The Russians are bringing us new trends in financial computer hacking:

A group of Russian hackers infiltrated the servers of Dow Jones & Co., owner of the Wall Street Journal and several other news publications, and stole information to trade on before it became public, according to four people familiar with the matter.

The Federal Bureau of Investigation, Secret Service and the Securities and Exchange Commission are leading an investigation of the infiltration, according to the people. The probe began at least a year ago, one of them said.

Dow Jones, in a statement, said: “To the best of our knowledge, we have received no information from the authorities about any such alleged matter, and we are looking into whether there is any truth whatsoever to this report by a competitor news organization.”

…

Information embargoed by companies and the government for release at a later time could be valuable to traders looking to gain an edge over other market participants, as could stories being prepared on topics like mergers and acquisitions that move stock prices.

…

The hack investigation shows how quickly law enforcers are shifting to a new front in insider trading: cyberspace. Market-moving, nonpublic information used to trade hands in secret meetings. Hackers are now stealing sensitive information and selling it to traders. This new vulnerability in the financial markets is challenging law-enforcement officials who are trying to keep pace with cyber-criminals’ rapidly evolving moneymaking schemes.For would-be inside traders, business journalists and data providers are a rich target. Potentially market-moving scoops often develop in-house for days or weeks, promising intruders a long pre-publication window to mine information and execute trades. Data being held for public release at a specified time can also be a gold mine in markets where the profitably of a trade is determined in a fraction of a second.

Life got a little better for preferred share investors today:

Click for Big

It was a glorious day for the Canadian preferred share market, with PerpetualDiscounts gaining 32bp, FixedResets winning 142bp and DeemedRetractibles up 120bp. The Performance Highlights table is as lengthy as one might expect. Volume was extremely heavy.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

