50 Bid-YTW : 2.97 % |

| MFC.PR.N | FixedReset | 1.99 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.01 Bid-YTW : 6.39 % |

| MFC.PR.C | Deemed-Retractible | 2.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.76 Bid-YTW : 7.12 % |

| MFC.PR.B | Deemed-Retractible | 2.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.20 Bid-YTW : 7.00 % |

| NA.PR.S | FixedReset | 2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 4.43 % |

| RY.PR.L | FixedReset | 2.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.56 Bid-YTW : 3.53 % |

| TRP.PR.B | FixedReset | 2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 12.10 Evaluated at bid price : 12.10 Bid-YTW : 4.21 % |

| BIP.PR.A | FixedReset | 2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 20.32 Evaluated at bid price : 20.32 Bid-YTW : 5.36 % |

| GWO.PR.M | Deemed-Retractible | 2.15 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2019-03-31 Maturity Price : 25.00 Evaluated at bid price : 25.69 Bid-YTW : 4.89 % |

| IFC.PR.A | FixedReset | 2.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.14 Bid-YTW : 8.63 % |

| GWO.PR.P | Deemed-Retractible | 2.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.41 Bid-YTW : 5.77 % |

| CM.PR.Q | FixedReset | 2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 20.29 Evaluated at bid price : 20.29 Bid-YTW : 4.34 % |

| FTS.PR.I | FloatingReset | 2.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 12.14 Evaluated at bid price : 12.14 Bid-YTW : 3.96 % |

| CIU.PR.A | Perpetual-Discount | 2.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 20.40 Evaluated at bid price : 20.40 Bid-YTW : 5.71 % |

| MFC.PR.H | FixedReset | 2.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.64 Bid-YTW : 4.73 % |

| HSE.PR.C | FixedReset | 2.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 16.96 Evaluated at bid price : 16.96 Bid-YTW : 5.94 % |

| GWO.PR.R | Deemed-Retractible | 2.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.79 Bid-YTW : 6.75 % |

| BAM.PF.G | FixedReset | 2.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 21.48 Evaluated at bid price : 21.76 Bid-YTW : 4.34 % |

| CM.PR.O | FixedReset | 2.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 18.89 Evaluated at bid price : 18.89 Bid-YTW : 4.23 % |

| BAM.PF.B | FixedReset | 2.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 19.77 Evaluated at bid price : 19.77 Bid-YTW : 4.43 % |

| TRP.PR.G | FixedReset | 2.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 20.26 Evaluated at bid price : 20.26 Bid-YTW : 4.62 % |

| PWF.PR.T | FixedReset | 2.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 22.40 Evaluated at bid price : 22.95 Bid-YTW : 3.55 % |

| RY.PR.M | FixedReset | 2.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 19.72 Evaluated at bid price : 19.72 Bid-YTW : 4.36 % |

| W.PR.H | Perpetual-Discount | 2.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 22.69 Evaluated at bid price : 22.93 Bid-YTW : 6.01 % |

| TRP.PR.C | FixedReset | 3.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 12.30 Evaluated at bid price : 12.30 Bid-YTW : 4.58 % |

| BAM.PF.E | FixedReset | 3.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 20.01 Evaluated at bid price : 20.01 Bid-YTW : 4.41 % |

| TRP.PR.E | FixedReset | 3.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 18.86 Evaluated at bid price : 18.86 Bid-YTW : 4.37 % |

| W.PR.J | Perpetual-Discount | 3.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 23.07 Evaluated at bid price : 23.33 Bid-YTW : 6.01 % |

| BAM.PF.A | FixedReset | 3.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 21.22 Evaluated at bid price : 21.22 Bid-YTW : 4.43 % |

| BAM.PR.C | Floater | 4.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 10.70 Evaluated at bid price : 10.70 Bid-YTW : 4.42 % |

| TRP.PR.D | FixedReset | 4.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 18.20 Evaluated at bid price : 18.20 Bid-YTW : 4.46 % |

| TRP.PR.F | FloatingReset | 5.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 13.60 Evaluated at bid price : 13.60 Bid-YTW : 4.38 % |

| BAM.PR.B | Floater | 5.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 10.75 Evaluated at bid price : 10.75 Bid-YTW : 4.40 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BIP.PR.B | FixedReset | 54,030 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 22.74 Evaluated at bid price : 23.91 Bid-YTW : 5.75 % |

| RY.PR.Z | FixedReset | 45,450 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 4.20 % |

| RY.PR.Q | FixedReset | 25,850 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-24 Maturity Price : 25.00 Evaluated at bid price : 25.70 Bid-YTW : 4.97 % |

| CM.PR.O | FixedReset | 21,434 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 18.89 Evaluated at bid price : 18.89 Bid-YTW : 4.23 % |

| RY.PR.H | FixedReset | 17,941 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-29 Maturity Price : 18.99 Evaluated at bid price : 18.99 Bid-YTW : 4.19 % |

| MFC.PR.G | FixedReset | 16,000 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 5.43 % |

| There were 3 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.T | FixedReset | Quote: 22.95 – 24.99 Spot Rate : 2.0400 Average : 1.4856 YTW SCENARIO |

| NA.PR.W | FixedReset | Quote: 18.02 – 18.70 Spot Rate : 0.6800 Average : 0.4352 YTW SCENARIO |

| CIU.PR.C | FixedReset | Quote: 12.33 – 13.46 Spot Rate : 1.1300 Average : 0.8966 YTW SCENARIO |

| SLF.PR.J | FloatingReset | Quote: 13.20 – 13.80 Spot Rate : 0.6000 Average : 0.3849 YTW SCENARIO |

| HSE.PR.A | FixedReset | Quote: 12.15 – 12.68 Spot Rate : 0.5300 Average : 0.3188 YTW SCENARIO |

| TRP.PR.B | FixedReset | Quote: 12.10 – 12.60 Spot Rate : 0.5000 Average : 0.3208 YTW SCENARIO |