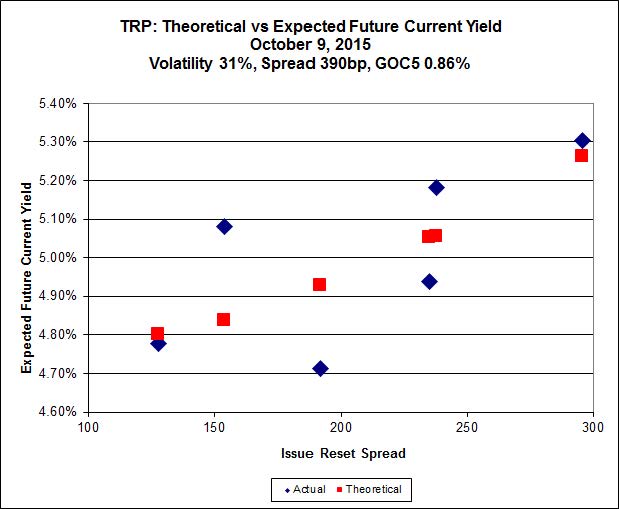

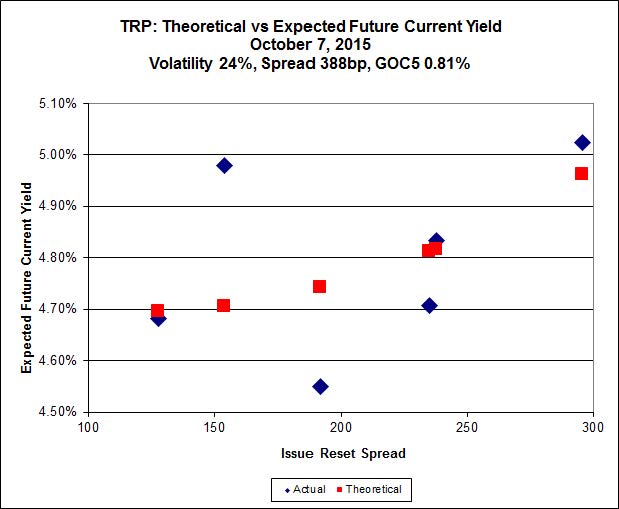

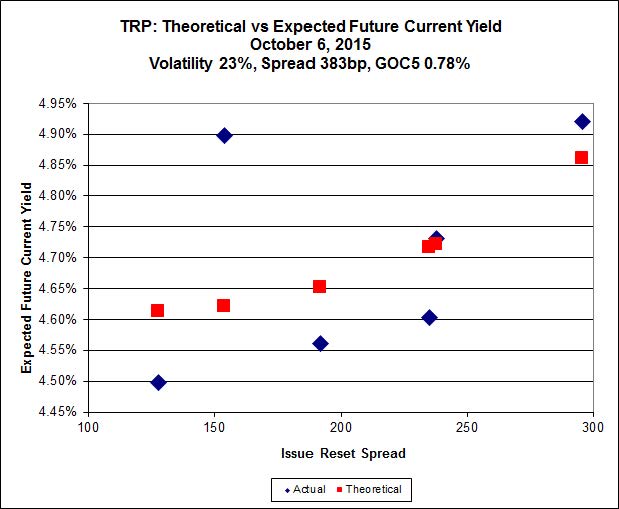

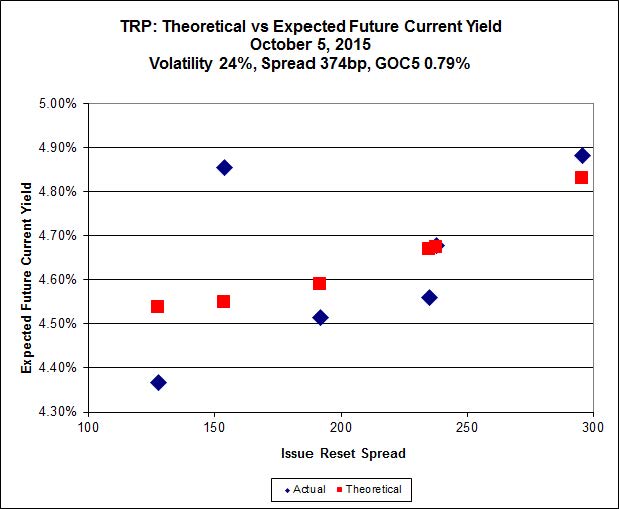

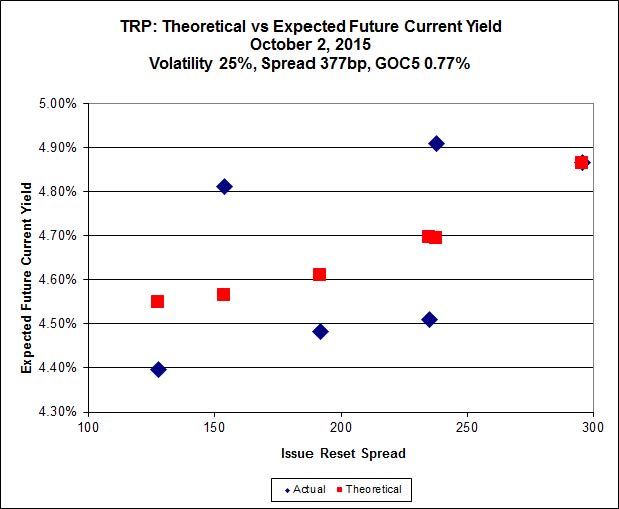

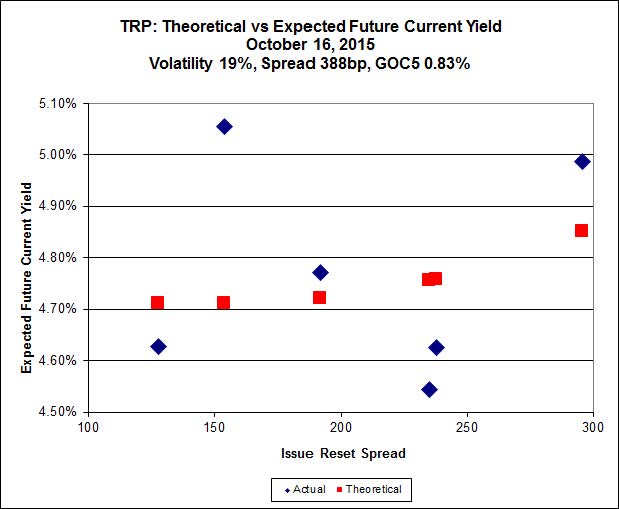

Here’s TRP:

Click for Big

Implied Volatility declined a lot today but remains high.

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.50 to be $0.78 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.86 cheap at its bid price of 11.72.

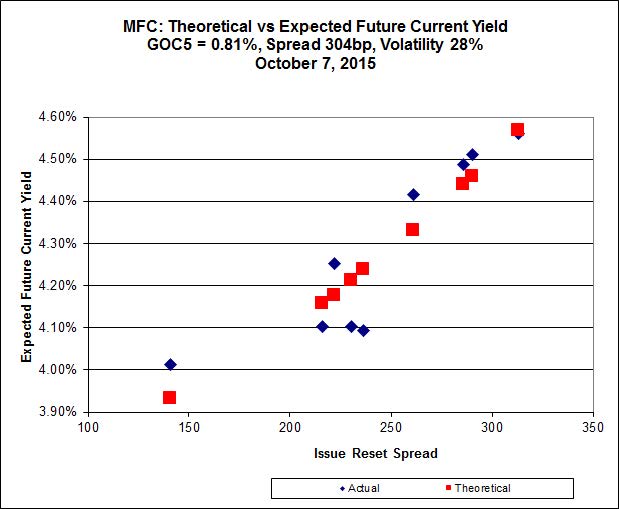

Click for Big

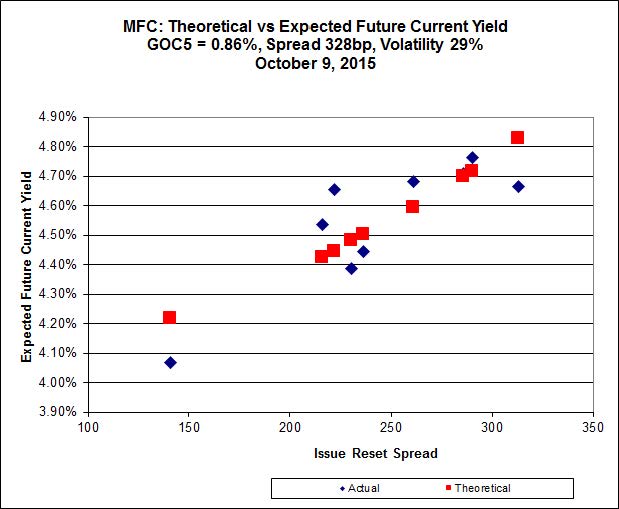

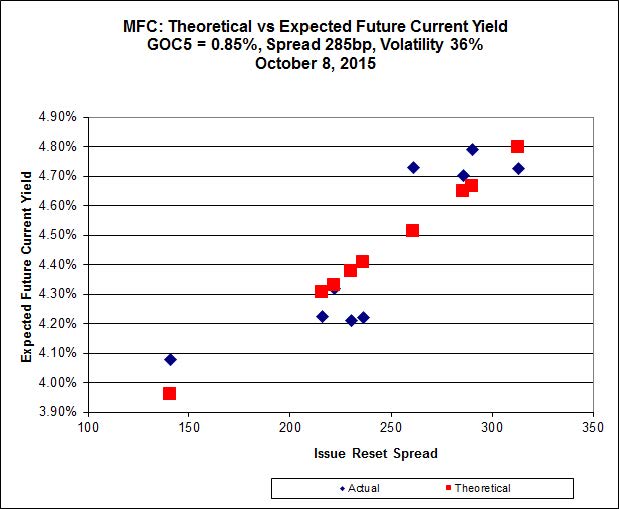

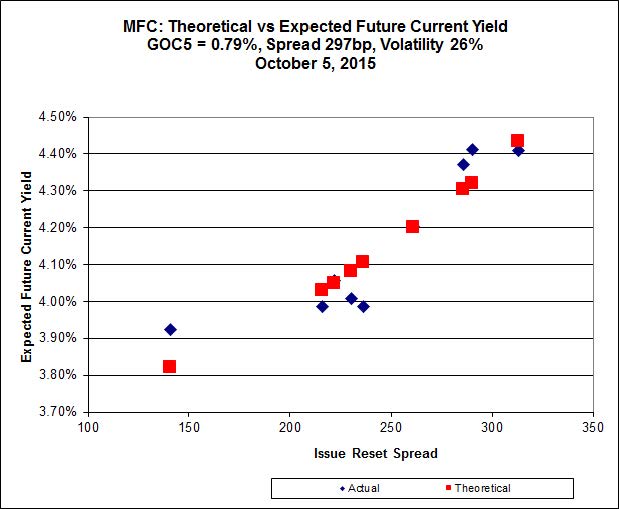

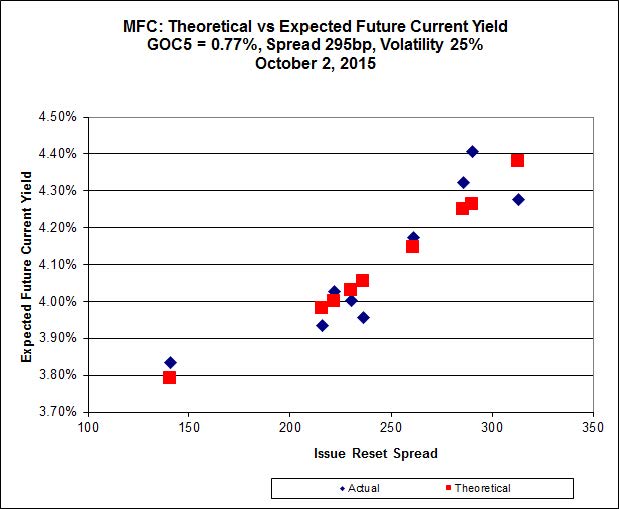

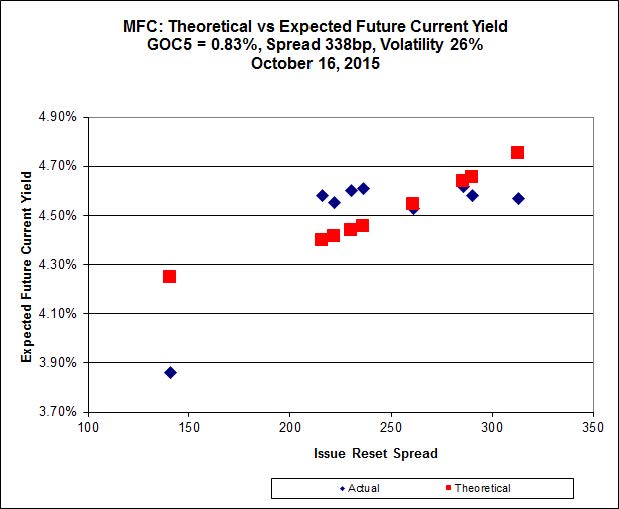

There was an incredible drop in Implied Volatility today – and it would be near zero if the calculation wasn’t distorted by the MFC.PR.F outlier. Dropping the outlier results in a very good fit:

Click for Big

Using the all-inclusive fit, the most expensive is MFC.PR.F, resetting at +141bp on 2016-6-19, bid at 14.50 to be 1.32 rich, while MFC.PR.L resetting at +216bp on 2019-6-19, is bid at 16.32 to be 0.68 cheap.

Click for Big

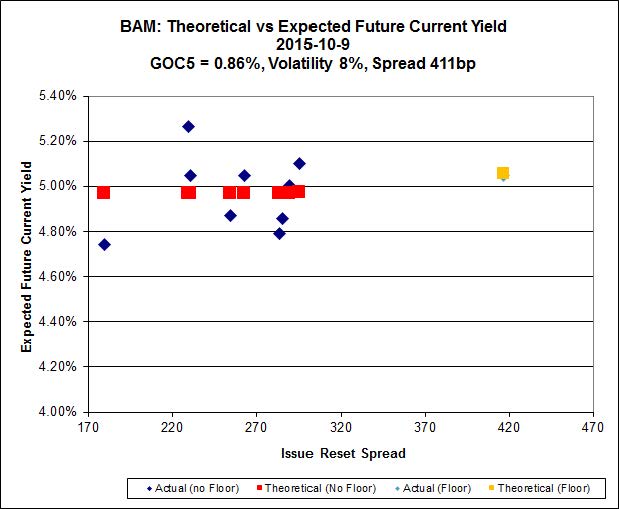

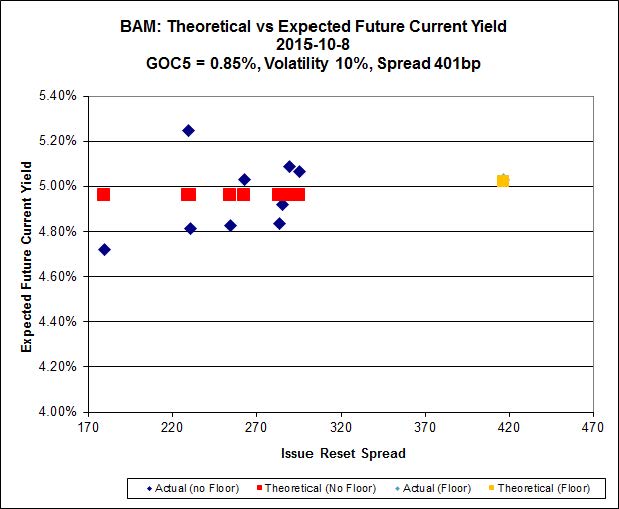

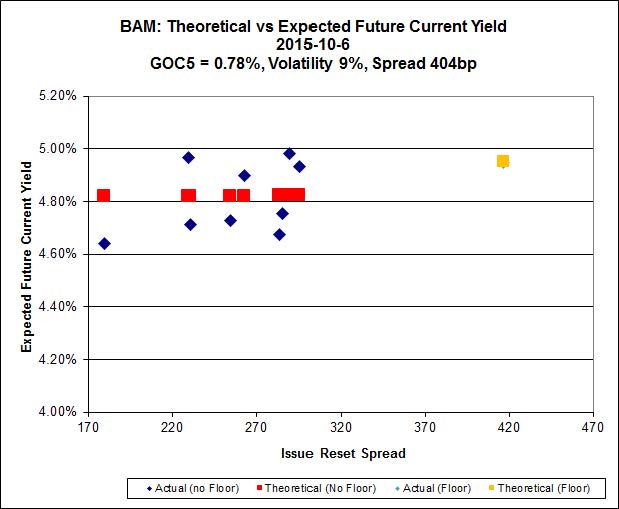

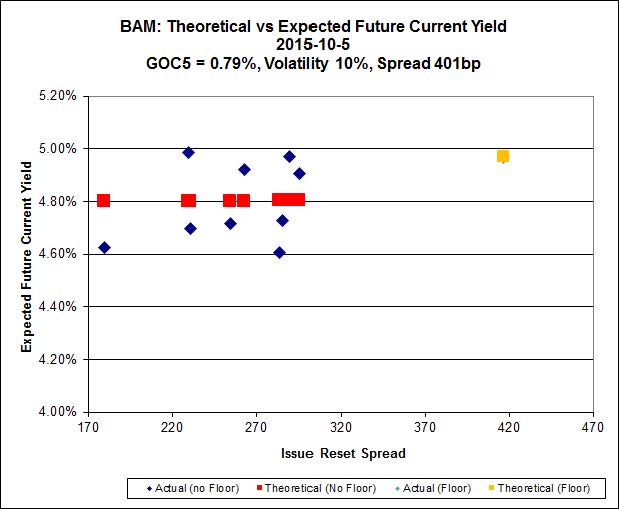

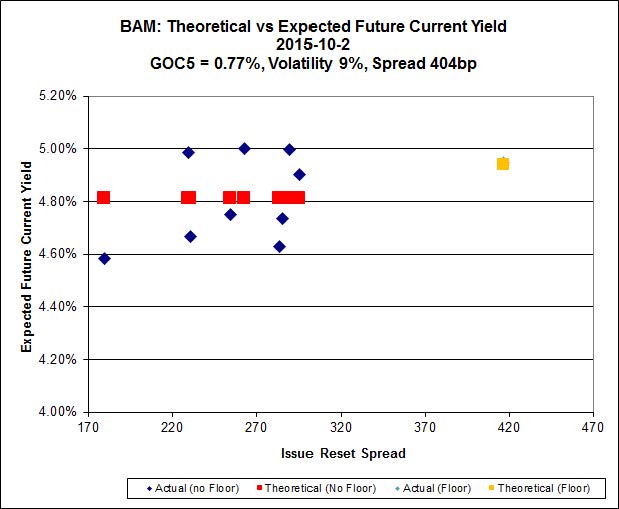

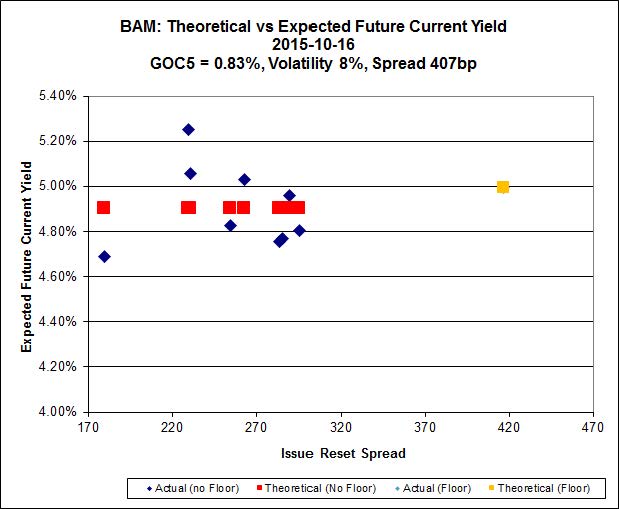

The fit on the BAM issues continues to be horrible!

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 14.90 to be $0.90 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 19.30 and appears to be $0.58 rich.

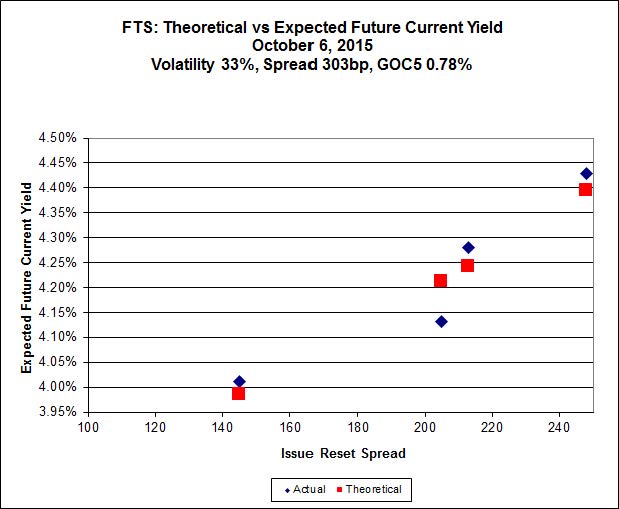

Click for Big

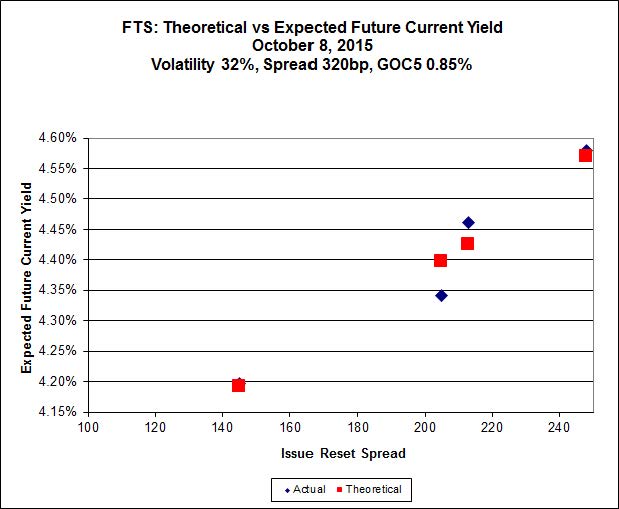

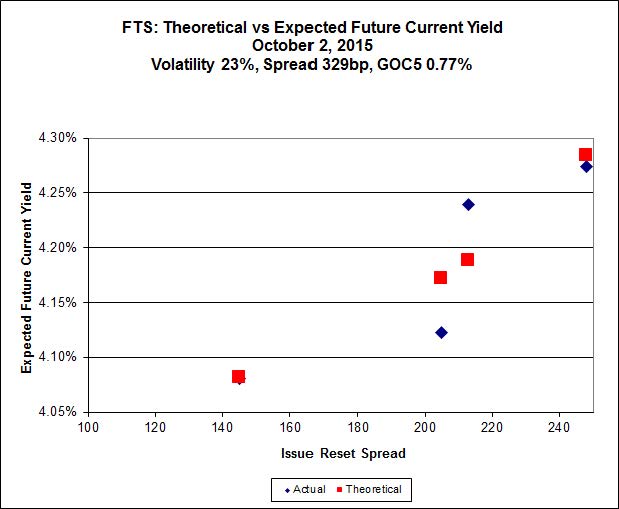

Implied Volatility declined substantially today but remains ridiculously high.

FTS.PR.M, with a spread of +248bp, and bid at 18.60, looks $0.39 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 16.24 and is $0.56 cheap.

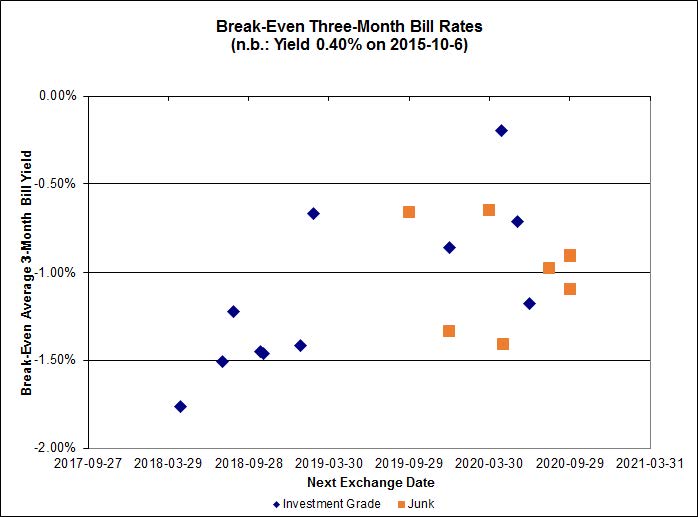

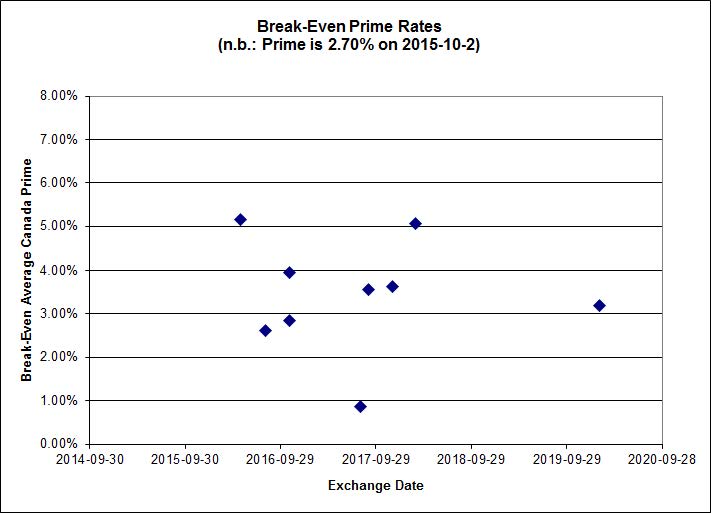

Click for Big

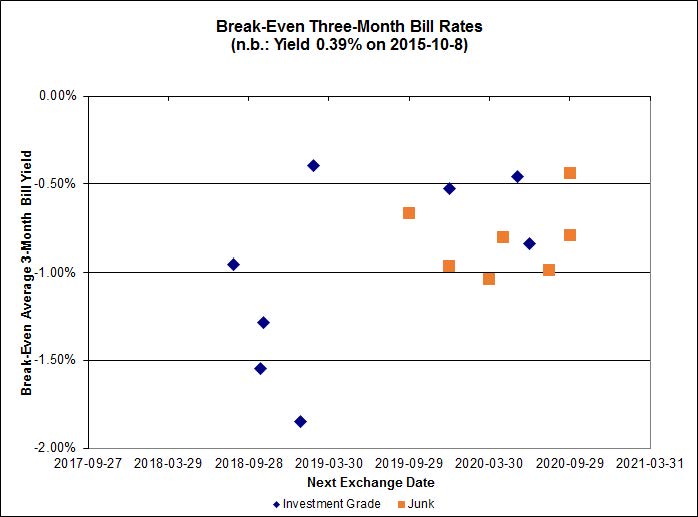

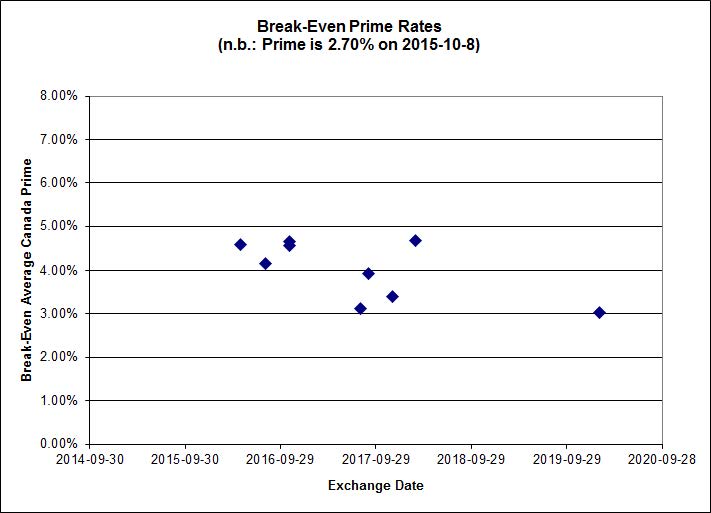

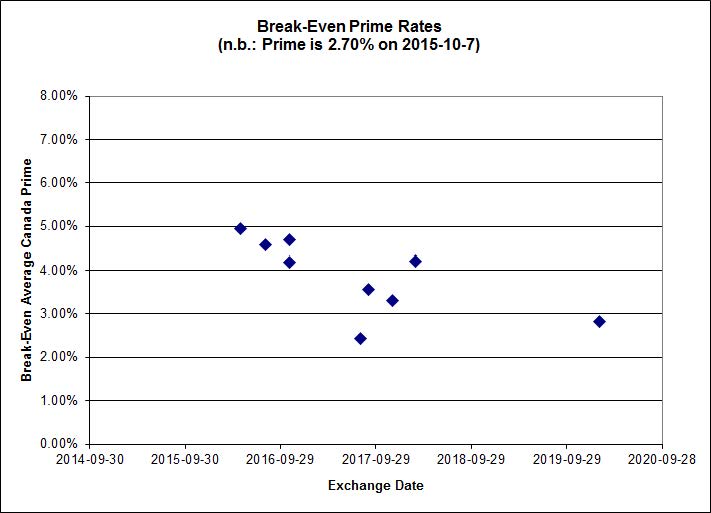

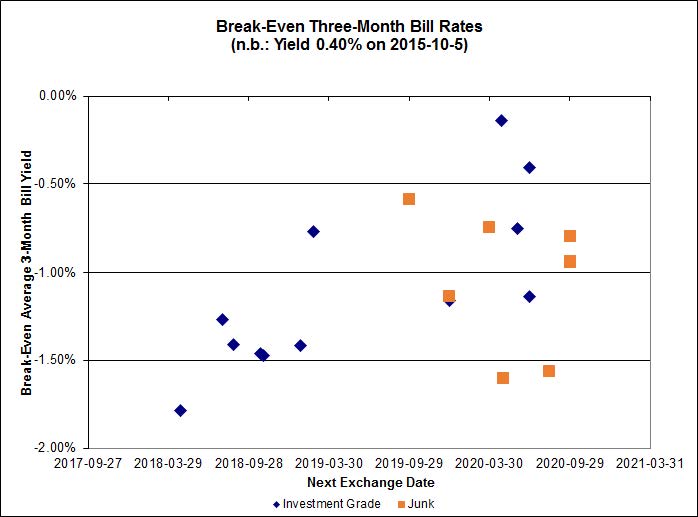

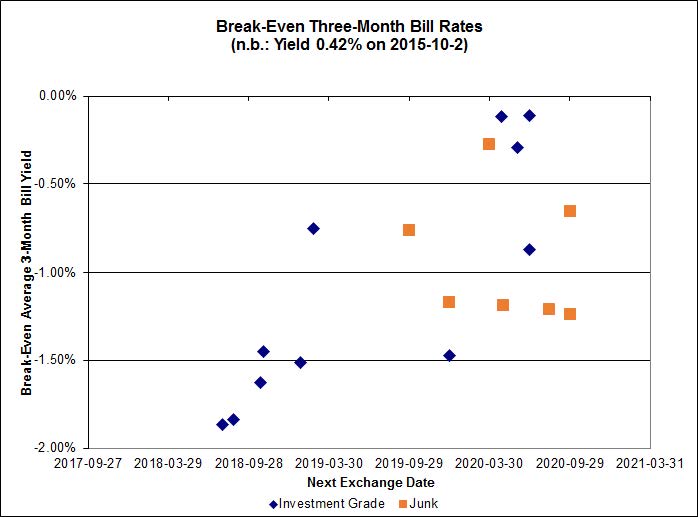

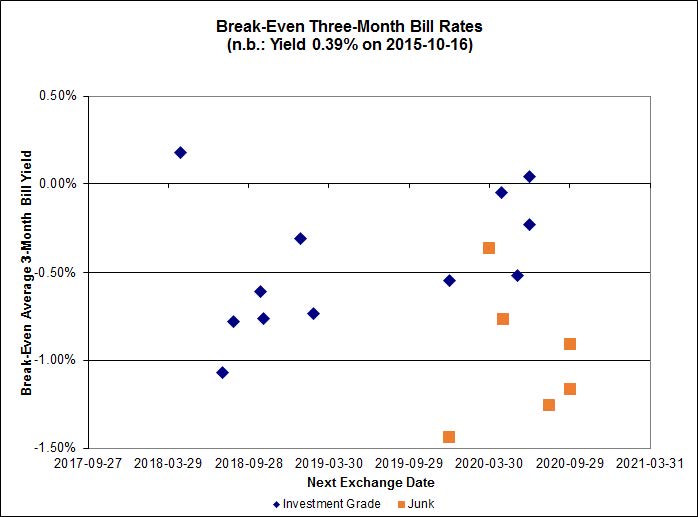

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.45%, with no outliers. The distribution is only slightly bimodal, with bank NVCC non-compliant pairs averaging -0.58% and other issues averaging -0.26%. There are three junk outliers above 0.50% and one below -1.50%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 4.0721 % | 1,633.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 4.0721 % | 2,856.9 |

| Floater | 4.55 % | 4.60 % | 62,771 | 16.24 | 3 | 4.0721 % | 1,737.0 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2505 % | 2,761.6 |

| SplitShare | 4.34 % | 5.14 % | 74,724 | 2.98 | 5 | -0.2505 % | 3,236.4 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2505 % | 2,525.2 |

| Perpetual-Premium | 5.98 % | 5.98 % | 68,243 | 13.96 | 5 | 0.4173 % | 2,435.4 |

| Perpetual-Discount | 5.78 % | 5.86 % | 80,238 | 14.10 | 33 | 0.3217 % | 2,466.1 |

| FixedReset | 5.38 % | 4.92 % | 199,722 | 15.09 | 76 | 1.4250 % | 1,896.9 |

| Deemed-Retractible | 5.28 % | 5.22 % | 103,083 | 5.46 | 33 | 1.1972 % | 2,523.5 |

| FloatingReset | 2.66 % | 4.77 % | 69,057 | 5.81 | 9 | 0.5348 % | 2,045.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BNS.PR.R | FixedReset | -1.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.76 Bid-YTW : 5.01 % |

| BNS.PR.D | FloatingReset | -1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.02 Bid-YTW : 6.89 % |

| BAM.PF.B | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 17.20 Evaluated at bid price : 17.20 Bid-YTW : 5.34 % |

| GWO.PR.P | Deemed-Retractible | 1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.44 Bid-YTW : 6.38 % |

| RY.PR.Z | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 17.29 Evaluated at bid price : 17.29 Bid-YTW : 4.78 % |

| HSB.PR.C | Deemed-Retractible | 1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.95 Bid-YTW : 5.21 % |

| IGM.PR.B | Perpetual-Premium | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 24.41 Evaluated at bid price : 24.70 Bid-YTW : 5.98 % |

| RY.PR.G | Deemed-Retractible | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.94 Bid-YTW : 4.69 % |

| RY.PR.E | Deemed-Retractible | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.90 Bid-YTW : 4.72 % |

| RY.PR.C | Deemed-Retractible | 1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.90 Bid-YTW : 4.82 % |

| PWF.PR.S | Perpetual-Discount | 1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 5.74 % |

| MFC.PR.N | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.01 Bid-YTW : 8.68 % |

| HSB.PR.D | Deemed-Retractible | 1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.81 Bid-YTW : 5.22 % |

| FTS.PR.G | FixedReset | 1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 16.24 Evaluated at bid price : 16.24 Bid-YTW : 4.90 % |

| GWO.PR.G | Deemed-Retractible | 1.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.56 Bid-YTW : 6.70 % |

| TD.PF.A | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 17.25 Evaluated at bid price : 17.25 Bid-YTW : 4.76 % |

| BAM.PR.R | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 14.90 Evaluated at bid price : 14.90 Bid-YTW : 5.48 % |

| BMO.PR.W | FixedReset | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 4.84 % |

| HSE.PR.A | FixedReset | 1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 13.35 Evaluated at bid price : 13.35 Bid-YTW : 5.01 % |

| CM.PR.P | FixedReset | 1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 17.15 Evaluated at bid price : 17.15 Bid-YTW : 4.77 % |

| SLF.PR.H | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.34 Bid-YTW : 8.70 % |

| TRP.PR.E | FixedReset | 1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 4.93 % |

| BNS.PR.A | FloatingReset | 1.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.30 Bid-YTW : 4.33 % |

| GWO.PR.N | FixedReset | 1.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.91 Bid-YTW : 9.59 % |

| RY.PR.J | FixedReset | 1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 18.66 Evaluated at bid price : 18.66 Bid-YTW : 4.90 % |

| IFC.PR.C | FixedReset | 1.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.95 Bid-YTW : 8.02 % |

| BAM.PF.E | FixedReset | 1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 17.51 Evaluated at bid price : 17.51 Bid-YTW : 5.29 % |

| TRP.PR.B | FixedReset | 1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 11.40 Evaluated at bid price : 11.40 Bid-YTW : 4.74 % |

| FTS.PR.K | FixedReset | 1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 16.40 Evaluated at bid price : 16.40 Bid-YTW : 4.82 % |

| BNS.PR.M | Deemed-Retractible | 1.80 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.85 Bid-YTW : 4.60 % |

| CU.PR.C | FixedReset | 1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 18.74 Evaluated at bid price : 18.74 Bid-YTW : 4.50 % |

| GWO.PR.H | Deemed-Retractible | 1.88 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.70 Bid-YTW : 6.87 % |

| TD.PF.D | FixedReset | 1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 19.01 Evaluated at bid price : 19.01 Bid-YTW : 4.80 % |

| TRP.PR.F | FloatingReset | 1.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 12.80 Evaluated at bid price : 12.80 Bid-YTW : 4.55 % |

| RY.PR.H | FixedReset | 2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 17.38 Evaluated at bid price : 17.38 Bid-YTW : 4.80 % |

| BNS.PR.L | Deemed-Retractible | 2.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.85 Bid-YTW : 4.60 % |

| BAM.PF.A | FixedReset | 2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 5.21 % |

| BAM.PF.F | FixedReset | 2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 19.35 Evaluated at bid price : 19.35 Bid-YTW : 5.07 % |

| TD.PF.E | FixedReset | 2.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 19.82 Evaluated at bid price : 19.82 Bid-YTW : 4.71 % |

| TRP.PR.A | FixedReset | 2.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 14.41 Evaluated at bid price : 14.41 Bid-YTW : 5.08 % |

| SLF.PR.B | Deemed-Retractible | 2.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.17 Bid-YTW : 7.16 % |

| BAM.PR.C | Floater | 2.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 10.13 Evaluated at bid price : 10.13 Bid-YTW : 4.70 % |

| GWO.PR.R | Deemed-Retractible | 2.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.54 Bid-YTW : 6.92 % |

| NA.PR.Q | FixedReset | 2.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.51 Bid-YTW : 4.53 % |

| POW.PR.G | Perpetual-Discount | 2.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 23.63 Evaluated at bid price : 24.09 Bid-YTW : 5.83 % |

| SLF.PR.D | Deemed-Retractible | 2.56 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.05 Bid-YTW : 7.52 % |

| FTS.PR.J | Perpetual-Discount | 2.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 20.83 Evaluated at bid price : 20.83 Bid-YTW : 5.79 % |

| MFC.PR.C | Deemed-Retractible | 2.56 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.01 Bid-YTW : 7.63 % |

| CM.PR.Q | FixedReset | 2.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 19.65 Evaluated at bid price : 19.65 Bid-YTW : 4.64 % |

| RY.PR.M | FixedReset | 2.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 18.42 Evaluated at bid price : 18.42 Bid-YTW : 4.84 % |

| MFC.PR.K | FixedReset | 2.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.75 Bid-YTW : 8.68 % |

| BAM.PR.X | FixedReset | 2.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 14.02 Evaluated at bid price : 14.02 Bid-YTW : 5.12 % |

| SLF.PR.E | Deemed-Retractible | 2.75 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.18 Bid-YTW : 7.49 % |

| SLF.PR.A | Deemed-Retractible | 2.76 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.21 Bid-YTW : 7.08 % |

| FTS.PR.M | FixedReset | 2.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 18.60 Evaluated at bid price : 18.60 Bid-YTW : 4.79 % |

| SLF.PR.C | Deemed-Retractible | 2.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.86 Bid-YTW : 7.65 % |

| BAM.PR.K | Floater | 2.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 10.35 Evaluated at bid price : 10.35 Bid-YTW : 4.60 % |

| TRP.PR.G | FixedReset | 3.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 5.09 % |

| MFC.PR.I | FixedReset | 3.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.98 Bid-YTW : 6.93 % |

| BAM.PR.Z | FixedReset | 3.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 19.72 Evaluated at bid price : 19.72 Bid-YTW : 5.06 % |

| MFC.PR.J | FixedReset | 3.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.00 Bid-YTW : 7.31 % |

| SLF.PR.G | FixedReset | 3.42 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.50 Bid-YTW : 9.11 % |

| VNR.PR.A | FixedReset | 3.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.96 % |

| BMO.PR.T | FixedReset | 3.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 17.51 Evaluated at bid price : 17.51 Bid-YTW : 4.74 % |

| PWF.PR.T | FixedReset | 4.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 20.35 Evaluated at bid price : 20.35 Bid-YTW : 4.18 % |

| TRP.PR.D | FixedReset | 4.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 17.35 Evaluated at bid price : 17.35 Bid-YTW : 4.90 % |

| SLF.PR.I | FixedReset | 4.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.07 Bid-YTW : 7.33 % |

| MFC.PR.G | FixedReset | 5.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.35 Bid-YTW : 6.64 % |

| MFC.PR.H | FixedReset | 6.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.67 Bid-YTW : 6.07 % |

| BMO.PR.Y | FixedReset | 6.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 20.25 Evaluated at bid price : 20.25 Bid-YTW : 4.61 % |

| BAM.PR.B | Floater | 6.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 10.70 Evaluated at bid price : 10.70 Bid-YTW : 4.45 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| PWF.PR.F | Perpetual-Discount | 283,400 | Nesbitt crossed blocks of 238,000 and 40,000, both at 22.40. Nice tickets! YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 22.01 Evaluated at bid price : 22.25 Bid-YTW : 5.91 % |

| PWF.PR.O | Perpetual-Premium | 190,856 | Nesbitt crossed 176,700 at 24.36. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 24.03 Evaluated at bid price : 24.33 Bid-YTW : 5.97 % |

| BAM.PF.A | FixedReset | 160,376 | Scotia crossed two blocks of 50,000 each, both at 18.58, and a block of 40,000 at 18.70. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 5.21 % |

| RY.PR.H | FixedReset | 125,541 | Scotia crossed 42,200 at 17.25 and sold 14,100 to RBC at 17.40. RBC bought 11,900 from TD at 17.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 17.38 Evaluated at bid price : 17.38 Bid-YTW : 4.80 % |

| TRP.PR.E | FixedReset | 118,299 | Desjardins crossed 103,400 at 17.85. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 4.93 % |

| RY.PR.J | FixedReset | 98,436 | Scotia crossed 47,500 at 18.60. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-16 Maturity Price : 18.66 Evaluated at bid price : 18.66 Bid-YTW : 4.90 % |

| There were 67 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| IFC.PR.A | FixedReset | Quote: 14.65 – 15.98 Spot Rate : 1.3300 Average : 0.7704 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 19.00 – 19.92 Spot Rate : 0.9200 Average : 0.5750 YTW SCENARIO |

| IAG.PR.G | FixedReset | Quote: 19.10 – 19.93 Spot Rate : 0.8300 Average : 0.5138 YTW SCENARIO |

| CU.PR.C | FixedReset | Quote: 18.74 – 19.50 Spot Rate : 0.7600 Average : 0.4628 YTW SCENARIO |

| PWF.PR.P | FixedReset | Quote: 14.11 – 14.85 Spot Rate : 0.7400 Average : 0.4857 YTW SCENARIO |

| GWO.PR.S | Deemed-Retractible | Quote: 23.29 – 23.95 Spot Rate : 0.6600 Average : 0.4104 YTW SCENARIO |